High net-worth individuals face a unique tax landscape that demands more than standard approaches. The difference between a mediocre tax plan and an optimized one can mean hundreds of thousands of dollars over your lifetime.

At Clear View Business Solutions, we’ve worked with successful business owners and investors who discovered that tax strategies for high net-worth individuals require coordination across investments, business structures, and estate planning. This blog post walks through the specific tactics that actually move the needle.

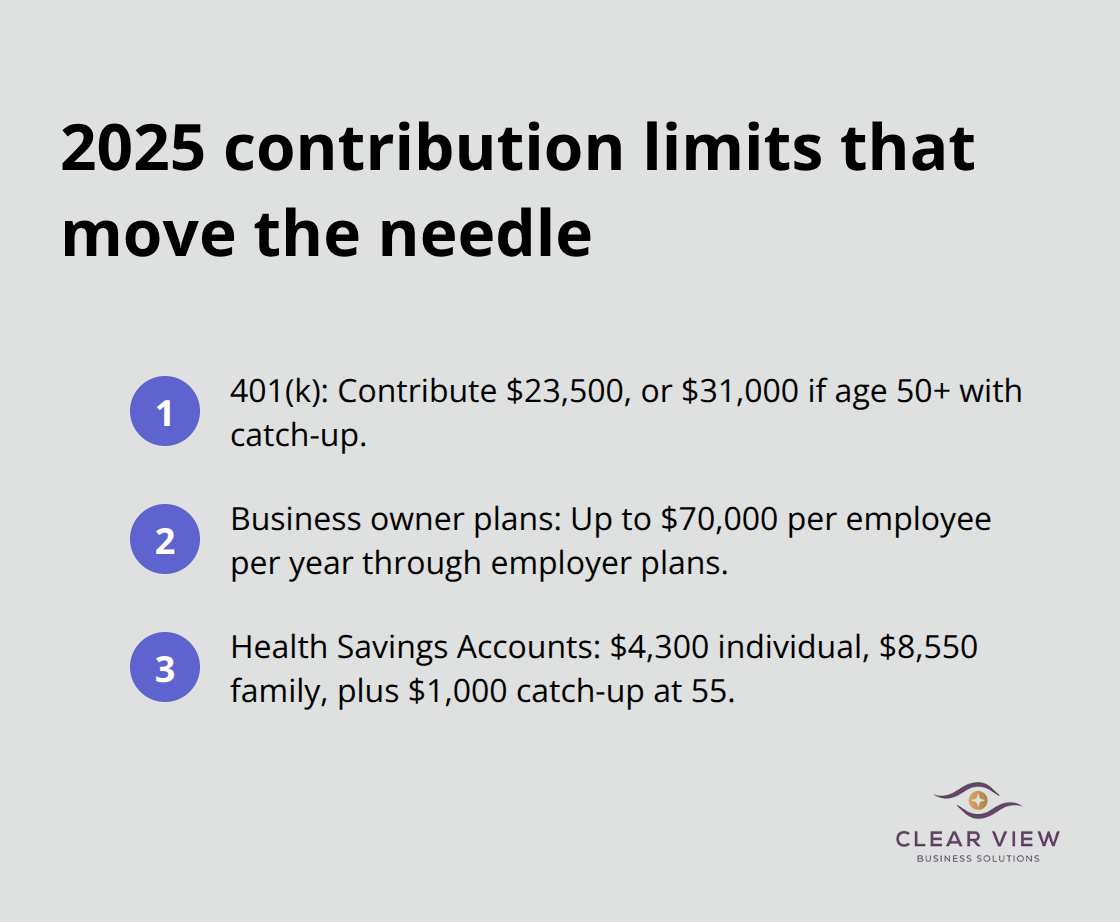

The tax code gives high-net-worth investors multiple levers to reduce what they owe each year. Most successful investors use three specific approaches that compound dramatically over time. The first involves maxing out tax-advantaged retirement accounts. For 2025, you can contribute $23,500 to a 401(k), or $31,000 if you’re 50 or older with catch-up contributions. If you own a business, you can contribute up to $70,000 per employee per year through employer plans-far more than W-2 employees realize. Health Savings Accounts offer another angle: $4,300 for individuals or $8,550 for families in 2025, with an extra $1,000 catch-up at 55.

