Most people know they should save more money, but they don’t have a clear plan to get there. Without a structured approach to wealth management and financial planning, your income disappears faster than you can build real wealth.

At Clear View Business Solutions, we’ve seen firsthand that the difference between people who build wealth and those who don’t comes down to one thing: a solid financial plan. This guide walks you through the exact steps to take control of your finances and start building lasting wealth.

You cannot build wealth if you don’t know your starting point. Most people have a vague sense of whether they’re doing okay financially, but vague doesn’t cut it. You need exact numbers. Start by recording every dollar that comes in and every dollar that goes out for at least one month. The Consumer Financial Protection Bureau recommends tracking your spending to identify where your money actually goes, not where you think it goes.

Many people discover they spend more than they realized on subscriptions, dining out, and impulse purchases. Open a simple spreadsheet or use a free app and record transactions daily. Don’t estimate or round numbers. The precision matters because small leaks in your budget compound into thousands of dollars lost annually. Once you have a month of data, calculate your net income after taxes and list every expense category. You’ll spot patterns immediately.

One client discovered she was paying for four streaming services she barely used. Another found he was spending $340 monthly on coffee shop visits. These aren’t moral judgments-they’re data points that show you where adjustments are possible.

Your net worth tells you more than your paycheck ever could. List everything you own minus everything you owe. Include your home, vehicles, retirement accounts, savings accounts, and investment accounts on the asset side. On the liability side, add mortgage balances, car loans, credit card debt, student loans, and any other obligations.

Calculate your net worth by subtracting your total liabilities from your total assets. Financial well-being isn’t determined by income alone. Write down this number today. You’ll use it as your baseline to measure progress over time.

Don’t say you want to retire someday or save for a house eventually. Instead, write that you want $50,000 for a down payment in five years, or you want to retire at 62 with $1.2 million saved. The more specific and measurable your goals, the more actionable your plan becomes.

Separate your goals into short-term (under one year), mid-term (one to five years), and long-term (five years and beyond). This framework helps you decide where money should go right now and prevents you from spreading resources too thin across competing priorities. With your current financial situation mapped out and your goals clearly defined, you’re ready to move forward with a strategic plan that actually works.

