Moving out is one of the biggest financial decisions you’ll make. Most people underestimate the costs involved, from deposits and first month’s rent to furniture and utilities.

At Clear View Business Solutions, we’ve helped countless people navigate financial planning for moving out successfully. This guide walks you through assessing your current finances, building a realistic moving budget, and establishing a solid financial foundation in your new place.

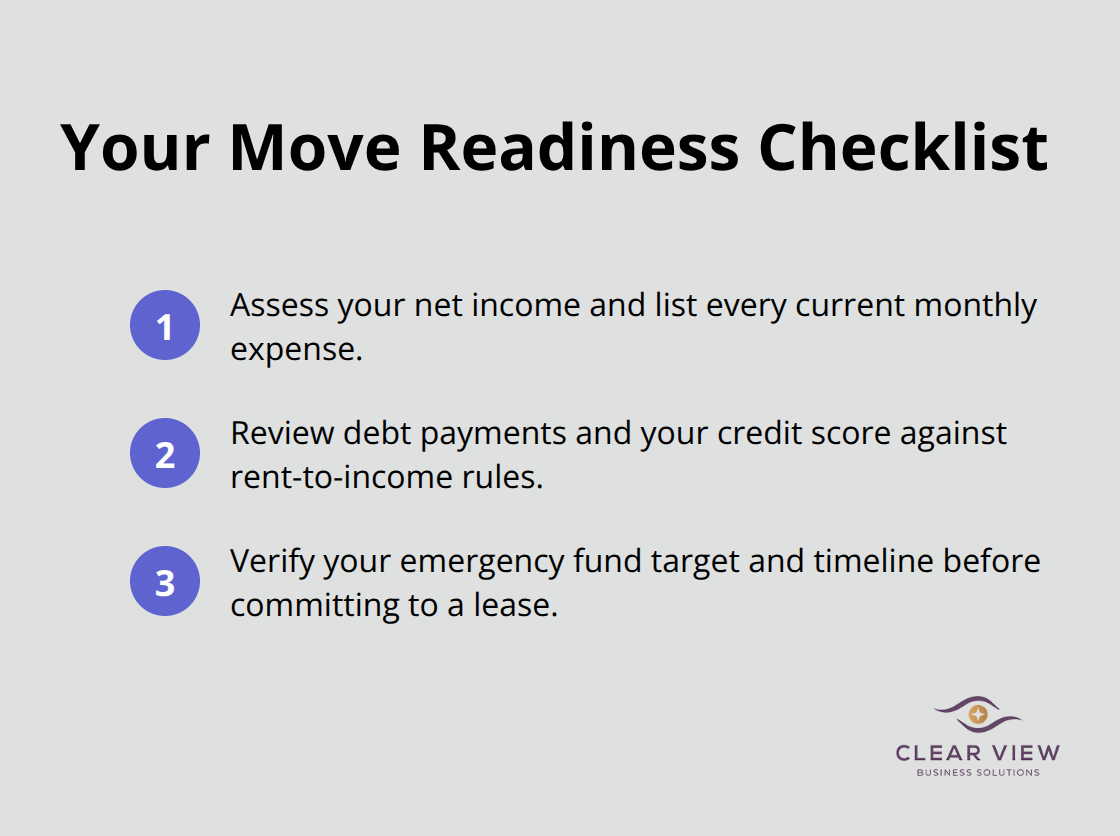

Before you can plan a realistic move, you need an honest picture of your money right now. Calculate your actual take-home pay after taxes, insurance, and retirement contributions-this is what you actually have to work with each month, not your gross salary. List every expense you currently pay: rent, utilities, debt payments, groceries, transportation, subscriptions, everything. Most people are shocked when they add this up. A real example from someone planning to move shows net monthly income of $3,580 after deductions, with fixed monthly costs totaling $1,570 before housing. That left $2,010 for rent and other expenses. Without this breakdown, you’ll make guesses instead of decisions.

Your credit score and existing debt directly affect whether you can afford to move. Landlords typically require proof that you earn at least 40 times the monthly rent in annual gross income, or they use the three times rent rule where your monthly income must be three times the rent amount. If you’re carrying significant debt payments, those reduce what’s left for housing. Someone with a $530 monthly debt payment needs to account for that before committing to an expensive apartment. Check your credit score now at no cost through your bank or a service like Credit Karma. If your score is below 650, work on paying down high-interest debt before moving. Landlords often run credit checks and may deny your application or charge higher deposits if your score is low. Your debt obligations are real constraints on your moving budget, not obstacles to ignore.

