Roth conversions can save you thousands in taxes, but only if you make the right moves at the right time. The decisions you make in 2026 will shape your tax bill for years to come.

At Clear View Business Solutions, we’ve seen too many people convert without a plan and end up in higher tax brackets than necessary. This guide walks you through the strategy, the pitfalls, and exactly how to approach your conversion decision this year.

A Roth conversion is not a withdrawal. This distinction matters because it changes everything about how taxes and future income work. When you withdraw from a traditional IRA, you pull out money and pay taxes on it-that’s income for the year. A Roth conversion moves pre-tax dollars from a traditional IRA, 401(k), 403(b), SEP, or SIMPLE IRA into a Roth account, and you pay ordinary income tax on the converted amount in that same year. The critical difference is what happens next. After conversion, those funds grow tax-free forever, and qualified withdrawals in retirement are completely tax-free. With a traditional IRA withdrawal, you pay taxes now and again later on any growth.

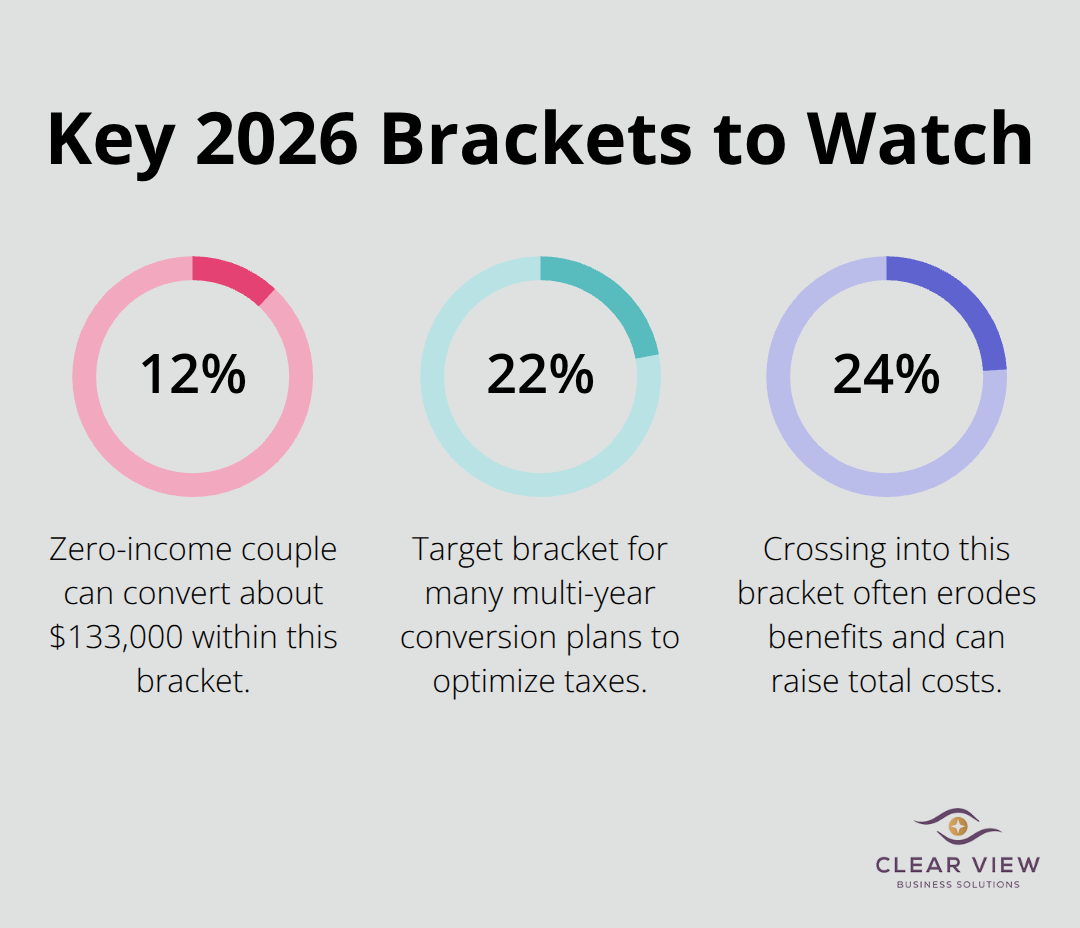

The 2026 standard deduction for married filing jointly is $32,200, with an additional $1,650 per spouse aged 65 or older. This creates immediate tax-free space you can fill with conversions before hitting higher brackets. A zero-income couple can convert roughly $133,000 within the 12% tax bracket alone.

