Managing substantial wealth requires more than just earning money-it demands a strategic approach to taxes, estate planning, and investments. At Clear View Business Solutions, we’ve worked with high-net-worth individuals who discovered that small planning oversights cost them hundreds of thousands in unnecessary taxes and fees.

This guide walks you through the essential strategies for financial planning for high-net-worth individuals, from tax optimization to wealth preservation and diversified investing.

High-net-worth individuals face a hard truth: without deliberate tax planning, you’ll hand over far more to the IRS than necessary. According to RBC Wealth Management data, nearly 72% of UK high-net-worth individuals lack adequate guidance on tax planning, leaving significant money on the table. The difference between reactive and proactive tax strategy isn’t small-it compounds over decades.

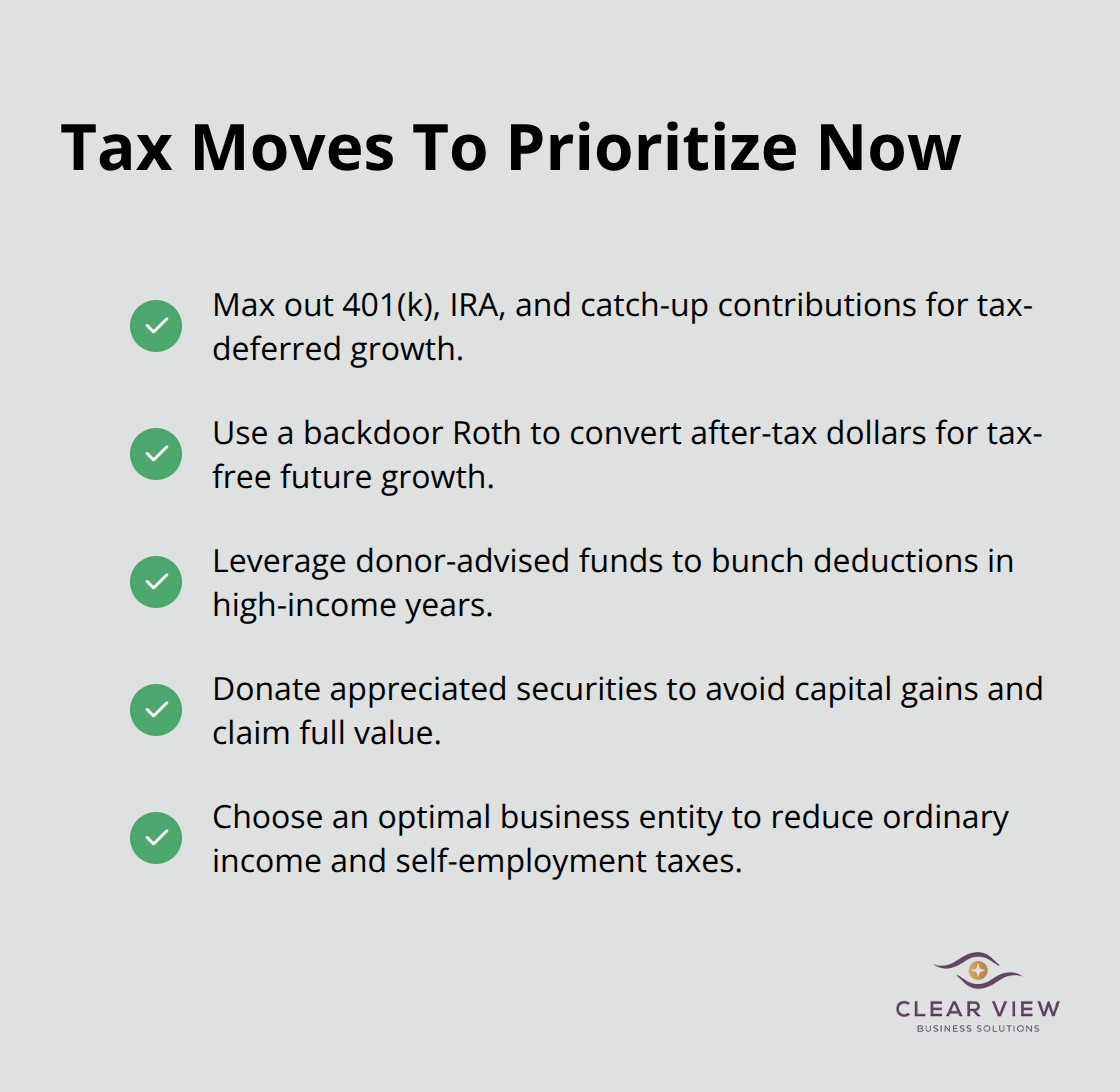

Your first move should be maxing out tax-advantaged accounts before considering anything exotic. In 2026, you can contribute $23,500 to a 401(k) and an additional $7,500 as a catch-up contribution if you’re 50 or older. For IRAs, the limit sits at $7,500 annually, plus $1,000 catch-up. These accounts grow tax-deferred, which means your investments compound without annual tax drag.

High-income earners often skip these because the contribution limits feel small relative to their wealth, but that’s a mistake-the tax deferral effect alone saves thousands per year on investment gains. Beyond basic retirement accounts, consider a backdoor Roth if your income exceeds standard IRA eligibility thresholds. This strategy lets you convert after-tax contributions into Roth accounts where future growth remains tax-free forever. The mechanics require precision, but the long-term benefit justifies the effort.

Charitable giving offers one of the most underutilized tax strategies for affluent individuals. A donor-advised fund (DAF) lets you make a tax-deductible contribution in a high-income year, receive the deduction immediately, then distribute funds to charities over time at your pace. This structure proves particularly powerful if you have volatile income or anticipate a large one-time gain from a business sale or stock concentration.

RBC Wealth Management notes that incorporating gifting and philanthropy into your wealth plan smooths intergenerational transfer while generating immediate tax relief. If you’re charitably inclined but uncertain which organizations to support, a DAF eliminates the pressure to decide immediately. Another approach for business owners involves donating appreciated securities directly to charities rather than selling them. You avoid capital gains tax on the appreciation and receive a charitable deduction for the full fair market value. That’s a dual tax benefit most people overlook.

