Most investors focus on picking winning stocks and building their portfolio. But here’s what many miss: investment tax strategies can add thousands to your bottom line every year.

At Clear View Business Solutions, we’ve seen firsthand how the right tax moves transform returns. This guide walks you through four proven strategies to reduce what you owe and keep more of what you earn.

Tax-loss harvesting sounds complex, but it’s straightforward: sell investments that have lost value to offset gains elsewhere in your portfolio. The IRS allows you to deduct up to $3,000 of net losses against ordinary income each year, with unlimited carryforwards for future years. This isn’t theoretical. If you realize $25,000 in gains from one investment and $30,000 in losses from another, you offset the gains completely and use $3,000 against ordinary income in the current year, leaving $2,000 to carry forward. At a 15% long-term capital gains rate and a 35% ordinary income tax rate, that single move could save you roughly $4,800 in taxes. The strategy works best when you have significant realized gains in the same tax year, which makes timing your sales critical. Most investors wait until December to harvest losses, but that creates a bottleneck and limits flexibility.

A better approach spreads loss recognition throughout the year as opportunities emerge, so you avoid rushed decisions when market volatility creates losses late in the year.

The timing question isn’t when the market drops, but when your portfolio has both gains and losses. Many investors sit on losing positions hoping for a rebound, missing the tax benefit entirely. Instead, evaluate your portfolio quarterly to identify positions underwater by 10% or more. If you’ve also realized gains earlier in the year from rebalancing or selling winners, harvest losses immediately to capture the offset. The deadline matters too: trades must settle by December 31st each year, so a sale on December 29th might not settle in time. Coordinate with your brokerage to confirm settlement dates. One practical tip: use specific lot identification when you sell. If you own 200 shares of a stock purchased at different times, you can choose which shares to sell to maximize the loss while keeping your highest-cost shares for future gains. Vanguard’s MinTax method automates this decision across many investments, identifying which lots to sell to minimize tax impact most years.

After you sell at a loss, the wash-sale rule prohibits you from purchasing the same or substantially identical investment within 30 calendar days before or after the sale. Violate this rule and the IRS disallows the loss entirely. Many investors miss this trap because it applies across all your accounts, including IRAs and 401(k)s, and the 30-day window runs 61 days total (30 days before the sale, the sale date itself, and 30 days after). The solution is straightforward: reinvest in a similar but different investment. If you sell a broad US stock index fund at a loss, purchase a different index fund tracking the same market segment, or choose an actively managed fund with similar holdings. The two funds don’t need to be identical, just different enough that the IRS won’t view them as substantially identical. Sector funds, international funds, or different fund families all qualify. This keeps you invested in the market while the 30-day window closes, then you can shift back to your original choice if you prefer. Document your replacement purchases clearly, as the IRS scrutinizes wash-sale claims. The effort pays off: automated tax-loss harvesting across many investments can add meaningful after-tax returns, though benefits shrink if your realized gains are small or you’re in a lower tax bracket.

Tax-loss harvesting works best as part of a larger strategy. Where you hold your investments matters just as much as when you sell them. The next section shows how strategic asset location-placing the right investments in the right accounts-compounds your tax savings year after year.

Tax-loss harvesting reduces what you owe on gains, but strategic asset location accomplishes something more powerful: it prevents unnecessary taxes from occurring in the first place. Where you hold an investment matters as much as what you hold. Bonds, dividend-paying stocks, and actively managed funds generate taxable events every year through interest payments, dividend distributions, and frequent trading. These assets belong in tax-deferred accounts like traditional IRAs and 401(k)s, where growth compounds without annual tax bills.

The IRS allows 401(k) contributions up to $23,500 for 2025, plus catch-up contributions of $7,500 for those age 50 and older. A 2025 contribution deadline of April 15, 2026 means maximizing these accounts should happen before year-end. Meanwhile, tax-efficient investments like municipal bonds and index funds thrive in taxable accounts. Municipal bonds generate interest exempt from federal income tax, making them wasteful inside a retirement account where the tax exemption provides no benefit. Index funds and ETFs trade infrequently, distribute minimal capital gains, and let you control when you sell to harvest losses.

