Tax planning for business owners is a critical aspect of financial management that can significantly impact your company’s bottom line. At Clear View Business Solutions, we’ve seen firsthand how effective tax strategies can lead to substantial savings and improved cash flow.

This blog post will guide you through the essential elements of tax planning, providing practical strategies to optimize your business’s tax position and avoid common pitfalls. We’ll also highlight the long-term benefits of proactive tax planning for sustainable business growth.

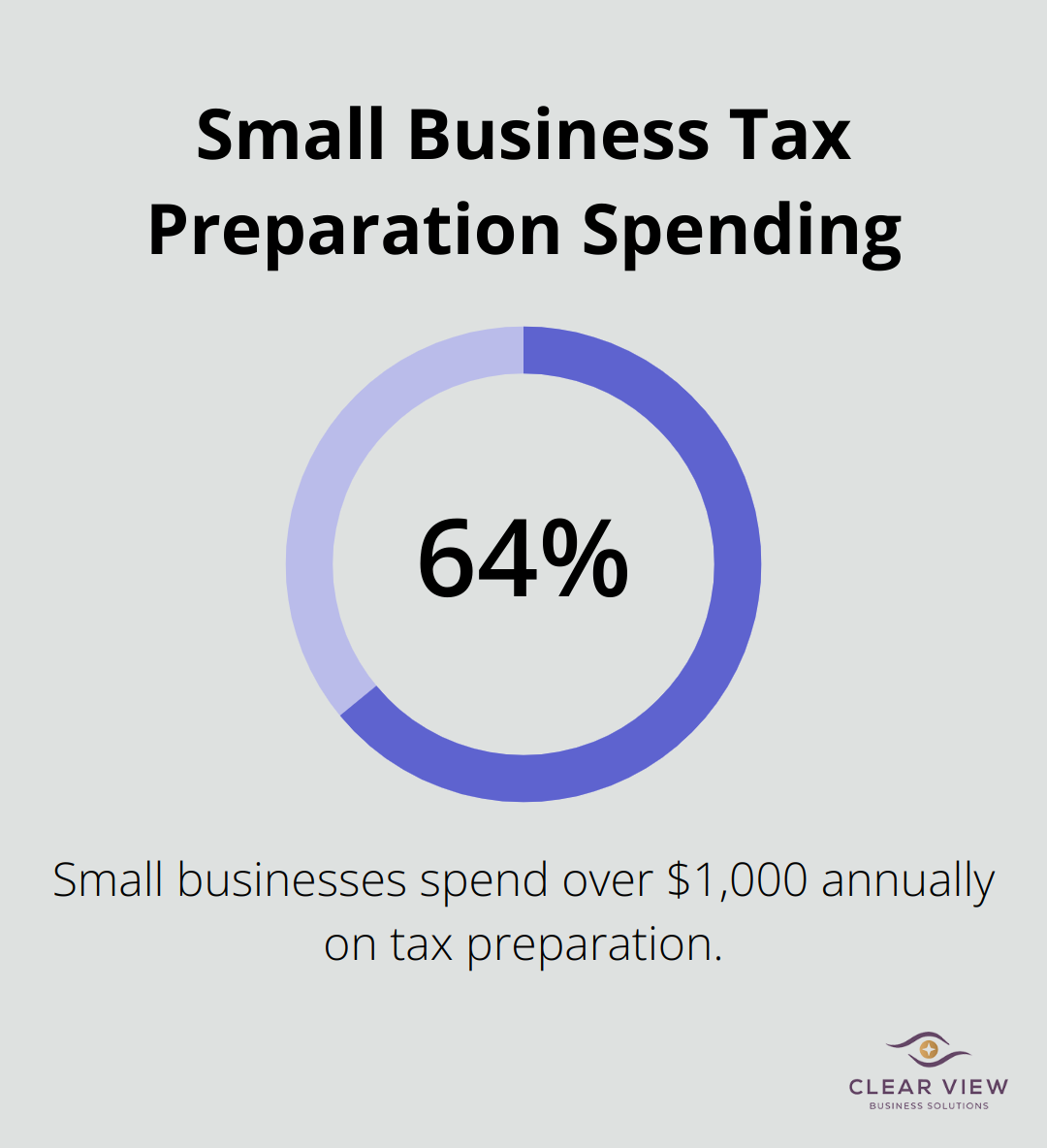

Tax planning is a strategic approach to manage business finances and minimize tax liabilities while complying with tax laws. This process directly impacts a company’s bottom line. The National Small Business Association reports that 64% of small businesses spend over $1,000 annually on tax preparation. However, businesses that engage in proactive tax planning often save significantly more than they spend on these services.

