Tax compliance isn’t optional-it’s the foundation that keeps your business operating without legal or financial risk. The IRS audits roughly 0.4% of all tax returns annually, but the consequences of being unprepared are severe.

At Clear View Business Solutions, we’ve seen firsthand how small mistakes in record-keeping and filing can spiral into costly penalties. This guide walks you through the most common pitfalls, the documentation you need, and the systems that keep you audit-ready all year long.

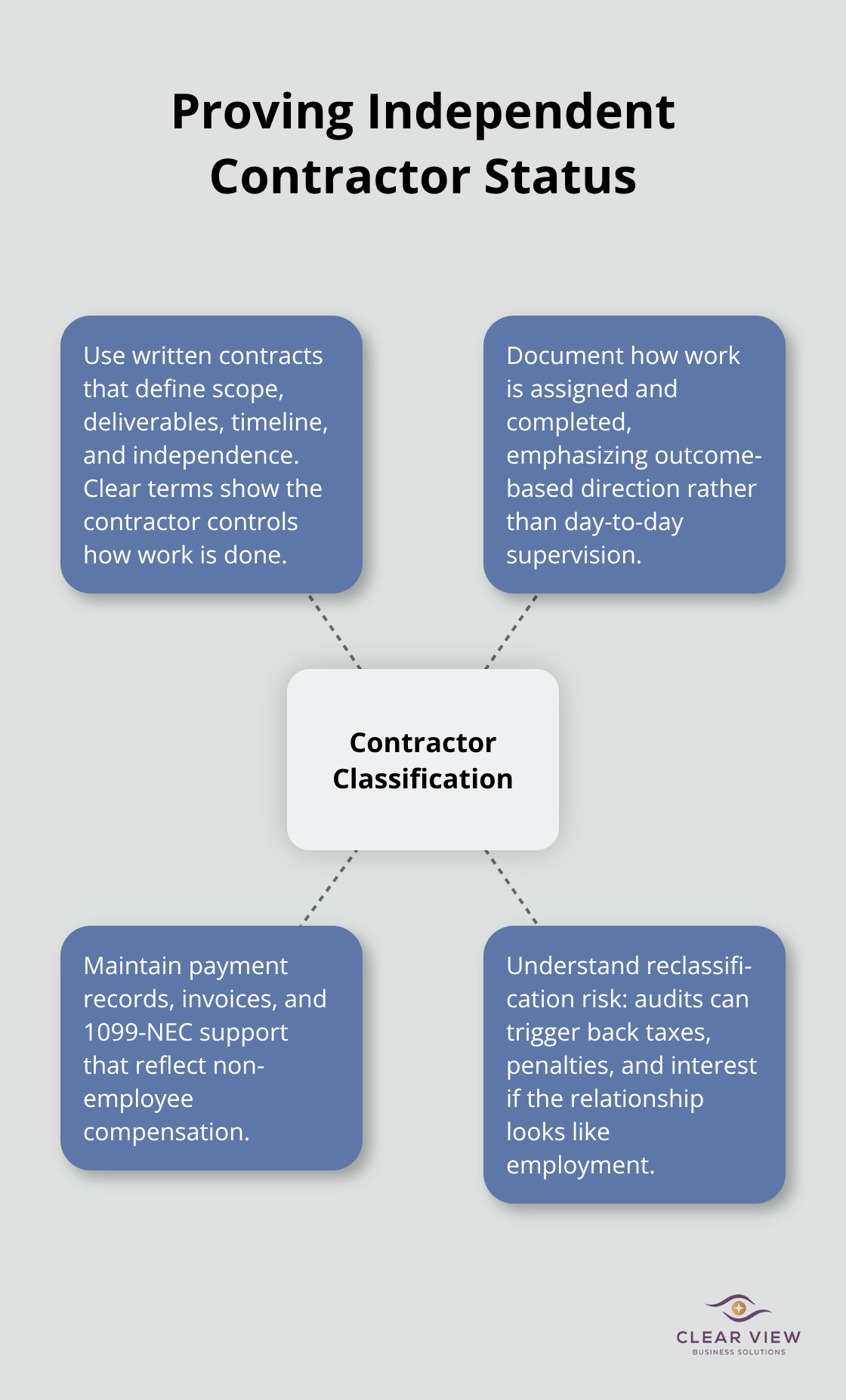

The IRS identifies six primary audit triggers, and three of them stem from decisions businesses make during day-to-day operations. Misclassifying workers as independent contractors instead of employees ranks high on that list. The IRS defines an independent contractor as someone who controls the work and how it’s done, with the payer only dictating the end result. Many businesses blur this line to avoid payroll taxes and benefits obligations, but the IRS catches this regularly.

