Self-employed professionals face unique challenges when building retirement savings. Without employer-sponsored plans, you must take full control of your financial future.

We at Clear View Business Solutions see many entrepreneurs struggle with retirement planning for self-employed individuals. The good news is that several powerful retirement vehicles offer higher contribution limits than traditional employee plans.

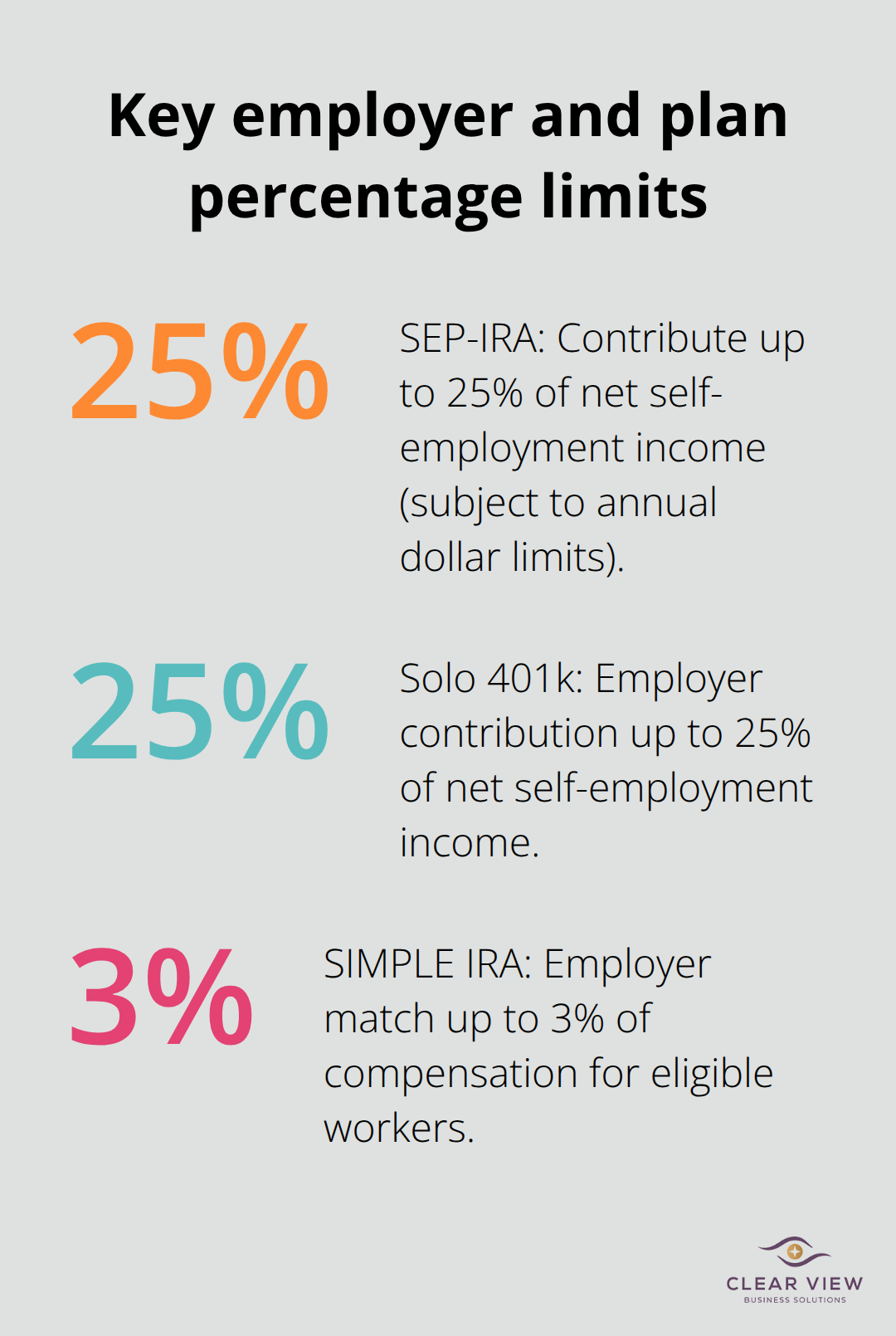

The SEP-IRA stands out as the most straightforward option for self-employed professionals who want maximum contribution flexibility. You can contribute up to 25% of your net self-employment income or $69,000 for 2024 (whichever amount is lower). The IRS allows contributions until your tax deadline, which includes extensions, so you have time to assess your annual income before you commit funds.

You can establish a SEP-IRA with only a simple one-page Form 5305-SEP, which makes it the fastest retirement plan to set up. The major advantage lies in its scalability – if you hire employees later, you must contribute equally for all eligible workers, but this creates a powerful recruitment tool.

