Families raising children with special needs face unique financial challenges that most standard planning approaches don’t address. Medical expenses, therapy costs, and long-term care requirements can quickly overwhelm a household budget without proper preparation.

At Clear View Business Solutions, we’ve created this guide to help you build financial planning for special needs families that actually works. We’ll walk you through the specific tools, accounts, and strategies designed to protect your family’s financial future.

Families raising children with special needs face expenses that standard budgeting approaches simply don’t cover. The USDA estimates that raising a typical child from birth to 18 costs about $13,000 per year, but children with special needs can cost up to $30,000 annually or more depending on their specific needs. These numbers represent the baseline, and many families find their actual expenses exceed these figures significantly once they factor in specialized therapies, equipment, medications, and in-home care services.

Start with your actual spending patterns. Pull your bank statements from the last six months and categorize every expense related to your child’s special needs-medical care, therapy sessions, educational support, and daily living expenses. This approach reveals where your money goes and where costs might increase as your child ages. You’ll spot patterns that generic budgets miss entirely.

Many special needs students require higher-cost specialized schooling or intensive therapy programs that standard public school systems cannot provide. Cost of specialized education and therapy services can range significantly based on the type of intervention needed. Document which services your child currently receives and which ones your care team recommends for the future.

Research the actual costs in your area rather than relying on national averages. Contact providers directly, ask about sliding scale fees, and investigate whether your insurance covers portions of these expenses. Some states offer funding assistance for specialized education through vocational rehabilitation programs-identify and apply for these immediately if your child qualifies.

About 90 percent of caregivers for special needs individuals report that retirement planning isn’t their main priority, according to The American College of Financial Services. This mindset creates serious long-term problems because many families overlook government benefits like Medicaid and SSI, which can offset massive expenses if properly structured into your financial plan.

Before age 18, contact your state’s lead agency for adult services and determine what your child qualifies for. Medicaid eligibility, SSI income limits, and other programs have specific rules that directly impact how you should save money. If you save incorrectly (for example, putting assets in your child’s name), you can inadvertently disqualify them from benefits that would cover far more than you could fund yourself.

This is why understanding how government benefits interact with your savings strategy matters so much. The next section covers the specific accounts and tools designed to preserve your child’s benefit eligibility while building the financial security your family needs.

The first step in creating a comprehensive financial plan is establishing an emergency fund that covers three to six months of essential expenses. For special needs families, this safety net prevents you from derailing your long-term strategy when unexpected costs hit. A job loss, medical crisis, or equipment breakdown can destabilize your entire plan if you lack liquid reserves. Calculate your monthly must-have expenses-medications, therapy sessions, housing, utilities-and multiply by four or five months. This becomes your emergency fund target. Many families treat this as optional, but it forms the foundation that protects everything else you’ll build. Once you’ve secured three months of expenses in a high-yield savings account, shift focus to the accounts that will grow your child’s financial security while preserving government benefits.