The IRS allows cash-basis taxpayers to defer income to the following year by delaying billing until January. This strategy can benefit businesses that expect to be in a lower tax bracket next year.

The Section 179 deduction allows businesses to deduct up to $1,250,000 for qualifying equipment purchases in 2025. This deduction can substantially reduce taxable income for businesses planning major equipment upgrades.

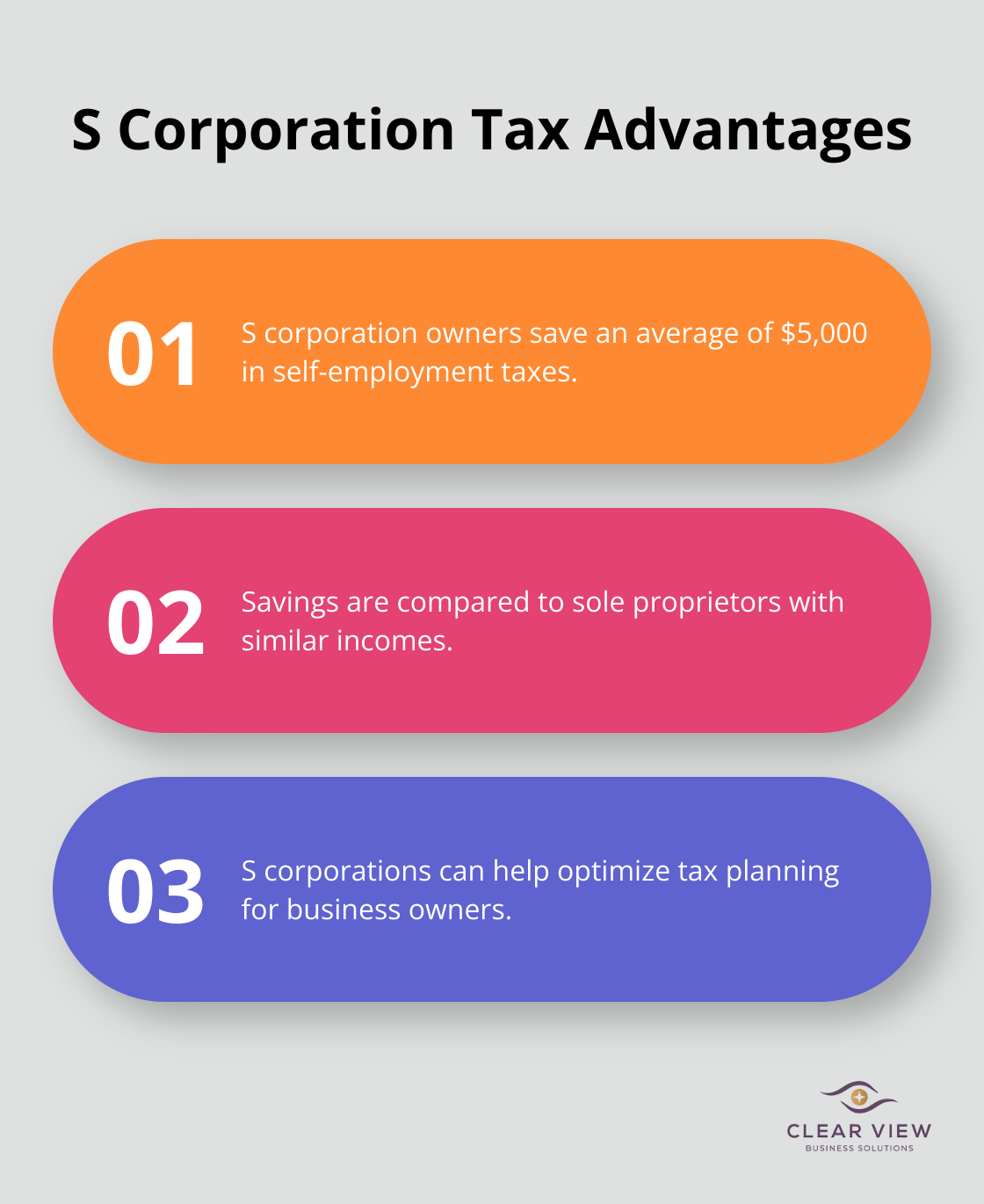

Your business structure significantly influences your tax obligations. S corporations can help owners save on self-employment taxes. A U.S. Treasury study found that S corporation owners paid an average of $5,000 less in self-employment taxes compared to sole proprietors with similar incomes.

Tax planning extends beyond reducing the current year’s tax bill. It involves creating a long-term strategy that aligns with business goals. This might include setting up retirement plans with tax advantages, such as a SEP IRA. For 2025, SEP IRAs allow contributions of up to 25% of the employee’s compensation, or $69,000, whichever is less.

