Crypto investors often leave thousands of dollars on the table each year by missing basic tax optimization opportunities. The IRS treats cryptocurrency transactions differently than stocks, and most people don’t understand these rules until tax season arrives.

At Clear View Business Solutions, we’ve helped investors implement crypto tax strategies that actually work. This guide walks you through the mistakes to avoid, the techniques that reduce your tax bill, and the systems you need to stay compliant.

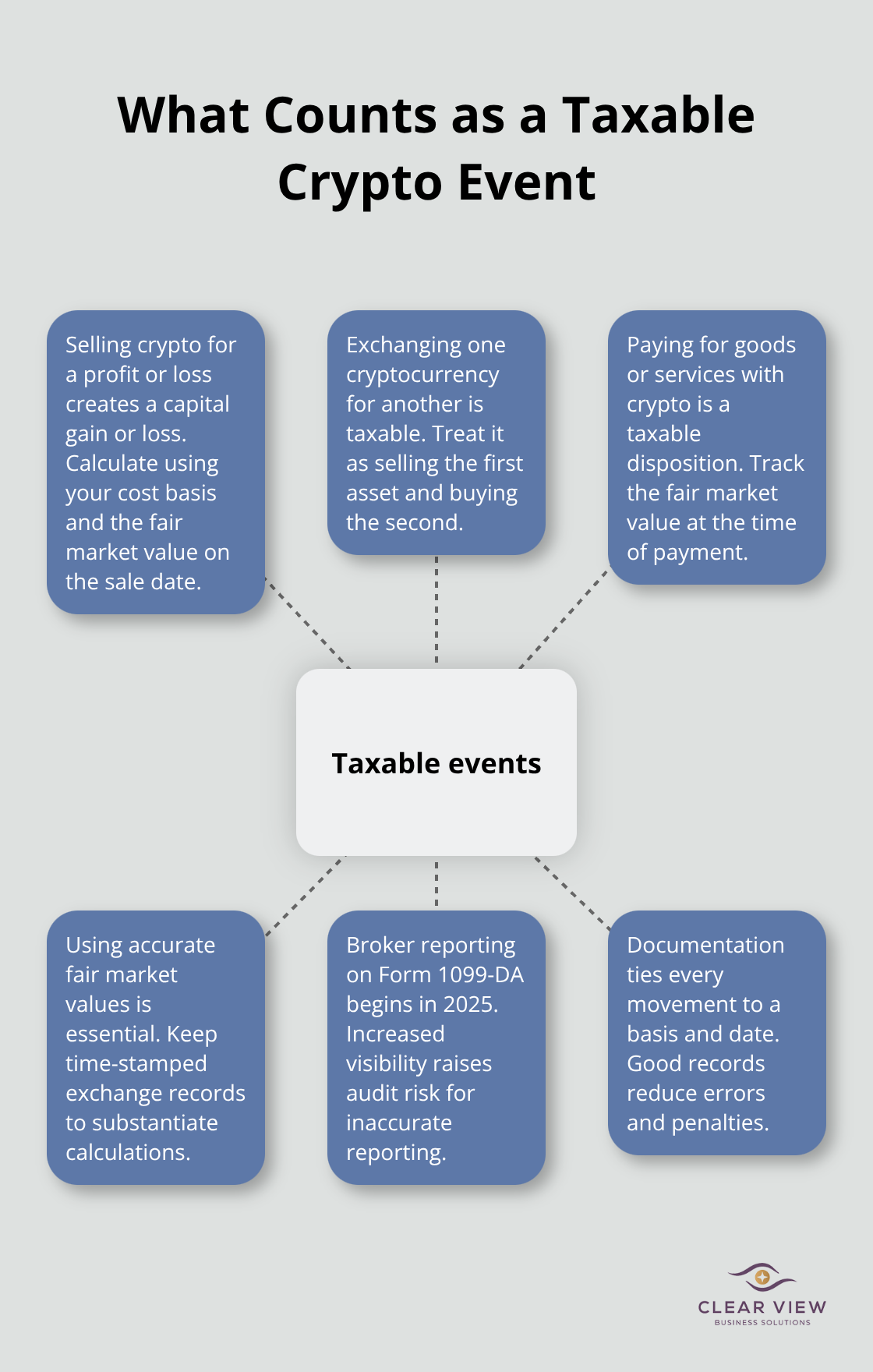

The IRS classifies cryptocurrency as property, not as a security or currency. This distinction matters because it changes how you calculate gains and losses.

