Are you tired of paying more taxes than necessary? At Clear View Business Solutions, we understand the importance of keeping more money in your pocket.

This guide offers practical tax planning tips for individuals to help reduce your personal tax bill. We’ll explore strategies to maximize deductions, optimize your income, and leverage tax-advantaged accounts.

At Clear View Business Solutions, we know that maximizing deductions and credits is essential to reduce your personal tax bill. Let’s explore effective strategies to help you keep more money in your pocket.

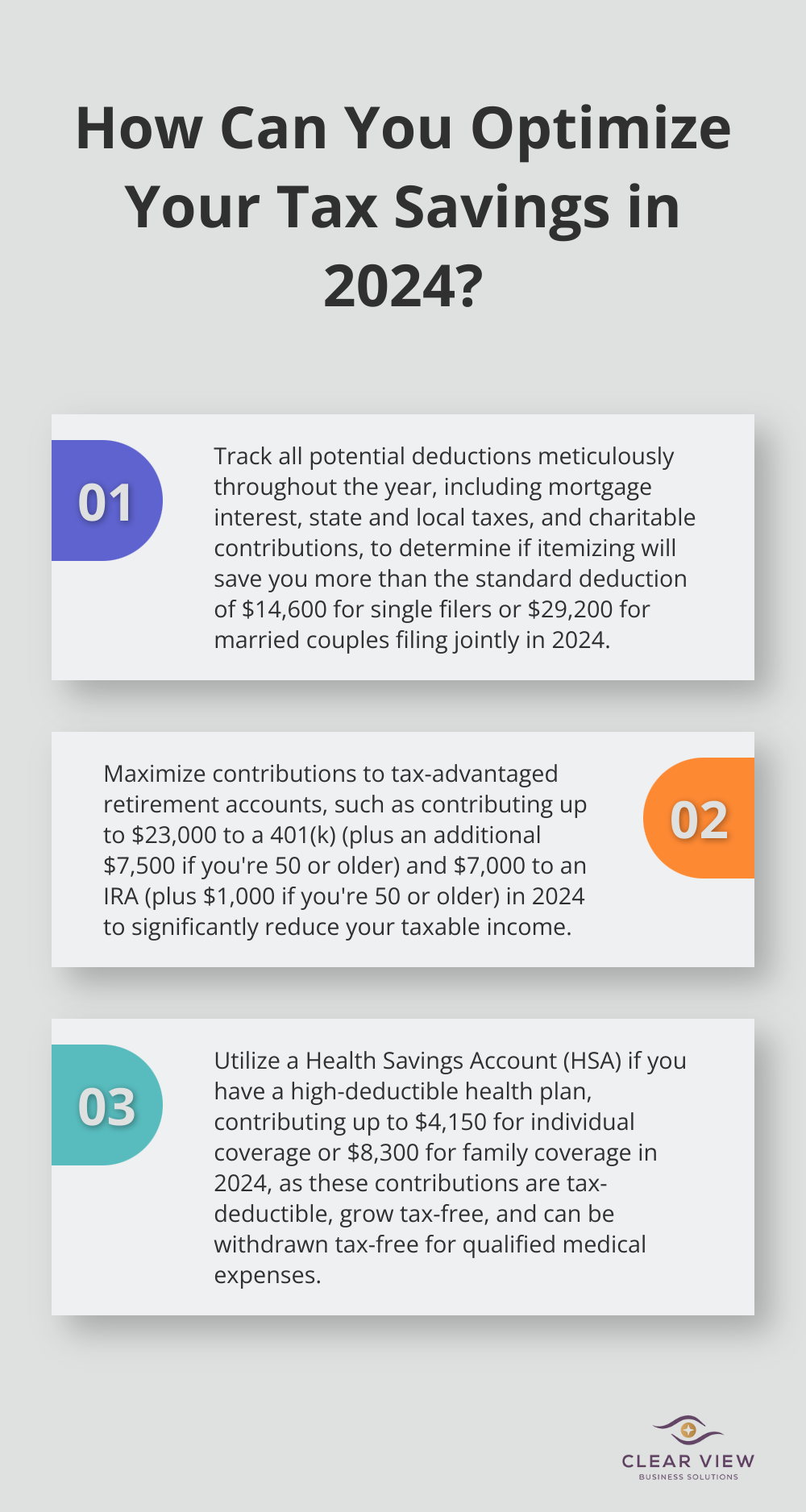

For 2024, the standard deduction is $14,600 for single filers and $29,200 for married couples filing jointly. You should itemize if your deductions exceed these amounts. Common itemized deductions include mortgage interest, state and local taxes (up to $10,000), and charitable contributions. Keep detailed records of these expenses throughout the year to simplify tax preparation.

