Income tax planning can make a big difference in your financial life. By using smart strategies, you can keep more of your hard-earned money and reduce your tax bill.

At Clear View Business Solutions, we’ve seen firsthand how effective tax planning can lead to significant savings for our clients. This blog post will explore practical ways to minimize your tax burden and maximize your financial well-being.

Maximizing deductions and credits is a powerful way to reduce your tax bill. This strategy can lead to significant savings for taxpayers who understand how to use it effectively.

The choice between itemizing deductions and taking the standard deduction can significantly impact your tax liability. For 2025, the standard deduction is $14,600 for single filers and $29,200 for married couples filing jointly. If your itemized deductions exceed these amounts, itemizing could lead to substantial savings.

Common itemized deductions include mortgage interest, property taxes, and charitable contributions. You should keep detailed records of these expenses throughout the year to make an informed decision when tax time arrives.

Many taxpayers miss out on valuable deductions simply because they don’t know about them. For instance, self-employed individuals can deduct health insurance premiums (including those for long-term care coverage). Educators can deduct up to $300 for out-of-pocket classroom expenses. If you’ve moved for work, certain moving expenses might be deductible.

Don’t overlook state and local sales taxes, which can be especially beneficial if you’ve made large purchases during the year. Medical expenses exceeding 7.5% of your adjusted gross income are also deductible, including costs for prescription medications and medical equipment.

Tax credits are even more valuable than deductions because they directly reduce your tax bill dollar-for-dollar. The Child Tax Credit, for example, can provide up to $2,000 per qualifying child. For those pursuing higher education, the American Opportunity Tax Credit offers up to $2,500 per eligible student for the first four years of post-secondary education.

The Earned Income Tax Credit (EITC) is another powerful tool, especially for low to moderate-income workers. In 2023, the maximum EITC amount is $7,830 for taxpayers with three or more qualifying children.

For energy-conscious homeowners, the Residential Clean Energy Credit allows a credit of 30% of the cost of eligible solar electric property, solar water heating property, and fuel cell property installed anytime from 2022 through 2032.

The world of tax deductions and credits can be challenging to navigate, but the potential savings make it worthwhile. A professional tax advisor can help identify these opportunities, ensuring you don’t leave money on the table. Their personalized approach takes into account your unique financial situation to maximize your tax savings.

As we move forward, it’s important to consider how retirement accounts can further reduce your tax burden. These accounts not only help secure your financial future but also offer significant tax advantages in the present.

Retirement accounts serve as powerful tools to reduce your tax burden while securing your financial future. Let’s explore how you can leverage these accounts to minimize your tax liability.