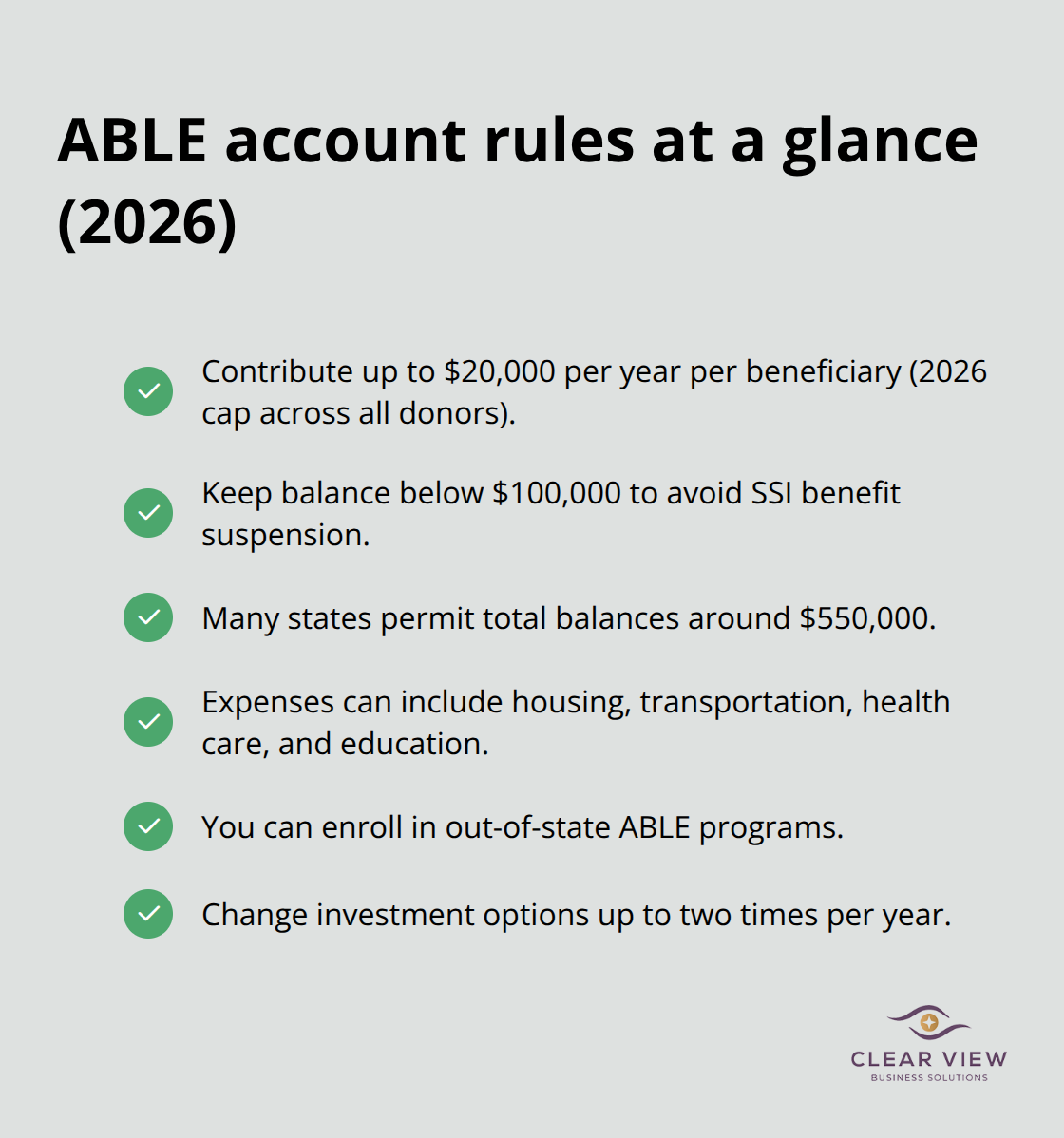

ABLE accounts let you save up to $20,000 annually per beneficiary for disability-related expenses without affecting SSI or Medicaid eligibility, as long as the account balance stays below $100,000. For 2026, this contribution limit applies across all donors combined, so coordinate with grandparents and other family members who want to contribute. Many states allow ABLE account balances up to around $550,000 before triggering restrictions. Qualified disability expenses under ABLE accounts cover housing, transportation, health care, education, employment training, assistive technology, and personal supports.

You can enroll in out-of-state programs even if you live elsewhere, giving you flexibility to find the plan with the lowest fees and best investment options. Within your ABLE account, you can switch investment strategies up to twice annually, so rebalance as your needs change.

A special needs trust is a legal document that lets you leave money to your child without disqualifying them from benefits. The trust holds assets in the trustee’s name, not your child’s name, which preserves eligibility. You’ll need a disability law attorney to set this up properly, and trustee selection matters significantly-choose between an individual family member, a professional trustee, or a corporate trustee based on your family’s complexity and available resources. Unlike ABLE accounts, special needs trusts work best for larger inheritances or assets you want to pass down over time.

Investment strategy for both accounts should match your timeline. If your child is young, you can weather market volatility and pursue growth-focused investments. As your child approaches adulthood, gradually shift toward stability. For retirement accounts outside these special structures, try to save 5 to 10 percent of household income initially and grow toward 10 to 15 percent over time through employer 401(k) plans or traditional and Roth IRAs. Life insurance for primary caregivers acts as a critical backup-name your child’s special needs trust as the beneficiary so funds flow into protected accounts rather than directly to your child.

ABLE accounts and special needs trusts complement each other rather than replace one another. Many families use both to create layered protection for their child’s future. Check beneficiary designations on life insurance, annuities, and retirement plans regularly; these designations override wills and can inadvertently disqualify your child from benefits if structured incorrectly. Coordinate with family members who want to contribute to your child’s financial security-their gifts to ABLE accounts count toward the $20,000 annual limit across all donors. With your emergency fund in place and your benefit-preserving accounts established, you’re ready to explore the specific tools and resources that help you manage these accounts effectively and stay on track with your plan.