These accounts grow tax-free and withdrawals for medical expenses never get taxed. Most high-net-worth individuals overlook HSAs because they view them as basic healthcare tools, but they rank among the most powerful tax shelters available.

Tax-loss harvesting generates real after-tax wealth. The strategy works like this: when an investment falls in value, you sell it at a loss, then immediately purchase a similar but not identical security to stay invested. That loss offsets capital gains from winners in your portfolio. If losses exceed gains, you deduct up to $3,000 against ordinary income each year and carry the remainder forward indefinitely. The IRS wash-sale rule requires 30 days before or after the sale to avoid repurchasing the same security, but this is easy to navigate with slightly different funds or securities. The tax savings compound because you reinvest that money instead of sending it to the IRS. Automated tax-loss harvesting continuously scans portfolios for opportunities, which matters because manual harvesting happens once yearly and misses intra-year losses. Long-term capital gains taxed at 15% or 20% can be completely eliminated in years you harvest enough losses, while short-term gains at your ordinary income rate receive the most benefit.

Municipal bonds exempt interest income from federal tax, and sometimes from state and local taxes depending on where you live. For investors in the top tax brackets, the after-tax yield on a 5% municipal bond often surpasses a 7% taxable bond. The strategy extends further: coordinate which assets sit in taxable accounts versus tax-deferred accounts. High-dividend stocks and REITs belong in retirement accounts where dividends compound tax-free. Growth stocks with minimal dividends belong in taxable accounts where you harvest losses and defer gains. Bonds and fixed income should fill retirement accounts first because their interest gets taxed as ordinary income. This asset-location strategy alone improves after-tax returns by 0.5% to 1% annually depending on your allocation and tax bracket.

Tax-efficient investing requires more than isolated decisions about individual accounts or securities. Your business structure, charitable giving, and estate plans all interact with your investment strategy. A concentrated stock position from a business sale, for example, demands different treatment than diversified portfolio holdings. Appreciated real estate, private business interests, and retirement accounts each have distinct tax implications that affect how you should structure your overall wealth. The most successful high-net-worth individuals treat tax planning as a coordinated system rather than separate silos, which is why the next sections address how business structure and estate planning amplify the investment strategies covered here.