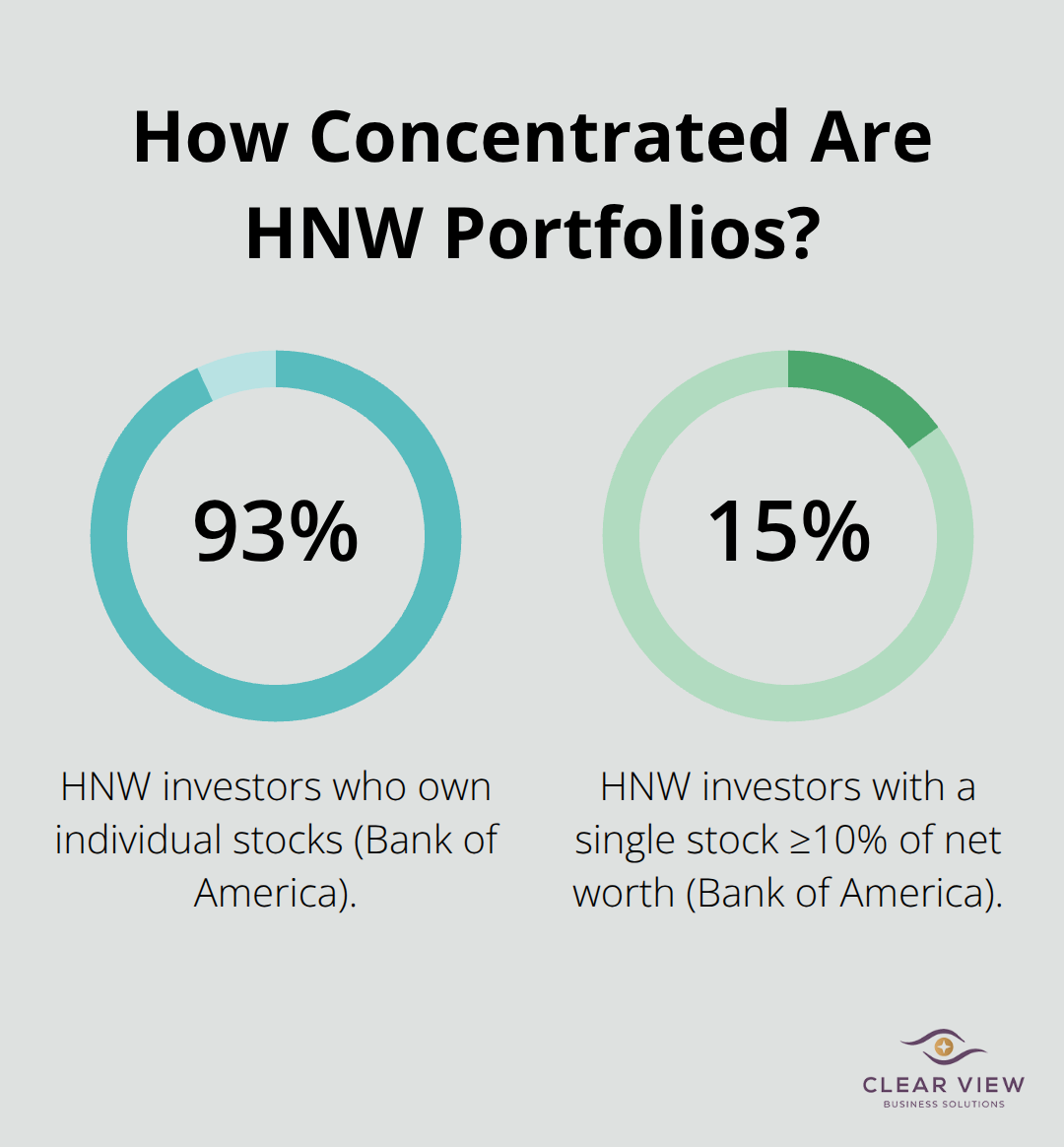

For those with concentrated stock positions-research from Bank of America shows about 15% of high-net-worth investors have a single stock representing at least 10% of their net worth-this strategy helps diversify while managing taxes strategically.

How you structure your business ownership determines whether you pay ordinary income tax or capital gains tax, whether you owe self-employment taxes, and how easily you can transition wealth to the next generation. Sole proprietorships and general partnerships pass all income to your personal return at ordinary rates, which can exceed 37% federally. An LLC or S-corporation can reduce this burden by allowing you to take a reasonable salary and distribute remaining profits as dividends or distributions taxed at lower rates.

The optimal structure depends on your specific income level, state of residence, and whether you plan to reinvest profits or distribute them. This isn’t a set-it-and-forget-it decision-tax law changes regularly, and your circumstances evolve. Working with a tax professional who understands entity structure planning prevents costly mistakes.

For business owners planning an exit, the entity structure you chose years earlier directly impacts how much you keep after sale. An S-corporation with clean books and clear documentation commands higher valuations and smoother transactions than a disorganized sole proprietorship. The tax savings compound when you combine entity structure with strategic charitable giving and maxed retirement contributions, creating a coordinated plan rather than isolated tactics. These foundational strategies set the stage for the next critical piece of your financial plan: protecting what you’ve built through comprehensive estate planning and asset preservation structures.

Your tax strategy means nothing if your assets end up in probate court or your heirs face a crushing tax bill. Estate planning isn’t about being morbid-it’s about controlling what happens to your wealth when you’re gone and minimizing what the government takes along the way. According to a 2023 National Will Register survey, only 44% of UK adults have a will, and just 30% under age 55 have documented their wishes. For high-net-worth individuals with complex assets, this gap is far more costly.

Without a plan, your heirs could lose 40% or more of your estate to taxes and legal fees.