You need emergency savings before and after moving. Financial advisors recommend 3 to 6 months of living expenses set aside, though most people start with less. If your total monthly expenses including rent will be $2,100, try for at least $6,300 in savings before you move. Someone with $5,000 saved and monthly expenses of $1,800 has barely 2.7 months of coverage, which is thin. Moving costs money upfront: application fees, security deposits, first month’s rent, and potentially renter’s insurance around $28.62 monthly according to Sonnet Insurance. After paying these one-time costs, your emergency fund shrinks further. If you don’t have 3 months of expenses saved, either delay moving, increase your income with a second job, or commit to building the fund faster after you move. Moving without this cushion means one car repair or job loss puts you in crisis mode.

With your financial snapshot in hand, you’re ready to build a realistic moving budget. The next section walks you through estimating actual moving costs, calculating first-month expenses, and setting a savings timeline that works for your situation.

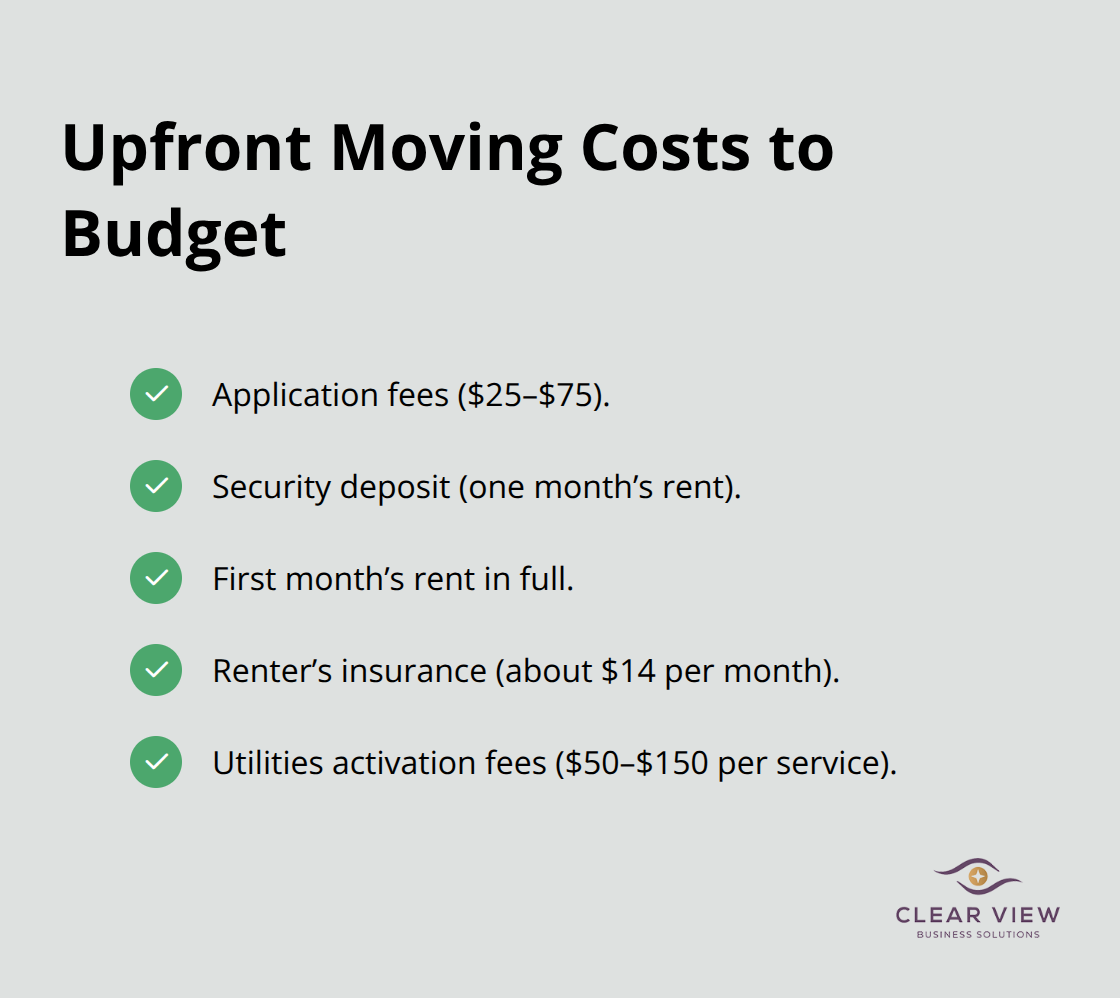

Moving costs shift dramatically based on distance and volume. A local move within 50 miles costs $25 to $50 per hour per mover, while long-distance relocations use weight-based pricing starting around $0.60 per pound according to the Federal Motor Carrier Safety Administration. A 2,000 square foot home averages 7,000 to 10,000 pounds, which means interstate moves range from $800 to $12,000 depending on distance and services you select. The cheapest time to move falls between October and March, with weekday moves costing 15 to 25 percent less than weekends. You should obtain three binding quotes from licensed interstate movers to compare actual prices instead of estimating. DIY truck rentals cost less upfront but require your own labor and efficient packing, while full-service movers handle everything but charge significantly more. Beyond the truck itself, you need to budget for application fees (typically $25 to $75), security deposits equal to one month’s rent, first month’s rent in full, and renter’s insurance around $14 monthly. One-time setup costs also include utilities activation fees, which vary by region but often run $50 to $150 per service.

