Most companies leave money on the table every year. Between missed deductions, suboptimal entity structures, and overlooked credits, the average business overpays taxes significantly.

At Clear View Business Solutions, we’ve seen firsthand how strategic corporate tax planning transforms a company’s bottom line. This guide walks you through concrete strategies to identify inefficiencies, optimize your structure, and claim deductions you’re likely missing.

Your tax returns from the past three years hold the answers to where your company overpays. Most businesses operate under a structure chosen years ago and never revisited, even though operations have changed dramatically. Pull your last three years of filed returns and your current year’s financial statements. Look specifically at your reported income, total deductions claimed, and your effective tax rate. If you operate as a sole proprietor or general partnership but your revenue exceeds $500,000 annually, you almost certainly pay more federal taxes than necessary. An S corporation or LLC taxed as an S corporation saves 15 percent or more on self-employment taxes once you reach that threshold. Calculate what you actually paid in federal income tax, self-employment tax, and state taxes combined, then divide by your net income. That percentage represents your real tax burden. Most owners guess this number and experience shock when they calculate it accurately.

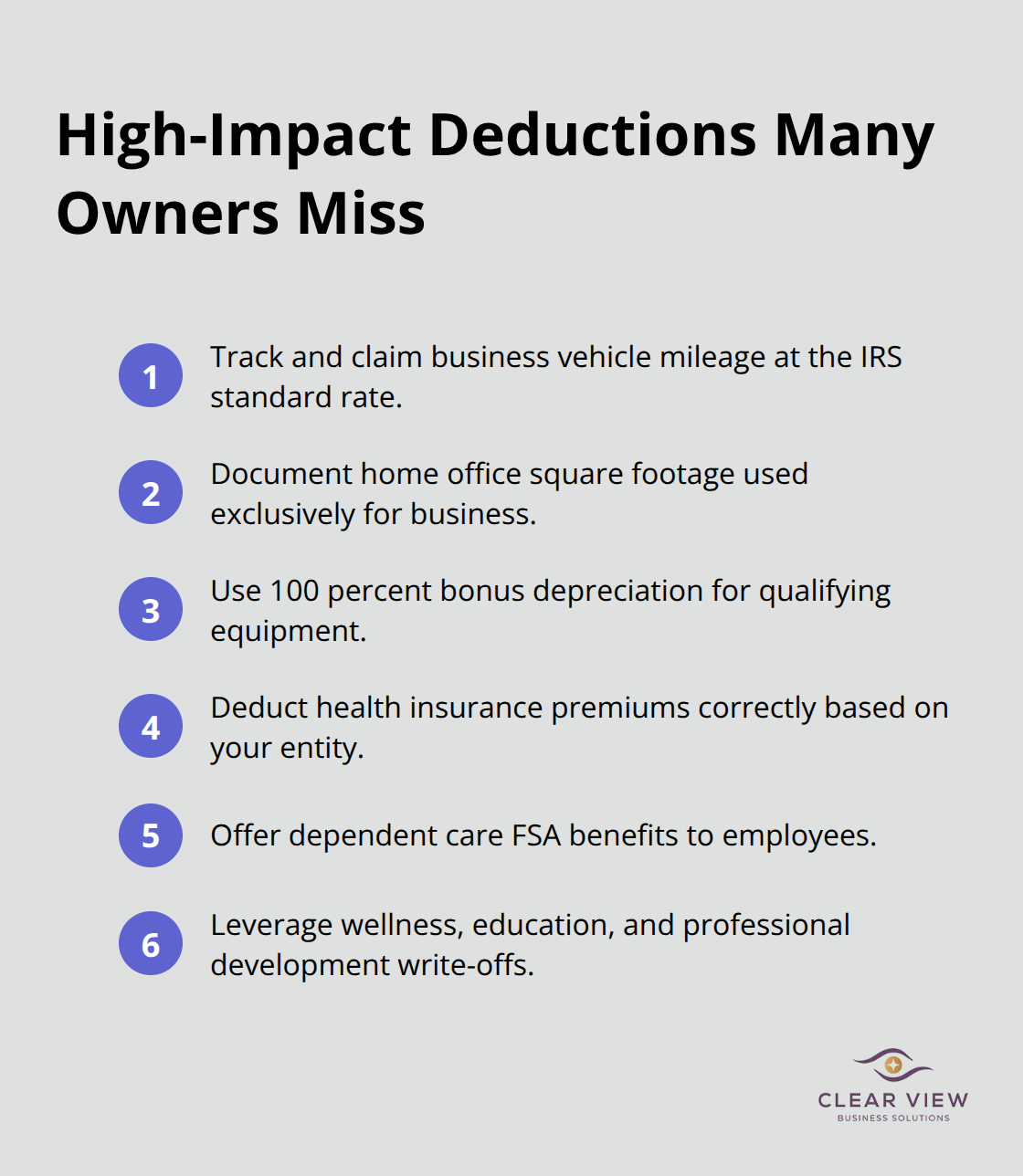

Examine what deductions your business claimed versus what it qualified for. The IRS allows a standard mileage rate of 67 cents per mile in 2026 for business vehicle use, yet most small business owners either skip this deduction entirely or dramatically underestimate their actual mileage. If you drive 15,000 business miles annually, that equals $10,050 in deductions you can claim. Home office deductions receive equally poor treatment. If you use 300 square feet of a 3,000 square foot home exclusively for business, you can deduct 10 percent of your rent or mortgage interest, property taxes, utilities, and insurance. For a $2,000 monthly mortgage on a $200,000 home with 4 percent interest, that amounts to roughly $400 per year in additional deductions, plus utilities and other carrying costs. Equipment purchases present another major opportunity. With 100 percent bonus depreciation now available for equipment placed in service after January 19, 2025, a $50,000 equipment purchase that would have generated depreciation over five years can now receive full deduction in the year of purchase. Review your capital expenditures from the past two years and ask whether you claimed these items under bonus depreciation or spread them across multiple years using traditional depreciation.