The reality is that high-net-worth estates spanning multiple asset classes, real estate holdings, and potential business interests require structured planning that goes far beyond a basic will. RBC Wealth Management research shows that regularly updating your will to reflect complex, multi-jurisdictional assets and evolving tax rules is essential, yet most affluent individuals treat estate planning as a one-time event rather than an ongoing process. Your plan should be reviewed every three to five years, especially after major life changes like selling a business, inheriting assets, or relocating. The difference between a stale plan and an updated one can mean tens of thousands in unnecessary taxes for your heirs.

Trusts form the backbone of serious estate planning for high-net-worth individuals. A revocable living trust allows you to control your assets during your lifetime while avoiding probate entirely when you pass. Probate is expensive, time-consuming, and public-your entire estate becomes a matter of court record. More importantly, trusts give you control over how and when your heirs receive distributions. Instead of handing a lump sum to a 25-year-old beneficiary, a trust can specify that distributions happen at age 30, 40, and 50, protecting your wealth from poor decisions or creditor claims.

For business owners, a trust structure prevents forced liquidation of your company to pay estate taxes. Strategic tax planning alongside wills and gifting plans optimizes tax implications across jurisdictions. If you own real estate in multiple states or have international assets, the complexity multiplies. Trusts also shield assets from creditors in ways simple ownership cannot. If your profession carries liability risk-you’re a doctor, attorney, or business owner-a properly structured trust protects your wealth from malpractice claims or business disputes that might otherwise reach your personal assets. The cost of setting up a trust now is far cheaper than the cost of litigation later.

Estate taxes represent the single largest threat to intergenerational wealth transfer. The federal estate tax exemption sits at $15,000,000 per person in 2026. State-level estate taxes are even more aggressive-some states tax estates above $1 million. If your net worth exceeds these thresholds, every dollar above the exemption faces a 40% federal tax rate. That’s not a penalty; that’s confiscation.

Minimizing this requires strategic gifting during your lifetime. You can gift $18,000 per person per year tax-free in 2026 without touching your exemption. If you’re married, that’s $36,000 per year to each child or grandchild. Over a decade, a couple can transfer $360,000 per child without triggering any gift tax. More aggressive strategies involve using your lifetime exemption strategically. If your estate will exceed exemption limits, using trusts to hold appreciating assets-like a growing business or real estate-locks in today’s valuation for tax purposes while future appreciation passes to heirs tax-free. This technique, called a grantor retained annuity trust or GRAT, requires precise execution but can save millions.

Charitable remainder trusts serve dual purposes: they generate a current income stream for you while funneling the remainder to charity, creating an immediate tax deduction that reduces your taxable estate. The mechanics are complex, but the results justify working with a specialist.

Your estate plan must coordinate with your tax strategy and investment structure. If you’ve optimized your business entity for income taxes but structured your estate naively, you’ve won a battle and lost the war. These three pieces-tax planning, estate structure, and investment diversification-must work together. A comprehensive plan addresses how your business will transfer, whether your real estate holdings will trigger unnecessary capital gains, and whether your heirs will receive assets efficiently or through a tax-inefficient mess. This coordination is where professional guidance becomes indispensable, not optional. The next critical step involves building an investment portfolio that supports both your current lifestyle and your long-term wealth transfer goals.

Your estate plan and tax strategy create the foundation, but your investment portfolio determines whether your wealth actually grows or stagnates. High-net-worth individuals face a specific challenge: traditional stocks and bonds alone won’t generate the returns needed to fund multi-decade retirements, fund philanthropy, and transfer substantial wealth to heirs. Research from Bank of America shows that roughly 93% of high-net-worth investors own individual stocks, yet about 15% have a single stock representing at least 10% of their net worth. This concentration creates both opportunity and catastrophic risk. A market downturn affecting that one sector or company can devastate your entire portfolio.

The answer isn’t to abandon stocks but to deliberately spread capital across asset classes in ways that reduce volatility while maintaining growth potential. RBC Wealth Management data shows that long-horizon investing improves odds significantly: roughly 75 to 80% chance of positive returns over one year on a diversified portfolio, climbing to 90% over three years and near 100% beyond five years. That’s not luck; that’s mathematical probability working in your favor when you stay invested across multiple asset types.