If you hire contractors, you need written contracts and payment records that clearly show the contractor relationship. Document how work is assigned and completed to support your classification. A single reclassification audit can cost thousands in back taxes, penalties, and interest, making this worth getting right from the start.

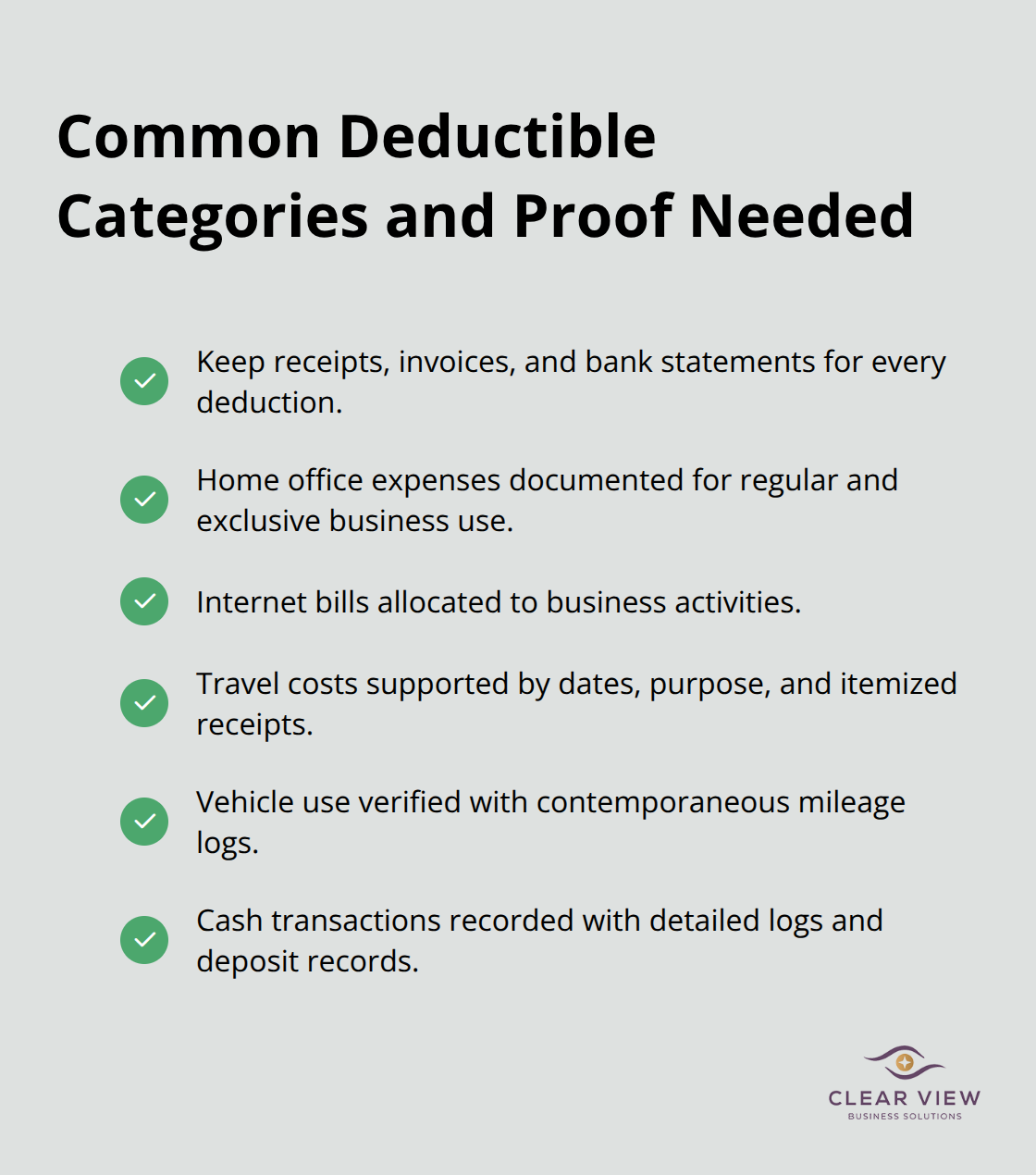

Failing to track deductible expenses is equally costly, though it works differently. Self-employed individuals filing Schedule C face higher audit rates because they control both income reporting and expense deductions. Many business owners round figures, average expenses across years, or simply estimate rather than documenting actual transactions.

Deductible expenses must be ordinary and necessary, and you need receipts, invoices, and bank statements to back them up. Common deductible categories include home office, internet bills, travel costs, and vehicle use, but substantiation is essential. Cash-heavy businesses like restaurants and beauty salons face extra scrutiny because large cash transactions require robust income verification and transaction documentation.