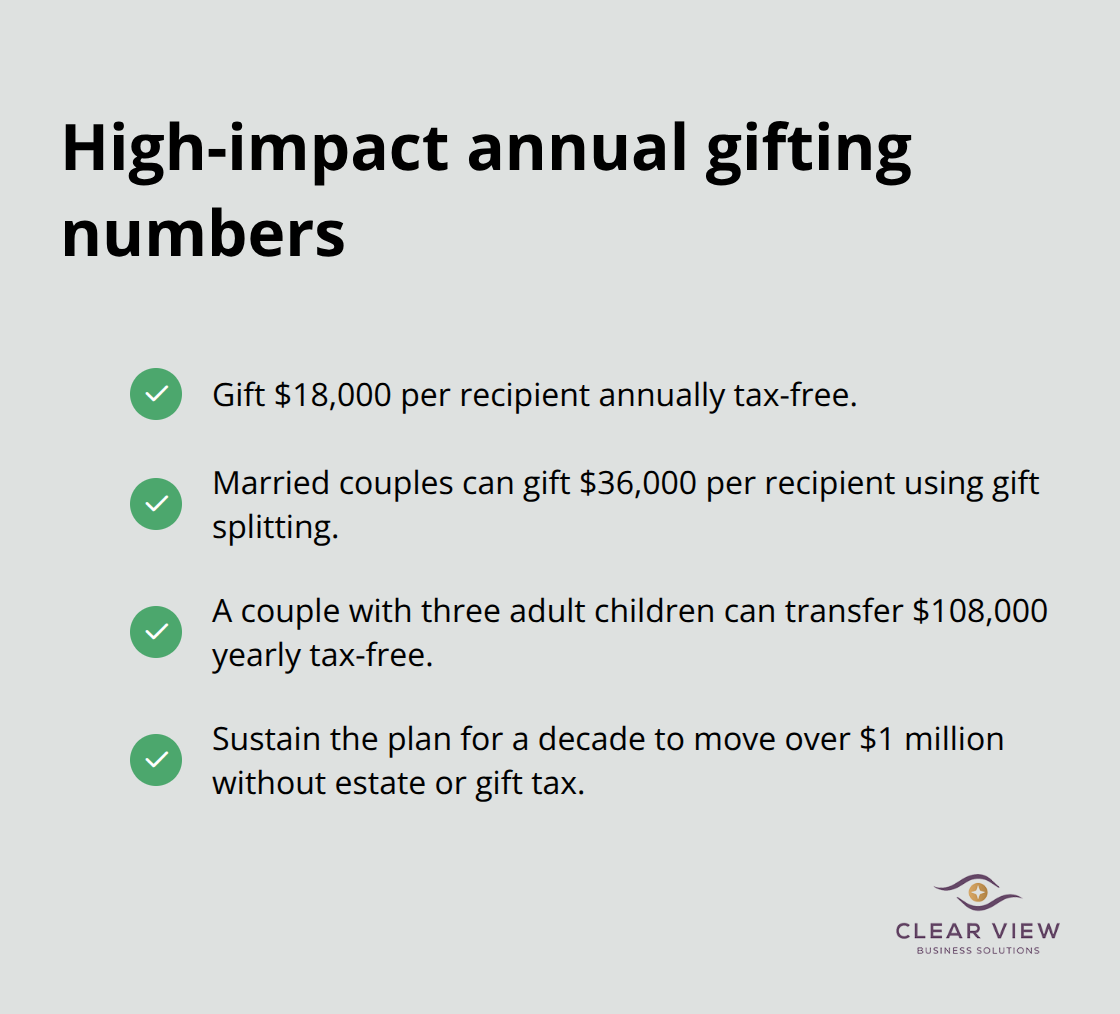

Estate taxes and transfer taxes consume 40% or more of your wealth if you fail to plan strategically. The federal estate tax exemption sits at $13.99 million per individual for 2025, but this drops significantly after 2025 unless Congress acts. High-net-worth individuals who wait until death to address this face a catastrophic tax bill. The solution involves moving assets out of your taxable estate during your lifetime through deliberate gifting and trust structures.

Annual gifts of $18,000 per recipient remain tax-free, and married couples can double this to $36,000 through gift splitting without touching your lifetime exemption. This means a couple with three adult children can transfer $108,000 yearly tax-free. Over ten years, that strategy moves over $1 million to the next generation without any estate or gift tax consequence.

Family Limited Partnerships and family LLCs hold appreciating assets and allow you to gift minority interests at discounted values over time, compressing what the IRS values for transfer tax purposes. Grantor Retained Annuity Trusts freeze current asset value and pass all future appreciation to heirs with minimal gift tax cost, making them especially powerful for businesses or real estate expected to grow.

Irrevocable Life Insurance Trusts remove life insurance proceeds from your taxable estate entirely, which matters because a $5 million policy on a high-net-worth individual can otherwise inflate your estate by $5 million and trigger substantial taxes. Revocable Living Trusts avoid probate and simplify multi-state asset management, though they don’t reduce estate taxes since you retain control. These structures require proper setup and funding to prevent costly mistakes that can render protections ineffective.

Charitable giving accomplishes dual goals: it reduces your taxable estate while supporting causes you care about. Donor-Advised Funds let you take an immediate income tax deduction when you contribute appreciated assets, then grant to charities over decades at your pace. This bunching strategy lets you surpass the itemization threshold in high-giving years, then take the standard deduction in other years and still support charities annually. Charitable Remainder Trusts provide you an income stream for life or a set term, offer an upfront charitable deduction, and remove the remaining assets from your estate entirely. Donating appreciated securities avoids capital gains tax on the appreciation while generating a charitable deduction equal to the full market value, effectively giving you two tax benefits simultaneously. According to Giving USA, U.S. families and individuals donate over $1 billion to charity every day, and strategic donors structure these gifts to minimize taxes while maximizing impact.