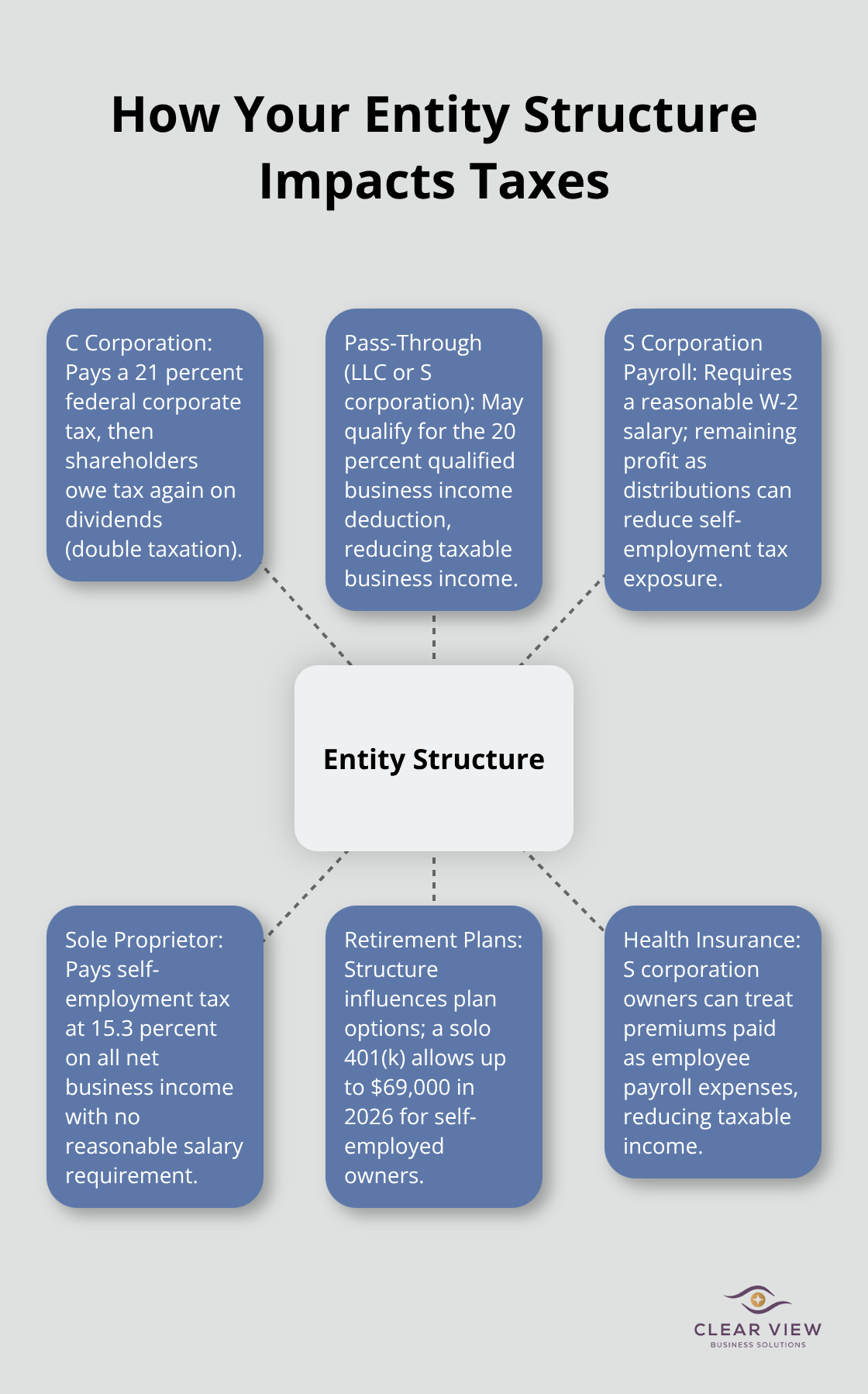

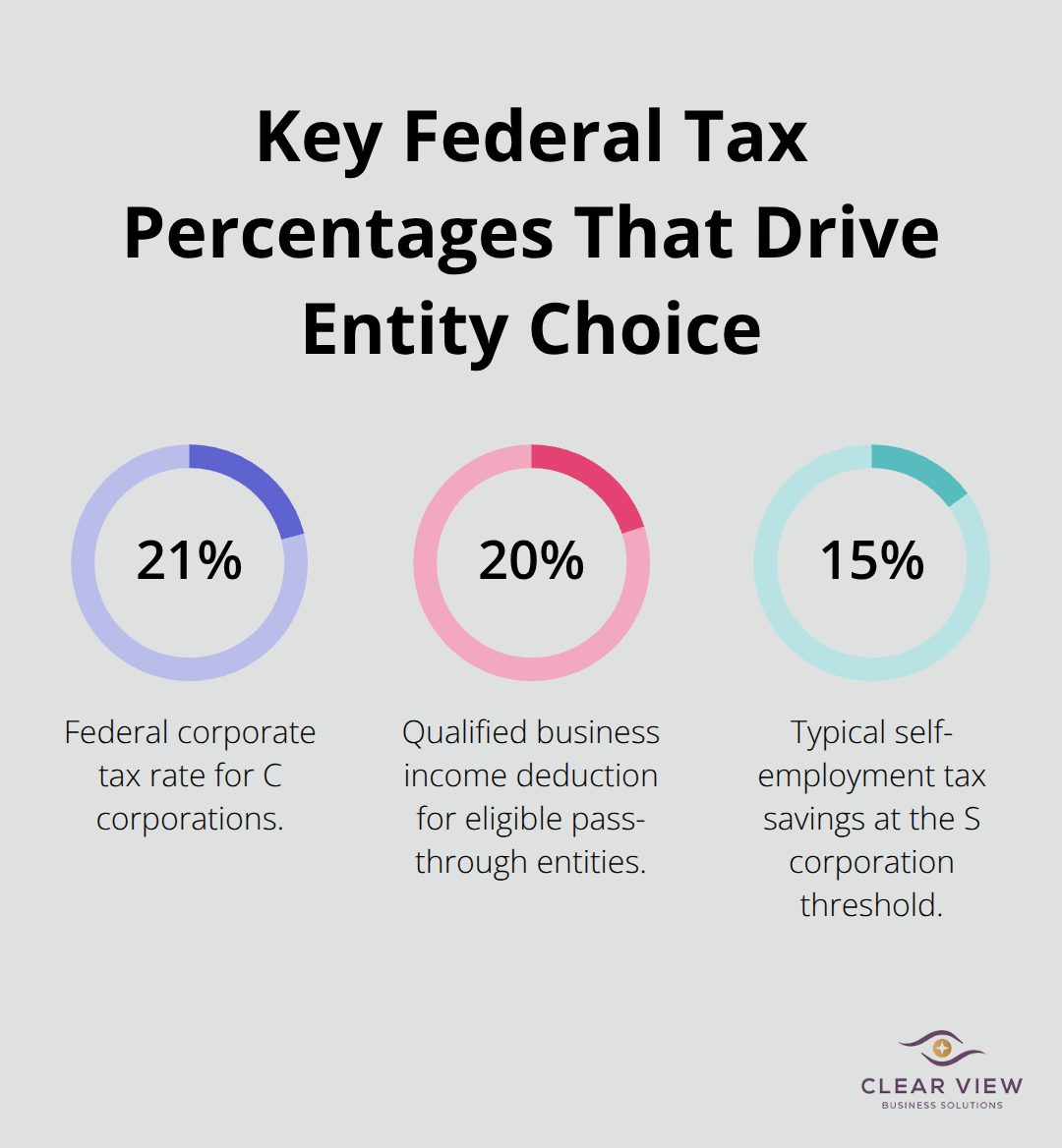

Your current legal structure determines which deductions and credits you actually qualify for. If you operate as a C corporation, you pay corporate tax at 21 percent federal rate, then your shareholders pay tax again on dividends. If you structure as a pass-through entity like an LLC taxed as a partnership or S corporation, you benefit from the 20 percent qualified business income deduction, which means 20 percent of your business income avoids taxation entirely if you qualify. Pass-through entities avoid double taxation, but they require more sophisticated payroll planning. An S corporation requires you to pay yourself a reasonable W-2 salary and take the remainder as distributions, which reduces self-employment tax exposure. A sole proprietor or single-member LLC pays self-employment tax on all net business income at 15.3 percent, with no reasonable salary requirement. If your business generates $300,000 in net profit and you operate as a sole proprietor, you owe approximately $42,390 in self-employment tax alone. That same business structured as an S corporation with a $100,000 W-2 salary and $200,000 in distributions would owe only $15,300 in self-employment tax on the W-2 portion, saving $27,090 annually.

Your structure also affects which retirement plans you can establish and how much you can contribute. A solo 401(k) allows you to contribute up to $69,000 in 2026 as a self-employed person, compared to $7,000 in a traditional IRA. These contributions reduce your taxable income dollar-for-dollar.