Tax laws change frequently. The Tax Cuts and Jobs Act of 2017 brought significant changes, and more are expected in the coming years. Staying informed and adjusting your strategy accordingly is essential for effective tax planning.

As we move forward, let’s explore specific strategies to optimize your business tax planning and maximize your financial benefits.

Your business structure significantly impacts your tax obligations. S corporations can help owners save on self-employment taxes. However, the best structure depends on your specific situation. Consult with a tax professional to determine the most advantageous structure for your business.

Take full advantage of available deductions and credits. The Section 179 deduction allows businesses to deduct up to $1,250,000 for qualifying equipment purchases in 2025. This can substantially reduce your taxable income if you plan major equipment upgrades. Don’t overlook smaller deductions like office supplies, business travel, or professional development expenses. These can add up to significant savings over time.

Timing plays a crucial role in tax planning. Cash-basis taxpayers can defer income to the following year by delaying billing until January. This strategy benefits businesses that expect to be in a lower tax bracket next year. Conversely, if you anticipate being in a higher tax bracket next year, you might want to accelerate income into the current year and defer expenses to the next.

Setting up a retirement plan not only secures your financial future but also offers immediate tax benefits. SEP IRAs allow contributions of up to 25% of the employee’s compensation or $69,000 (whichever is less) for 2025. These contributions are tax-deductible, reducing your current tax liability while building your retirement nest egg.

Tax laws constantly evolve. The Tax Cuts and Jobs Act of 2017 brought significant changes, and more are expected in the coming years. Stay informed about these changes for effective tax planning. Subscribe to reputable tax news sources or work with a tax professional who can keep you updated on relevant changes.

As you implement these strategies, it’s important to consider the potential pitfalls that can derail even the best-laid tax plans. Let’s explore some common tax planning mistakes and how to avoid them.

Accurate and organized records form the foundation of effective tax planning. The IRS requires businesses to maintain records that support income, expenses, and credits claimed on tax returns for at least three years. We recommend keeping records for seven years to be safe. Use accounting software like QuickBooks to streamline this process. A survey by Wasp Barcode Technologies found that 55% of small business owners dislike bookkeeping the most among their tasks. Don’t let this aversion lead to neglect – poor record-keeping can result in missed deductions and potential audits.

Misclassification of employees as independent contractors is a common and costly mistake. The IRS estimates that 15% of employers misclassify workers, leading to billions in lost tax revenue. This error can result in back taxes, penalties, and interest. To avoid this, use the IRS’s 20-factor test to determine worker status. If you’re unsure, classify workers as employees. The consequences of misclassification far outweigh any short-term savings.

Many businesses focus solely on federal taxes, overlooking state and local obligations. This oversight can lead to unexpected tax bills and penalties. Each state has unique tax laws, and some cities impose additional taxes. For example, New York City has a 4% unincorporated business tax (on top of state and federal taxes). If you operate in multiple states, you may need to file multiple state tax returns. Try to understand your obligations across different jurisdictions to avoid surprises.

Failure to make estimated tax payments is a common oversight that can result in penalties. The IRS requires most businesses to make quarterly estimated tax payments if they expect to owe $1,000 or more in taxes. Set reminders for the quarterly due dates (April 15, June 15, September 15, and January 15) and use the Electronic Federal Tax Payment System (EFTPS) for easy online payments. Underpayment penalties can be as high as 6% of the unpaid tax, so it’s critical to stay on top of these payments.

Many businesses miss out on valuable tax credits simply because they’re unaware of them. The Research and Development (R&D) tax credit is often overlooked. Eligible organizations include those that have under $5 million in gross receipts in the current year and no more than 5 years of generating gross receipts. Other commonly missed credits include the Work Opportunity Tax Credit and various energy efficiency credits. Review available credits regularly or work with a tax professional to ensure you’re not leaving money on the table.

Tax planning for business owners forms a cornerstone of financial success. Strategic approaches reduce tax burdens and improve bottom lines. However, businesses must avoid common pitfalls such as poor record-keeping and employee misclassification to reap the full benefits of tax planning.

The complexity of tax laws underscores the importance of professional guidance. Clear View Business Solutions specializes in comprehensive tax planning for small businesses and individuals in Tucson. Our expertise can help navigate the intricacies of tax planning while ensuring compliance and maximizing benefits.

Proactive tax planning aligns with business goals and fosters growth. It requires regular review and adjustment to adapt to evolving business needs and changing tax landscapes (especially given frequent legislative updates). Effective tax planning transforms a daunting task into a powerful tool for business growth and financial empowerment.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2933 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.