The Solo 401k allows you to contribute as both employer and employee, which helps you reach the same $69,000 limit for 2024 through different mechanisms. You can defer up to $23,500 in salary deferrals plus employer contributions of up to 25% of net income. Workers aged 50 and older gain an additional $8,000 catch-up contribution, which brings their total to $77,000.

This plan works exclusively for businesses without employees, so it fits perfectly for independent contractors and single-member LLCs. The Solo 401k also permits loans against your balance, which provides access to funds during emergencies without penalties.

SIMPLE IRAs work best for small businesses with employees who want shared retirement benefits. The 2025 contribution limit reaches $16,500 for employee deferrals, with employers required to match up to 3% of compensation or provide a flat 2% contribution for all eligible workers.

This plan requires less administrative burden than traditional 401k plans while it still offers meaningful retirement savings.

Workers over 50 can add $3,500 in catch-up contributions. The mandatory employer match makes this option expensive if you have multiple employees, but it creates strong employee retention benefits for businesses that want to grow.

These contribution limits represent just the foundation of smart retirement tax strategy. The real power comes from how you time these contributions to minimize your current tax burden while you maximize long-term growth potential.

Self-employed professionals must master the art of retirement contribution timing to slash their tax burden. The IRS allows SEP-IRA and Solo 401k contributions until your tax filing deadline (including extensions), which means you can wait until April or October to make your full year contribution. This flexibility lets you calculate your exact net income before you commit funds, but smart timing goes deeper than just meeting deadlines.

Early retirement contributions deliver compound benefits that most self-employed individuals miss. When you front-load contributions using a SEP IRA or Solo 401(k), you can make large contributions that are fully deductible. More importantly, large early contributions reduce your quarterly estimated tax payments throughout the year, which improves your cash flow.

The IRS requires estimated payments based on prior year taxes or 90% of current year liability. Retirement contributions made by each quarterly deadline directly reduce that quarter’s payment requirement. This creates immediate cash flow benefits while you build long-term wealth.

Self-employed income fluctuates dramatically, which creates perfect opportunities for Roth conversions during lean years. When your business income drops below $47,150 for single filers in 2024, you remain in the 12% tax bracket. This makes conversions extremely cost-effective compared to waiting until retirement when required minimum distributions might push you into higher brackets.

Convert traditional all or part of your traditional IRA to a Roth IRA and pay regular income taxes on the converted amount during these low-income periods rather than later. The five-year rule requires Roth conversions to age five years before tax-free withdrawals, so start conversions in your 50s to maximize flexibility.