Business succession planning demands explicit attention because a business without a formal transition plan often loses value or forces a fire-sale to cover estate taxes. Buy-Sell Agreements predefine how ownership transfers during death or disability and are typically funded with life insurance to provide immediate liquidity. Without this, your heirs face the choice of selling the business quickly at a discount or struggling to pay estate taxes while operating it. Update your estate plan every two to three years or after major life changes like a business sale, significant inheritance, or major asset acquisition, since tax law changes and personal circumstances shift strategy constantly. These estate structures interact directly with your business entity choice and tax classification, which is why tax planning amplifies your overall tax efficiency.

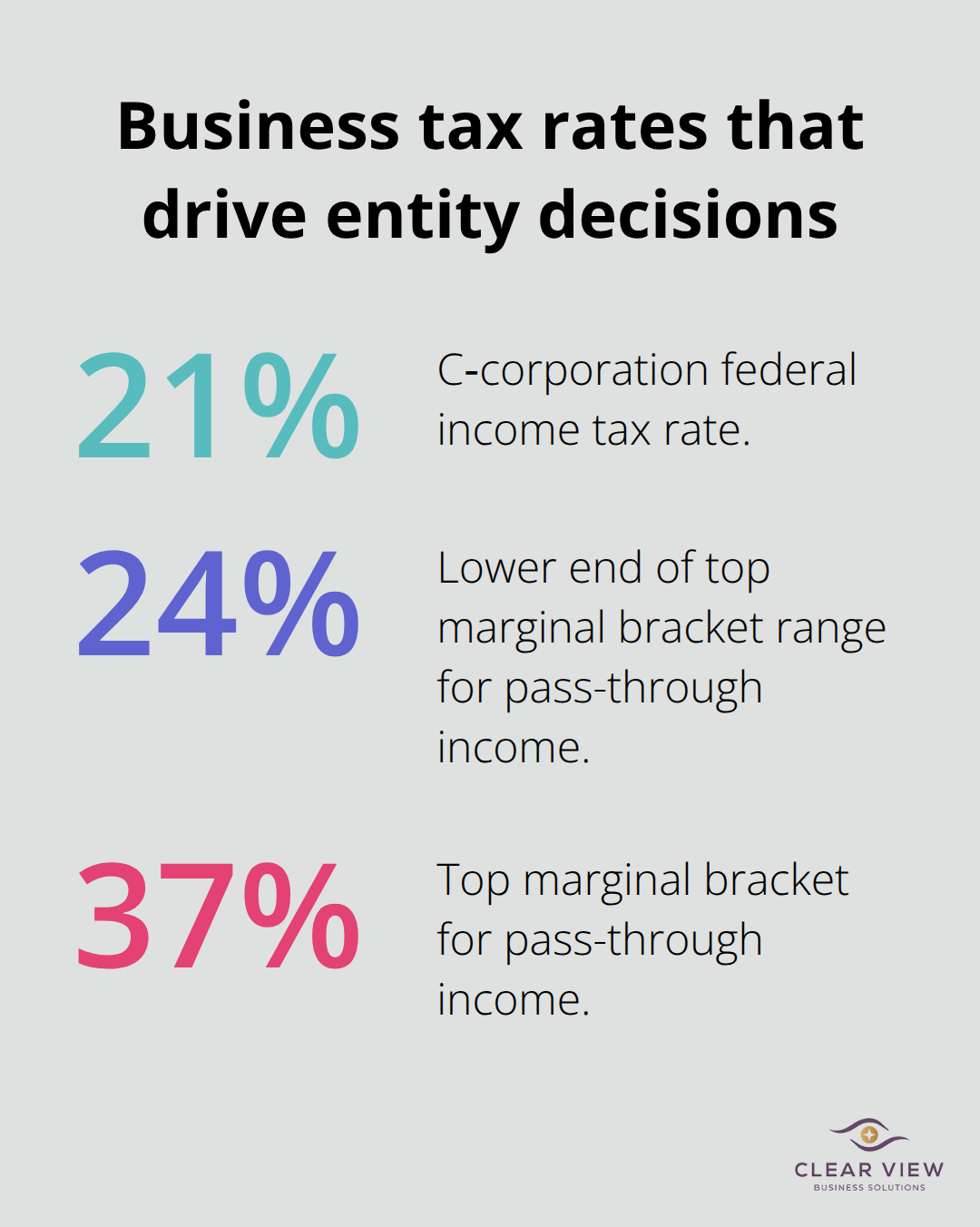

Your choice of business entity directly determines how much federal income tax you pay annually. The difference between operating as a sole proprietorship versus an S-corporation can save $15,000 to $40,000 yearly depending on your income level, yet most high-net-worth business owners never optimize this decision. The IRS taxes C-corporations at a flat 21% rate, but C-corps create double taxation when you distribute profits as dividends to yourself, making them inefficient for most situations.