The retirement plan you select directly impacts both your current tax liability and your long-term wealth. A SEP IRA lets you contribute up to 25 percent of your net self-employment income, capped at $69,000 in 2026. A SIMPLE IRA works well for businesses with fewer than 100 employees and allows contributions up to $16,000 in 2026, plus employer matches. A profit-sharing plan lets you vary contributions year to year based on business performance. These plans offer startup tax credits of up to $5,000 if you establish them before year-end, which directly reduces your tax liability. The IRS also allows you to make contributions to these plans until your tax return due date (including extensions), giving you flexibility to assess your final income before committing funds. If you operate as an S corporation, you can establish a solo 401(k) and contribute significantly more than other entity types, making this structure particularly attractive for higher-income business owners.

Your entity structure decision affects every tax dollar you pay. Most businesses that operate as sole proprietorships or partnerships beyond $500,000 in revenue leave substantial savings on the table. The combination of self-employment tax exposure, missed deductions, and overlooked credits creates a compounding effect that grows worse each year you delay optimization. The next section examines specific tax strategies that work within your chosen structure and shows how timing decisions throughout the year can further reduce your overall tax burden.

The timing of when you recognize income and claim deductions determines how much tax you owe more than almost any other factor. Most business owners treat tax planning as an annual event in December, but the real savings come from decisions made throughout the year. If you operate on a cash basis, you control whether revenue hits your books in December or January simply through when you invoice clients and when they pay. A service business that completes $50,000 in work in late November can delay invoicing until January, pushing that income into the next tax year. Conversely, if your profit forecast shows a strong year, accelerating customer collections into the current year while deferring vendor payments to January creates a timing mismatch that reduces current-year taxable income.

Equipment purchases deserve the same strategic attention as income timing. The 100 percent bonus depreciation rule allows qualified business property owners to take a full deduction in the year the property is placed in service. If your business generates $200,000 in profit and you make an equipment purchase in November, your taxable income drops accordingly, saving roughly $18,900 in federal tax at the 21 percent corporate rate. Defer that same purchase to January and you lose that deduction in the current year entirely. Cash-basis business owners should also evaluate prepaying business expenses in December if profits are running high. Insurance premiums, professional services, subscriptions, and software licenses paid in December reduce current-year income even if the service extends into future months. The IRS allows this timing strategy for legitimate business expenses, not just year-end gimmicks.

