Most small business owners spend hours on bookkeeping without understanding what they’re actually doing. Full-cycle bookkeeping is the backbone of financial clarity, yet many companies treat it as an afterthought.

At Clear View Business Solutions, we’ve seen firsthand how proper bookkeeping transforms struggling businesses into financially healthy ones. This guide walks you through everything you need to know to get your finances in order.

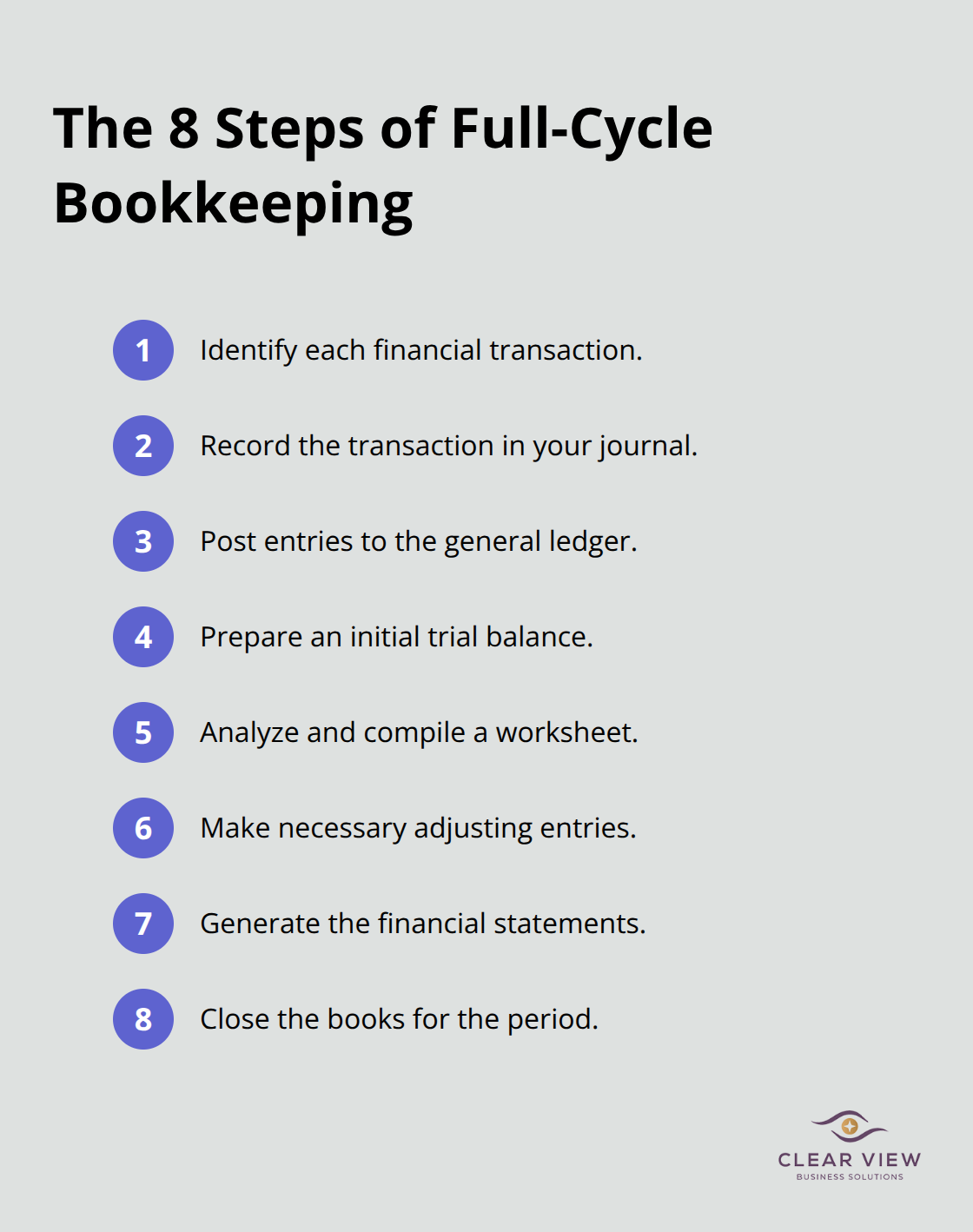

Full-cycle bookkeeping is the complete process of recording, organizing, and closing out your financial transactions from start to finish within an accounting period. It’s not just data entry-it’s an eight-step system that begins when money moves in or out of your business and ends when you generate the financial statements you need to make decisions. The eight steps are identifying transactions, recording them in your journal, posting to the general ledger, preparing a trial balance, analyzing a worksheet, making adjusting entries, generating financial statements, and closing the books. Many small business owners skip steps or do them inconsistently, which creates gaps in their financial picture.

