Wealthy tax strategies aren’t one-size-fits-all, and most high-income earners leave significant money on the table by using generic approaches. At Clear View Business Solutions, we’ve seen firsthand how targeted planning can reduce tax bills by thousands annually.

The strategies in this guide go beyond basic deductions. They’re designed specifically for those with substantial income and assets who want to keep more of what they earn.

Retirement accounts form the foundation of tax-efficient wealth building, yet most high-income earners fail to maximize what’s available to them. For 2025, you can contribute $23,500 to a 401(k) with a catch-up allowance if you’re 50 or older. If you own a business, the picture changes dramatically-combined contributions per worker can reach $70,000, which means you reduce current taxable income by that full amount. This isn’t theoretical; it’s direct, measurable tax relief. Many wealthy individuals stop at the employee limit and miss the employer contribution opportunity entirely. If you have any self-employment income or run a small business, you’re leaving tens of thousands in annual deductions on the table. The carry-forward rule for concessional super contributions also matters-you can use unused caps from the previous five years according to ATO guidance, which creates a backdoor to catch up if you had lower income years.

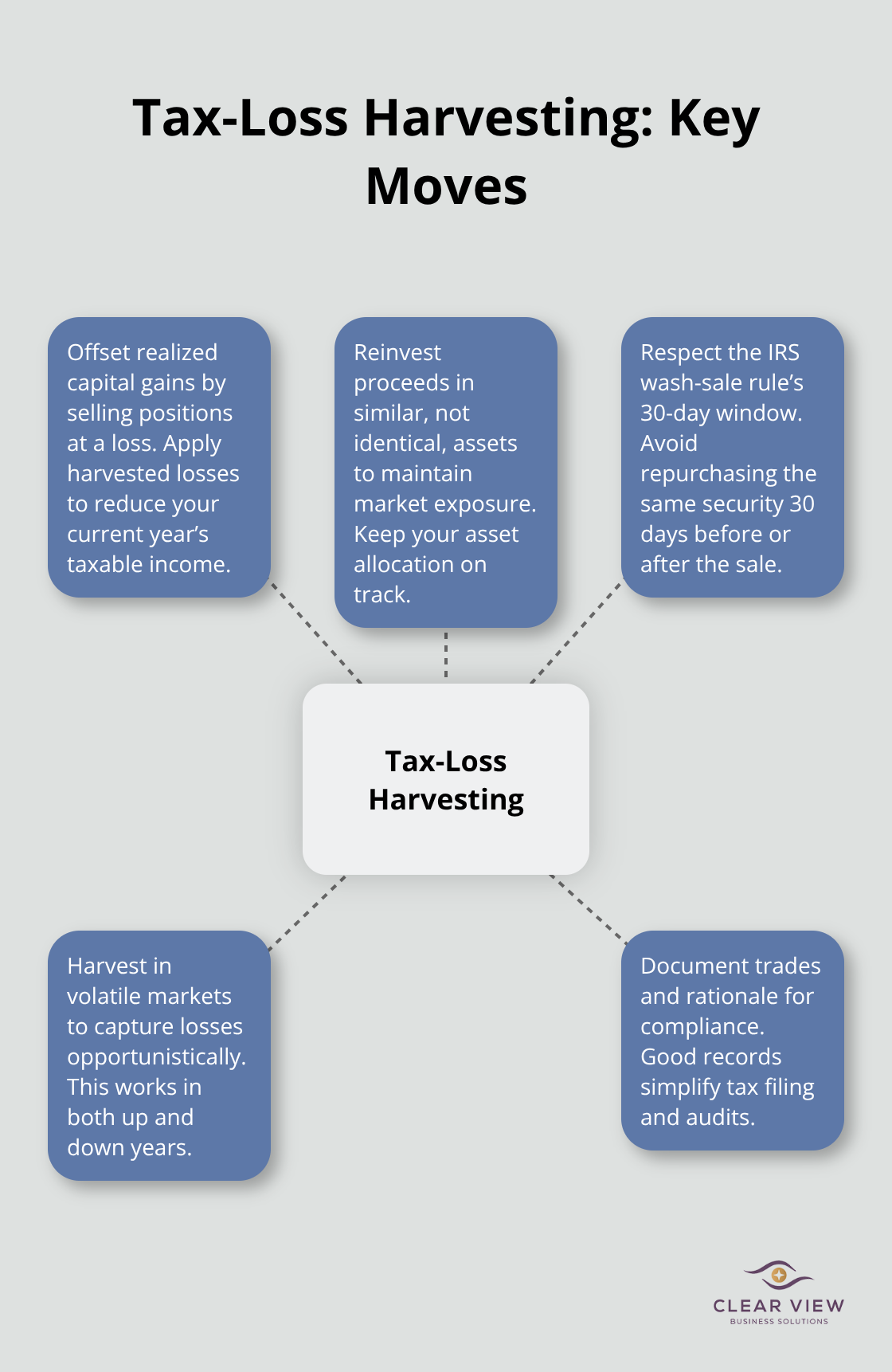

Tax-loss harvesting deserves serious attention because it works in both strong and weak market years. You sell securities at a loss to offset capital gains elsewhere in your portfolio, then immediately reinvest in similar but not identical investments to maintain your market exposure. This isn’t market timing or speculation; it’s systematic tax optimization. If you harvest losses worth $50,000 against gains, you’ve just reduced your taxable income by that amount. The IRS wash-sale rule prevents you from buying the same security within 30 days before or after the sale, but comparable alternatives exist in the same sector or asset class.

Long-term capital gains receive preferential tax treatment, and timing your asset sales strategically saves substantial sums. Hold investments for at least 12 months to access preferential tax rates, which provides a meaningful advantage over short-term gains taxed as ordinary income. If you sit on appreciated securities, avoid selling them all in one year if you can spread the sales across multiple years-this keeps you in lower tax brackets and maximizes the benefit of preferential rates. For high-income earners, municipal bonds offer another angle because their interest remains exempt from federal taxes and potentially from state and local taxes depending on where you live. This tax-free income directly increases your after-tax returns compared to taxable bonds yielding similar nominal rates.

Franking credits on Australian shares offset other taxable income or generate refundable tax offsets, which enhances after-tax returns according to ATO guidance. The practical step here involves reviewing your portfolio’s tax drag annually-how much of your returns are consumed by taxes rather than compounding for growth. Many investors focus on gross returns and ignore the tax efficiency of how those returns are structured. Your investment strategy should account for the tax treatment of each position, not just its potential for appreciation. This shift in perspective often reveals that restructuring your holdings can preserve thousands in after-tax wealth without changing your overall market exposure or risk profile.

