Most business owners leave thousands of dollars on the table each year by missing tax deductions and optimization opportunities. The difference between a mediocre tax return and a strategic one often comes down to planning and knowledge.

At Clear View Business Solutions, we’ve seen firsthand how the right business tax strategies can transform your bottom line. This guide walks you through actionable deductions, timing tactics, and entity structures that actually reduce what you owe.

Self-employed professionals routinely overlook deductions that directly reduce taxable income. Office supplies, software subscriptions, professional development courses, and industry publications are all deductible but often go unclaimed because owners don’t track them systematically. The IRS expects you to deduct legitimate business expenses, and failing to claim them means you’re paying taxes on money that shouldn’t be taxed.

If you work from home, the simplified method allows you to deduct $5 per square foot of dedicated workspace, capped at 300 square feet, giving you up to $1,500 annually with minimal documentation. The regular method requires tracking actual expenses like utilities, internet, insurance, and depreciation, which typically yields larger deductions for those with substantial home office space.

Dedicating a specific room or portion of a room exclusively to work is the threshold requirement. The space must be your principal place of business or where you regularly meet clients. If your home office is merely where you answer emails, it likely won’t qualify. Measure the square footage precisely-even rounding up costs you deductions if the IRS questions it.

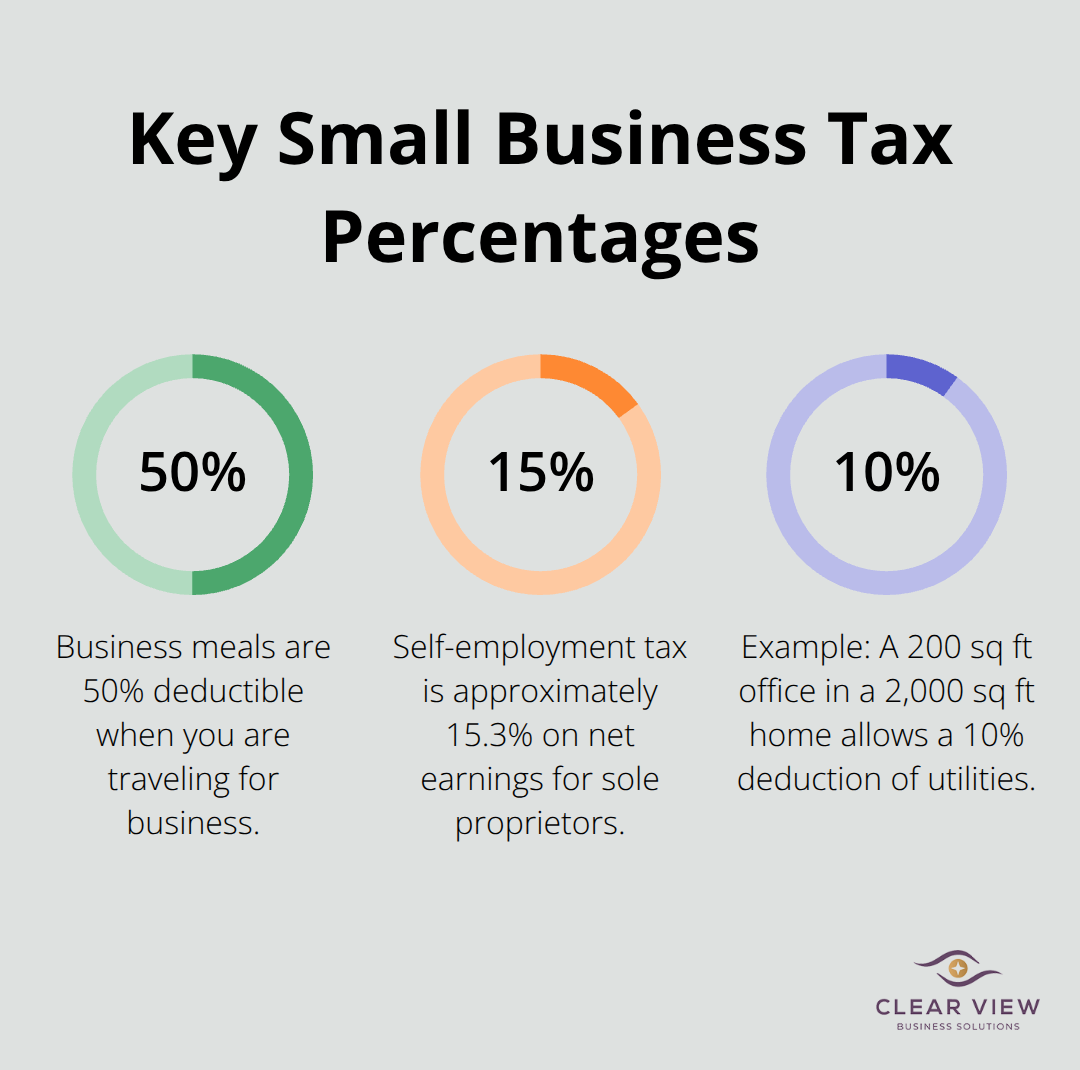

Calculate utilities based on the percentage of your home the office occupies; if your office is 200 square feet and your home is 2,000 square feet, you deduct 10% of electric and heating bills. Internet and phone bills that serve the business are fully deductible if you have a separate business line or can document business use. Home insurance and mortgage interest are trickier; you can only deduct the portion allocable to the office space, and mortgage interest may have limitations depending on your loan structure.

Equipment purchases get special treatment under Section 179, which lets you deduct the full cost of qualifying assets in the year you buy them rather than depreciating them over years. For 2025, bonus depreciation is 100%, meaning if you purchase equipment before year-end, you can claim the entire expense immediately.

Vehicle deductions work two ways: the standard mileage rate, which is 70 cents per mile in 2025, requires minimal record-keeping, or you can track actual expenses like fuel, maintenance, and insurance. Only business-related mileage counts, so commuting from home to your office doesn’t qualify, but client visits, supplier runs, and service calls do.

Maintain a mileage log if you claim the standard rate. The IRS has specific requirements: date, destination, business purpose, and miles driven. Apps like MileIQ or Stride Health automatically log trips using GPS, reducing manual entry errors. If you choose actual expenses instead, track fuel, maintenance, repairs, insurance, and depreciation for the business-use percentage of your vehicle. Heavy vehicles over 6,000 pounds qualify for first-year depreciation deductions up to $20,200 plus bonus depreciation, making trucks and SUVs attractive for business owners who genuinely use them for work.