According to IRS Notice 2014-21, you trigger a taxable event when you sell crypto for a profit, exchange one cryptocurrency for another, or use crypto to pay for goods or services. Most investors miss this last point: paying with Bitcoin for coffee or a service counts as a taxable disposition, not just selling on an exchange. You must calculate the gain or loss based on the fair market value at the time of the transaction, which means tracking not just your purchase price but also the exact date and value when you spent the crypto.

Starting January 1, 2025, brokers must report all crypto sales to the IRS on the new Form 1099-DA. In 2026, they will include your cost-basis data for purchases made on their platform. This means the IRS now has direct visibility into your transactions, and inaccurate reporting creates audit risk.

Receiving crypto triggers ordinary income tax, not capital gains tax. If you earn crypto as salary, mining rewards, staking income, or from airdrops and hard forks, that income is taxable at the fair market value on the day you received it. Mining and staking create immediate tax liability even if you haven’t sold anything. This is where most crypto holders get blindsided: you owe taxes on staking rewards worth $5,000 even if you hold that crypto and it drops to $3,000 by year-end.

You cannot offset that ordinary income with capital losses from selling other crypto at a loss. However, you can use capital losses to offset capital gains first, then up to $3,000 of ordinary income annually. If you conduct crypto activities as part of a trade or business, your income is reported on Schedule C and subject to self-employment tax.

The distinction between holding crypto and actively trading it affects your tax treatment significantly. Casual investors report gains on Schedule D (Form 1040) using Form 8949, while frequent traders may be classified as dealers, which changes their entire tax structure. The IRS doesn’t publish a bright-line rule for when you cross into dealer status, so documenting your intent and frequency matters.

