At Clear View Business Solutions, we know that proper financial planning can significantly impact your tax liability. Many people overlook the connection between their financial decisions and their tax obligations.

Understanding what happens to your tax liability with proper financial planning is crucial for optimizing your overall financial health. This blog post will explore key strategies to reduce your tax burden and common mistakes to avoid.

Financial planning and tax liability are inseparable components of your financial health. Financial planning involves strategic decisions about money management to achieve your goals. These choices directly influence your tax situation, creating a dynamic relationship between your financial moves and tax obligations.

Every financial action you take can trigger a tax event. When you earn income, you owe income tax. When you sell an investment for a profit, you face capital gains tax. Even decisions that seem unrelated to taxes, such as purchasing a home, can impact your tax liability (through mortgage interest deductions, for example).

A proactive approach to tax planning can result in substantial savings. This approach includes understanding your tax bracket, reviewing your withholding amounts, reducing your taxable income and liability, and knowing if you need to make estimated tax payments. Instead of merely reacting to tax bills after they arrive, smart financial planning anticipates tax implications. This foresight empowers you to make informed decisions that minimize your tax burden while advancing your financial goals.

Timing plays a critical role in tax-efficient financial planning. These tax strategies could save you thousands this year. Some options include investing in municipal bonds, taking long-term capital gains, and starting a business. You can strategically realize investment losses to offset gains and reduce your tax bill. Additionally, you might bunch deductible expenses into a single tax year to exceed the standard deduction threshold, potentially lowering your taxable income.

Financial planning isn’t just about growing wealth-it’s about retaining more of what you earn. Understanding how your financial decisions impact your taxes allows you to make choices that align with both your financial goals and tax-saving strategies. This approach not only reduces immediate tax liability but also sets the stage for long-term financial growth.

As we move forward, let’s explore specific strategies you can employ to reduce your tax burden through smart financial planning. These tactics will help you navigate the complex intersection of personal finance and tax law, ensuring you’re well-equipped to make decisions that benefit your overall financial picture.