Travel expenses for business purposes-lodging, meals at 50% of the cost, airfare, and ground transportation-are deductible when you can document the business purpose and dates. Many owners fail to claim meals because they assume the IRS won’t allow them, but the 50% deduction is straightforward if you keep receipts showing the date, amount, location, and attendees. Travel meals are commonly underclaimed because owners don’t realize the 50% deduction applies to meals while traveling for business overnight trips.

Hotel receipts, airfare confirmations, and rental car agreements should all be filed together.

Personal expenses-commuting, vacations, and entertainment unrelated to business-are never deductible, so you must separate business and personal travel. If you take a trip that mixes business and pleasure, only the business portion qualifies, and you must have clear documentation of which days were business-related.

The key to maximizing all these deductions is organization: use accounting software like QuickBooks or Xero to categorize expenses as you incur them, photograph receipts, and maintain a mileage log if you use the standard rate. The IRS expects three years of documentation for substantiation, so digital storage with regular backups protects you in an audit. Too many business owners wait until tax season to gather receipts and guess at deductions, which leaves money on the table and increases audit risk.

With your deductions properly tracked and documented, the next step is to think strategically about when you claim them and how your business structure affects what you owe.

Tax planning that waits until December costs you thousands in missed opportunities. The reality is that timing decisions made throughout the year directly determine your tax liability, and waiting until December 31 to act severely limits your options. Most business owners think tax planning happens in December, but that approach leaves deductions unclaimed simply because they didn’t understand when to take them.

If you expect a strong profit year, defer income to the next calendar year while accelerating deductible expenses into the current year. For cash-basis businesses, this means delaying invoices to clients until January and prepaying expenses like insurance premiums, software subscriptions, and professional services before year-end. Accrual-basis businesses face stricter rules because they recognize income when earned and expenses when incurred, not when cash changes hands, but you still control the timing of certain discretionary expenses. If profits look weak, reverse the strategy: accelerate cash receipts by invoicing early and push expenses into the next year. This flexibility ranks among the most underutilized tax planning tools available.

Make these decisions by mid-November so you have time to execute them. Waiting until December 15 leaves you scrambling and often unable to implement the strategy effectively. Many owners also overlook net operating losses, which allow you to carry forward losses to offset future income. If you have an NOL from a prior year, coordinate with your tax advisor on whether to carry it forward or back to recoup taxes paid in an earlier year.