Many people delay conversions thinking they’ll be in lower brackets later, but that’s backward. The years between retirement and required minimum distributions starting at age 73 are your optimal window. Once RMDs begin, the IRS forces you to take taxable distributions whether you need them or not, crushing your ability to control income and fill bracket space.

The pro-rata rule is where conversions get complicated if you own multiple IRAs. The IRS requires you to aggregate all your traditional, SEP, and SIMPLE IRAs when calculating how much of a conversion is tax-free. You cannot cherry-pick after-tax basis and convert only that portion. If you have a $350,000 traditional IRA with $50,000 in after-tax basis and convert $100,000, only about $14,300 of that conversion escapes taxation because the IRS treats all your IRAs as one pool. This rule catches people off guard and inflates conversion taxes significantly.

Medicare premiums also spike based on modified adjusted gross income from two years prior, creating what advisors call IRMAA cliffs. A single filer at $109,000 MAGI triggers higher Part B and Part D premiums; married filers face the equivalent around $218,000. A $100,000 conversion in 2026 could add thousands in annual Medicare costs in 2028. Scenario planning matters here. A couple aged 63 and 62 with low current income might convert $85,000 to $100,000 annually for ten years, staying within the 22% bracket while saving roughly $52,000 in taxes over that decade, with over $120,000 in lifetime tax-free growth. High earners need different math. A 66-year-old with pension income should limit conversions to $50,000 to $65,000 annually to avoid IRMAA thresholds, spreading the strategy over seven years. A tax professional can model these scenarios across multiple years and prevent expensive mistakes that you cannot undo. The right conversion amount fills up to the top of your current bracket without crossing into the next bracket or triggering an IRMAA cliff-and that calculation shifts based on your filing status, income, and state taxes.

The years between retirement and age 73 represent your conversion goldmine, and 2026 is the perfect time to act if you fall into that window. Most people squander this opportunity by waiting for a market crash or assuming they will land in a lower bracket later. That assumption fails. Once required minimum distributions start at age 73, you lose control entirely. The IRS forces you to take taxable distributions whether you need the money or not, and those forced distributions fill your tax brackets regardless of your preferences. A couple aged 63 and 62 with minimal income right now sits in the 12% bracket with roughly $133,000 of unused bracket space. Converting $85,000 to $100,000 annually for the next decade keeps them in the 22% bracket while saving approximately $52,000 in total taxes over ten years. That calculation reflects real numbers across multiple years, not theory. The window closes fast. In five years, when they approach 68 and 67, Social Security will kick in, pension income may start, and suddenly that same conversion pushes them into the 24% or 32% bracket. Starting now while income stays low is the only rational move.

Market timing matters, but not the way most people think about it. Converting when your account value drops 15% or 20% means you move fewer shares at the same tax cost. If your $500,000 traditional IRA falls to $425,000 during a market downturn, converting $100,000 costs the same taxes but you transfer a larger percentage of your remaining assets into tax-free growth. A 66-year-old with $800,000 in a traditional IRA should not wait for the perfect market moment. Instead, spread conversions across multiple years so market volatility smooths out naturally. This approach removes the pressure to time the market perfectly and lets you execute a consistent strategy regardless of what stocks do in any given quarter.

