Most investors focus on picking winning stocks and funds. They overlook the fact that taxes can eat 20–30% of their returns over time.

Tax-efficient investing isn’t about complex schemes or risky moves. It’s about placing the right investments in the right accounts, harvesting losses strategically, and using tax-free income sources like municipal bonds. We at Clear View Business Solutions help clients implement these straightforward tactics to keep more of what they earn.

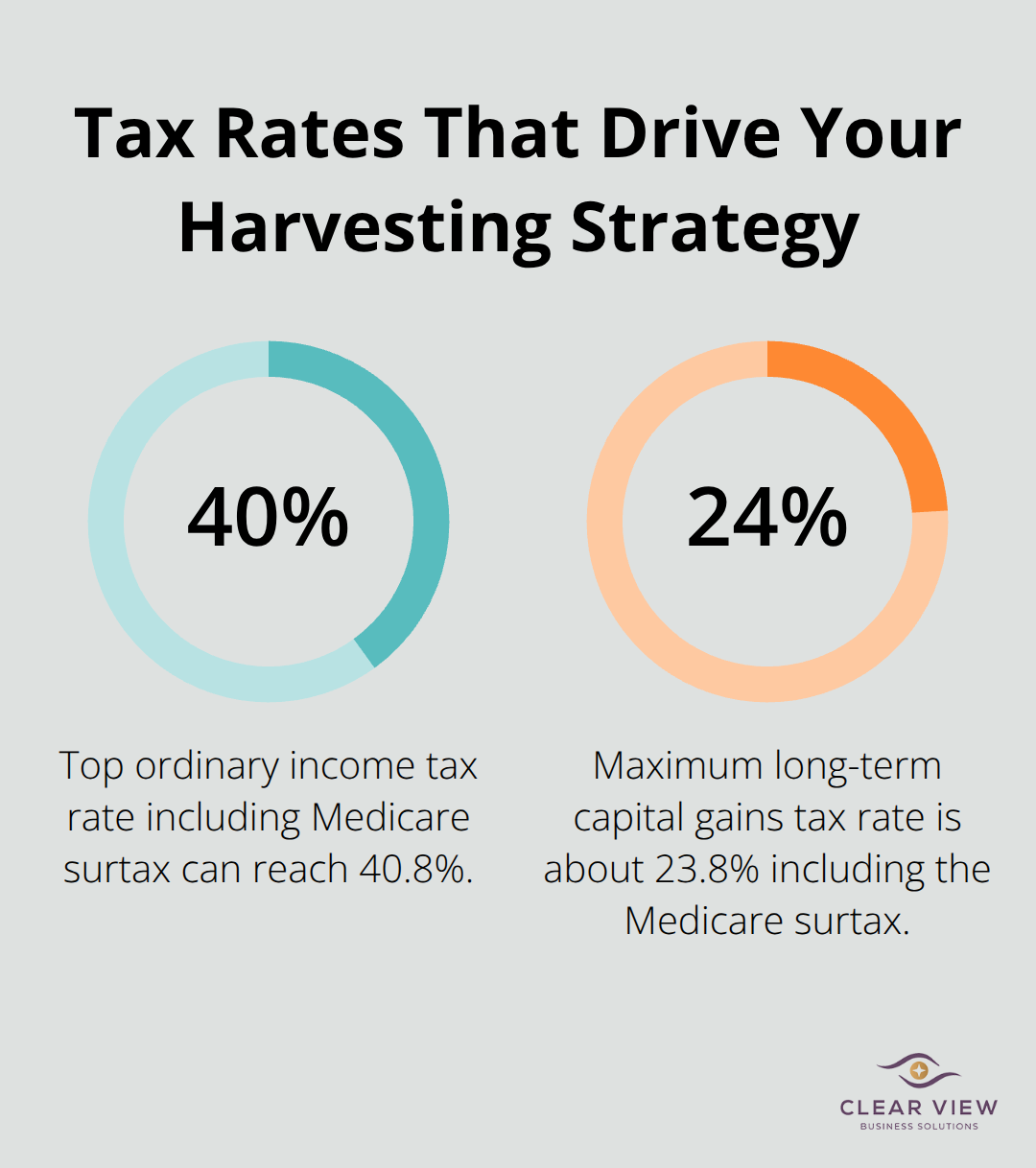

Tax-loss harvesting works by selling investments that have declined in value to offset gains you’ve realized elsewhere in your portfolio. When you sell a stock or fund at a loss, that loss cancels out capital gains dollar-for-dollar. If you sold mutual funds earlier in the year and locked in $25,000 in gains, a $25,000 loss wipes out that entire tax liability. The real power emerges when losses exceed gains. The IRS lets you deduct up to $3,000 of excess losses against ordinary income in the current year, then carry forward any remaining losses indefinitely. This matters because ordinary income gets taxed at rates up to 40.8% when you include the Medicare surtax, while long-term capital gains max out around 23.8%. A $30,000 loss that offsets $25,000 in gains and then reduces ordinary income by $3,000 can save roughly $1,200 in taxes in the current year alone, with another $2,000 carried forward.