The difference between full-cycle bookkeeping and partial bookkeeping is stark: partial bookkeeping might give you transaction records, but full-cycle bookkeeping gives you accurate, complete financial statements that reflect reality.

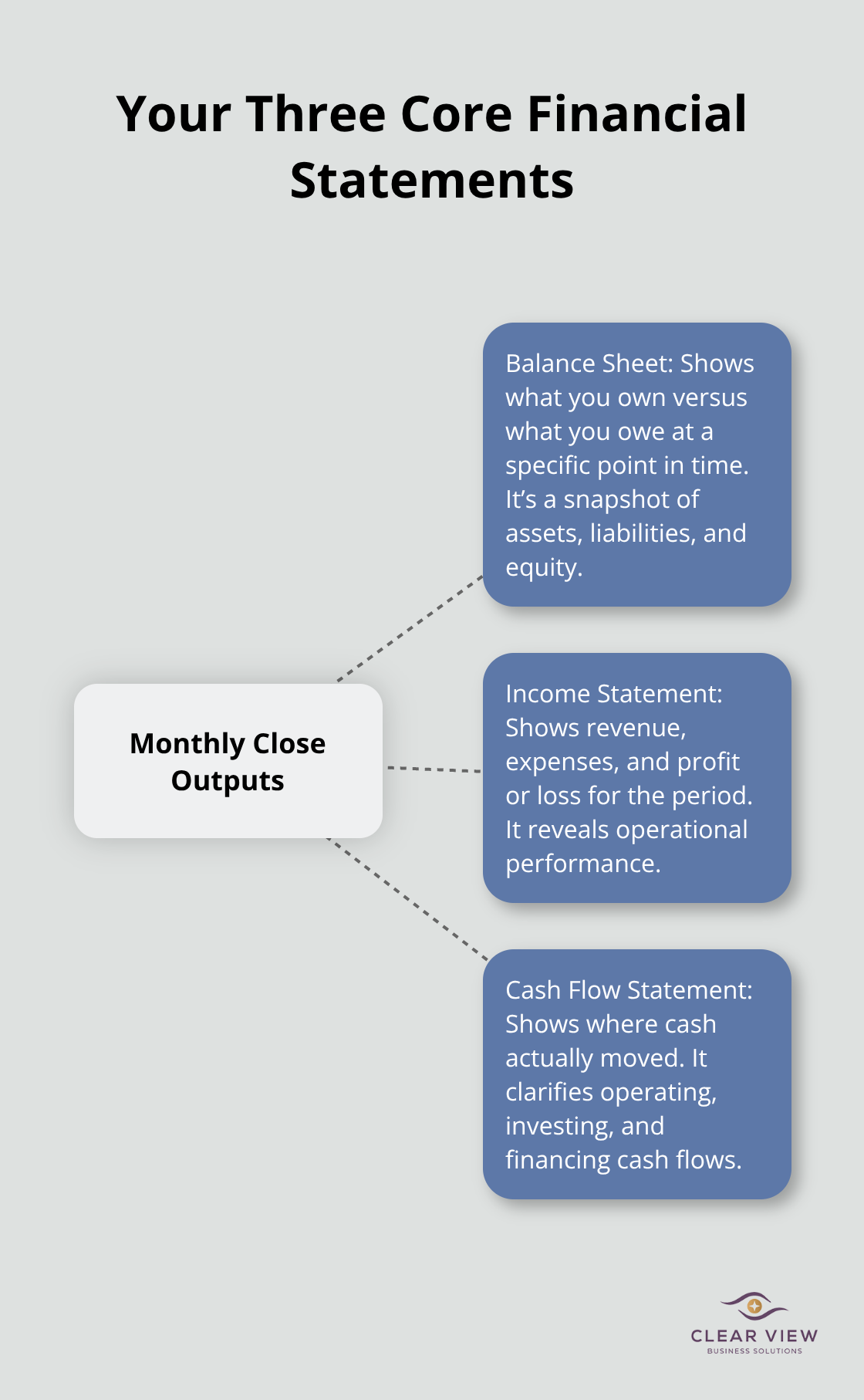

The monthly close is where full-cycle bookkeeping proves its value. After you record all transactions for the month, you reconcile your bank accounts, verify that debits equal credits, make adjusting entries for items like accrued expenses or deferred revenue, and then generate three critical financial statements: the balance sheet, income statement, and cash flow statement. The balance sheet shows what you own versus what you owe on a specific date. The income statement shows whether you made or lost money during the month. The cash flow statement shows where your actual cash moved.

Small businesses that close their books monthly catch errors early, spot spending trends, and know their true profitability instead of guessing. Waiting until year-end to close means errors compound, tax surprises emerge, and you’ve lost months of actionable financial data. A business that closes monthly typically spends 5 to 10 hours per week on bookkeeping, depending on transaction volume and automation. Larger businesses with more transactions may need more time, but accounting software with bank synchronization and automated categorization cuts this burden significantly.

Bookkeeping and accounting are not the same thing, and treating them as such creates confusion. Bookkeeping is the mechanical work of recording, organizing, and categorizing transactions. Accounting is the interpretation and analysis of those records to provide strategic insights and tax planning. A bookkeeper records that you spent $500 on office supplies. An accountant analyzes your spending patterns, identifies tax deductions you missed, and recommends cost-control strategies. Most small businesses need a bookkeeper first and an accountant second. You cannot skip bookkeeping and jump to accounting because accounting requires clean, complete financial data.

The distinction between these two functions matters because it shapes how you approach your financial operations. When you establish solid bookkeeping practices-whether you handle them yourself or hire someone-you create the foundation that accountants, tax professionals, and financial advisors need to help you grow. Without accurate transaction records and organized financial data, no professional can give you reliable tax planning, strategic insights, or compliance guidance. This is why the next section focuses on the specific tasks and responsibilities that make full-cycle bookkeeping work in practice.