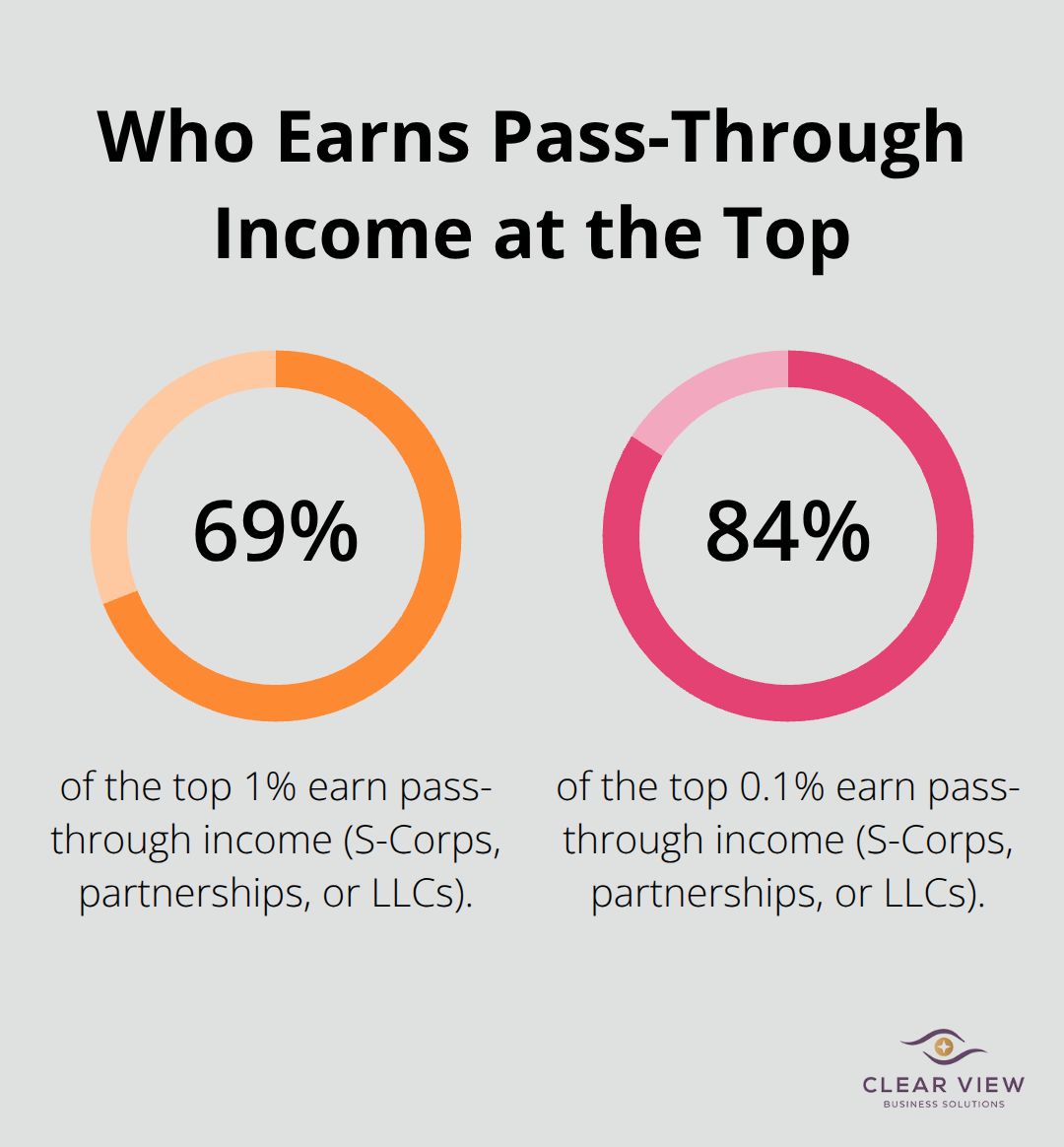

Your choice of business entity determines how much of your income gets taxed and when. S-Corps, LLCs, and C-Corps each carry different tax consequences, and the wrong structure costs high-income earners tens of thousands annually. Research from Smith, Yagan, Zidar, and Zwick at the National Bureau of Economic Research found that over 69% of the top 1% and over 84% of the top 0.1% earn pass-through income, meaning they operate as S-Corps, partnerships, or LLCs rather than traditional corporations. This matters because pass-through structures allow you to reduce Medicare payroll tax burdens by classifying compensation as profits rather than wages, provided you structure it correctly and maintain substantiation.

An S-Corp requires you to pay yourself a reasonable salary subject to payroll tax, then take the remainder as a distribution, which avoids the 15.3% self-employment tax on that portion. If you operate as a sole proprietor or partnership without this split, every dollar of profit faces self-employment tax. The practical difference proves substantial: a business that generates $200,000 in profit could save $15,000 to $25,000 annually by electing S-Corp status, depending on how much you legitimately classify as profit versus salary.

LLCs offer flexibility in how they’re taxed-you can elect to be taxed as an S-Corp, C-Corp, or sole proprietorship-so most high-income business owners use an LLC taxed as an S-Corp to preserve liability protection while capturing tax savings.

C-Corps face double taxation at the corporate and individual level, making them inefficient for most wealthy individuals unless you’re retaining earnings for reinvestment and can justify that strategy with documented business plans. The corporate tax rate applies first, then shareholders pay tax again on distributions, which erodes wealth faster than pass-through structures. This dual hit makes C-Corps suitable only in narrow circumstances where you intentionally retain profits inside the corporation for strategic reasons.

Real estate investors should implement cost segregation studies immediately if they own commercial properties, multifamily buildings, or specialized assets. A cost segregation study reclassifies portions of a building and its components into shorter depreciation schedules, which accelerates deductions into the early years of ownership. IRS Revenue Procedure 87-56 classifies car wash buildings as 15-year property rather than 39-year residential or commercial property, and self-storage facilities can treat interior partitions as 5-year property while roads and utilities remain 15-year improvements. The front-loaded benefit proves substantial: a $2 million property might generate $300,000 to $500,000 in first-year depreciation deductions through cost segregation, directly reducing your taxable income. However, depreciation recapture applies when you sell, so this strategy works best when you hold assets long-term and plan for eventual tax liability.