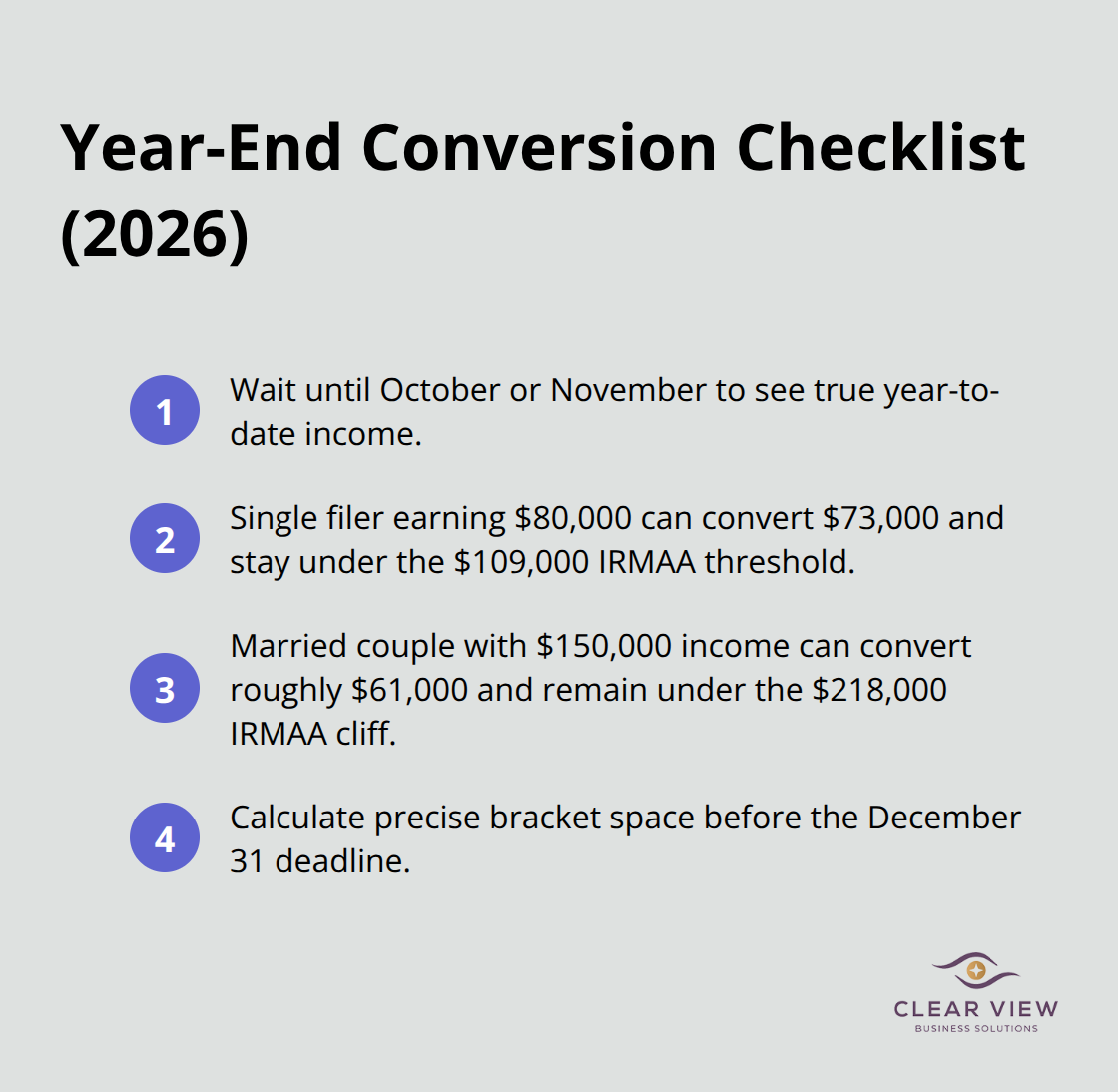

December 31 marks your deadline to know your full income picture for 2026. If you converted $50,000 in January without knowing you would earn a large bonus or consulting income in November, you might have overpaid taxes by thousands. Waiting until October or November lets you see your actual year-to-date income, calculate your exact bracket space, and convert the precise amount to fill it without crossing into the next bracket or triggering an IRMAA cliff. A single filer earning $80,000 from work can safely convert $73,000 to stay under the $109,000 IRMAA threshold for Medicare premiums.

A married couple with $150,000 combined income can convert roughly $61,000 to stay under the $218,000 IRMAA cliff. These numbers shift based on state taxes, deductions, and filing status, which is why working with a tax professional to model your specific 2026 income and conversion capacity makes the difference between saving $10,000 and losing $5,000 to preventable tax mistakes.