This simple repositioning boosts after-tax returns significantly. Research from Vanguard shows that strategic asset location improves after-tax returns by placing income-generating taxable assets in tax-deferred accounts and holding municipal bonds in taxable accounts. The math proves straightforward: a $500,000 portfolio earning 4% annually generates $20,000 in returns.

If half sits in bonds paying taxable interest in a regular account at a 35% tax rate, you lose $3,500 yearly. Move those bonds to a 401(k) and that $3,500 stays invested, compounding over decades into tens of thousands in additional wealth.

High-dividend stocks and corporate bonds create annual tax drag in taxable accounts. Corporate bonds pay interest taxed as ordinary income at rates up to 37% federally, while dividend distributions trigger capital gains taxes even if you reinvest them immediately. A bond fund yielding 4% in a taxable account nets only 2.6% after a 35% tax hit. The same fund in a traditional IRA or 401(k) keeps the full 4%, then grows tax-deferred until withdrawal.

Qualified dividends receive preferential long-term capital gains rates around 15%, but tax deferral still wins. The strategy here is clear: maximize retirement account space with your least tax-efficient holdings first. If your 401(k) holds $100,000 and your taxable account holds $300,000, identify which $100,000 generates the most annual taxable events. Corporate bonds, dividend-focused funds, and REITs typically rank highest. Shift these into your 401(k) before adding tax-efficient index funds to taxable space.

Health Savings Accounts offer an additional advantage for those with high-deductible health plans. HSAs provide a triple tax benefit: deductible contributions reduce current taxable income, growth compounds tax-free, and withdrawals for qualified medical expenses avoid taxes entirely. Few investors use HSAs as investment vehicles, but they function as a third retirement account tier, perfect for bonds or dividend stocks if you have space available.

The reverse strategy applies to tax-efficient investments. Municipal bond interest remains exempt from federal income tax under IRS rules, making them valuable in taxable accounts where that exemption saves real money. A muni bond yielding 3.5% in a taxable account beats a 4% corporate bond in a 401(k) after taxes for many investors. Index funds and ETFs generate minimal distributions and let you control taxable events through selective selling.

A total stock market index fund might distribute just 0.15% annually in capital gains, compared to 2% or more from actively managed funds. Over 20 years, that difference compounds dramatically. Try directing new taxable contributions toward low-cost index funds and ETFs first, then add individual stocks or bond allocations only after maximizing retirement accounts. This ensures your tax-deferred space holds the highest-tax-rate investments.

Vanguard’s research on tax-aware asset location shows that ETFs and passively managed index funds outperform actively managed funds on an after-tax basis for most investors, precisely because they generate fewer taxable events. If your broker offers tax-managed fund versions, examine their distribution records before choosing. Some actively managed funds explicitly minimize distributions through careful tax management, though most do not. The cost difference matters too: an actively managed fund charging 0.75% annually already starts behind a 0.04% index fund, and that gap widens when you add taxes on distributions.

This positioning strategy compounds year after year, turning small annual tax savings into substantial wealth differences over decades. The real power emerges when you combine asset location with tax-loss harvesting and long-term holding strategies. Your next move involves understanding how holding periods themselves shape your tax liability, and how to build a comprehensive plan around the timeline you hold each investment.

