Most people leave money on the table when they give to charity. They donate without thinking about how timing, asset selection, and tax planning can multiply their impact.

At Clear View Business Solutions, we’ve seen donors cut their tax bills significantly by using the right charitable giving tax strategies. This guide walks you through proven methods like donor-advised funds, appreciated asset donations, and donation timing that actually work.

Appreciated securities outperform cash donations by a significant margin. When you give long-term appreciated stocks or bonds directly to a charity, you avoid capital gains tax entirely while claiming a deduction equal to the full fair-market value. Capital gains tax consumes 20 percent of your gains at the federal level, plus state taxes. If you hold stock worth $10,000 that you bought for $2,000, selling it costs you $1,600 in federal capital gains tax alone. Donating that same stock to charity costs you nothing in capital gains tax and nets you a $10,000 deduction. You give the charity more money, reduce your tax bill, and keep more wealth.

The IRS allows deductions up to 30 percent of your adjusted gross income for appreciated assets gifting to public charities, with a five-year carry-forward for any excess. Real estate, non-publicly traded securities, and private business shares also qualify as appreciated assets you can donate before selling. Work with your broker to transfer securities directly to the charity’s account rather than liquidating and donating proceeds. This direct transfer eliminates capital gains tax-the critical step that makes this strategy work.

A Donor-Advised Funds operates like a giving account at a qualified charity where you contribute assets, claim an immediate tax deduction, and then distribute grants to charities over time. You receive the tax benefit upfront while the money grows tax-free inside the account before you grant it out. This structure works especially well during windfall years like business sales, inheritance, or strong investment gains when your income spikes.