A tax advisor models multiple scenarios across several years to prevent expensive mistakes that you cannot undo. The right conversion amount fills up to the top of your current bracket without crossing into the next bracket or triggering an IRMAA cliff, and that calculation shifts based on your filing status, income, and state taxes. A high earner aged 66 with pension income should limit conversions to $50,000 to $65,000 annually to avoid IRMAA thresholds, spreading the strategy over seven years. A high-net-worth couple aged 58 and 56 might convert $150,000 to $200,000 per year up to the 24% bracket over 15 to 17 years, potentially converting $2.25 million to $3 million and significantly reducing future RMDs. These scenarios require professional guidance because the interaction between conversions, Social Security, pensions, and Medicare premiums creates complexity that spreadsheets alone cannot capture.

The biggest conversion mistake we see is converting too much in a single year and waking up to a tax bill that erases half the benefit. A 65-year-old married couple with $120,000 in combined income converts $150,000 without modeling the full impact. They pay roughly 24% on the conversion, but the conversion pushes them into the 32% bracket on the tail end, and their Medicare premiums spike by $3,000 annually starting two years later due to IRMAA. That $36,000 IRMAA hit over a decade wipes out any tax savings from the conversion itself.

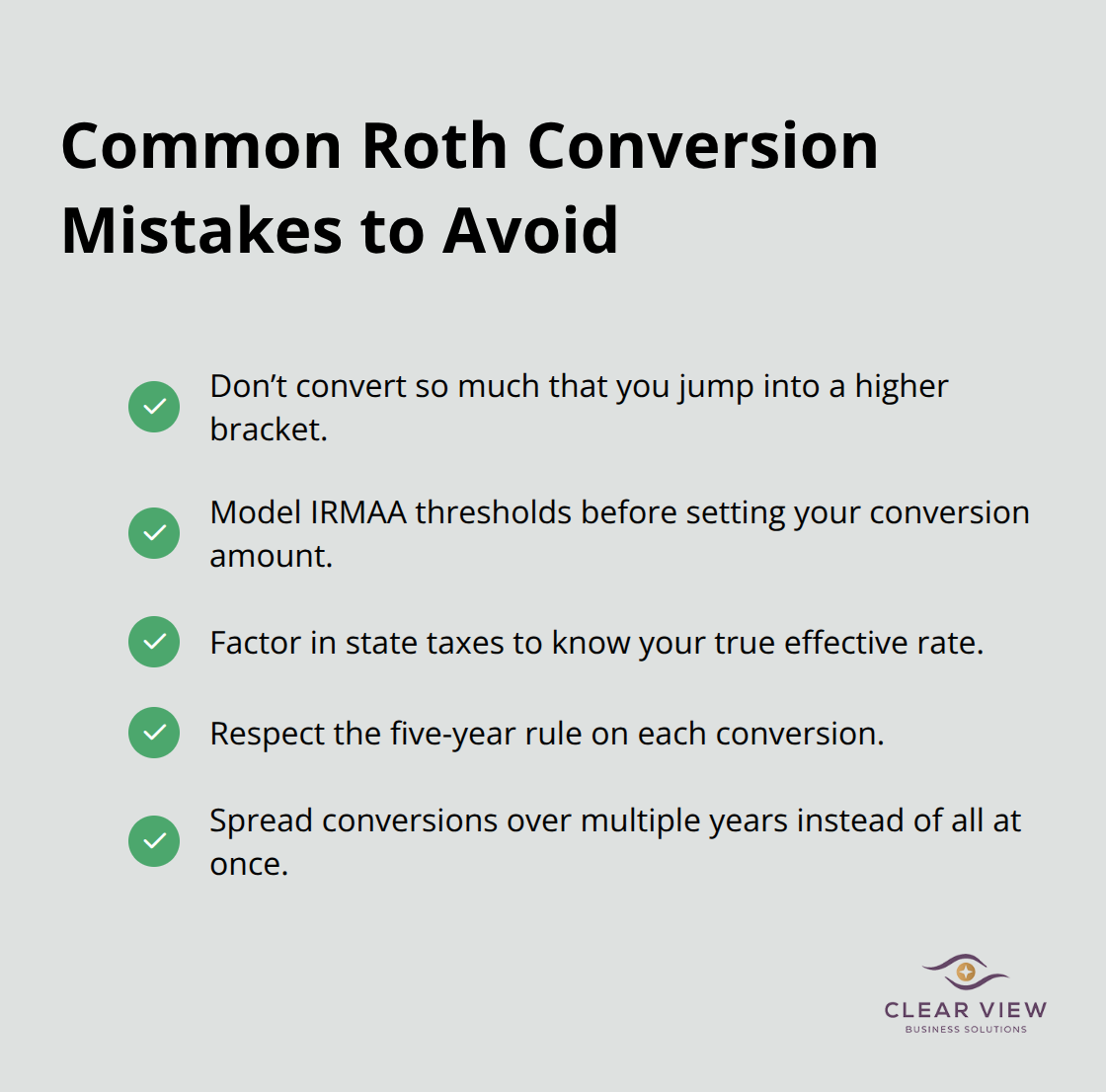

The solution is simple but requires discipline: fill your current bracket, stop, and wait until next year. A couple in the 22% bracket with $61,000 of unused bracket space should convert exactly that amount, not a penny more. That math comes from the 2026 MFJ brackets where the 22% bracket tops out at $211,400. If you earn $150,000, you have $61,400 of room to fill. Convert $61,000, pay roughly 22% in taxes, and leave the remaining bracket space for future years when income may shift again. The discipline to convert less feels wrong when you try to reduce future RMDs, but converting more creates taxes and IRMAA cliffs that cost far more than you save.

State taxes destroy conversion math in high-tax states and nobody plans for them. A couple living in California converting $150,000 faces 9.3% state tax on top of the federal 24%, bringing the total to 33.3%. That same conversion in Florida or Texas faces only federal taxes. High-income earners in states like New York, New Jersey, and California pay 10% to 13% in combined state and local taxes, which means your conversion math is completely different depending on geography.

A professional tax advisor models your specific state impact before recommending a conversion amount because ignoring state taxes leads to overpaying by thousands. If you live in a high-tax state, your conversion capacity shrinks by roughly one-third compared to what federal brackets suggest, and that changes the entire strategy. A couple with $100,000 of federal bracket space might only have $65,000 of true bracket space after accounting for California taxes, which means converting $100,000 pushes you into an effective combined rate of 32% to 35% instead of 24% federally.