The key is timing. You must execute trades before December 31 to capture the loss in the current tax year, and settlement typically occurs two business days later, so don’t wait until mid-December. Waiting until late December forces rushed decisions and increases the risk that your trades won’t settle in time. Plan your harvesting strategy in November so you can execute with confidence and avoid last-minute scrambling.

The IRS wash-sale rule blocks you from claiming a loss if you repurchase the same security or a substantially identical one within 30 days before or after the sale. This rule catches most investors because they immediately rebuy the same fund to stay invested. The 30-day window applies both directions, so selling on December 15 and rebuying on January 10 still triggers the rule. What makes this rule particularly strict is that it applies across all your accounts simultaneously-your taxable brokerage, IRAs, 401(k)s, and spousal accounts all count toward the 30-day period.

The solution is straightforward: sell the losing position and replace it with a similar but not substantially identical investment. If you own a total U.S. stock market index fund that’s down, sell it and immediately buy a different provider’s total market fund or a large-cap value fund. Both track similar markets without triggering wash-sale violations. The replacement should match your original allocation closely enough that you don’t abandon your investment strategy while waiting out the 30 days. After 31 days pass, you can move back to your preferred fund if you wish.

Consider a $500,000 portfolio with $40,000 in unrealized losses spread across various positions. Harvesting these losses in year one offsets $40,000 in gains and reduces ordinary income by $3,000, saving approximately $1,200 in taxes that year. If you reinvest those tax savings, the compounding effect accelerates over time. Over 10 years, consistent tax-loss harvesting could preserve an additional $15,000 to $20,000 in after-tax wealth, depending on your tax bracket and market performance.

The benefit intensifies in volatile years when you hold both significant winners and losers. A 2022-style downturn created massive loss-harvesting opportunities for investors who executed trades strategically. Those who harvested losses in December 2022 used those losses through 2023 and 2024 to offset gains as markets recovered. Automated services scan portfolios continuously for harvesting opportunities, but they require you to understand the wash-sale rule and implement replacements correctly.

Harvesting losses is only half the equation. Where you place your remaining investments matters just as much. Strategic asset location-positioning high-yield investments in tax-advantaged accounts and tax-efficient holdings in taxable accounts-amplifies the benefits you gain from loss harvesting. This coordinated approach transforms tax-loss harvesting from a standalone tactic into part of a comprehensive tax-efficient strategy.

Asset location determines whether you waste thousands in tax savings or capture them. You can harvest losses perfectly, but if you hold bond funds in a taxable account and stock index funds in a 401(k), you forfeit substantial tax advantages. The strategy works by placing investments that generate high taxable income in tax-advantaged accounts like traditional IRAs and 401(k)s, while holding tax-efficient investments in your taxable brokerage account.

Bonds produce ordinary income taxed at rates up to 40.8%, making them ideal candidates for a traditional 401(k) where that income compounds tax-deferred. Stocks held long-term generate capital gains taxed at just 23.8% including the Medicare surtax, positioning them perfectly for taxable accounts where you benefit from lower rates. Vanguard research estimates this simple reallocation boosts after-tax returns by 0.05% to 0.30% annually. On a $1 million portfolio over 30 years, that compounds to roughly $74,000 in additional after-tax wealth.