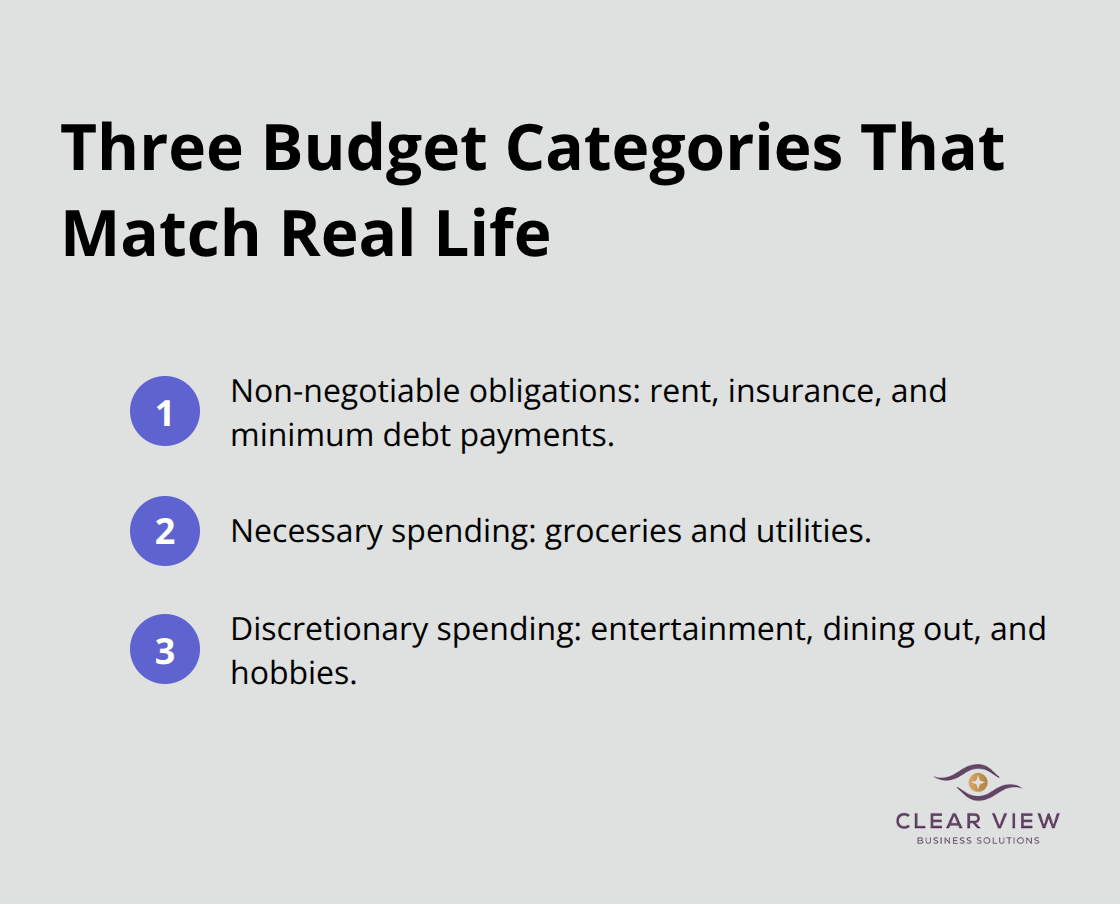

The 50/30/20 budgeting rule sounds clean on paper, but it fails for most people because their actual lives don’t fit into those percentages. We’ve worked with clients who tried to force their spending into this framework and abandoned their budget within weeks. Your budget only works if it matches reality.

Start with your tracked income and expenses from the previous month. Separate everything into three categories: non-negotiable obligations like rent, insurance, and minimum debt payments; necessary spending like groceries and utilities; and discretionary spending on entertainment, dining out, and hobbies. The Consumer Financial Protection Bureau found that people who write down their bill due dates and align them with their income weeks stay on track significantly better than those who don’t.

Request your landlord or service providers to shift due dates if they cluster around the same week.

Once you map your baseline spending, identify what you actually want to prioritize. If travel matters more to you than a luxury car, your budget should reflect that trade-off. If you have kids in activities, that’s a line item, not a luxury. Build your budget around your lifestyle, not some generic template. Review it weekly for the first month, not monthly. Weekly reviews catch overspending before it becomes a pattern. After four weeks, you’ll see which categories need adjustment. Most people find they can cut 10 to 15 percent from discretionary spending without feeling deprived once they see where money actually goes.

An emergency fund prevents you from derailing your wealth-building plan when unexpected costs hit. The CFPB recommends starting with emergency fund covers three to six months of essential expenses, though your specific number depends on your job stability and family situation. Someone in a stable corporate role might try three months of expenses. A freelancer or someone with irregular income should try six months.

Calculate this by taking your essential monthly spending (rent, utilities, insurance, minimum debt payments, food) and multiplying by the appropriate number. If your essentials total $3,500 monthly, your emergency fund target is $10,500 to $21,000. This sounds large, but it’s the difference between using a credit card at 18 percent interest when your car breaks down and having cash on hand. Open a separate high-yield savings account specifically for this fund. Keep it away from your checking account so you’re not tempted to raid it.

Set up automatic transfers from each paycheck, even if it’s only $50 initially. The CFPB research shows that automatic transfers work better than manual ones because they remove the decision-making step. Once your emergency fund reaches your target, redirect those monthly contributions toward debt reduction or investing.

Debt matters more than you think because high-interest balances work against you every single month. High-interest debt should be eliminated aggressively. List all your debts with their interest rates. Pay minimums on everything, then attack the highest-interest debt with extra payments. This approach saves the most money over time compared to paying off smallest balances first.

If you carry $8,000 in credit card debt at 19 percent APR, you’re paying roughly $1,520 annually in interest alone. Paying an extra $200 monthly cuts that debt down in about 40 months instead of 60, saving you over $3,000 in interest charges. With your budget in place, your emergency fund started, and your debt reduction strategy clear, you’re ready to shift focus toward building wealth through strategic investments.

Once you’ve eliminated high-interest debt and built your emergency fund, your money needs to work harder than sitting in a savings account. Too many people leave thousands of dollars on the table because they don’t understand how to structure their investments or take advantage of tax-advantaged accounts. The difference between someone who builds $500,000 in wealth and someone who builds $1.2 million often comes down to investment strategy and account selection, not just how much they save.