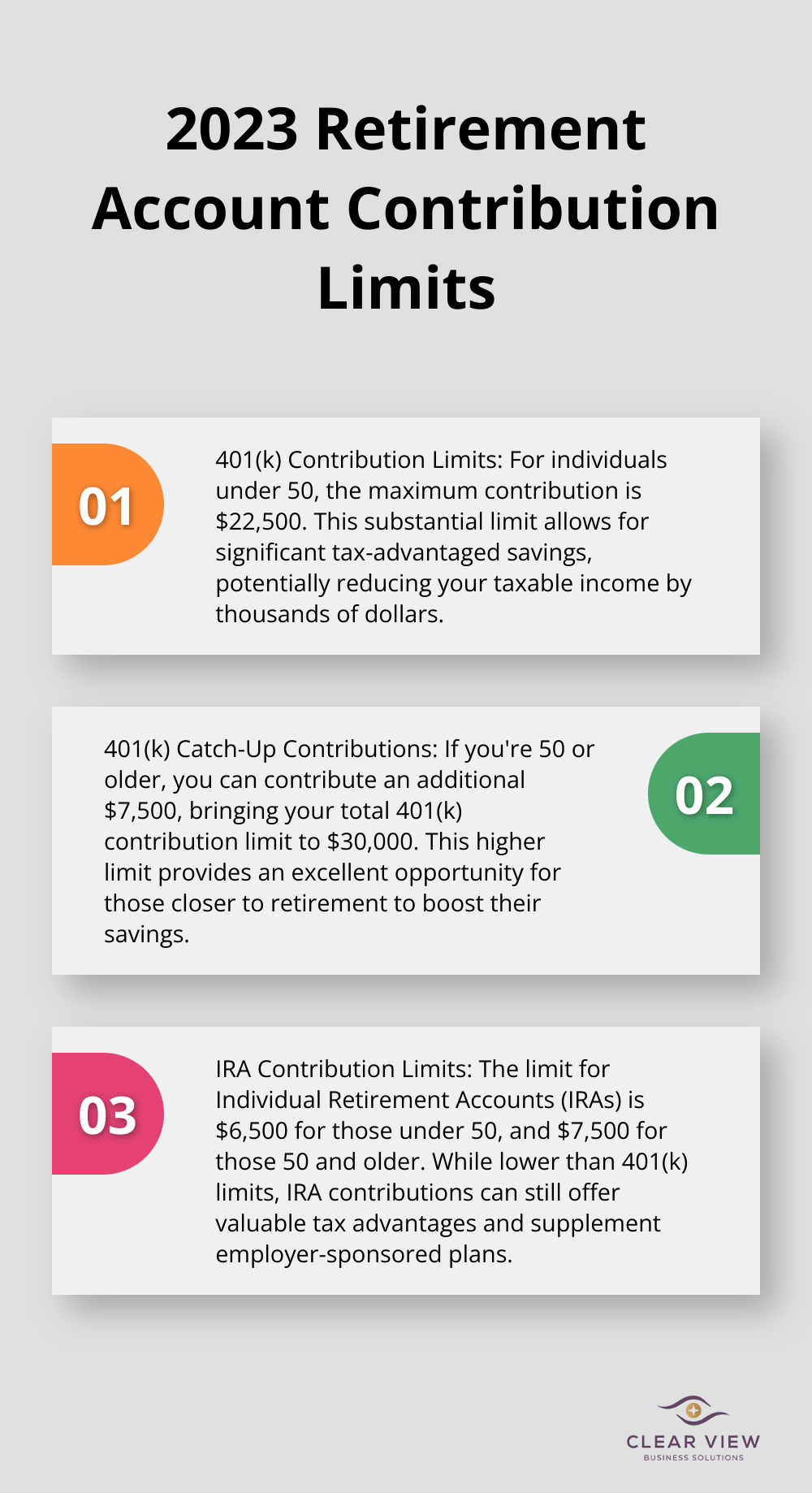

Maximizing contributions to tax-advantaged retirement accounts will lower your taxable income. In 2023, you can contribute up to $22,500 to a 401(k) if you’re under 50, and $30,000 if you’re 50 or older. For IRAs, the limits are $6,500 and $7,500, respectively. Maxing out these accounts could potentially save you thousands in taxes this year alone.

Strategic timing of income and deductions will significantly impact your tax bill. If you’re self-employed or control when you receive income, consider deferring some earnings to the next tax year if you expect to be in a lower tax bracket. Conversely, if you anticipate being in a higher bracket next year, accelerating income into the current year could benefit you.

For deductions, bunching strategies can prove effective. This involves consolidating deductible expenses into a single tax year to exceed the standard deduction threshold. For example, if you’re close to the standard deduction limit, make two years’ worth of charitable donations in one year to itemize and maximize your deductions.

Tax-efficient investing will save you a bundle. Hold investments for over a year to qualify for long-term capital gains rates, which are typically lower than short-term rates. For instance, in 2023, single filers with taxable income under $44,625 pay 0% on long-term capital gains.

Exchange-Traded Funds (ETFs) often have lower turnover and fewer capital gains distributions compared to actively managed mutual funds, making them more tax-efficient. Municipal bonds can also be an excellent choice for high-income earners, as the interest is typically exempt from federal taxes (and sometimes state taxes).

Charitable giving isn’t just good for the soul; it’s good for your tax bill too. Donate appreciated securities held for more than a year to avoid capital gains tax and deduct the full fair market value of the donation. For those over 70½, Qualified Charitable Distributions (QCDs) from IRAs can satisfy Required Minimum Distributions (RMDs) without increasing taxable income.

Set up a Donor-Advised Fund (DAF) if you want to make a large charitable gift but spread out the actual donations over time. This allows you to take the full deduction in the year of the contribution to the DAF, even if you distribute the funds to charities over several years.

Effective tax planning is an ongoing process, not a once-a-year event. Implementing these strategies can significantly reduce your tax liability and keep more of what you earn. However, tax laws are complex and ever-changing. To ensure you’re making the most of these opportunities, it’s wise to consult with a professional. Let’s explore some common financial planning mistakes that could inadvertently increase your tax burden.

Financial planning involves complex decisions that can significantly impact your tax burden. Let’s explore some common pitfalls and how to avoid them.

Many investors miss out on tax-loss harvesting, a strategy that can reduce taxable income. This technique allows you to sell investments that are down, replace them with reasonably similar investments, and then offset realized investment gains. The IRS allows investors to deduct up to $3,000 in net capital losses against ordinary income each year (with any excess carried forward to future years).

The timing of substantial financial moves can dramatically impact your tax bill. Selling a business, exercising stock options, or liquidating large investment positions without considering the tax implications can push you into a higher tax bracket. For instance, if you plan to sell your business, spreading the sale over multiple tax years could keep you in a lower tax bracket each year (potentially saving tens of thousands in taxes).

Many retirees face unexpected tax consequences from Required Minimum Distributions (RMDs) from their retirement accounts. Starting at age 72, you must withdraw a certain amount from most retirement accounts each year. Failure to take RMDs results in a hefty 50% penalty on the amount not withdrawn. Moreover, these distributions are taxed as ordinary income, potentially pushing you into a higher tax bracket. Planning for RMDs well in advance can help manage this tax burden effectively.

The Alternative Minimum Tax (AMT) is a parallel tax system designed to ensure that high-income earners pay a minimum amount of tax. However, it can also affect middle-income taxpayers who exercise incentive stock options or have large deductions. For 2025, the AMT exemption amounts are $137,000 for married filing jointly, $88,100 for unmarried filers, and $68,500 for married filing separately. If you’re close to these thresholds, strategies like timing the exercise of stock options or spreading out large deductions over multiple years can help you avoid triggering the AMT.

Tax laws change frequently, and navigating them without professional help can lead to costly mistakes. While some may attempt to handle their taxes independently, seeking advice from qualified professionals often results in significant tax savings. Clear View Business Solutions offers comprehensive financial advisory and tax services, ensuring that clients make informed decisions and maximize their tax benefits.

Proper financial planning reduces your tax liability significantly. It allows you to keep more of your hard-earned money and accelerates your path to financial freedom. The strategies we discussed, from maximizing retirement contributions to strategic charitable giving, represent only a fraction of available tax-saving opportunities.

Tax laws change constantly, and what works one year might not be the best strategy the next. Professional guidance often proves a wise investment in navigating this complex landscape. Clear View Business Solutions offers comprehensive financial advisory and tax services tailored to your unique situation.

Effective tax planning requires an ongoing, proactive approach. You can transform your tax liability into opportunities for growth and prosperity through informed financial decisions. Our team of experts can help you develop a personalized financial plan that maximizes tax benefits while ensuring compliance with all relevant regulations.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2933 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.