A person moving from New York City to Nashville with moderate belongings faces roughly $2,685 to $3,571 for a DIY move or $3,571 to $5,342 hiring professional movers, plus deposits and first month’s rent on top of that total.

Your first month proves expensive because you pay upfront for things you’ll later pay monthly. If rent is $1,200, you owe $1,200 for the first month plus a refundable security deposit of another $1,200, totaling $2,400 just for rent and deposit before utilities arrive. Utilities depend on your region and season, but you should budget $150 to $250 for electricity, water, internet, and gas combined during your first month, then adjust based on actual bills. Renter’s insurance protects your belongings and covers liability if someone is injured in your apartment. Most landlords won’t finalize your lease until insurance is active, so add this to your upfront costs. If you move with roommates, split these costs evenly but document the arrangement in writing to prevent disputes about who owes what. Someone with $3,580 monthly net income and $1,570 in existing expenses can comfortably afford rent around $1,095 to $1,200 monthly using the 30 percent rule, leaving roughly $500 to $750 for utilities and other living costs after rent and deposits are paid.

You should set a concrete savings target and work backward from your moving date. Add your estimated moving costs, deposits, first month’s rent, utilities deposits, furniture if needed, and a $1,000 buffer for unexpected costs. If that total is $6,500 and you can save $400 monthly, you need 16 months to move comfortably without draining your emergency fund. Most people underestimate how long this takes and move too soon, landing in financial stress. If your timeline is shorter, increase income with a second job or reduce other expenses temporarily to accelerate savings. You should track spending weekly instead of monthly to spot where money actually goes and find cuts faster. Someone saving for a move should avoid major purchases, subscriptions, or lifestyle increases until after relocating and stabilizing their new budget. Once you hit your target savings number, you can move forward confidently knowing you have real money behind your decision.

With your moving costs calculated and savings target set, the next step involves building the monthly budget you’ll live on after you arrive in your new place. The following section covers how to structure your ongoing expenses, protect yourself with an emergency fund, and plan for financial goals beyond just covering rent and utilities.

Your first month in a new place feels financially stable because you’ve saved and planned carefully. That feeling vanishes quickly once you realize your actual monthly expenses don’t match what you estimated. Track your real spending for the first three months after moving. This isn’t theoretical budgeting-it’s real data about where your money actually goes. If you estimated groceries at $250 monthly but spend $340, utilities at $150 but pay $210, and gas at $80 but use $120, your carefully planned budget collapses.