Investment returns compound over decades, and the earlier you start, the more dramatic the effect becomes. A person who invests $500 monthly starting at age 25 and achieves an average 7% annual return will have approximately $1.1 million by age 65, assuming consistent contributions. The same person starting at 35 ends up with roughly $470,000. That 10-year delay costs over $600,000 in final wealth due to compound growth. Your investment portfolio should reflect your timeline and risk tolerance, not chase whatever market is hot this month. If you have 30 years until retirement, you can weather market downturns and should hold more stocks. If retirement is five years away, your portfolio should look entirely different with more bonds and stable assets. Most people fail here because they either avoid investing altogether or panic-sell when markets drop 15 percent, locking in losses at the worst possible time.

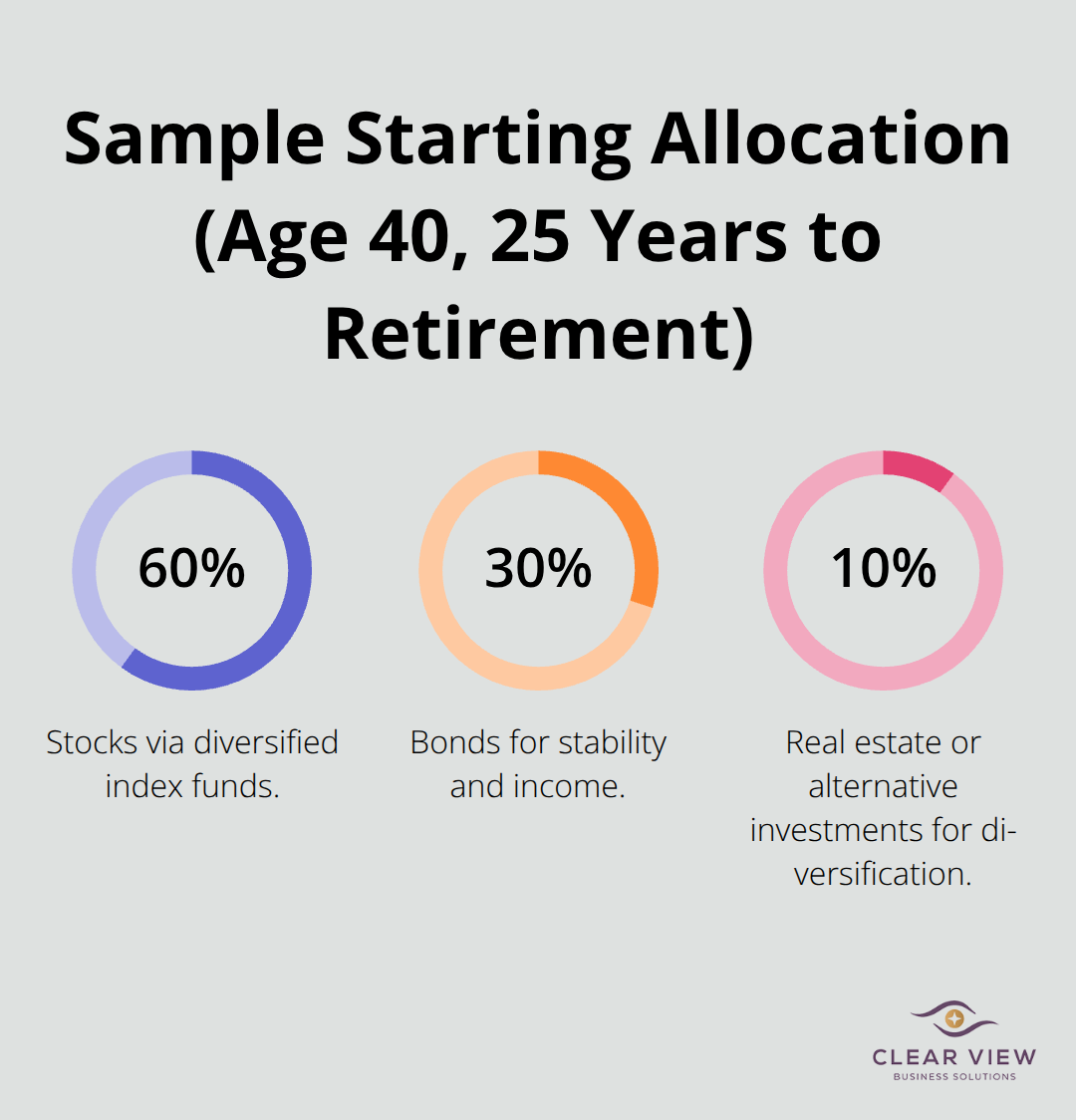

Diversification isn’t just financial advice; it’s the only reliable way to reduce risk without sacrificing growth. A portfolio holding only technology stocks might soar 40 percent one year but crash 30 percent the next, keeping you awake at night. The same money spread across US stocks, international stocks, bonds, and real estate investment trusts smooths those swings significantly. A balanced portfolio might return 8 percent one year and 6 percent the next, but you sleep better and stay invested long enough to benefit from compounding. Don’t spread your money so thin that you hold 50 different investments; that’s just busy work. Instead, hold 5 to 8 core positions that cover different asset classes and sectors. Low-cost index funds make this simple because one fund can give you exposure to 500 