Retirement contributions and estimated tax payments create additional timing opportunities that most owners overlook. An S corporation owner can contribute to a solo 401(k) until the tax return due date including extensions, meaning you have until October 15 of the following year to assess final income and determine how much to contribute. That flexibility lets you maximize contributions when you know your actual profit picture rather than guessing in November. If you operate as an LLC taxed as an S corporation, your estimated tax payments on quarterly distributions affect your cash flow significantly. Paying 90 percent of current-year tax liability or 100 percent of prior-year tax liability avoids penalties, but paying exactly 100 percent of the prior year’s liability often works best for growing businesses where income increases year over year. You avoid overpaying while staying compliant.

Pass-through entity owners in states like Arizona should evaluate the pass-through entity tax election available in certain jurisdictions. Paying state-level tax at the entity level rather than individual level creates a federal deduction on your personal return, effectively converting a non-deductible state tax into a deductible business expense. State tax planning requires coordination with your CPA because rules vary significantly by state, but the savings justify the complexity. These timing strategies work best when you plan them throughout the year rather than scrambling in December. The next section examines specific deductions and credits that most businesses overlook entirely, showing you where to find additional tax savings within your current structure.

Most business owners claim the same deductions year after year without questioning whether they capture everything the IRS allows. The reality is that home office expenses, vehicle mileage, equipment purchases, and employee benefits contain some of the largest unclaimed deductions available to small businesses. You likely qualify for thousands of dollars in deductions that never make it to your tax return because nobody told you they existed or because the calculation process seemed too complicated.

The IRS standard mileage rate of 72.5 cents per mile in 2026 means a business owner who drives 20,000 business miles annually can claim $14,500 in deductions. Yet most owners either skip mileage tracking entirely or estimate wildly inaccurate numbers. Home office deductions work similarly. If you use 400 square feet of a 2,000 square foot home exclusively for business, you qualify to deduct 20 percent of your mortgage interest or rent, property taxes, utilities, insurance, and maintenance costs. For someone paying $2,500 monthly in housing costs, that translates to $6,000 annually in additional deductions.

Equipment purchases deserve equally aggressive attention because the 100 percent bonus depreciation rule allows you to deduct qualifying property in full during the year you place it in service. A $30,000 computer system or manufacturing equipment purchased in November generates a $30,000 deduction immediately rather than spreading across multiple years. These three categories alone often represent $15,000 to $40,000 in missed deductions annually depending on your business type.

Health insurance and employee benefits create another major deduction opportunity that varies significantly based on your business structure. If you operate as an S corporation and pay health insurance premiums for yourself as an employee, you deduct those premiums as payroll expenses on your business return rather than claiming them as individual deductions on your personal return. This distinction matters because business deductions reduce your self-employment tax exposure while personal deductions do not. A sole proprietor paying $8,000 annually in health insurance premiums can only deduct this amount on their personal return, but an S corporation owner deducts it as a business expense and avoids self-employment tax on that amount, saving roughly $1,200 in combined taxes.

Dependent care credits and childcare benefits offer similar advantages. The IRS allows employers to provide up to $5,000 annually in dependent care benefits to employees on a pre-tax basis, and employers can claim a credit for providing childcare assistance. If your business has employees, establishing a dependent care flexible spending account costs minimal administrative effort yet creates tax savings for both you and your employees. Employee wellness programs, professional development, and educational assistance also qualify as deductible business expenses that most owners either overlook or implement inconsistently. These benefits cost money, but the tax deductions and employee retention benefits often justify the expense.

The distinction between what you can deduct and what you actually deduct represents the gap between paying what you owe and overpaying what the tax code never intended.

The gap between what your business owes in taxes and what you actually pay represents real money sitting on the table. Corporate tax planning isn’t complicated when you break it into three concrete actions: optimize your entity structure, time your income and deductions strategically, and claim every deduction the tax code allows. Most business owners leave between $15,000 and $40,000 annually unclaimed through missed deductions alone.

Your vehicle mileage, home office, equipment purchases, and employee benefits contain thousands in tax savings that require nothing more than proper documentation and awareness. An S corporation owner who structures properly saves $27,000 annually on self-employment taxes compared to a sole proprietor, and a business that captures bonus depreciation on equipment purchases reduces taxable income by the full purchase amount rather than spreading deductions across years. These aren’t theoretical savings-they’re concrete reductions in what you owe.

Pull your last three years of tax returns and calculate your actual effective tax rate, then compare that number against what you’d pay under a different entity structure. Identify which deductions you claimed versus which ones you qualified for but missed, and this analysis reveals exactly where your business overpays. We at Clear View Business Solutions specialize in tax planning for small businesses and startups, helping owners identify inefficiencies and implement strategies that stick.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2933 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.