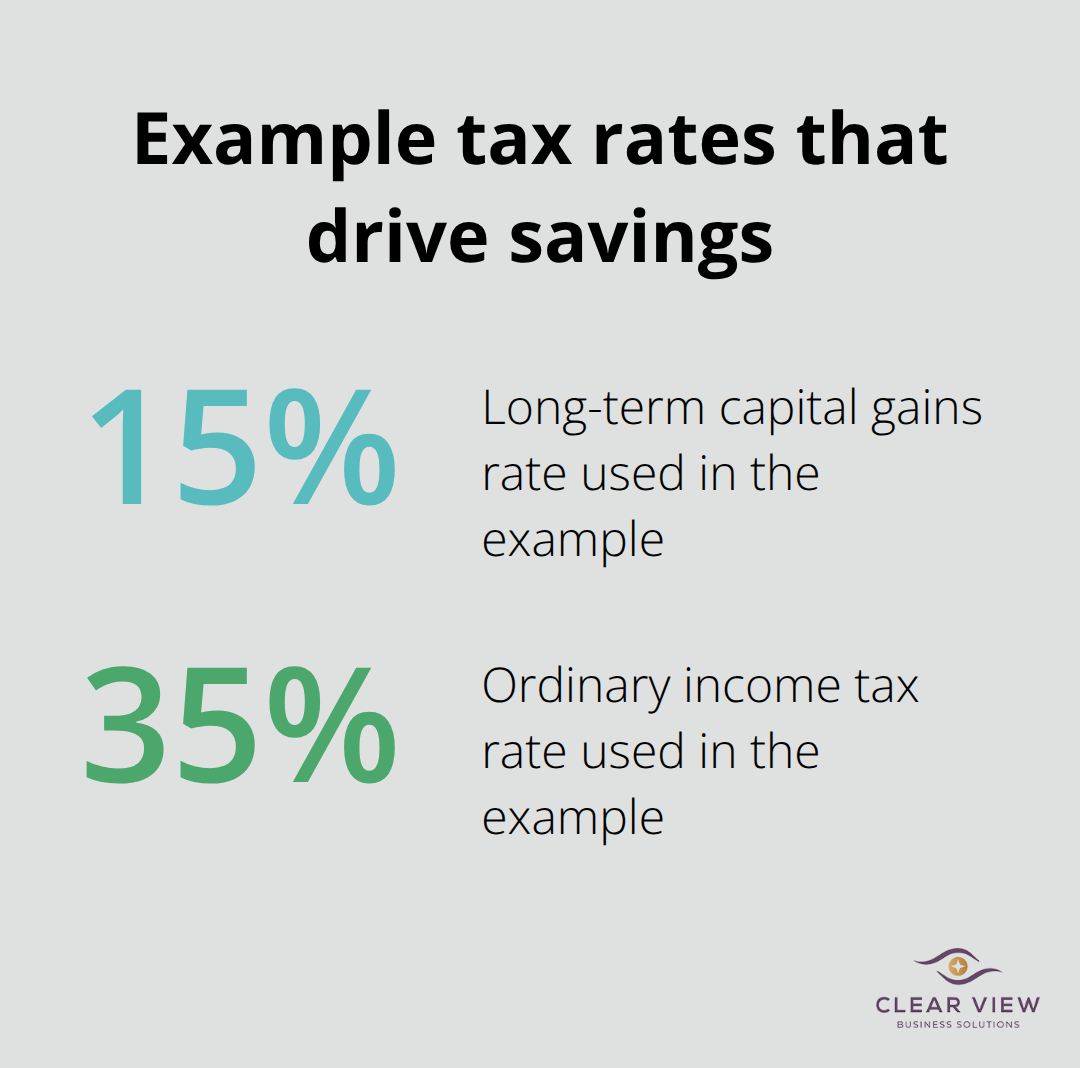

The difference between selling an investment after 11 months versus 12 months can cost you thousands in unnecessary taxes. Short-term capital gains, earned on investments sold within 12 months, face taxation as ordinary income at federal rates ranging from 10% to 37% depending on your bracket. Long-term capital gains preferential tax rates of 0%, 15%, or 20% apply to investments held longer than 12 months. That gap matters enormously. An investor in the 37% tax bracket who realizes a $10,000 gain on a short-term sale pays $3,700 in federal taxes. Hold that same investment for just over one year and the tax drops to $1,500, saving $2,200 on a single transaction.

The math becomes even more compelling across a full portfolio. If you generate $50,000 in annual gains split evenly between short-term and long-term positions, the tax difference between treating all gains as short-term versus all as long-term could exceed $10,000 yearly. State taxes compound this further. Washington State implemented a 7% capital gains tax on gains up to $1 million and 9.9% above that threshold starting in 2025, while nine states including Texas, Florida, and Alaska impose no capital gains tax whatsoever. Your state residency alone can swing your effective tax rate on investment gains by 10 percentage points or more.