companies. If you have $50,000 to invest and you’re 40 years old with 25 years until retirement, a reasonable starting allocation might be 60 percent stocks (through diversified index funds), 30 percent bonds, and 10 percent real estate or alternative investments. As you age, that ratio shifts toward bonds and away from stocks to protect gains.

This is where most people make their biggest mistake. They invest money in regular taxable brokerage accounts while leaving employer 401k matches unclaimed or IRAs unfunded. A 401k with an employer match is free money with an immediate return. If your employer matches 3 percent of your salary and you earn $60,000, that’s $1,800 annually the company will contribute if you contribute $1,800 yourself. Refusing that match means leaving $1,800 on the table every single year. Contribute enough to your 401k to capture the full employer match, even if it means cutting discretionary spending. After securing the match, max out a Roth IRA if you’re eligible. For 2026, that limit is $7,000 annually. Unlike a traditional 401k, Roth contributions grow tax-free and you withdraw them tax-free in retirement. A 25-year-old who contributes $7,000 annually to a Roth IRA from now until age 65 will have approximately $2.7 million (assuming 7 percent average returns), and they’ll owe zero taxes on that entire amount. That’s transformational wealth-building. After maxing your Roth, increase your 401k contributions beyond the match limit. The 2026 limit is $23,500 annually for people under 50. Higher-income earners should investigate SEP IRAs or Solo 401ks if they’re self-employed, which allow contributions up to $69,000 annually. These accounts exist specifically to help you build wealth while reducing your current tax burden.