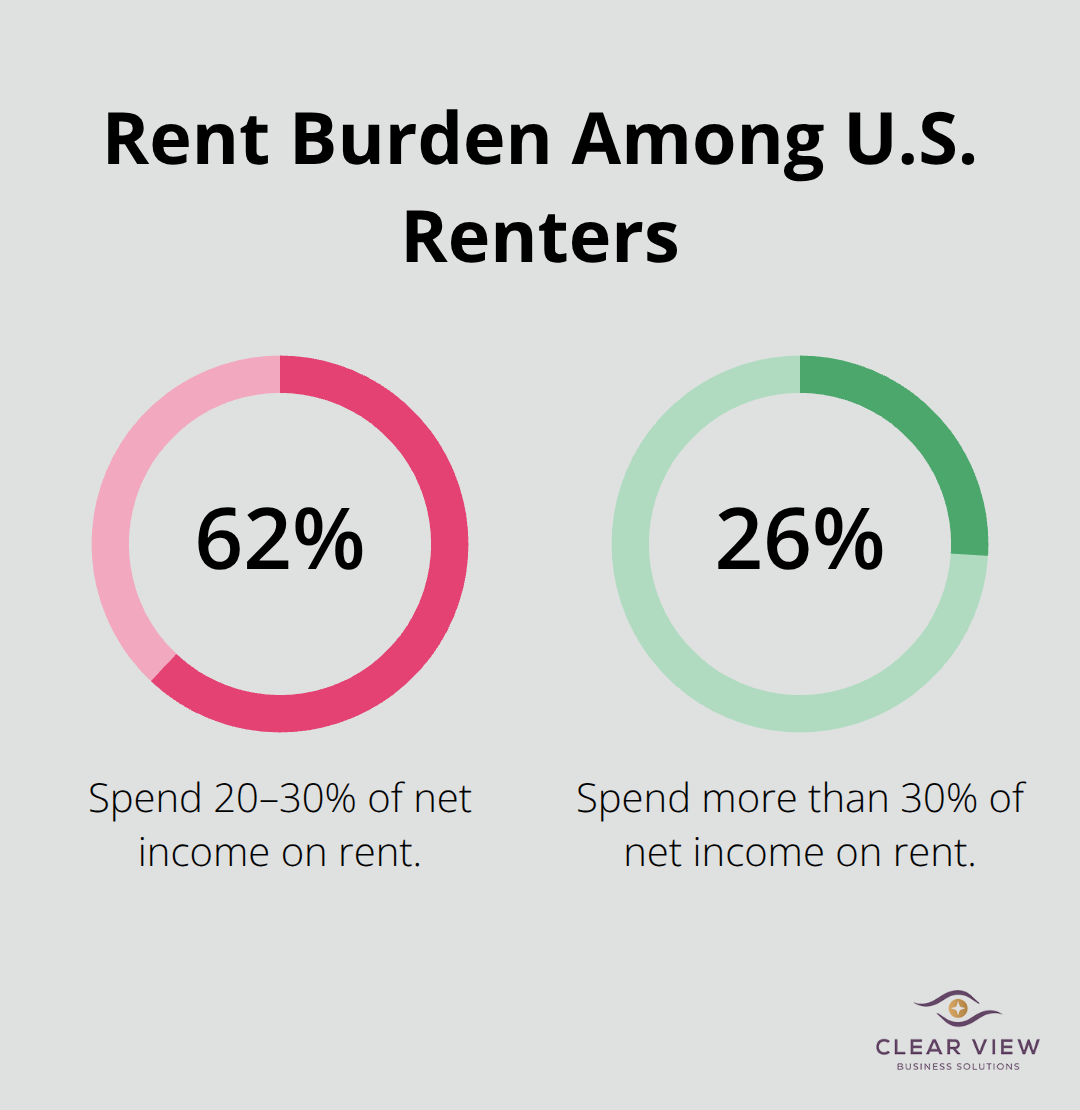

A CreditDonkey poll found that 62 percent of renters spend between 20 and 30 percent of their net income on rent, while 26 percent spend more than 30 percent. If you’re in that higher group, your remaining money for food, transportation, entertainment, and personal care shrinks dangerously.

The 50/30/20 rule is a simple way to plan your budget, but adjust it to your situation. Use a spending tracker or simple spreadsheet to record actual expenses in categories: housing, utilities, groceries, transportation, phone, subscriptions, entertainment, and personal care.

After three months, you’ll see your real spending patterns and adjust accordingly. If your actual expenses exceed your income, cut discretionary spending first-streaming services, dining out, and entertainment are easier to trim than food or transportation. If cuts aren’t enough, you need more income, not a different budget.

Your emergency fund becomes critical immediately after moving because unexpected costs arrive without warning. A car repair costs $800, your laptop dies at $1,200, or your apartment needs emergency repairs you’re responsible for as a renter. Without savings already in place, you’ll use credit cards and build debt right when you should be building stability.

Try to restore your emergency fund to three months of expenses within six months of moving. If your monthly expenses total $2,100, that’s a $6,300 target. Save aggressively by cutting expenses or taking on extra work temporarily. Beyond emergencies, plan for irregular but predictable costs that don’t fit monthly categories: car insurance paid quarterly, medical deductibles, holiday gifts, and annual subscriptions. Budget $100 to $150 monthly into a separate account for these expenses so they don’t derail your regular budget when they arrive.

Long-term financial goals matter less than stability right now, but don’t ignore them completely. Contribute to tax-advantaged accounts like IRAs or HSAs to reduce your taxable income and build retirement savings simultaneously. At $3,580 monthly net income, even 5 percent toward future goals is $179 monthly. Small consistent contributions compound over time and prevent you from reaching age 35 with zero retirement savings. Your financial foundation strengthens through honest tracking, realistic adjustments, and consistent saving-not through perfect initial planning.

Moving out successfully requires honest financial assessment, realistic budgeting, and consistent follow-through after you sign the lease. Your financial plan for moving out only works if you track spending monthly, adjust when reality differs from estimates, and rebuild your emergency fund immediately after relocating. Small adjustments early prevent financial stress from building into crisis.

Long-term stability comes from consistent saving, even small amounts, and maintaining your emergency fund at three to six months of expenses. Contribute to retirement accounts, avoid taking on new debt while adjusting to your new financial reality, and compare actual expenses to your budget during your first six months in your new place. Your financial foundation strengthens through action, not intention.

If financial planning feels overwhelming or your situation involves complex tax considerations, Clear View Business Solutions offers personalized financial advisory and tax planning to help you make informed decisions. Whether you’re managing your first move or coordinating finances across multiple responsibilities, professional guidance simplifies the process and ensures you’re maximizing your financial position.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.