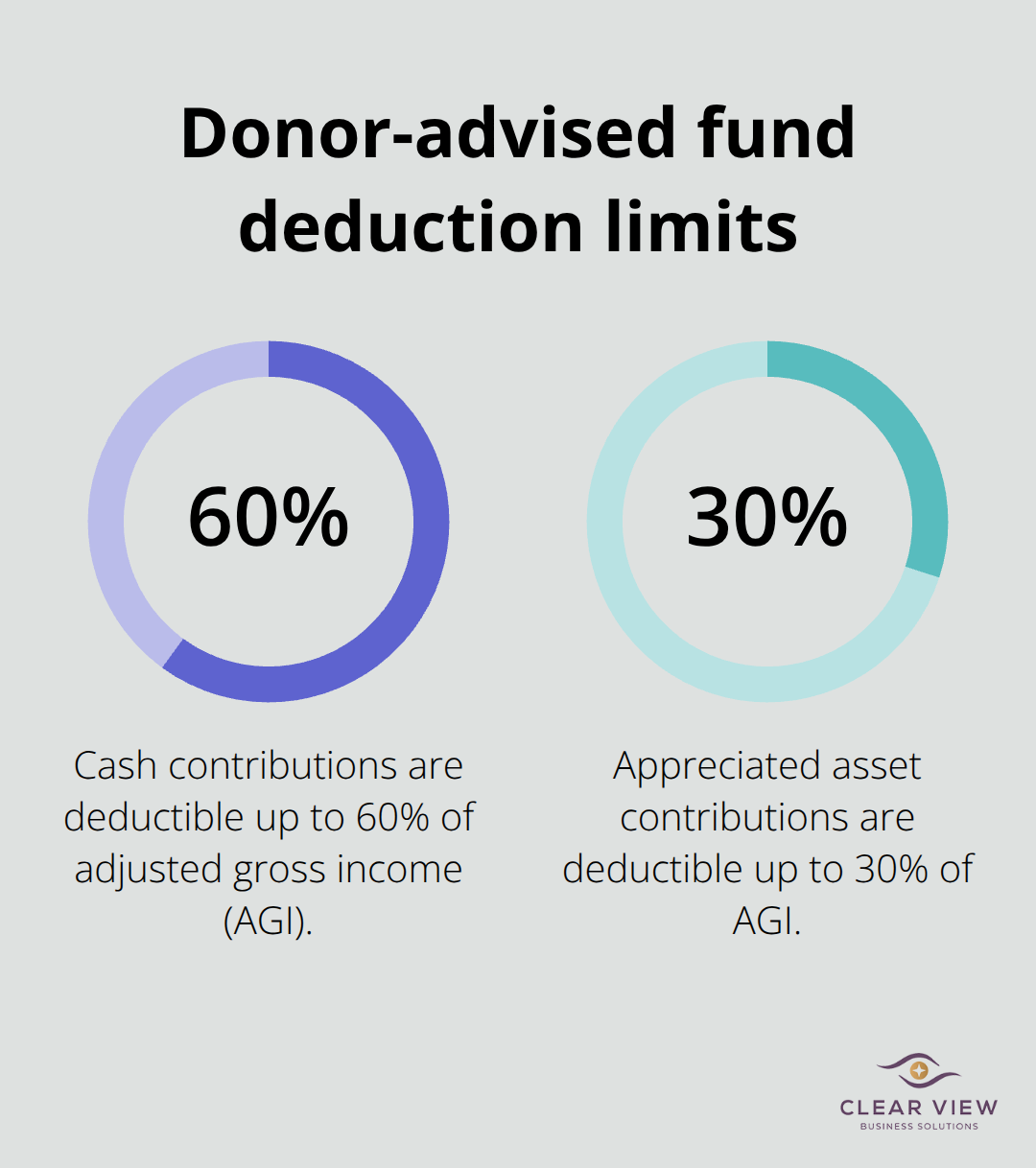

You can fund a donor-advised fund with appreciated securities, cash, or real estate, and you avoid capital gains tax when the fund sells contributed assets. The deduction limit for cash contributions is 60 percent of your adjusted gross income, with a five-year carry-forward. For appreciated assets, the limit is 30 percent of your adjusted gross income. There is no minimum contribution requirement to open an account.

This approach pairs perfectly with bunching-the strategy of combining multiple years of charitable giving into one year to exceed the standard deduction threshold and claim itemized deductions. Many donors use donor-advised funds to front-load their charitable deductions in high-income years, then grant to charities during lower-income years.