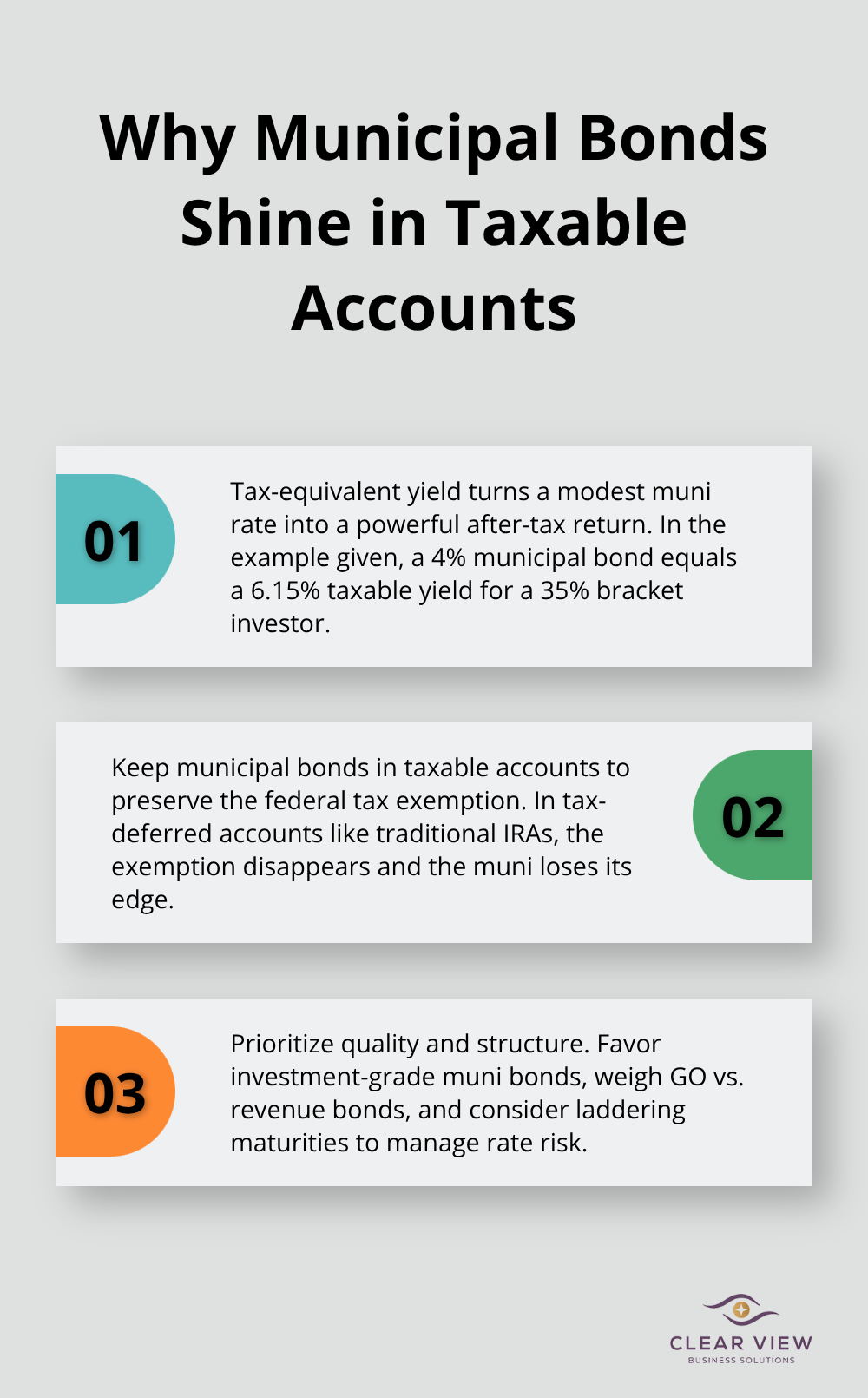

Municipal bonds pay interest free from federal income tax, with some offering state tax exemptions for residents of the issuing state. If you earn $200,000 annually and fall into the 35% federal tax bracket, a municipal bond yielding 4% provides the same after-tax income as a taxable bond yielding 6.15%. The tax-equivalent yield formula reveals this advantage: divide the municipal yield by one minus your marginal tax rate.

A 4% municipal bond for a 35% bracket investor equals 6.15% in taxable income.

This calculation exposes a critical mistake most investors make. Municipal bonds exclusively belong in taxable accounts where high earners capture the full tax exemption. In a tax-deferred account like a traditional IRA, that federal tax exemption vanishes, making the municipal bond pointless compared to a higher-yielding corporate bond. General obligation bonds backed by the issuer’s full faith and credit offer greater safety than revenue bonds dependent on specific project income, though revenue bonds sometimes yield higher returns if credit quality justifies the risk. Most investors should prioritize high-quality municipal bonds rated investment-grade to minimize default risk and consider laddering bonds across different maturities to manage interest-rate risk.

Exchange-traded funds beat traditional mutual funds on taxes because of how they handle inflows and outflows. When investors redeem mutual fund shares, the fund manager must sell securities to pay them, often triggering capital gains that get distributed to remaining shareholders. ETFs use creation units to handle redemptions differently, allowing managers to deliver securities directly instead of selling them. This structural advantage almost never triggers capital gains distributions.