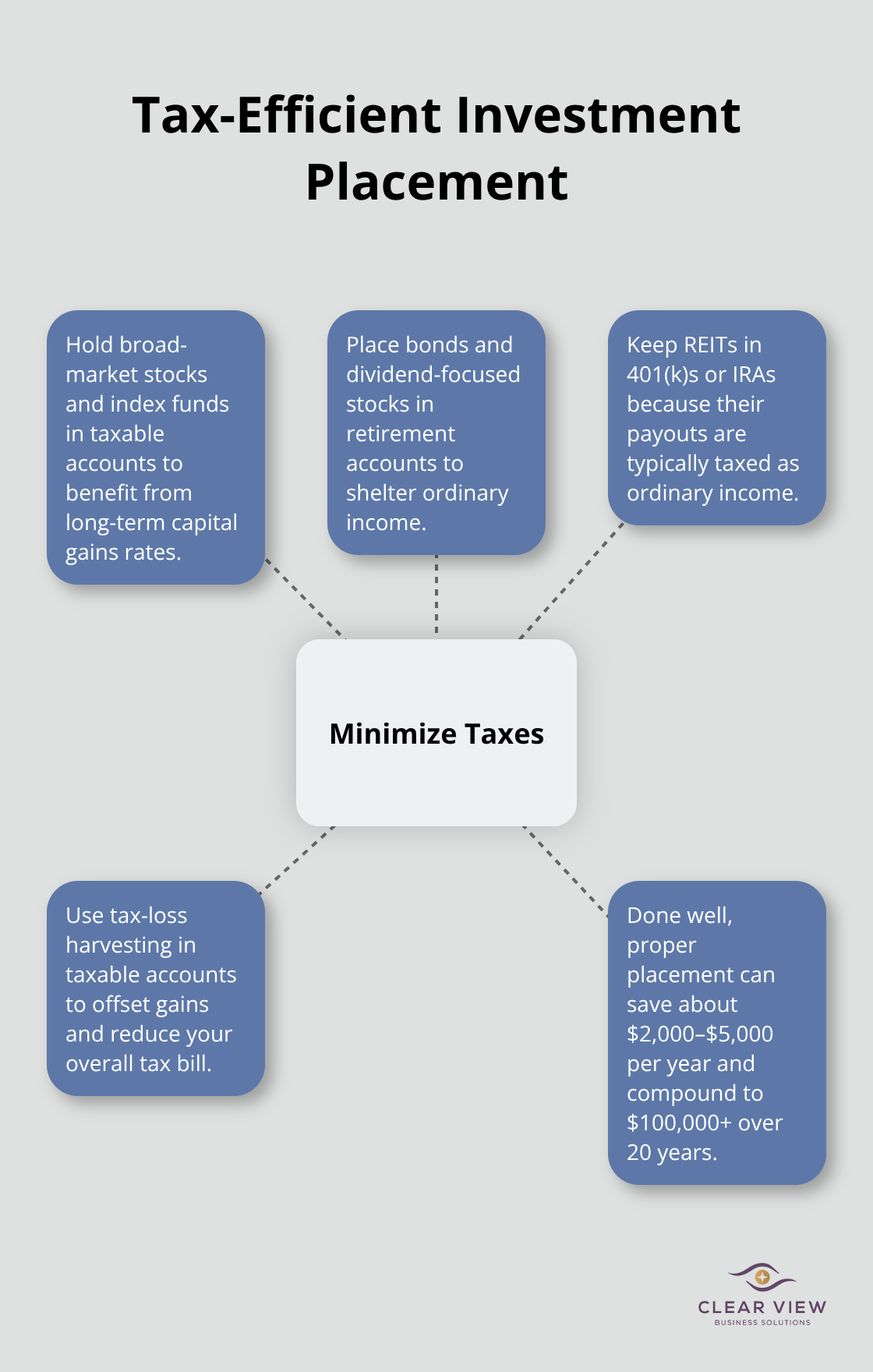

Once you understand which accounts to use, placement matters enormously. Tax-efficient investments belong in taxable accounts while tax-inefficient investments belong in retirement accounts. Stocks and index funds that you hold long-term generate capital gains taxed at favorable rates, so they’re fine in regular brokerage accounts.

Bonds and dividend-paying stocks generate ordinary income taxed at your regular rate, so they belong in 401ks or IRAs where they grow tax-free. Real estate investment trusts throw off taxable income and should sit in retirement accounts. A person with $200,000 in invested assets can save $2,000 to $5,000 annually in taxes simply through proper account placement, and that tax savings compounds into an extra $100,000 or more over 20 years. Consider using tax-loss harvesting in taxable accounts, where you sell losing investments to offset gains elsewhere, reducing your overall tax bill. This requires tracking transactions carefully, but it’s worth the effort. The goal isn’t to avoid taxes illegally; it’s to structure your investments so you pay the minimum amount legally required. That difference adds up to serious wealth over time.

Wealth management and financial planning work best when you review your progress regularly and adjust your strategy as life changes. Set a calendar reminder for the first Sunday of every month to compare your budget against actual spending, and check quarterly whether you’re on track toward your goals. Once yearly, recalculate your net worth and shift your investment allocation if your timeline or risk tolerance has shifted.

The real work happens after you create your plan, because most people drift back to old habits within weeks. Consistency and regular review separate those who build substantial wealth from those who don’t, and your financial plan should adapt to major life shifts-a raise, job loss, new child, or unexpected expense-rather than break under pressure. You now have a roadmap: track your spending, calculate your net worth, define specific goals, build a budget that matches your life, establish an emergency fund, eliminate high-interest debt, and invest strategically in tax-advantaged accounts.

We at Clear View Business Solutions help individuals and small business owners navigate complex finances, optimize tax strategies, and build plans that actually work for your situation. Whether you need help structuring your investments, understanding tax-advantaged accounts, or creating a comprehensive financial strategy, contact Clear View Business Solutions to turn your wealth-building goals into reality.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.