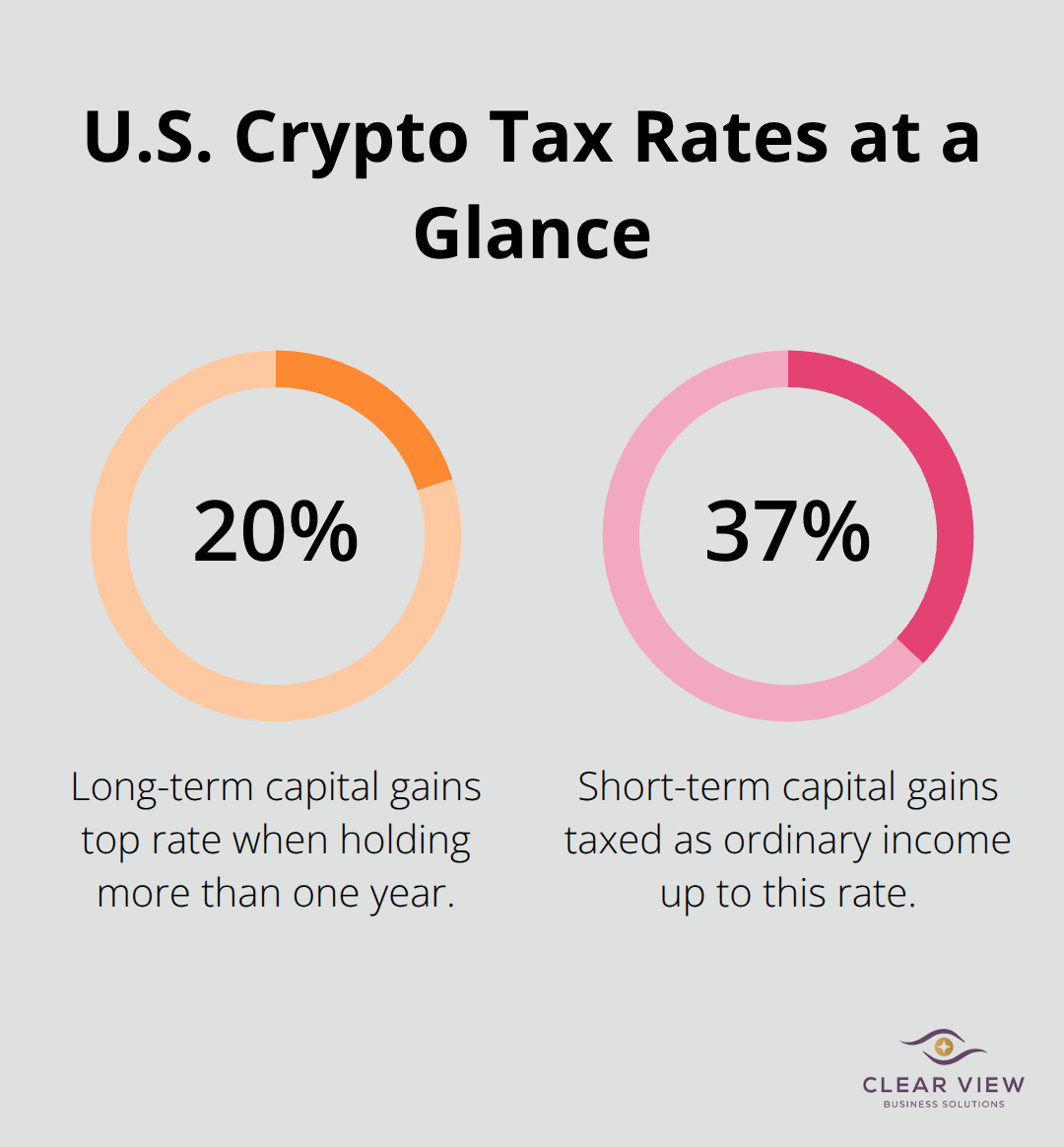

Long-term holdings of more than one year qualify for preferential capital gains rates ranging from 0% to 20%, while short-term holdings are taxed as ordinary income at rates up to 37%. This holding-period rule is your most powerful tax lever. Understanding these three categories-taxable dispositions, ordinary income events, and holding periods-sets the foundation for the tax strategies that actually reduce what you owe. The next section covers the mistakes that undermine these strategies and cost investors thousands each year.

Most crypto investors report only the obvious transactions: selling Bitcoin for dollars on an exchange or trading Ethereum for another token. The IRS sees it differently. Every crypto-to-crypto trade counts as a taxable event, which means swapping Solana for Dogecoin triggers capital gains or losses that must be reported. Many investors skip reporting these internal trades because no cash changes hands, but the IRS has blockchain analysis tools like Chainalysis that track these movements. Starting in 2026, Form 1099-DA will report your cost basis for purchases made on major exchanges, giving the IRS a direct comparison point to catch unreported trades.

Download your transaction history from every exchange you use and filter for every sale, trade, and income event. Most exchanges provide CSV exports that feed directly into tax software like Koinly or CoinLedger, which can auto-calculate gains and generate Form 8949 entries. This step eliminates the manual work and reduces calculation errors.

If you received crypto as payment for work, mining rewards, staking rewards and airdrops are ordinary income on the day you received it at fair market value. Ignoring this creates a mismatch between what the IRS knows and what you report, and penalties for underreporting crypto income can reach 75% of the unpaid tax under accuracy-related rules.

If you used crypto to buy anything-coffee, services, equipment-that transaction qualifies as a taxable disposition at the fair market value on that exact date. Treat every movement of crypto as potentially taxable until proven otherwise, then document the cost basis and date for each transaction.

Wash-sale rules don’t apply to crypto, which sounds like a tax advantage until you realize the IRS is watching for abuse. You can sell Bitcoin at a loss to harvest that loss for tax purposes, then immediately buy Bitcoin back without the 30-day waiting period that applies to stocks. This is legal tax planning, not tax evasion, but only if you actually realize genuine losses. The trap is selling crypto at an inflated loss claim or failing to use the actual fair market value on the sale date.

If you sold Bitcoin for $40,000 when it was trading at $45,000 that day, the IRS can challenge your loss calculation. Keep exchange records showing the exact price at the time of sale, not just the price you think it was worth.

Staking rewards and airdrops are where casual investors get caught. If you staked Ethereum and received 0.5 ETH worth $900 on June 15, you owe income tax on $900 even if you never touched that crypto. If Ethereum drops to $500 by December and you sell it, you then have a $400 capital loss. Many investors skip reporting the $900 income and only report the loss, which creates a red flag.

The IRS cross-references exchange deposits and blockchain records to identify staking income, so omitting it is high-risk. Track staking rewards with the same precision as salary: record the date, quantity, fair market value, and wallet address. If you claim capital losses from selling that staked crypto later, the income and loss must both appear on your return to be consistent. Understanding these reporting gaps sets the stage for the tax reduction strategies that actually work-strategies that depend on accurate records and honest calculations.