Most small businesses fail at transaction recording because owners don’t understand what constitutes a transaction or how to categorize it properly. A transaction is any financial event: a customer payment, a vendor invoice, payroll, equipment purchase, or loan payment. Businesses often record sales correctly but miss expense transactions entirely, creating balance sheets that don’t reflect reality. You must record every transaction with the date, amount, account affected, and source documented.

Bank reconciliation happens monthly and is non-negotiable. You pull your bank statement and match it against your recorded transactions to catch errors, duplicate entries, or unauthorized charges. Most small businesses complete this in 30 minutes to an hour if they reconcile monthly; businesses that wait three months or longer often spend days hunting down discrepancies. Monthly reconciliation prevents small errors from compounding into major problems.

Accounts payable management means tracking money you owe vendors and suppliers. When you receive an invoice, record it immediately in your accounting software rather than leaving it in an email or pile. This prevents overpaying, missing early payment discounts that typically range from 1 to 3 percent, and accidentally paying invoices twice. Prompt recording also gives you an accurate picture of your cash obligations.

Accounts receivable is money customers owe you. If you invoice clients but don’t track what they’ve paid, you’ll face cash shortages even though your income statement looks healthy. Generate an aging report monthly showing which invoices are 30, 60, or 90 days overdue. Invoices over 60 days old have significantly lower collection rates, so you should follow up within two weeks of the due date. This discipline directly impacts your cash flow.

Payroll processing requires precision because mistakes trigger IRS penalties and employee frustration. Federal and state tax withholding rates change annually, and many small business owners either withhold too much (creating unnecessary refunds) or too little (creating liability). If you have employees, you must file payroll taxes quarterly even if you file income taxes annually. The IRS expects estimated payroll deposits on specific dates: semi-weekly filers deposit on Wednesdays or Fridays depending on their payroll schedule, while monthly filers deposit by the 15th of the following month. Missing a deposit date costs you a failure-to-pay penalty of 0.5 to 10 percent of the unpaid amount.