Missing filing and payment deadlines compounds these problems significantly. The IRS will complete an audit and issue findings if you don’t respond by the due date, and you lose the opportunity to provide evidence that supports your position. Extensions are available for mail audits (one automatic 30-day extension), and you can request a face-to-face audit if you have too many records to mail, but you must act before the deadline passes.

The statute of limitations for assessment is generally three years from the due date or filing, though substantial errors can extend this to six years. Staying audit-ready means you maintain current, organized records year-round rather than scrambling to reconstruct documents months after filing. This foundation of organized documentation directly shapes how you respond when the IRS requests specific information-a process we’ll cover in the next section.

The IRS requires you to keep all records used to prepare your tax return for at least three years, though substantial errors can extend this to six years. This isn’t a suggestion-it’s the difference between surviving an audit and scrambling to reconstruct evidence months after filing. Business owners often discover mid-audit that they’ve discarded critical documentation, forcing them to rely on reconstructed records that auditors view with skepticism. Your financial records must include bank statements, credit card statements, and transaction logs that show exactly where money came from and where it went. For businesses with multiple accounts or cash transactions, this becomes non-negotiable.

Receipts and invoices for every deductible expense should be organized by category and stored digitally or in a filing system you can access within hours, not days. The IRS doesn’t care if your receipt is crumpled or faded-they care that it exists and shows the date, vendor, amount, and business purpose. Organization matters more than perfection. A business owner filing Schedule C who maintains monthly expense summaries in a spreadsheet and stores receipts in labeled folders will withstand an audit far better than someone with boxes of unsorted paperwork.

Digital tools like QuickBooks or similar accounting software create an audit trail that shows when transactions were entered, who entered them, and whether corrections were made. The IRS accepts electronic records, but verify with an auditor what file formats work for your specific audit. Expense documentation should include not just receipts but also supporting evidence-mileage logs for vehicle deductions, utility bills for home office deductions, or invoices showing services rendered for travel expenses. Many audits fail not because the expense wasn’t legitimate but because the taxpayer couldn’t prove the business purpose or connection to income generation.

Payroll records demand particular attention because the IRS cross-references W-2 filings, 1099 reports, and your internal records to catch misclassification. Keep written contracts with independent contractors, documentation showing how work was assigned and completed, and payment records that prove the contractor relationship. For employees, maintain I-9 forms, W-4 withholding elections, timesheets, and records of any payroll adjustments or corrections.