Expenses across multiple accounts, professional coordination, and legal document maintenance become overwhelming without proper systems. Dedicated budgeting software outperforms spreadsheets for special needs families because you deal with recurring therapy costs, medical bills, and variable expenses that generic tools miss. QuickBooks or YNAB (You Need A Budget) let you categorize spending by expense type-therapy, medications, equipment, education-and generate reports showing exactly where money flows each month. These platforms sync with your bank accounts automatically, eliminating manual data entry and reducing errors.

Most families discover that expense tracking reveals unexpected patterns: therapy costs spike during school transitions, medical expenses cluster around certain seasons, or equipment replacements happen predictably every few years. Once you see these patterns, you adjust your emergency fund targets and ABLE account contributions accordingly. The ABLE National Resource Center provides worksheets and templates specifically designed for disability-related expenses, helping you document spending in ways that matter for both budgeting and potential tax deductions.

Professional guidance matters more for special needs families than standard financial planning because the intersection of tax rules, government benefits, and trust structures creates real consequences for mistakes. A Certified Financial Planner who holds the ChSNC credential (Chartered Special Needs Consultant) understands how ABLE account contributions affect SSI eligibility, how to structure life insurance beneficiary designations properly, and which investment strategies preserve government benefits while building wealth. Generalist advisors lack this specialized knowledge and often recommend approaches that inadvertently disqualify your child from benefits.

Tax planning specifically for special needs families requires understanding how to claim dependent exemptions, maximize dependent care credits, and document medical expenses for deductions. Your accountant should coordinate with your estate planning attorney to ensure beneficiary designations on retirement accounts and life insurance align with your special needs trust structure. Many families waste thousands annually through misaligned designations that contradict their trust provisions. Clarify fees upfront-whether your advisor charges hourly rates, flat fees, or asset-based percentages-so you understand the actual cost of ongoing guidance. A disability law attorney with experience in special needs trusts charges $2,000 to $5,000 for initial trust drafting, but this investment prevents far costlier mistakes like accidentally disqualifying your child from benefits or creating tax complications that persist for decades.

Your legal documents require specific structures that standard estate plans do not include. Managing government benefits through special needs trust structures allows people with disabilities to receive supplemental financial support while maintaining access to vital public programs. The trust document must explicitly address resource limits for SSI, include language about Medicaid payback rules, and specify which expenses the trustee can fund without jeopardizing benefits. The ABLE National Resource Center and the Academy of Special Needs Planners offer directories of qualified attorneys in your state.

Beyond the trust itself, you need a Letter of Intent that documents your child’s medical history, daily routines, preferences, medication schedules, and emergency contacts-information that no one else in your family may possess. Update this document annually as your child’s needs evolve. Your will should explicitly state that your child receives nothing directly, with all inheritance flowing through the special needs trust instead.

Beneficiary designations on life insurance, retirement accounts, and annuities require annual review, especially after major life events like job changes or account rollovers. Beneficiary designations override wills completely-if you name your child as direct beneficiary on a life insurance policy, that money goes to them regardless of what your will says, potentially disqualifying them from SSI and Medicaid despite your best planning intentions. Coordinate with family members who want to contribute to your child’s financial security, ensuring their gifts to ABLE accounts count toward the $20,000 annual limit across all donors. This coordination prevents accidental over-contributions that trigger tax complications and prevents duplicate ABLE accounts (only one account per eligible individual is permitted).

Your financial planning for special needs families requires ongoing attention and professional coordination that extends far beyond initial setup. Life events trigger immediate plan adjustments-job changes affect your retirement savings capacity and insurance coverage, while shifts in your child’s diagnosis or functional abilities open new government benefit opportunities or change long-term care projections. Family circumstances like inheritances, divorces, or additional children demand coordination with your existing special needs structures to prevent unintended consequences.

We at Clear View Business Solutions understand that managing these interconnected financial elements demands expertise most families lack internally. Our team provides comprehensive financial advisory and tax services specifically designed to help families navigate complex planning situations, coordinating your ABLE accounts, special needs trusts, retirement savings, and tax strategies so everything works together rather than against each other. Whether you need guidance to maximize deductions related to your child’s care or help structuring your accounts to preserve government benefits, professional support prevents costly mistakes that could undermine years of careful planning.

Contact a qualified financial advisor or disability law attorney to start your financial planning for special needs families today. The investment in professional guidance pays dividends through preserved benefits, optimized tax outcomes, and peace of mind knowing your child’s financial future receives proper protection.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2025 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.