Tax compliance extends beyond payroll. You need to track deductible business expenses throughout the year rather than scrambling at tax time. Office supplies, internet, vehicle mileage, professional services, and equipment depreciation all reduce your taxable income, but only if you document them. The IRS requires receipts for expenses over $75 and contemporaneous written acknowledgment for charitable contributions. Many small business owners lose thousands in deductions because they didn’t organize receipts or forgot transactions happened six months earlier.

Accounting software with receipt scanning and automatic bank feeds eliminates manual entry errors and saves 10 to 15 hours per month for businesses with 200 or more monthly transactions. The discipline of processing these tasks consistently-not sporadically-is what separates businesses with accurate financial statements from those with surprises at tax time. When you establish these routines, you create the data foundation that determines whether your financial statements actually reflect your business performance. The next section explores the tools and systems that make these daily tasks manageable and reliable.

Accounting software is not optional anymore, and selecting the wrong platform wastes time and money. QuickBooks Online dominates the small business market for good reason: it integrates with most banks, automatically categorizes transactions, and generates financial statements in seconds. Pricing ranges from $30 to $200 monthly depending on features. However, QuickBooks is not right for every business. If you process fewer than 50 transactions monthly and need basic income and expense tracking, Wave or ZipBooks might suffice at lower cost. If you run a service business with project tracking needs, FreshBooks combines invoicing and time tracking with bookkeeping. The critical mistake small business owners make is selecting software based on price alone rather than workflow fit. A $15 monthly tool that creates data entry chaos costs far more than a $150 monthly platform that syncs your bank, automatically categorizes spending, and generates accurate reports.

Test any software with your actual transaction types before committing. Most platforms offer 30-day free trials, and using real data during that trial reveals whether the software matches how you actually work. QuickBooks Online works well for most small businesses because its integration ecosystem is strongest and its learning curve is manageable. The software’s widespread adoption means accountants across the country know how to read QuickBooks files quickly during tax season, which simplifies your tax preparation process.

Organization determines whether your bookkeeping system survives contact with reality or collapses under pressure. Create a centralized folder structure on your computer or cloud service with separate folders for each month, vendor, and transaction type. This sounds tedious, but businesses that organize receipts digitally as they arrive spend 5 to 10 hours annually on tax preparation, while disorganized businesses spend 30 to 50 hours hunting for documentation. Use your accounting software’s receipt scanning feature to photograph invoices and receipts immediately rather than storing paper piles. Link each scanned receipt to the corresponding transaction in your general ledger so that auditors or accountants can verify expenses instantly.