Charitable Remainder Trusts convert appreciated assets into income streams while reducing your estate tax exposure. You transfer highly appreciated securities or real estate into a CRT, receive an immediate income tax deduction, and the trust generates regular payments to you for life or a set term. When the trust terminates, remaining assets pass to your designated charity. For example, if you hold $1 million in appreciated stock with a $200,000 cost basis and transfer it to a CRT, you avoid the $160,000 capital gains tax on the appreciation while taking an upfront charitable deduction and receiving income distributions. The IRS valuation tables determine your deduction amount based on your age, trust terms, and discount rates. This structure works particularly well for business owners who need liquidity after a sale or for those holding concentrated positions they want to diversify without triggering capital gains.

These business structure decisions interact with your overall wealth plan, and the right choice depends on your specific income level, asset composition, and long-term goals. The next section examines how you can maximize deductions through strategic timing and expense categorization, turning ordinary business activities into tax-efficient wealth preservation.

Home office and vehicle expenses represent the largest missed deduction opportunities for self-employed professionals and business owners. The IRS allows two methods for home office deductions: the simplified method at $5 per square foot up to 300 square feet (maximum $1,500 annually) or the regular method that deducts a percentage of your mortgage interest, property taxes, utilities, insurance, and repairs based on the office’s square footage relative to your total home. Most high-income earners choose the simplified method and leave money on the table. If your home office occupies 200 square feet, the simplified method yields $1,000 annually, but the regular method often produces $3,000 to $6,000 depending on your home’s value and location. Your office must be used exclusively and regularly for business-a desk in your bedroom doesn’t qualify, but a dedicated room with a door used only for work absolutely does.

Vehicle expenses work similarly with two options. You can deduct the standard mileage rate, which the IRS set at 70 cents per mile for self-employed and business use, or track actual expenses including fuel, maintenance, insurance, and depreciation. If you drive 20,000 business miles annually, the standard rate yields $14,000 in deductions, but actual expense tracking frequently produces $15,000 to $18,000 when depreciation is properly calculated. Once you choose actual expenses, switching back to standard mileage becomes difficult, so start with whichever method produces larger deductions in your first year and stick with it. Maintain a mileage log documenting business purpose, destination, and miles driven; the IRS scrutinizes vehicle deductions heavily, and contemporaneous records separate legitimate claims from disallowed ones.

Education credits and dependent deductions interact with income thresholds that phase out benefits for high earners, making strategic timing essential. The American Opportunity Tax Credit provides up to $2,500 per student for four years of undergraduate education, but phases out between $80,000 and $100,000 for single filers. The Lifetime Learning Credit offers up to $2,000 per return but phases out between $80,000 and $100,000 as well. If your income falls near these thresholds, income bunching becomes essential. Income bunching involves timing deductible expenses and deferring income across years to stay below phase-out ranges when education credits apply. For example, if you’re self-employed, deferring client invoices into the following year while accelerating business expenses into the current year can reduce your modified adjusted gross income enough to capture education credits worth thousands.

Dependent deductions have shifted significantly since 2017, but each qualifying dependent still generates a $2,000 child tax credit (with income limits beginning at $400,000 for married filers), and dependent exemptions remain useful for complex tax situations. These credits interact with your overall tax picture, so coordinate dependent claims with education credits and other phase-out provisions to maximize total benefits.