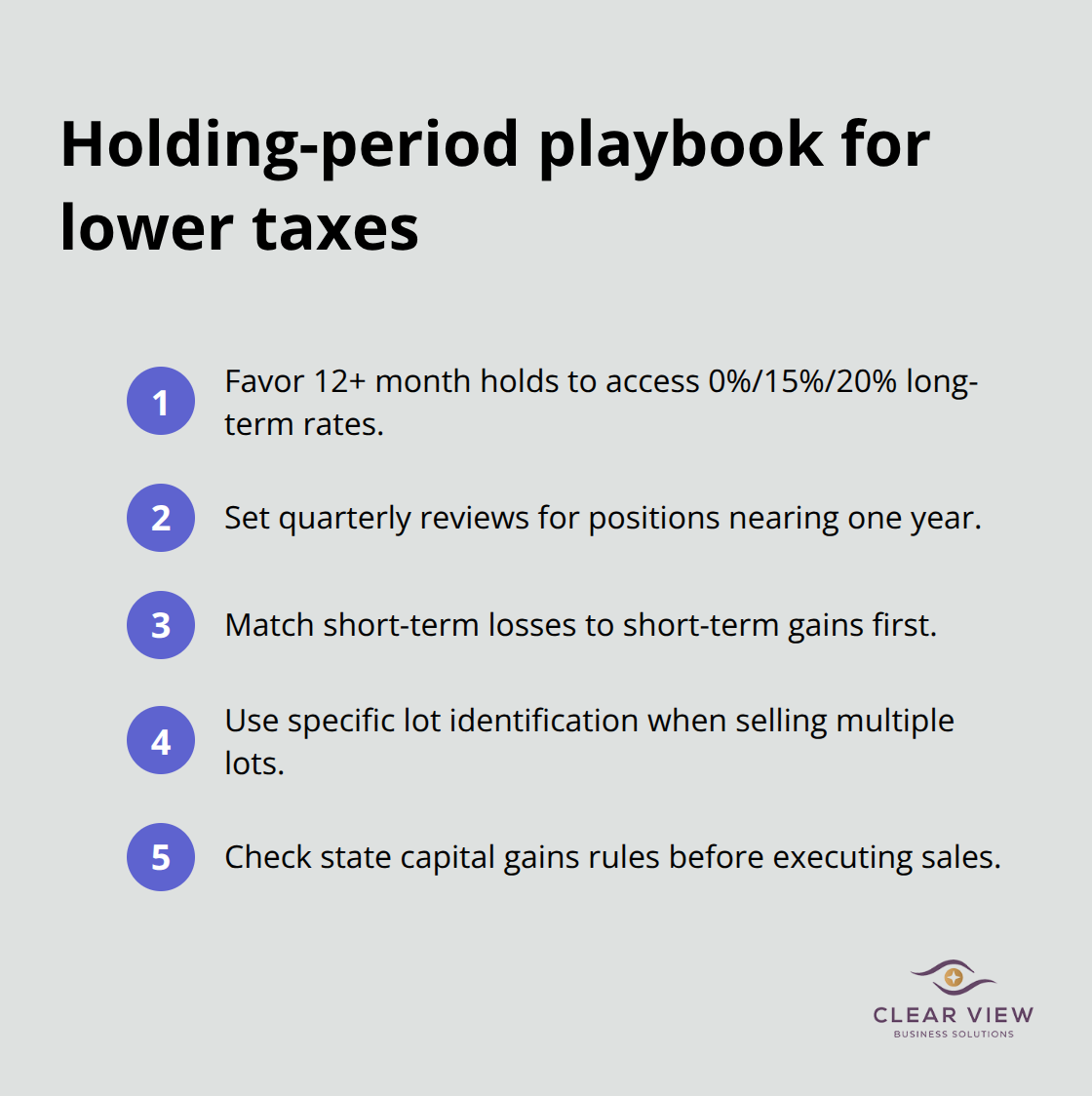

The 12-month holding period creates a natural decision point that should anchor your portfolio management. If you purchased a stock at $50 that now trades at $75, you have an unrealized $25 gain. Selling at month 11 triggers short-term capital gains tax. Waiting until month 13 cuts your federal tax bill by roughly 50% for most investors. This isn’t speculation; it’s mechanical tax math. The challenge emerges when you own dozens or hundreds of positions across multiple accounts. Most investors lack visibility into which holdings crossed the 12-month threshold and which remain underwater. Set quarterly calendar reminders to review positions approaching their one-year anniversary, particularly those with significant gains. Your brokerage platform typically displays the purchase date and holding period for each position. Identify winners that are approaching 12 months and flag them for potential rebalancing after the holding period expires.

Conversely, identify losers still within the 12-month window and evaluate whether you should harvest the loss now, since short-term losses offset short-term gains dollar-for-dollar while long-term losses only offset long-term gains. A position that’s been down 8 months might warrant immediate sale for the tax loss rather than waiting 4 more months hoping for a recovery that may never come. The interaction between holding periods and tax-loss harvesting creates complexity worth managing systematically. If you harvest losses strategically throughout the year, confirm you don’t accidentally create short-term gains elsewhere that those losses could offset more efficiently. A short-term loss offsets short-term gains first, then long-term gains at a less favorable rate. Sequence your sales thoughtfully to match loss types with gain types. When you eventually sell, your brokerage needs to know which shares you’re selling if you own multiple lots purchased at different times. Use specific lot identification to select the shares with the highest cost basis first, minimizing your realized gain. Vanguard’s MinTax method automatically identifies which lots to sell to minimize current-year taxes while preserving flexibility for future planning.

Most investors rebalance their portfolios annually or semi-annually without considering tax consequences. That approach leaves thousands on the table. Instead, build a rebalancing calendar that respects holding periods and tax brackets. Start by listing your largest positions and their purchase dates. Calculate which will cross the 12-month threshold in the coming months. Plan rebalancing moves to harvest losses in positions still under 12 months while allowing winners to