Tax credits directly reduce your tax bill dollar-for-dollar, making them more valuable than deductions. Some popular credits include:

Contributing to tax-advantaged retirement accounts effectively reduces your taxable income. For 2024, you can contribute up to $23,000 to a 401(k), with an additional $7,500 catch-up contribution if you’re 50 or older. IRA contribution limits are $7,000 (with an extra $1,000 for those 50+). These contributions can significantly lower your taxable income while securing your financial future.

Charitable donations provide substantial tax benefits if you itemize. Consider bunching your donations into a single tax year to surpass the standard deduction threshold. For instance, if you typically donate $5,000 annually, you might donate $10,000 every other year to maximize your deduction.

Another strategy involves donating appreciated assets, such as stocks. This approach allows you to avoid capital gains tax and claim a deduction for the asset’s full market value. For example, if you donate $10,000 worth of stock that you purchased for $5,000, you can deduct $10,000 without paying taxes on the $5,000 gain.

Don’t overlook health-related tax benefits. Contribute to a Health Savings Account (HSA) if you have a high-deductible health plan. For 2024, you can contribute up to $4,150 for individual coverage or $8,300 for family coverage. HSA contributions are tax-deductible, grow tax-free, and can be withdrawn tax-free for qualified medical expenses.

Now that we’ve covered ways to maximize deductions and credits, let’s explore how to optimize your income to further reduce your tax bill.

Timing plays a key role in tax planning. If you’re self-employed or control when you receive income, consider deferring income to the following year if you expect to be in a lower tax bracket. On the flip side, if you anticipate a higher bracket next year, accelerate income into the current year.

For expenses, apply the opposite approach. If you expect a higher tax bracket this year, pay deductible expenses before year-end. This could include paying property taxes early or making an extra mortgage payment to increase your interest deduction.