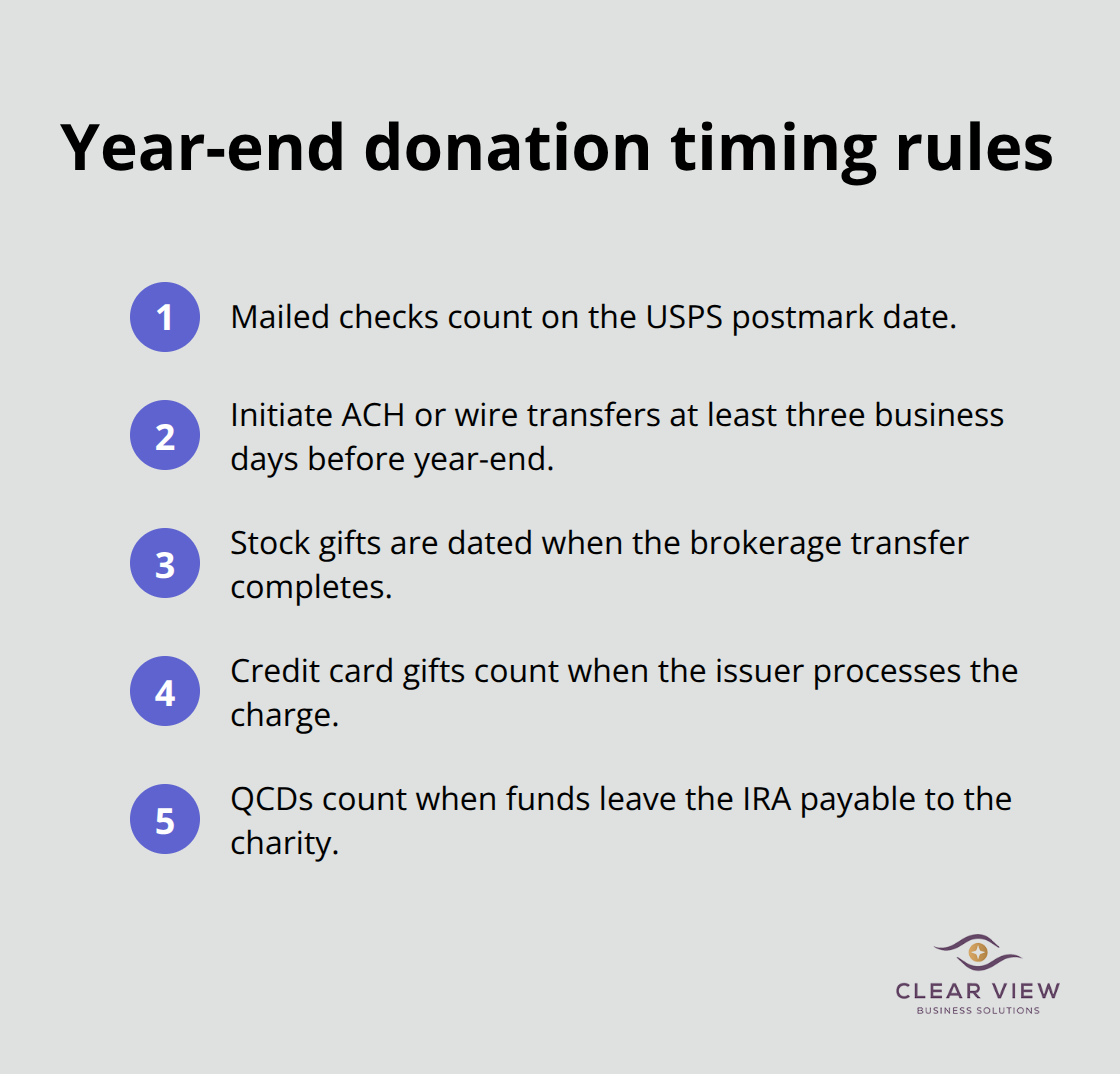

The date your donation reaches the charity determines which tax year you claim the deduction. Mailed checks count as donated on their postmark date if postmarked by December 31, but USPS machine postmarks since late December can shift the actual date, creating uncertainty. Use a Postage Validation Imprint, manual postmark, or Certificate of Mailing to lock in your intended year.

Wire transfers and ACH gifts are dated when funds credit to the charity’s account, so initiate these at least three business days before year-end. Stock transfers through your broker are dated when the transfer completes, which can take several days, so coordinate with your broker in early December. Credit card donations are dated when your card issuer processes the charge, not when you authorize the payment.

Qualified Charitable Distributions from IRAs for donors age 70½ and older count when funds leave your IRA and are payable to the charity, not when you request the distribution. QCDs offer a powerful benefit for retirees who don’t itemize deductions-the distribution counts toward your required minimum distribution without being taxed as income, effectively reducing your taxable income while supporting charity. Plan your giving method and timing together to maximize the deduction in your intended year. Understanding these timing rules sets the stage for the next critical step: structuring your overall charitable plan to work with your broader financial picture.

The standard deduction for 2025 sits at $15,000 for single filers and $30,000 for married couples filing jointly, according to IRS inflation adjustments. Less than 10 percent of taxpayers itemize deductions today because the standard deduction is simply too high for most households. This creates a significant problem for charitable donors: your gifts produce zero tax benefit unless you exceed the standard deduction threshold.

Bunching solves this problem by concentrating multiple years of charitable giving into a single tax year. If you typically give $8,000 annually, bunching three years of giving into one year creates $24,000 in itemized deductions, which exceeds your $30,000 standard deduction threshold and unlocks a real tax write-off. A donor-advised fund makes bunching remarkably straightforward. You contribute a lump sum to the fund in a high-income year, claim the full deduction immediately, then distribute grants to your chosen charities over the following years at your own pace. This approach works especially well when you receive a business sale, inheritance, or substantial investment gains. You capture the tax benefit when your income peaks, then continue supporting charities during normal years without worrying about hitting deduction thresholds again.