A $100,000 investment in an actively managed mutual fund might generate $2,000 to $4,000 in annual taxable distributions, while the same allocation in an ETF generates minimal distributions. Over 20 years, this difference compounds into tens of thousands in additional after-tax wealth.

Index-based ETFs prove most tax-efficient because their low turnover rarely produces capital gains, while leveraged and inverse ETFs remain relatively tax-inefficient due to heavy derivative use that triggers 60/40 long-term/short-term gain splits regardless of your holding period. The practical recommendation is straightforward: use broad-based index ETFs for equity exposure in taxable accounts and reserve actively managed funds for tax-deferred retirement accounts where distributions don’t matter.

When selecting ETFs, examine expense ratios, average duration, and average maturity to verify you’re not paying excess fees that offset tax benefits. This coordinated approach-combining tax-loss harvesting with strategic asset location and tax-efficient fund selection-transforms individual tactics into a comprehensive strategy that maximizes your after-tax returns. The next step involves implementing these strategies across your actual portfolio by selecting the right mix of investments based on account type and monitoring your positions throughout the tax year.

The real test of tax-efficient investing arrives when you actually construct your portfolio across multiple accounts. Theory collapses without execution. Start with a concrete inventory of what you own and where it lives. List every holding in your taxable brokerage, traditional IRA, Roth IRA, and 401(k) separately. Then categorize each holding by its tax profile: bonds and interest-bearing investments generate ordinary income taxed at your marginal rate, while stocks and equity funds produce long-term capital gains taxed at 23.8% or less. This simple spreadsheet reveals immediately whether your allocation matches your account structure.

Most portfolios fail this test spectacularly. A typical mistake places bond funds in a taxable account while stock index funds sit in a 401(k), reversing the optimal structure entirely. Fix this misalignment first. Strategic asset placement across account types amplifies portfolio efficiency beyond basic diversification. Move your bond holdings into your traditional IRA or 401(k) where ordinary income compounds tax-deferred. Shift equity index ETFs to your taxable account where long-term gains receive favorable treatment. If you hold municipal bonds, they must occupy taxable account space exclusively because their tax exemption evaporates in tax-deferred accounts.