S-corporations and LLCs taxed as S-corps avoid this trap by passing income through to your personal return at your marginal rate, which ranges from 24% to 37% in the top brackets.

The real advantage emerges through self-employment tax savings. Sole proprietors and partnerships pay 15.3% self-employment tax on all net earnings, while S-corp owners pay themselves a reasonable salary subject to payroll taxes, then take remaining profits as distributions that escape self-employment tax entirely. A business generating $200,000 in net income as a sole proprietor costs roughly $30,600 in self-employment tax, but structured as an S-corp with a $120,000 salary and $80,000 distribution, you pay approximately $18,400 in payroll taxes, saving $12,200 annually. This strategy works because the IRS requires S-corp owners to pay themselves a reasonable salary for work performed, preventing abuse, but distributions beyond that threshold avoid the 15.3% tax.

LLCs offer flexibility by allowing you to choose taxation as either a sole proprietorship, partnership, or S-corp depending on your income level and business structure. Family LLCs and Limited Partnerships serve additional purposes beyond tax reduction. These entities hold appreciated assets and enable minority interest gifts at valuation discounts for estate planning, creating a dual benefit that compounds over decades.

Business expenses reduce taxable income dollar-for-dollar, but only if you track and document them properly. Home office deductions apply if you use a dedicated space exclusively for business. You can deduct either 5% of your home’s rent or mortgage plus utilities proportionally, or use the simplified method of $5 per square foot up to 300 square feet annually. Vehicle expenses allow either actual expense tracking of fuel, maintenance, and depreciation, or the standard mileage rate of 67.5 cents per mile for 2025 according to the IRS. Most business owners miss significant deductions because they fail to maintain detailed records throughout the year.

Health insurance premiums you pay for yourself and employees reduce your business income directly. Retirement contributions through SEP-IRAs or Solo 401(k)s offer substantial tax deferral, allowing contributions up to 25% of net self-employment income with a maximum of $69,000 for 2025, far exceeding the $23,500 limit for W-2 employees. Business meals and entertainment expenses require documentation showing the business purpose and attendees, with 50% deductibility for meals under current tax law. Depreciation on equipment, furniture, and vehicles spreads costs over multiple years, reducing taxable income while you benefit from the asset.

The IRS Section 179 expensing rule lets you deduct up to $1 million of equipment purchases in the year acquired rather than depreciating over time, though this phases down with total purchases exceeding $2.5 million. These deductions interact directly with your entity choice, since S-corps and partnerships allocate deductions differently than sole proprietorships, affecting whether deductions benefit you or create losses that carry forward.

The tax strategies for high-net-worth individuals covered throughout this post work best when you coordinate them as a system rather than apply them in isolation. Maxing retirement accounts, harvesting losses, optimizing your business structure, and planning your estate all interact with each other-a decision about your business entity affects how much self-employment tax you pay, which influences how much you can contribute to retirement plans, which changes your overall tax bracket and the value of charitable deductions. This interconnection explains why scattered tax moves often disappoint while integrated planning delivers substantial results.

Professional tax planning transforms these strategies from theoretical concepts into concrete savings. A qualified advisor identifies which tactics apply to your specific situation, sequences them in the right order, and adjusts them as your circumstances change. The difference between handling taxes yourself and working with someone who understands high-net-worth planning often exceeds tens of thousands of dollars annually, especially when business ownership, significant investments, or estate considerations enter the picture.

At Clear View Business Solutions, we help individuals and business owners in Tucson implement tax strategies that actually stick. Contact us today to discuss how integrated tax planning can improve your after-tax wealth.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2933 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.