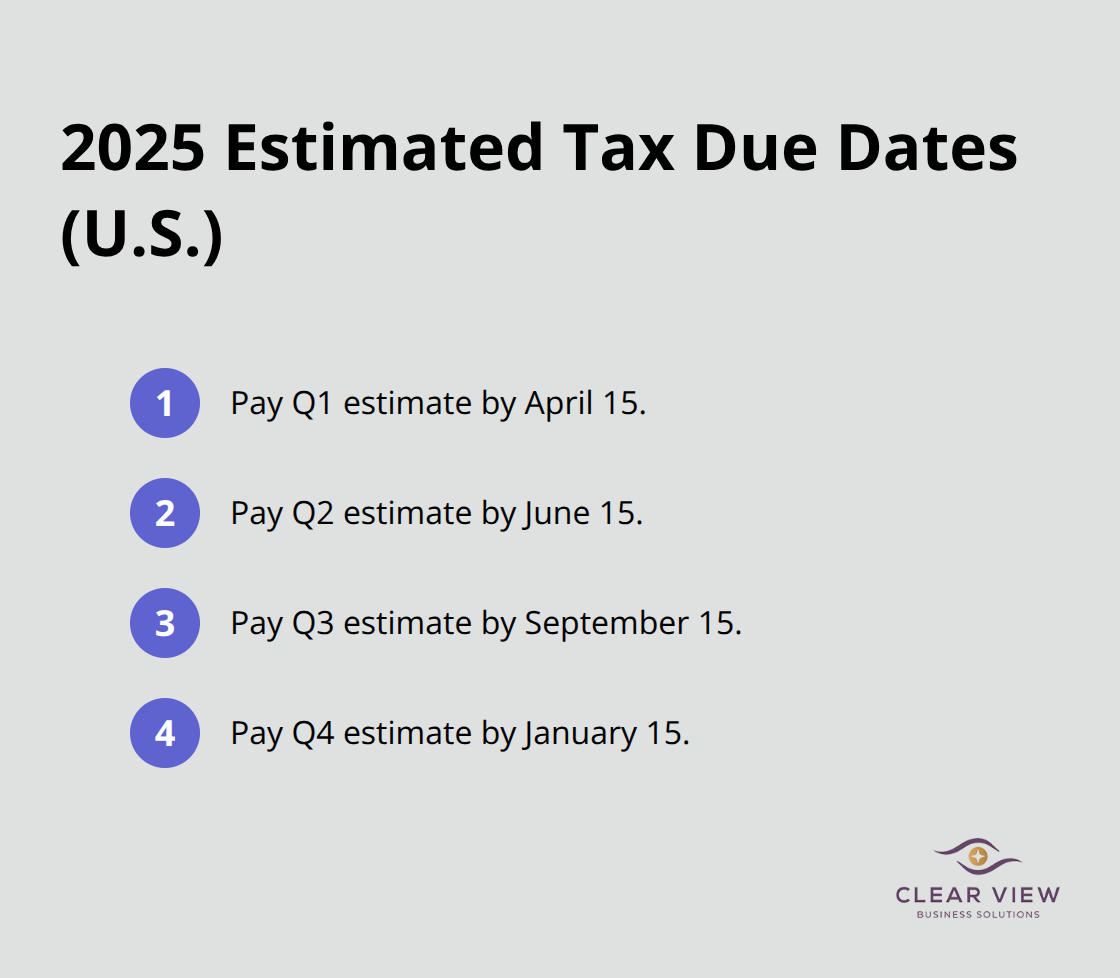

Quarterly estimated tax payments matter far more than most owners realize. The IRS requires you to pay estimated taxes if you expect to owe $1,000 or more in taxes for the year, with four quarterly payments due on April 15, June 15, September 15, and January 15. Missing these payments triggers penalties and interest, even if you ultimately owe nothing. Thomson Reuters Institute research shows that businesses without dedicated tax help are roughly 50% more likely to incur IRS penalties, and many of those penalties stem from missed estimated payments.

Calculate your estimated tax by taking your projected annual income, subtracting deductions and credits, and dividing by four. If your income is uneven, consider paying higher amounts in months when revenue is strong and lower amounts when it’s slow. Use IRS Form 1040-ES to guide your calculations, or work with a tax professional to avoid underpayment penalties.