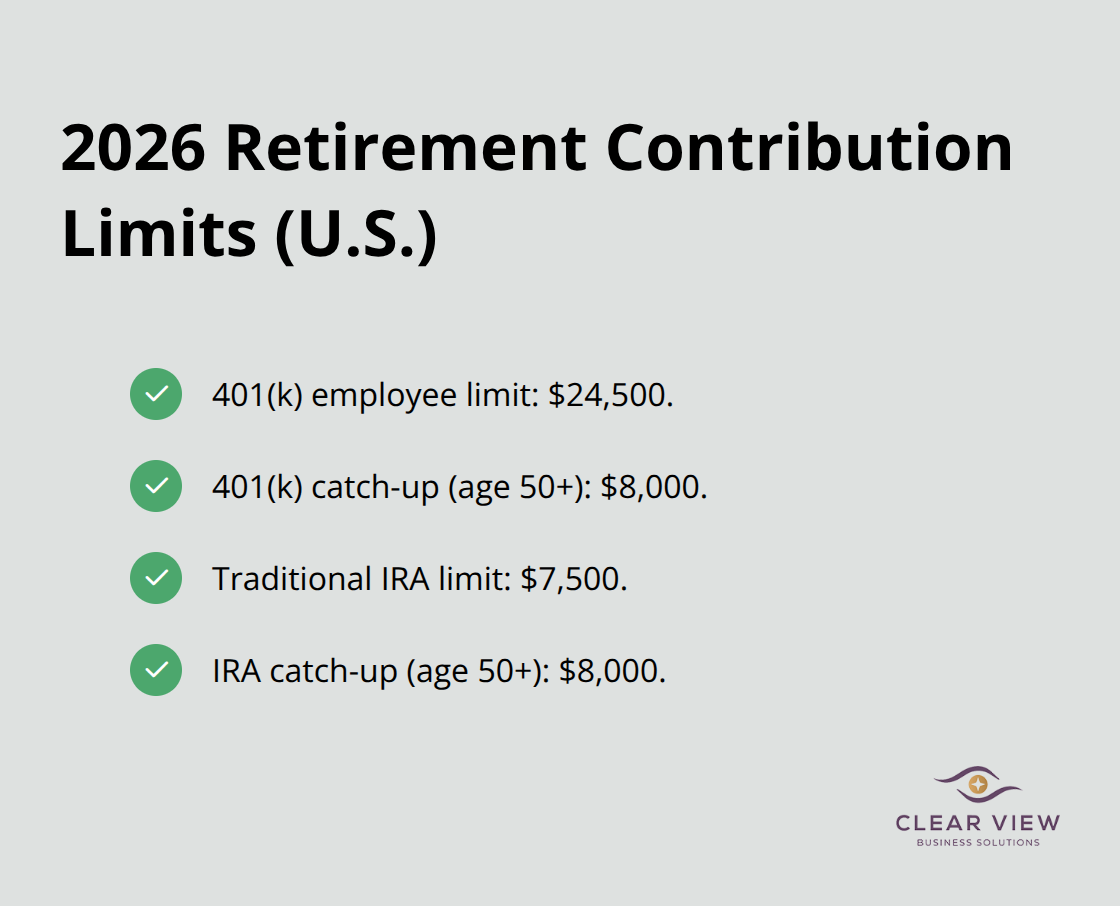

A $500,000 portfolio correctly positioned across three account types generates $1,500 to $3,000 in additional after-tax annual returns compared to haphazard placement. Over a 30-year working life, Vanguard research shows this discipline compounds to roughly $74,000 in extra after-tax wealth. The 2026 contribution limits matter here: you can stash $24,500 in a 401(k) with an $8,000 catch-up if you’re 50 or older, and $7,500 in a traditional IRA with another $8,000 catch-up. These limits define how much high-income-producing debt you can shelter from annual taxation. Max these accounts first before taxable investing, since tax deferral beats paying taxes today on ordinary income.

Quarterly reviews prevent December scrambling and capture opportunities as markets move. Set a review in March, June, September, and December to identify losses worth harvesting and rebalancing needs. During volatile periods, losses accumulate quickly and often go unrecognized until year-end when time pressure forces rushed decisions. A disciplined quarterly check catches losses early when you can thoughtfully select replacement investments that avoid wash-sale violations.

Track your cost basis meticulously because the IRS requires you to identify which specific shares you sold when harvesting losses, not just a round number. Most brokers default to a first-in-first-out method, but specific identification lets you select the highest-cost shares to maximize tax losses. This matters considerably: selling your 100 shares with a $5,000 cost basis generates a larger loss than selling shares with a $3,000 basis, potentially saving hundreds in taxes.

Monitor distribution announcements from mutual funds and ETFs before year-end, since mutual fund distributions can trigger unexpected taxable income in December. Many investors receive unwelcome capital gains distributions just before the new year after the fund already experienced significant losses. ETFs rarely create this problem due to their structural advantages, reinforcing why they belong in taxable portfolios.

A tax professional transforms these mechanics from solo effort into coordinated strategy. A qualified tax advisor reviews your complete financial picture, not just isolated investments, and identifies opportunities you’d miss alone. They understand your state tax situation, which matters enormously because some states don’t permit loss carryforwards while others offer additional deductions. They coordinate tax-loss harvesting timing with your income patterns and charitable giving strategy.

A $200,000-income earner in a high-tax state benefits enormously from professional guidance that might net $3,000 to $8,000 annually in tax savings through coordinated strategies you cannot execute in isolation. This ongoing relationship costs far less than the tax savings it generates, making professional guidance economically rational rather than discretionary.

Tax-efficient investing reduces what you pay in taxes and increases what you keep from your returns. The strategies covered here work together: tax-loss harvesting captures losses to offset gains, strategic asset location places bonds in tax-deferred accounts and stocks in taxable ones, and municipal bonds provide tax-free income for high earners. ETFs deliver these benefits without the capital gains distributions that plague mutual funds, and implementing all three simultaneously compounds their individual advantages into meaningful wealth preservation.

A $500,000 portfolio optimized for tax efficiency generates an extra $1,500 to $3,000 annually in after-tax returns compared to a haphazardly structured one. Over 30 years, this discipline compounds to roughly $74,000 in additional after-tax wealth. Your state tax rules, income level, and account structure all influence which tactics deliver the greatest benefit, making personalized guidance far more valuable than generic advice.

Start by inventorying your current holdings across all accounts and identifying misaligned positions. Move bonds into tax-deferred accounts and equities into taxable ones, harvest losses quarterly rather than waiting until December, and select index-based ETFs for taxable accounts. Contact Clear View Business Solutions to review your portfolio structure and identify specific opportunities within your situation.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.