Income tax planning can make a big difference in your financial health. At Clear View Business Solutions, we’ve seen how smart tax strategies can save individuals and businesses thousands of dollars each year.

This post will share essential income tax planning tips to help you keep more of your hard-earned money. We’ll cover key strategies, common pitfalls to avoid, and why professional guidance matters.

Income tax planning is a strategic approach to manage finances and minimize tax liability while complying with tax laws. It involves analyzing your financial situation to identify opportunities for tax savings. This process includes understanding current tax laws, anticipating future changes, and making informed decisions about income, expenses, and investments.

Tax planning often revolves around the strategic timing of income and expenses. This approach can potentially lower your tax bracket. For example, self-employed individuals might delay sending invoices in December to push income into the next tax year if they expect to be in a lower tax bracket.

Another vital strategy involves maximizing contributions to tax-advantaged accounts. For 2025, individuals can contribute up to $23,500 to a 401(k), with an additional catch-up contribution of $11,250 for those 50 or older. These contributions reduce taxable income dollar-for-dollar, potentially resulting in a lower tax bracket.

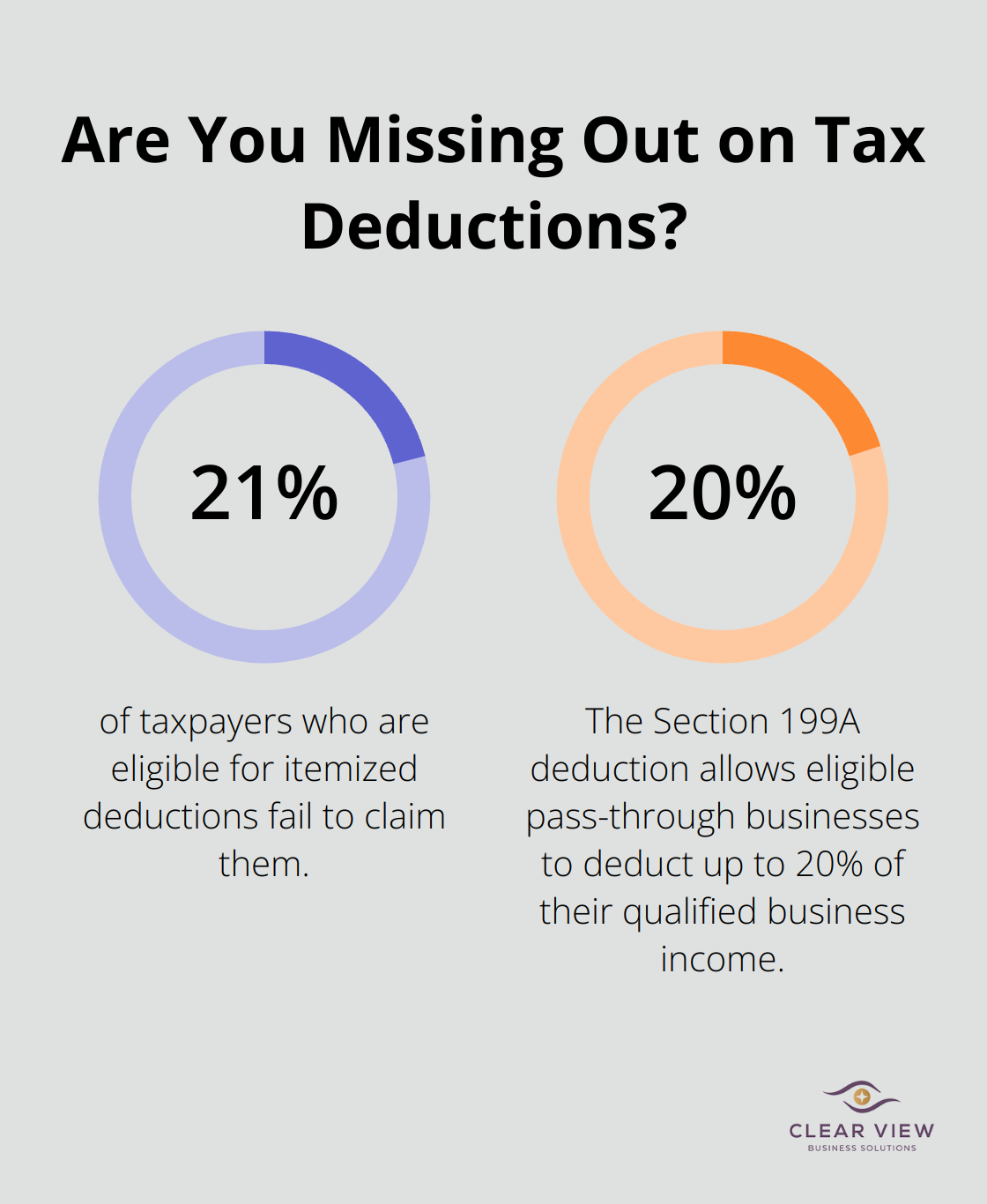

Proactive tax planning can lead to substantial savings for individuals. A study by the Government Accountability Office found that about 21% of taxpayers who are eligible for itemized deductions fail to claim them (missing out on potential tax savings).

Businesses benefit significantly from strategic tax planning. The Section 199A deduction allows eligible pass-through businesses to deduct up to 20% of their qualified business income. This can effectively reduce the top marginal tax rate for qualifying business owners.

Tax planning isn’t just about the current year; it’s about creating a long-term strategy that aligns with your financial goals. Contributing to a Roth IRA now means tax-free withdrawals in retirement, which can be a significant advantage if you expect to be in a higher tax bracket later in life.

Understanding these fundamental aspects of income tax planning sets the stage for implementing effective strategies to reduce your tax liability. The next section will explore specific tactics you can use to minimize your tax burden and maximize your financial well-being.

Above-the-line deductions are powerful tools for reducing your adjusted gross income (AGI). These deductions are available even if you don’t itemize. Some key above-the-line deductions include:

Strategic timing of income and expenses can significantly impact your tax bill. For instance, if you’re a freelancer or small business owner, consider delaying invoicing for work completed in December until January. This pushes the income into the next tax year, potentially lowering your current year’s tax bracket.

On the flip side, if you expect to be in a higher tax bracket next year, accelerating income into the current year might be beneficial. This could involve asking for year-end bonuses to be paid in December rather than January.