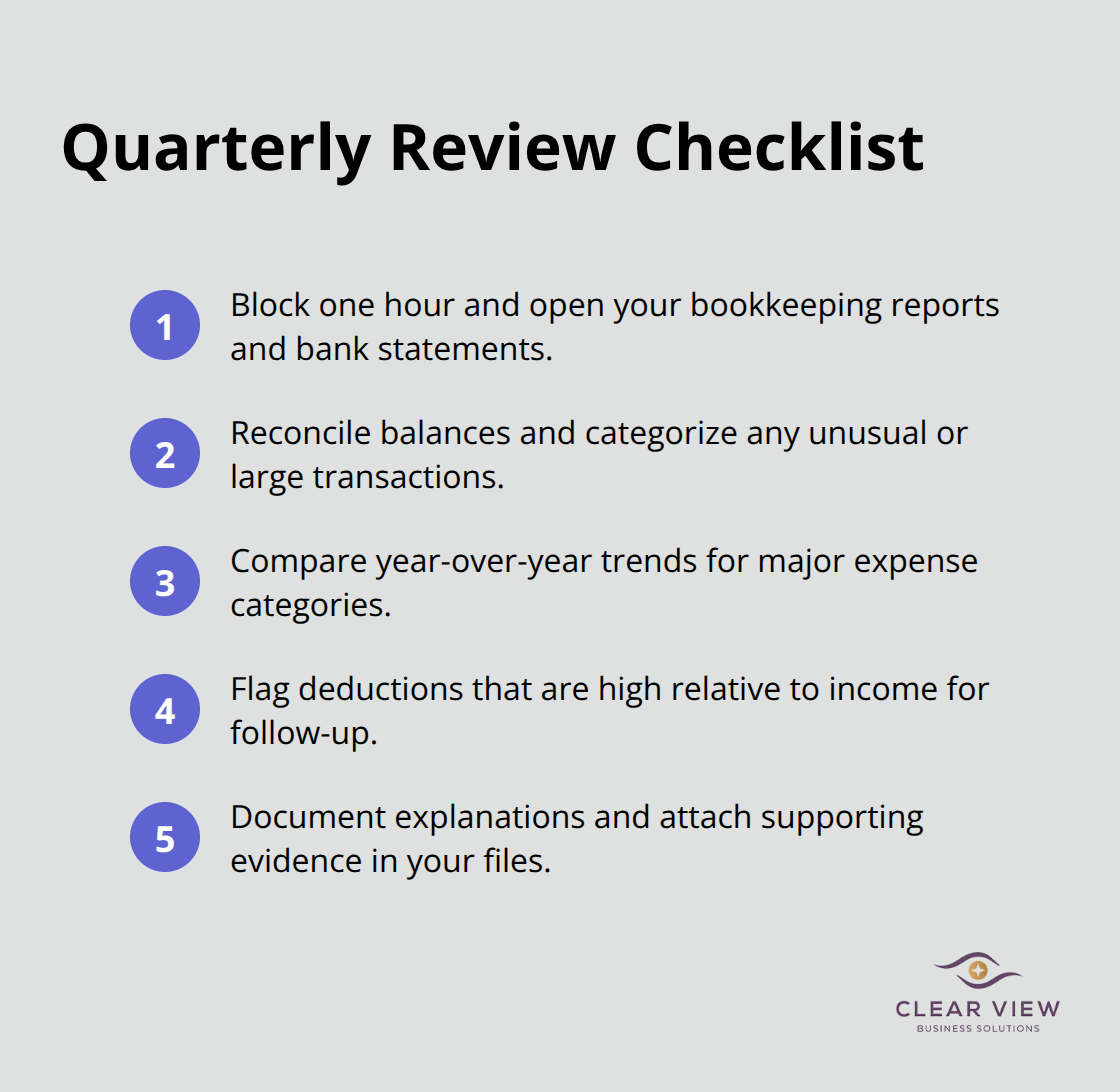

Cash-heavy businesses face heightened scrutiny, so if your operation involves large daily cash transactions, implement a point-of-sale system that records each transaction with a timestamp and description. This creates objective evidence of income that’s harder to challenge than memory or reconstruction. Set a calendar reminder to review your records quarterly, checking for gaps, missing receipts, or unexplained transactions before they become audit vulnerabilities. This proactive approach to documentation sets the stage for the next critical step: establishing systems that maintain these records consistently throughout the year.

Audit readiness requires systems that operate consistently without constant manual effort. Bookkeeping software like QuickBooks or FreshBooks creates automatic audit trail creation in bookkeeping software, recording when transactions were entered, who entered them, and any corrections made afterward. This digital record proves to auditors that your books were maintained throughout the year rather than hastily reconstructed after the IRS selected you for examination. Set up your chart of accounts to match the categories the IRS expects on Schedule C or your tax return, so your software generates reports that align directly with what you file. The software handles the repetitive work, freeing you to focus on running your business while maintaining the documentation that auditors expect to see.

Schedule a focused quarterly review-roughly one hour per quarter-where you compare your software reports to your bank statements and verify that large or unusual transactions are categorized correctly. This simple practice catches patterns the IRS spots regularly: dramatic expense spikes year-over-year, deductions that are disproportionately high relative to income, or income that doesn’t reconcile with bank deposits. Identifying these patterns yourself in Q2 gives you time to explain them, adjust if needed, or prepare supporting documentation before you file.

This proactive approach transforms you from someone hoping the IRS overlooks a problem into someone who has already addressed it. Many businesses that sail through audits do so because someone was checking the books every quarter, not scrambling to reconstruct records months after filing.

A tax professional-whether a CPA or enrolled agent-becomes your partner in maintaining audit readiness. They review your quarterly reports, flag areas where your documentation might be weak, and identify where the IRS is likely to ask questions. They catch audit vulnerabilities before you file, not after you’ve been selected for examination. This ongoing relationship costs less than the penalties and interest you’d face if an audit exposed gaps in your records or misclassified expenses. A tax professional also stays current on IRS enforcement priorities and adjusts your compliance strategy accordingly. Their guidance transforms tax compliance from a once-a-year scramble into a managed process that protects your business throughout the year.

Tax compliance operates best when you build it into your business systems rather than treat it as a once-a-year task. The businesses that avoid audits maintain organized records throughout the year, address potential problems before they escalate, and work with professionals who understand current IRS priorities. Misclassifying workers, failing to document expenses, and missing deadlines cost thousands in penalties and interest-all preventable through consistent attention to your records and processes.

Staying compliant delivers benefits that extend far beyond avoiding penalties. You reduce stress when your records are organized and defensible, you save time through automated bookkeeping instead of reconstructing transactions months after filing, and you build confidence that your business operates on solid financial ground (which matters when seeking loans, attracting investors, or planning growth). Most importantly, you prevent the disruption and expense of an audit that better systems could have stopped.

Start this month by implementing one system: set up bookkeeping software if you haven’t already, schedule your first quarterly review, or contact Clear View Business Solutions to assess your current documentation and identify gaps. We specialize in full-cycle bookkeeping, tax planning, and IRS representation for small businesses, helping you build the tax compliance foundation that protects your operation year-round.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2025 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.