The traditional 60/40 portfolio of stocks and bonds worked for decades, but it no longer suits high-net-worth investors managing substantial capital. In 2026, affluent investors are increasingly moving into alternatives like private credit, fractional real estate, real-asset funds, and small-business crowdfunding, according to research from FNBO Wealth. These alternatives can improve diversification and income stability, though they typically involve longer lock-up periods and higher fees than public markets. That’s not a reason to avoid them; it’s a reason to evaluate them carefully.

Real estate deserves specific attention because it operates differently than equities. Real estate investments include direct property ownership, real estate investment trusts, private equity real estate funds, and real estate debt instruments. Each has distinct risk and return profiles. A direct commercial property generates steady rental income but requires active management and capital for repairs. A REIT offers liquidity and passive income but moves with stock market sentiment. A private real estate fund provides professional management and diversification but locks up capital for years. The practical question isn’t whether real estate belongs in your portfolio; it’s which real estate vehicle aligns with your liquidity needs and management capacity. For investors with $2 million to $10 million in investable assets, real estate typically represents 10 to 20% of total wealth. Beyond that, the percentage often increases because real estate provides inflation protection that stocks and bonds cannot match.

Sector rotation strategies matter more when you control substantial capital. Rather than holding the same technology, healthcare, energy, and consumer staples allocations year after year, quarterly reviews allow you to shift weights based on economic cycle position. This isn’t market timing; it’s disciplined rebalancing. FNBO Wealth research shows that active rebalancing on a quarterly schedule rather than annually allows faster response to market changes. Proactively rebalancing a 60/40 portfolio may add roughly 14 basis points in annual return-a small change that compounds significantly over decades.

Volatility remains the central fear for high-net-worth investors managing concentrated wealth. Market downturns test your discipline and your actual risk tolerance, which often differs from your stated tolerance. Insurance and hedging strategies exist specifically to limit damage during these periods. Whole-of-life insurance policies offer guaranteed death benefits and potential inheritance tax relief when placed in a suitable trust, particularly valuable in higher-rate environments where insurance pricing becomes more attractive. For business owners, key-person insurance protects the company if you become unable to work, and buy-sell insurance funds the purchase of your business interest by partners or the company if you die. These aren’t optional add-ons; they’re structural protection for your wealth.

Long-term care insurance deserves serious consideration because healthcare costs and long-term care expenses are rising sharply. Portfolio hedging through options, inverse ETFs, or managed futures strategies provides downside protection without selling positions. These tools cost money-they’re insurance premiums-but they prevent panic selling during 30 or 40% market declines. The mistake most investors make is implementing hedging strategies only after volatility arrives, when costs are highest. Building hedging into your portfolio structure during calm markets is far more effective.

For concentrated stock positions, collars allow you to sell upside above a certain price while purchasing downside protection below another price. This structure lets you reduce concentration risk without triggering immediate capital gains tax, a critical advantage for founders or executives holding substantial company stock.

Financial planning for high-net-worth individuals succeeds when tax optimization, estate protection, and disciplined investing work together as one coordinated system. Most high-net-worth individuals treat these areas separately, which costs real money over time. Your tax plan must align with your estate structure, your investment strategy must support your retirement timeline and legacy goals, and your insurance decisions must reflect your actual risk tolerance rather than your aspirational tolerance.

This coordination requires expertise that most individuals lack internally. High-net-worth financial planning demands specialists who understand tax code changes, estate law nuances, and investment mechanics across multiple asset classes. Working with advisors who coordinate across these disciplines prevents costly oversights and captures opportunities that most people miss entirely.

The next step is straightforward: schedule a conversation with a financial advisor who understands high-net-worth complexity and can assess your current situation against your long-term goals. Contact Clear View Business Solutions to start building a strategy tailored to your specific situation and goals.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2025 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.