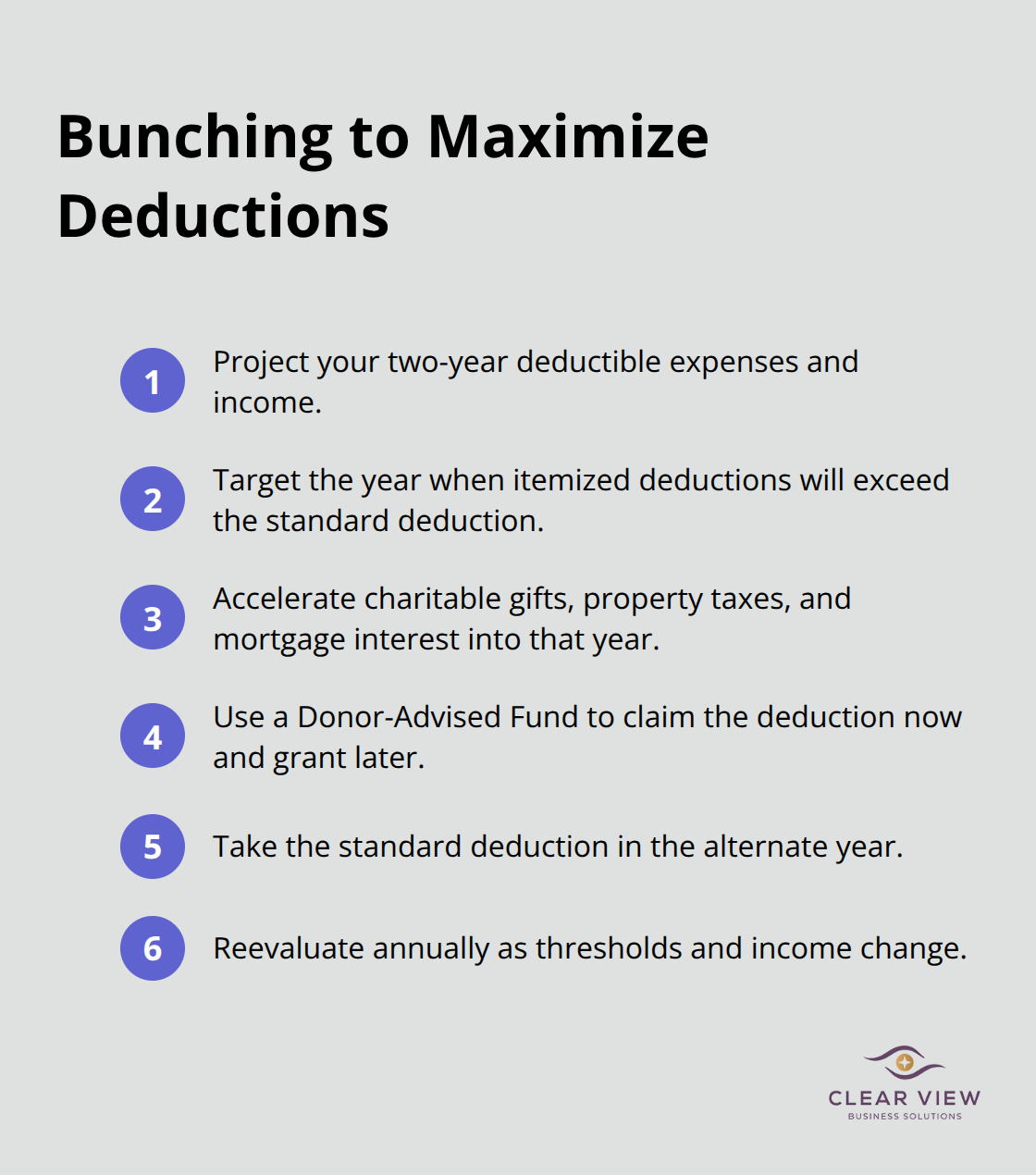

Itemized deductions require bunching strategies when your itemized deductions hover near the standard deduction threshold. For 2024, the standard deduction sits at $13,850 for single filers and $27,700 for married filing jointly. If you anticipate itemized deductions of $28,000 in one year and $26,000 in the next, bunching means accelerating charitable donations, property tax payments, and mortgage interest into a single year to exceed the standard deduction threshold, then taking the standard deduction in the alternate year.

This approach can increase total deductions by $2,000 to $5,000 over two years.

Charitable giving provides the clearest bunching opportunity. Rather than donating $5,000 annually, donate $10,000 in year one and nothing in year two, allowing year one itemized deductions to exceed the standard deduction while year two’s standard deduction covers baseline expenses. Donor-Advised Funds amplify this strategy by letting you claim a deduction in the year you fund the account while distributing money to charities across future years, separating the tax benefit from the actual charitable giving timing. This separation creates flexibility and maximizes your deduction impact without constraining when your money actually reaches charitable organizations.

The strategies outlined in this guide represent the difference between paying what you owe and overpaying what you don’t. Wealthy tax strategies require deliberate planning, not luck or generic compliance. A $20,000 annual tax reduction sustained over 30 years becomes $600,000 in preserved wealth, before accounting for investment growth on those savings.

High-income earners who succeed tax-wise treat planning as an investment in itself, not an afterthought. They coordinate retirement contributions with business structure decisions, align charitable giving with deduction thresholds, and time asset sales to manage capital gains across multiple years. This coordination separates those who save thousands from those who save tens of thousands annually.

Professional guidance matters more at higher income levels because the stakes grow proportionally. Tax law changes annually, your personal circumstances shift, and missed opportunities compound. Schedule a consultation with Clear View Business Solutions to review your current tax position and capture every legitimate deduction available to you.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.