Combining charitable giving with your broader investment strategy requires understanding how your assets interact with your tax situation. If you hold appreciated real estate, non-publicly traded business shares, or a concentrated stock position, you can donate these assets directly to a donor-advised fund and accomplish multiple objectives simultaneously. Appreciated assets donations allow you to avoid capital gains tax on the appreciation, claim a deduction for the full fair-market value (up to 30 percent of your adjusted gross income), and the fund sells the asset without triggering any tax liability. The charity then invests the proceeds and grows the pool available for future grants. This approach beats donating cash because you give more money to charity while reducing your own tax burden.

A financial advisor or tax professional transforms charitable giving from a standalone decision into part of your complete financial picture. Your advisor can model different giving scenarios against your income projections, investment timeline, and estate plan to identify the approach that maximizes both tax savings and charitable impact. They coordinate your charitable strategy with your required minimum distributions, Medicare premium calculations, and state tax situations, which vary dramatically by location.

Tax planning firms help clients structure these multi-layered strategies by analyzing your specific numbers rather than applying generic templates. The timing of your gifts, the types of assets you donate, and the vehicles you use should all align with your financial goals and tax circumstances. This coordination sets the foundation for the next critical decision: identifying which specific mistakes most donors make and how you can avoid them.

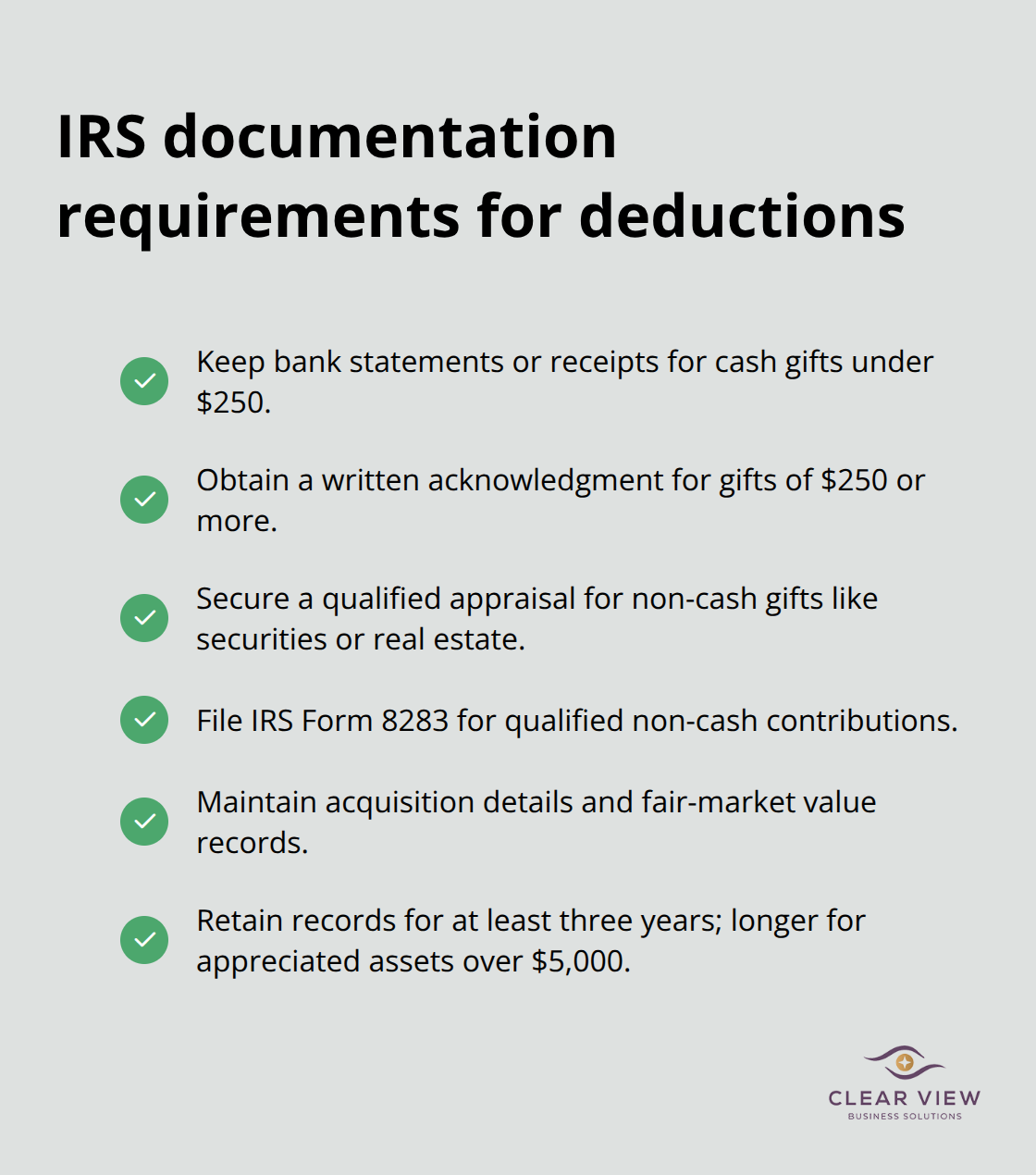

The IRS requires specific documentation to validate charitable deductions, and vague records invite audit risk. For cash gifts under $250, keep bank statements or receipts showing the charity’s name, amount, and date. For gifts of $250 or more, the charity must provide a written acknowledgment stating the amount and whether you received any goods or services in return. Many donors ignore this requirement and lose deductions entirely when the IRS challenges their claims.

For non-cash donations like appreciated securities or real estate, you need a qualified appraisal from an independent appraiser, Form 8283 filed with your tax return, and detailed records of how you acquired the asset and its fair-market value. The IRS Publication 561 provides valuation rules, but most donors skip this step and claim inflated deductions that trigger audits. Document every donation immediately with the charity’s tax identification number, your contribution amount, the asset type, and the date funds or property reached the charity’s account. Store these records for at least three years after filing your return, longer if you claim appreciated assets over $5,000.