mature into long-term status before selling. If you need to trim an overweight position that’s approaching 12 months of holding, wait the extra weeks to secure long-term rates. If you need to trim a losing position, do it immediately to capture the tax loss while it’s still available. This requires discipline because market movements tempt reactive selling, but the tax savings justify the planning effort. A concrete example: suppose you own $30,000 in a technology fund purchased eight months ago that’s now worth $35,000. Your portfolio allocation has drifted and you want to rebalance. Waiting four months to sell captures long-term capital gains treatment on the $5,000 gain, saving roughly $1,250 in federal taxes compared to selling now. If you absolutely must rebalance today, consider selling a different position instead, perhaps one with a loss that can offset other gains. The flexibility of managing multiple positions simultaneously creates opportunities to optimize the timing of taxable events. Document these decisions clearly so you maintain accurate records for tax filing purposes.

The three investment tax strategies covered here work together to transform your after-tax returns. Tax-loss harvesting captures real dollars from portfolio losses, strategic asset location prevents unnecessary taxes from occurring in the first place, and holding periods determine whether you pay ordinary income rates or preferential capital gains rates on your profits. Implementing all three simultaneously compounds the benefit far beyond what any single strategy delivers alone.

Start this year by auditing where your investments sit and moving high-dividend stocks and corporate bonds into retirement accounts while shifting municipal bonds and index funds to taxable accounts. Review your portfolio quarterly for loss-harvesting opportunities, particularly positions underwater by 10% or more, and flag holdings approaching their 12-month anniversary so you can plan sales strategically. These moves require minimal effort but generate measurable tax savings that compound across decades.

The complexity of investment tax strategies increases when you factor in state taxes, multiple account types, wash-sale rules, and the interaction between short-term and long-term gains-this is where professional guidance matters. A tax professional can coordinate your overall financial picture, identify opportunities you’d miss alone, and ensure your implementation avoids costly mistakes. Contact Clear View Business Solutions to discuss how these strategies can strengthen your financial position this year.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2025 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.