Retirement account contributions offer one of the most powerful tax deductions available, and the deadlines are non-negotiable. For 2025, you can contribute up to $23,500 to a traditional 401(k) or $7,000 to a traditional IRA if you’re under 50. If you’re self-employed or own a small business, a Solo 401(k) or SEP IRA allows contributions up to roughly 25% of net self-employment income, with a maximum contribution limit of $69,000 for 2025. The critical point is that retirement contributions must be made by the plan’s deadline to claim the deduction in the current tax year. For IRAs, the deadline is typically April 15 of the following year, but for 401(k) plans, contributions must be made by December 31 of the tax year. If you haven’t established a retirement plan by year-end, you forfeit the deduction for that year.

Additionally, small employers can claim a startup tax credit of up to $5,000 per year for the first three years when establishing a SEP IRA, SIMPLE IRA, or 401(k), making the initial setup cost-effective.

Many business owners fail to recognize that health savings accounts pair with high-deductible health plans to deliver substantial tax savings. HSA contributions are tax-deductible, the funds grow tax-free, and withdrawals for qualified medical expenses are tax-free. For 2025, individual coverage limits are $4,400 and family coverage limits are $8,750, and unused balances roll over indefinitely. This makes HSAs superior to health flexible spending accounts, which typically have use-it-or-lose-it rules.

If you employ staff, offering an HSA option alongside a high-deductible health plan is one of the most tax-efficient benefits you can provide, and it’s genuinely valued by employees because it reduces their healthcare costs. The next critical decision involves your business structure itself-whether you operate as a sole proprietorship, LLC, S-Corp, or C-Corp-because that choice fundamentally shapes your tax obligations and available deductions.

Your business structure determines whether you pay self-employment taxes on every dollar of profit or only what you actually take home as salary, and that difference often exceeds $10,000 annually for growing businesses. Most owners operate with whatever structure they started with, unaware that a shift to an S-Corp election or LLC taxed as an S-Corp can dramatically reduce what they owe. The IRS doesn’t care which structure you choose, but your wallet absolutely should.