State and local tax situations vary dramatically and directly impact your charitable deduction strategy. Some states allow charitable deductions on state returns even if you claim the standard deduction federally, while others do not. The non-itemizer charitable deduction is available for all taxpayers claiming the standard deduction, worth up to $1,000 ($2,000 for joint filers). A donor in a high-tax state benefits differently from the same giving strategy than a donor in a state with no income tax.

Additionally, not all charities qualify for tax deductions in all states. The IRS Charitable Organization Search confirms federal 501(c)(3) status, but you must verify state registration separately because some states maintain their own charity registries with different qualification rules. Foreign charitable organizations typically do not qualify for U.S. tax deductions except in rare cases under tax treaties. Private foundations and certain donor-advised fund restrictions also limit which organizations receive deductions.

Many donors donate to organizations they assume are qualified without verification, then claim deductions that the IRS later disallows. Verify your charity’s status through the IRS tool before donating, and confirm that your state allows deductions for that specific organization type. Work with a tax professional to model how state taxes affect your overall charitable strategy, especially if you live in a high-tax state or plan large gifts. This verification step protects you from audit risk and ensures your donations produce the tax benefits you expect.

Charitable giving tax strategies produce real results only when you implement them with intention. Donating appreciated assets eliminates capital gains tax entirely, donor-advised funds let you capture deductions in high-income years while supporting charities over time, and precise timing ensures your gifts count in the year you intend. Your specific situation determines which approach works best-a business owner facing a sale needs different planning than a retiree managing required minimum distributions.

Strategic planning separates donors who save thousands annually from those who leave money on the table. Your state tax situation, investment portfolio, and charitable goals all influence the optimal charitable giving tax strategy. This complexity is why working with a tax professional matters, as they model scenarios against your actual numbers and coordinate your charitable giving with your broader financial picture. Start by documenting your current giving patterns and identifying your charitable goals for the next three to five years, then work with a professional to model how appreciated asset donations, donor-advised funds, and donation timing interact with your income, investments, and estate plan.

We at Clear View Business Solutions help individuals and small business owners structure charitable giving strategies that align with their complete financial situation. Contact Clear View Business Solutions to discuss how charitable giving tax strategies fit into your overall financial plan and start maximizing both your tax benefits and charitable impact.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.