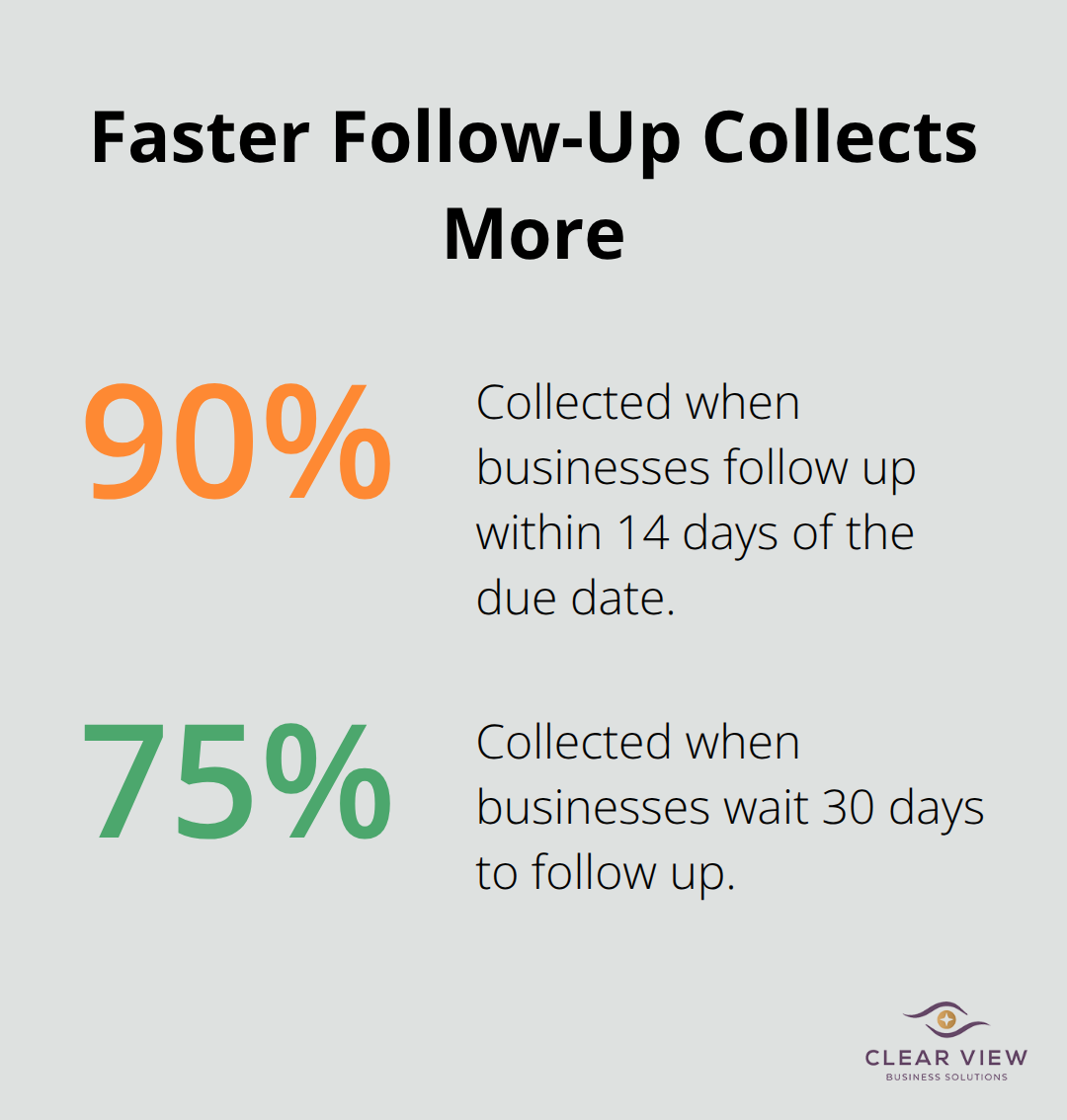

For accounts payable, establish a single inbox where all vendor invoices land before processing. This prevents duplicate payments and ensures you capture early payment discounts (typically 1 to 3 percent). Track accounts receivable by generating an aging report every month and identifying invoices 30 days past due. Contact customers within one week of the due date. Businesses that follow up on overdue invoices within 14 days collect 90 percent of those amounts; waiting 30 days drops collection rates to 75 percent according to credit management research.

Whether you manage bookkeeping in-house or hire a professional, consistency matters more than perfection. A bookkeeper working three hours weekly on organized systems produces cleaner financials than someone working 10 hours weekly in chaos. Consider outsourcing if your monthly transaction volume exceeds 300 or if you lack the discipline to process tasks on schedule. A professional bookkeeper costs about $47,000 a year depending on complexity but eliminates the stress of wondering whether your books are accurate. Outsourcing also frees your time for revenue-generating work.

Full-cycle bookkeeping directly determines whether your small business survives or thrives. Businesses that close their books monthly know their profitability, catch cash flow problems before they become crises, and file taxes with confidence instead of panic. The alternative-scrambling at year-end with disorganized records-costs you thousands in missed deductions, IRS penalties, and wasted time.

The systems you implement now compound over time. A business that reconciles bank accounts monthly, tracks accounts receivable aging, and processes payroll on schedule builds financial clarity that informs every decision. You’ll know whether to hire, whether to invest in equipment, and whether you actually generate profit.

We at Clear View Business Solutions help small businesses in Tucson establish full-cycle bookkeeping systems with QuickBooks training and ongoing support. Whether you start from scratch or fix a broken system, we simplify the process so you focus on growing your business. Your financial clarity starts with one decision: commit to the system.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.