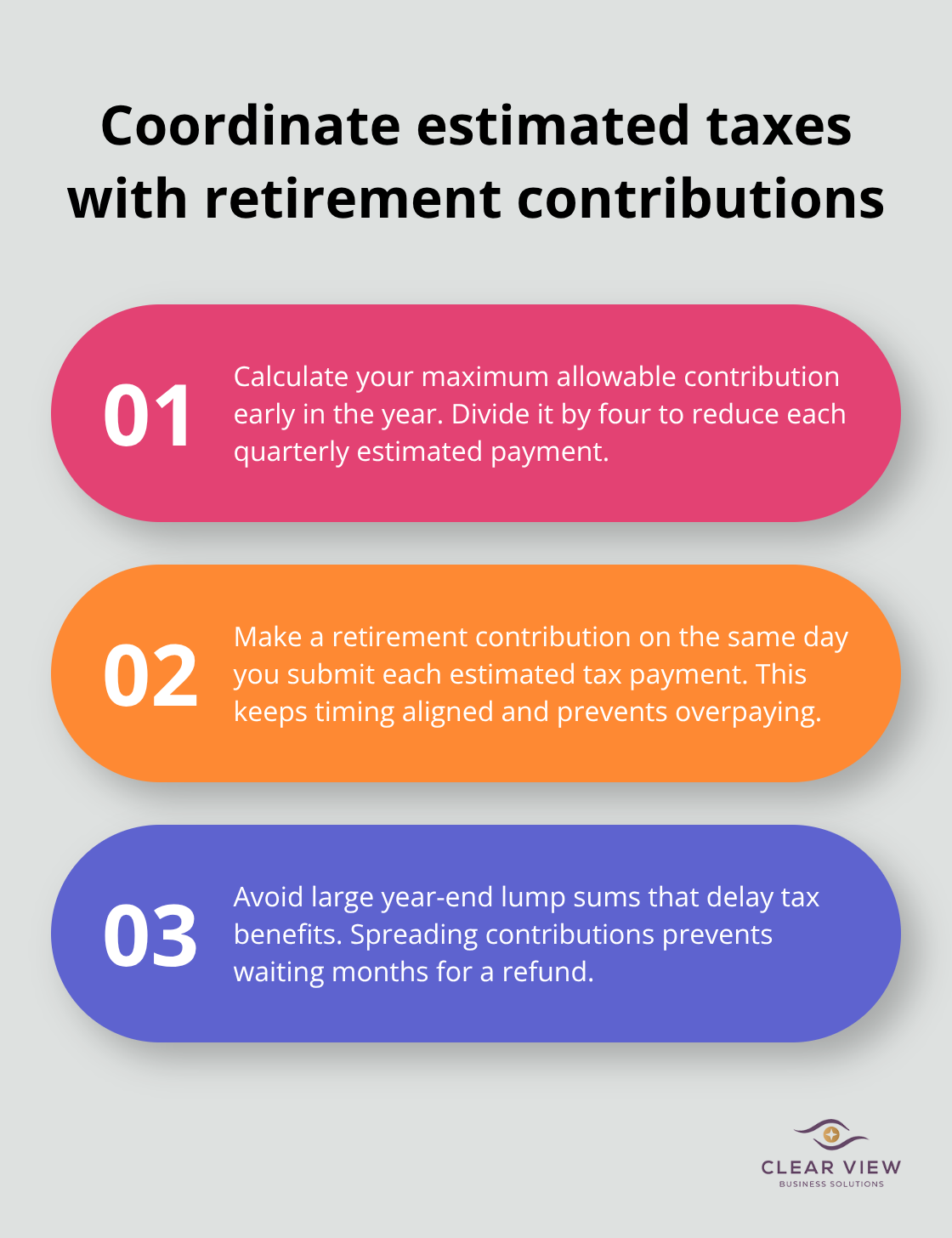

Most self-employed individuals overpay estimated taxes because they fail to account for retirement contributions in their quarterly calculations. Calculate your maximum allowable contribution early in the year, then divide it by four to reduce each quarterly payment proportionally. This strategy prevents the common mistake of making a large December contribution and then waiting months for your tax refund.

The key lies in consistent execution. Make your quarterly retirement contribution on the same day you pay estimated taxes to maintain perfect coordination between tax planning and retirement funding.

This approach transforms retirement savings from an annual burden into a systematic wealth-building process.

However, even the best contribution timing strategy can backfire if you fall into common retirement planning traps that plague self-employed professionals.