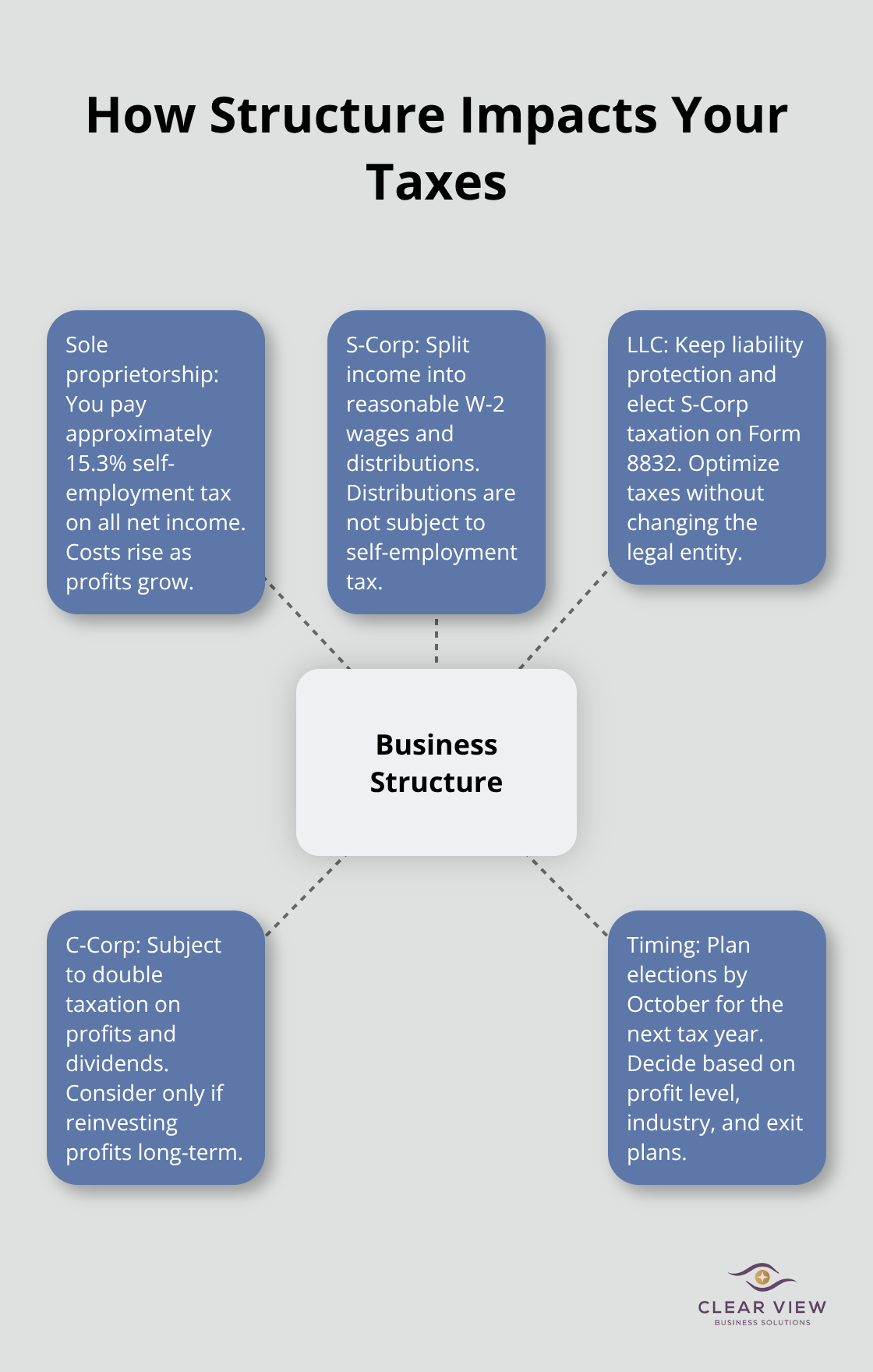

A sole proprietorship is simple to operate but taxes you on all net income at the self-employment rate of approximately 15.3%, meaning a $100,000 profit generates roughly $15,300 in self-employment taxes alone. This flat tax on all profits makes sole proprietorships expensive for owners whose businesses generate substantial income. The burden increases as your business grows, making the structure increasingly inefficient at higher profit levels.

An S-Corp election lets you split income into W-2 wages and distributions, taxing only the W-2 portion at the self-employment rate and allowing distributions to escape that tax entirely. If you operate as an S-Corp and pay yourself a reasonable $50,000 salary on that same $100,000 profit, the remaining $50,000 in distributions avoids self-employment tax, cutting your self-employment tax bill from $15,300 to approximately $7,650. That $7,650 savings justifies the additional accounting and payroll costs, which typically run $1,500 to $3,000 annually, making the net benefit substantial for any business generating $80,000 or more in annual profit.

LLCs offer flexibility because you can elect how they’re taxed without changing your legal structure. A single-member LLC defaults to taxation as a sole proprietorship, but you can elect to be taxed as an S-Corp on Form 8832, gaining the self-employment tax savings without the formality of incorporating. This approach appeals to many owners because you maintain LLC liability protection while optimizing taxes. The election takes effect on the date you specify, typically the first day of the tax year, so plan this decision by October to implement it for the current year.

C-Corporations are rarely optimal for small business owners because they face double taxation: the corporation pays corporate income tax on profits, then you pay personal income tax on dividends, effectively taxing the same money twice. However, if you plan to reinvest all profits into the business and never distribute them, a C-Corp can defer personal taxation, though this strategy works only in specific scenarios and requires careful planning. The qualified business income deduction allows eligible owners to deduct up to 20% of business income. Service businesses like accounting, law, and consulting face income thresholds that may disqualify them from this deduction.

Your choice hinges on profit level, industry, and whether you plan an exit. If you expect to sell within three to four years, the structure matters significantly because it affects your basis and capital gains treatment. Work with a tax professional to model the actual numbers for your situation rather than assuming one structure works universally, because the difference between a mediocre choice and an optimized one often means thousands of dollars in unnecessary taxes.

Knowledge of business tax strategies means nothing without action. Most business owners understand that deductions exist, yet they fail to claim them because tracking expenses feels overwhelming or they’re unsure which costs qualify. The gap between understanding tax strategy and executing it is where thousands of dollars slip away annually. Start by choosing one area to improve immediately: establish a retirement plan before year-end, calculate your home office deduction, or download a mileage app to track business trips. Small actions compound into substantial savings when repeated consistently.

Your business structure deserves attention next if you operate as a sole proprietor and generate $80,000 or more in annual profit. Model the numbers for an S-Corp election with a tax professional, as the self-employment tax savings often exceed the additional accounting costs within a single year. Review your quarterly estimated tax payments to avoid penalties that erode your profits unnecessarily. These decisions shape your tax bill far more than most owners realize.

The real protection comes from working with someone who understands your specific situation. We at Clear View Business Solutions help business owners navigate these decisions with personalized tax planning that aligns with your goals, whether you need help establishing a retirement plan, optimizing your entity structure, or implementing year-round bookkeeping that captures every deduction. Contact Clear View Business Solutions to transform tax planning from a burden into a competitive advantage.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2933 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.