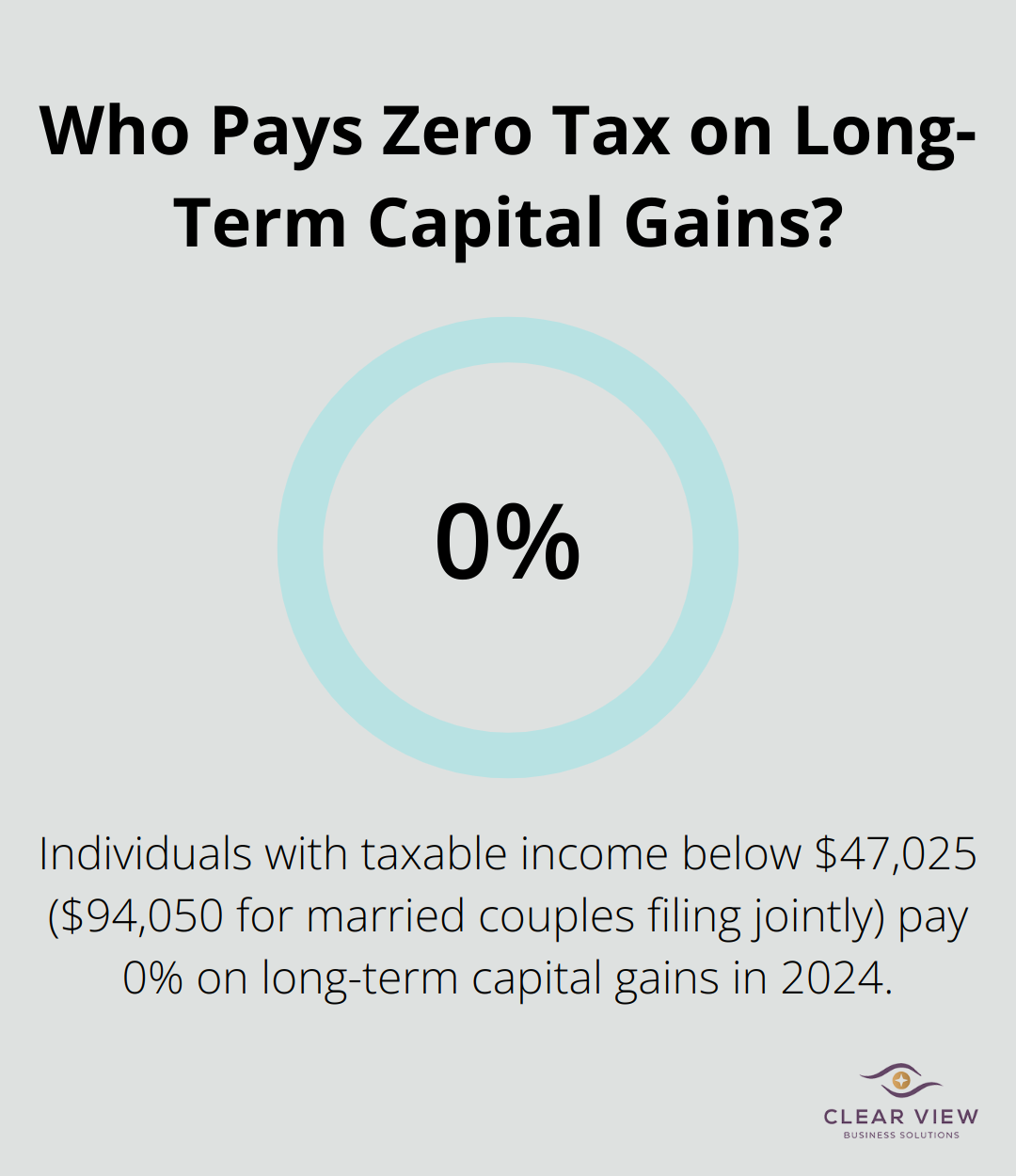

Invest with tax efficiency in mind to reduce your tax burden. Hold investments for more than a year to qualify for long-term capital gains rates, which are typically lower than short-term rates. For 2024, individuals with taxable income below $47,025 ($94,050 for married couples filing jointly) pay 0% on long-term capital gains.

Municipal bonds offer another tax-efficient investment option. The interest from these bonds is often exempt from federal taxes (and sometimes state and local taxes). While yields might be lower than corporate bonds, the tax savings can make them more attractive, especially for high-income earners.

A Roth IRA conversion can serve as a powerful tax planning tool, especially if you expect to be in a higher tax bracket in retirement. Convert traditional IRA funds to a Roth IRA to pay taxes on the converted amount now, but enjoy tax-free future withdrawals. This strategy works particularly well in years when your income is lower than usual.

However, carefully consider the tax implications of a Roth conversion. The converted amount adds to your taxable income for the year, which could push you into a higher tax bracket. A tax professional can help determine if a Roth conversion aligns with your specific financial situation.

Tax-loss harvesting involves selling investments at a loss to offset capital gains. This strategy can help reduce your overall tax liability. For example, by offsetting the capital gains of one investment with the capital loss of another, you could potentially save $7,000 on taxes (assuming a $20,000 gain and a 35% tax rate).

You can also deduct up to $3,000 of net capital losses against your ordinary income each year. Any unused losses carry forward to future tax years, providing ongoing tax benefits.

Optimizing your income for tax savings requires careful planning and consideration of your unique financial situation. While these strategies can prove effective, consult with a tax professional to ensure they align with your overall financial goals. The next chapter will explore how to leverage tax-advantaged accounts to further reduce your tax burden and maximize your savings.

Health Savings Accounts (HSAs) offer one of the most powerful tax-advantaged tools available. In 2024, families can contribute up to $8,300. These contributions are tax-deductible, grow tax-free, and can be withdrawn tax-free for qualified medical expenses. This triple tax advantage is unmatched in the tax code.

If you’re in the 24% tax bracket and max out your HSA contribution as a family, you could save $1,992 in taxes for the year. Over time, these savings compound significantly. Unlike Flexible Spending Accounts (FSAs), HSA funds roll over year to year, which allows for long-term growth.

FSAs provide immediate tax savings on medical and dependent care expenses. In 2024, you can contribute up to $3,200 to a healthcare FSA. These contributions come from pre-tax dollars, which reduces your taxable income. However, FSAs typically have a use-it-or-lose-it policy, so careful planning is essential.

For dependent care, FSAs allow contributions up to $5,000 for couples filing jointly. This can result in substantial tax savings for families with young children or dependent adults who need care.

529 plans serve as excellent vehicles for education savings. While contributions are not federally tax-deductible, many states offer tax deductions or credits for contributions. The primary benefit comes from tax-free growth and tax-free withdrawals for qualified education expenses.

Some states (like New York) offer deductions up to $5,000 per year for single filers and $10,000 for married couples filing jointly. This can lead to significant state tax savings, especially for high-income earners in states with high tax rates.

Cash value life insurance policies (such as whole life or universal life) can function as tax-advantaged savings vehicles. While premiums are not tax-deductible, the cash value grows tax-deferred. You can access this cash value through tax-free loans, which potentially provides a tax-efficient income stream in retirement.

However, these policies are complex and often include high fees. They don’t suit everyone and should only be considered after maxing out more traditional retirement accounts like 401(k)s and IRAs.

Tax-advantaged accounts offer significant benefits, but they require careful planning and consideration of your unique financial situation. A tax professional can help you navigate these options and create a comprehensive tax strategy that maximizes your savings and minimizes your tax burden.

Effective tax planning empowers individuals to reduce their personal tax bill. Tax planning tips for individuals include maximizing deductions, optimizing income, and leveraging tax-advantaged accounts. These strategies can lower your tax burden while securing your financial future.

Your unique financial situation determines the most effective approach for you. We at Clear View Business Solutions offer comprehensive tax services tailored to your individual needs. Our expertise helps navigate complex tax laws, identify savings opportunities, and ensure compliance with all regulations.

Tax planning requires an ongoing process. As tax laws change and your financial situation evolves, your tax strategy should adapt. Regular reviews and adjustments maintain an effective tax plan. Professional guidance helps you make informed decisions that lead to substantial tax savings year after year.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.