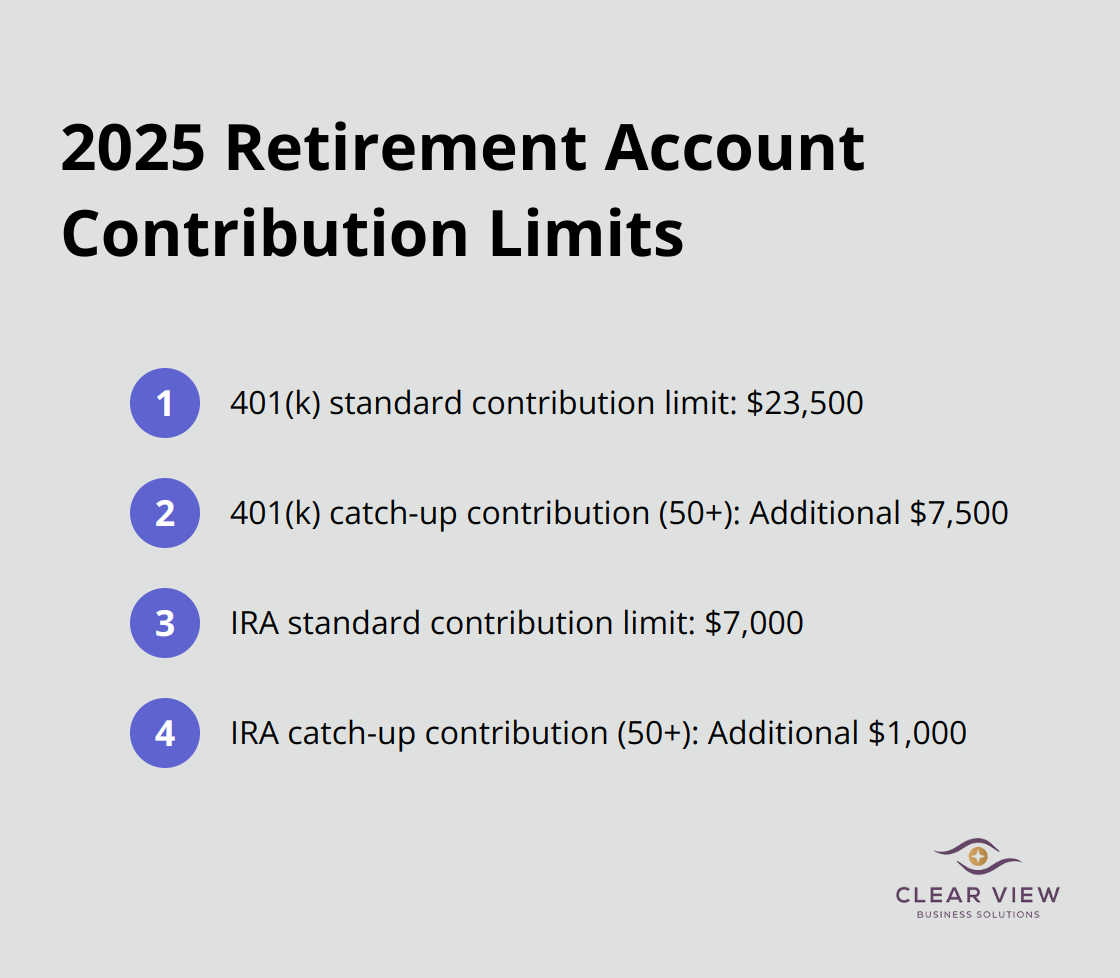

Traditional IRAs and 401(k)s offer immediate tax advantages by allowing pre-tax dollar contributions. For 2025, you can contribute up to $23,500 to a 401(k), or $31,000 if you’re 50 or older. These contributions directly reduce your taxable income for the year. For instance, if you earn $80,000 and contribute $20,000 to your 401(k), you’ll only be taxed on $60,000.

IRA contribution limits, while lower, remain significant. In 2025, you can contribute up to $7,000 to an IRA (or $8,000 if you’re 50 or older). However, deductibility may be limited if you or your spouse participate in an employer-sponsored retirement plan.

Roth IRA conversions can prove a smart move, particularly in lower-income years. While you’ll pay taxes on the converted amount, future withdrawals will be tax-free. This strategy works well if you anticipate a higher tax bracket in retirement.

High-income earners who can’t contribute directly to a Roth IRA due to income limits might consider the backdoor Roth IRA strategy. This involves making a non-deductible contribution to a traditional IRA and then immediately converting it to a Roth IRA.

Health Savings Accounts (HSAs) offer a unique triple tax advantage. Contributions are tax-deductible, the money grows tax-free, and withdrawals for qualified medical expenses are tax-free.

Unlike Flexible Spending Accounts, HSA funds roll over year to year, making them an excellent vehicle for long-term savings. Some investors even use HSAs as additional retirement accounts, paying for current medical expenses out-of-pocket and allowing the HSA funds to grow for future use.

To optimize your tax benefits, try to maximize your contributions to these accounts. Not only will this secure your financial future, but it will also provide significant tax benefits today. However, retirement account strategies can be complex, and it’s important to understand how they fit into your overall financial picture.

As you consider these retirement account strategies, it’s equally important to think about the timing of your income and expenses. This approach can further enhance your tax-saving efforts and complement your retirement account strategy effectively.

You can reduce your tax bill by pushing income to the next tax year. This strategy works well if you expect a lower tax bracket in the following year. Self-employed individuals might delay client billing until late December. Employees can request year-end bonuses in January instead of December.

Consider your overall financial situation before deferring income. This approach might not suit you if you need funds immediately or anticipate a higher tax bracket next year.

You can bring tax relief forward by paying for deductible expenses in the current year. Pay your January mortgage payment in December to claim the interest deduction sooner. Make planned charitable donations before year-end for immediate tax benefits.

Business owners have more flexibility with this strategy. They can purchase necessary equipment or supplies in December rather than January (allowing earlier deduction claims). Ensure these purchases align with your business needs and cash flow situation.

Tax-loss harvesting allows you to sell investments that are down, replace them with reasonably similar investments, and then offset realized investment gains. The IRS allows you to deduct up to $3,000 in net capital losses against your ordinary income each year (with excess carried forward to future years).

For example, if you sold stocks for a $10,000 gain earlier in the year, you could sell underperforming stocks at a $10,000 loss to offset this gain completely. This strategy requires careful planning and consideration of your overall investment strategy.

The Alternative Minimum Tax (AMT) applies to taxpayers with high economic income by setting a limit on those benefits. This parallel tax system aims to ensure that high-income taxpayers pay a minimum amount of tax. If you’re subject to AMT, some deductions and exemptions might not apply, changing the effectiveness of certain timing strategies.

Consult a tax professional to determine if AMT applies to your situation and how it might impact your tax planning efforts.

You can strategically manage your investment portfolio to minimize taxes. Hold investments for more than a year to qualify for long-term capital gains rates (which are typically lower than short-term rates). If you have unrealized losses, consider selling these assets to offset gains and reduce your tax liability.

Income tax planning empowers you to reduce your tax bill and maximize your financial well-being. You can lower your tax burden through strategic use of deductions, credits, retirement accounts, and timing of income and expenses. These approaches help you keep more money and contribute to your long-term financial security.

Tax planning requires a personalized approach tailored to your unique financial situation and goals. What works for one taxpayer may not suit another. Professional guidance becomes invaluable in navigating the complex world of tax regulations and identifying opportunities to reduce your tax liability.

Clear View Business Solutions specializes in tailored tax planning services for individuals and small businesses in Tucson. Our team of experts offers comprehensive financial advisory, tax services, accounting, and bookkeeping. We focus on maximizing tax benefits while maintaining compliance. Partner with Clear View Business Solutions to implement effective income tax planning strategies and optimize your financial future.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2933 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.