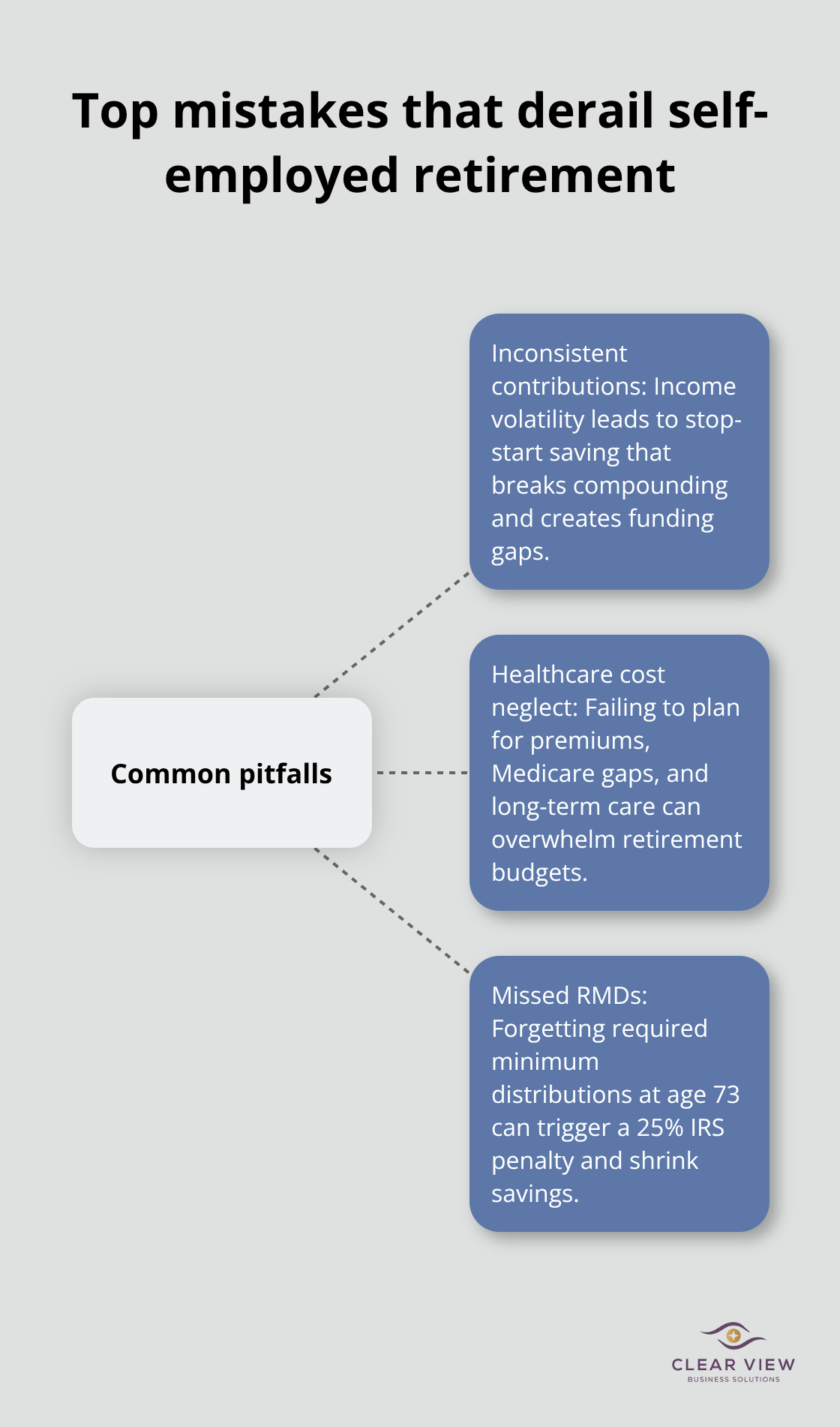

Self-employed professionals sabotage their retirement futures through three devastating mistakes that compound over decades. The most destructive error involves erratic contribution patterns driven by income volatility. When business income drops, most self-employed individuals slash retirement contributions to zero instead of maintaining consistent savings rates.

This stop-start approach destroys the power of compound growth and creates massive gaps in retirement funding.

The solution requires percentage-based contributions rather than fixed dollar amounts. Set your retirement contribution as 15-20% of net income and maintain this rate regardless of earnings fluctuations. During high-income years, your larger contributions create tax deductions that reduce quarterly payments. During lean periods, smaller absolute contributions still maintain your savings discipline.

Fixed-percentage strategies offer predictable income and systematic withdrawals provide flexibility. Automate transfers from your business account to retirement accounts monthly rather than making annual lump-sum decisions that depend on year-end emotions.

The second critical failure involves ignoring healthcare expenses during retirement. Self-employed individuals lose group insurance coverage and face individual market premiums that can exceed $2,000 monthly for couples over 60.

Best practice is to plan for Medicare coverage immediately after losing coverage to prevent any insurance gaps. Medicare covers only 80% of expenses, leaving substantial gaps for dental, vision, and long-term care costs. Health Savings Accounts become retirement goldmines for self-employed professionals because they offer triple tax advantages and penalty-free withdrawals for medical expenses after age 65. Maximize HSA contributions at $4,150 for individuals and $8,300 for families in 2024, then invest these funds aggressively for long-term growth.

The third mistake involves missing required minimum distributions that begin at age 73. The IRS imposes 25% penalties on missed RMD amounts (which can devastate retirement accounts). Self-employed individuals often forget about old SEP-IRAs or Solo 401k accounts from previous business ventures, leading to accidental violations.

Calculate RMDs using IRS life expectancy tables and withdraw amounts by December 31 each year. Consider Roth conversions in your early 60s to reduce future RMD requirements and maintain more control over your tax brackets during retirement.

Retirement planning for self-employed individuals demands strategic decisions and consistent action. The SEP-IRA delivers maximum contribution flexibility at $69,000 for 2024, while Solo 401k plans provide dual contribution advantages for single-member businesses. SIMPLE IRAs work best when you have employees and want shared retirement benefits.

Tax timing becomes your most powerful wealth-creation tool. Front-load contributions to reduce quarterly estimated payments and convert traditional accounts to Roth during low-income years. Maintain percentage-based contributions rather than fixed amounts to survive income volatility and avoid the three critical mistakes that destroy retirement security: inconsistent contribution patterns, healthcare cost neglect, and missed required minimum distributions.

Health Savings Accounts provide triple tax advantages and should be maximized alongside traditional retirement accounts (contribution limits reach $4,150 for individuals and $8,300 for families in 2024). We at Clear View Business Solutions help self-employed professionals navigate complex retirement decisions through our comprehensive financial advisory services. Start these strategies today to build the retirement security you deserve.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.