The five-year rule on Roth conversions creates a separate trap that catches people who need emergency access to their money. Each Roth conversion has its own five-year holding period, starting on January 1 of the year you convert. If you convert in 2026 and withdraw the converted amount in 2028, you may pay a 10% early withdrawal penalty plus ordinary income taxes on any earnings, even if you are over 59½. Roth contributions themselves can be withdrawn anytime penalty-free, but conversions are treated differently and the five-year clock is strict.

The fix is straightforward: never convert money you might need within five years. If you are 58 years old and converting at age 58, the five-year clock expires when you turn 63, which is before you can access penalty-free withdrawals at 59½ anyway. For people under 59½, the five-year rule creates a hard deadline that must align with your actual retirement date or cash flow needs. A 55-year-old converting $100,000 should not touch that money until age 60 minimum, preferably 65, because the five-year rule plus the 59½ age requirement stack together. The conversion window between retirement and RMDs that we discussed earlier assumes you can leave the converted funds alone for at least five years, which means this strategy works best for people aged 63 and older with secure income sources outside their IRA.

Roth conversion guidance for 2026 comes down to three core decisions: convert during your low-income years before RMDs start, fill your tax bracket without crossing into the next one, and account for Medicare premiums and state taxes that most people ignore. Converting $150,000 when you have only $61,000 of bracket space costs thousands in unnecessary taxes and IRMAA penalties that persist for a decade. Converting $85,000 to $100,000 annually over ten years while staying in the 22% bracket saves roughly $52,000 in taxes and generates over $120,000 in lifetime tax-free growth.

A tax professional models multiple years of conversions across your specific income, state taxes, and Medicare thresholds to capture the interaction between Social Security, pensions, conversions, and IRMAA cliffs. They show you exactly how much to convert this year, next year, and the year after that to maximize tax efficiency without triggering expensive mistakes you cannot undo. They also account for the five-year rule on converted funds and align your conversion timeline with your actual retirement date and cash flow needs.

Work with a tax professional who will model your numbers and help you execute a plan that saves real money over decades. Contact Clear View Business Solutions to discuss your Roth conversion strategy with an advisor who understands how conversions interact with your overall financial picture and can guide you through the complexity of 2026 planning.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2025 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.