Tax-loss harvesting without a 30-day wash-sale restriction separates crypto investors who pay thousands in unnecessary taxes from those who optimize their returns. Unlike stock investors who must wait 30 days to repurchase after selling at a loss, crypto has no wash-sale restriction. You can sell Bitcoin at a loss today and buy it back tomorrow, locking in the loss for tax purposes while maintaining your position.

The mechanics work straightforwardly. If you bought Bitcoin at $50,000 and it drops to $40,000, you sell immediately and realize a $10,000 loss. That loss offsets capital gains from other crypto sales dollar-for-dollar, then reduces ordinary income by up to $3,000 per year, with excess losses carrying forward indefinitely. The critical factor is timing. You must execute these sales before December 31 to claim losses in the current tax year. Most investors wait until mid-December, but prices move fast and you lose the opportunity if you hesitate.

Set calendar reminders in October to review your portfolio for underwater positions, then execute trades with enough time for settlement. Tax software like Koinly automatically flags harvesting opportunities by comparing your holdings against current prices, eliminating manual calculation work. When harvesting losses across multiple coins, prioritize coins with the largest unrealized losses first, since those create the biggest tax offsets. If you hold 0.5 Bitcoin down $8,000 and 10 Ethereum down $2,000, harvest the Bitcoin loss first to maximize impact.

Timing your sales around your annual income matters far more than most investors realize. Short-term capital gains taxed as ordinary income up to 37% versus long-term gains at 0-20%, with holdings over one year qualifying for preferential rates depending on your tax bracket. Holding an asset just 32 days longer can cut your tax rate in half.

A second timing strategy involves deferring sales into lower-income years. If you took a sabbatical, started a business that lost money, or experienced a temporary income drop, selling crypto during that year captures gains at lower marginal rates. Someone in the 22% bracket pays $2,200 tax on a $10,000 gain, while the same gain costs $3,700 in the 37% bracket. This difference compounds across multiple transactions, making income timing one of your most powerful levers.

Cost basis tracking determines whether you actually capture these advantages. When you sell crypto, you must identify which coins you are selling, and different identification methods produce different tax outcomes. Most exchanges default to FIFO (first in, first out), meaning the oldest coins sell first, but you can use specific identification to choose which coins sell and minimize gains.

If you bought Bitcoin in three separate transactions at $30,000, $40,000, and $50,000, and you sell one unit, you can designate the $50,000 purchase as the one you are selling, reducing your gain to zero. This requires documenting your election in writing before or at the time of sale, and keeping exchange records showing your purchase dates, quantities, and prices. Download CSV transaction history from every exchange immediately after each trade, then upload it into tax software that supports specific identification.

Services like Koinly and CoinLedger integrate directly with major exchanges through API, automatically importing transactions and letting you choose your cost-basis method before generating tax reports. This automation eliminates the manual spreadsheet work where calculation errors typically occur. The IRS expects you to report crypto transactions using Form 8949 and Schedule D, and brokers now issue Form 1099-DA starting in 2025, creating a paper trail the IRS can match against your return.

Inaccurate cost basis claims trigger audits faster than almost any other crypto issue, so prioritize this accuracy over everything else. Maintain a master spreadsheet that mirrors your tax software entries, creating a backup verification system that catches discrepancies before filing. This dual-record approach takes an extra hour per quarter but prevents costly mistakes when the IRS compares your reported gains against broker-reported data.

Crypto tax optimization requires three core actions: you must track every transaction accurately, understand which events trigger taxes, and execute strategies before year-end. The difference between investors who pay thousands in unnecessary taxes and those who minimize their liability comes down to documentation and timing, not luck or complex formulas. Form 1099-DA arrives in 2025, giving the IRS direct visibility into your transactions, so inaccurate reporting creates audit risk that costs far more than any taxes you might save.

We at Clear View Business Solutions help individuals and small business owners implement crypto tax strategies that reduce what you owe while keeping you compliant with IRS requirements. Our team identifies optimization opportunities you might miss on your own, from choosing the right cost-basis method to planning sales around your income and tax bracket. Whether you need help setting up record-keeping systems or navigating business income and staking rewards, professional support pays for itself through tax savings and reduced audit risk.

Start by downloading your complete transaction history from every exchange you use, then upload it into tax software that supports your preferred cost-basis method. Set a calendar reminder for October to review your portfolio for tax-loss harvesting opportunities, and reach out to a tax professional who specializes in crypto if your situation involves multiple exchanges or business income.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2933 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.