Contributions to traditional IRAs and 401(k)s can significantly reduce your taxable income. For 2024, you can contribute up to $23,000 to a 401(k), with an additional $7,500 catch-up contribution if you’re 50 or older. IRA contribution limits are $7,000, with a $1,000 catch-up contribution for those 50 and above.

A study by Vanguard found that the average 401(k) balance for those who consistently contributed over a 15-year period was $370,000, compared to just $90,000 for those who didn’t contribute regularly. This underscores the power of consistent retirement savings, both for your future and your current tax situation.

For business owners, selecting the appropriate business structure can have a major impact on taxes. The Tax Cuts and Jobs Act introduced a 20% qualified business income deduction for pass-through entities (like S corporations and LLCs). This can result in significant tax savings for eligible businesses.

However, the right structure depends on various factors, including your income level, business type, and long-term goals. Professional guidance can help you navigate these complex decisions to optimize your tax situation.

Tax laws are complex and constantly changing. Working with a professional tax advisor ensures you make the most of available opportunities while staying compliant with current regulations. Clear View Business Solutions specializes in helping small businesses and startups develop personalized tax strategies that align with their financial goals.

As we move forward, it’s important to understand that even with the best strategies, mistakes can happen. In the next section, we’ll explore common pitfalls in tax planning and how to avoid them, ensuring you maximize your tax-saving potential.

Accurate record-keeping forms the foundation of effective tax planning. The IRS reports that poor documentation ranks as one of the top reasons for audit adjustments. We recommend the use of digital tools to track expenses and income throughout the year. QuickBooks can serve as an excellent solution for small businesses. For individuals, apps like Mint or YNAB help categorize personal expenses that may qualify as tax-deductible.

Many taxpayers leave money on the table by overlooking valuable deductions and credits. The Government Accountability Office found that about 21% of eligible taxpayers fail to claim itemized deductions they qualify for. Some commonly missed deductions include:

To maximize your tax savings, create a checklist of potential deductions and credits relevant to your situation. Review this list with a tax professional annually to ensure you don’t miss out on any opportunities.

Tax laws present notorious complexity and constant change. The Tax Cuts and Jobs Act of 2017 made significant changes that still cause confusion for many taxpayers. For instance, the new 20% qualified business income deduction for pass-through entities has intricate rules that many business owners struggle to interpret correctly.

Staying informed proves essential. Subscribe to reputable tax news sources or consider working with a tax professional who stays current on legislative changes. Many firms (including Clear View Business Solutions) make it their mission to stay ahead of tax law changes to provide clients with the most up-to-date advice.

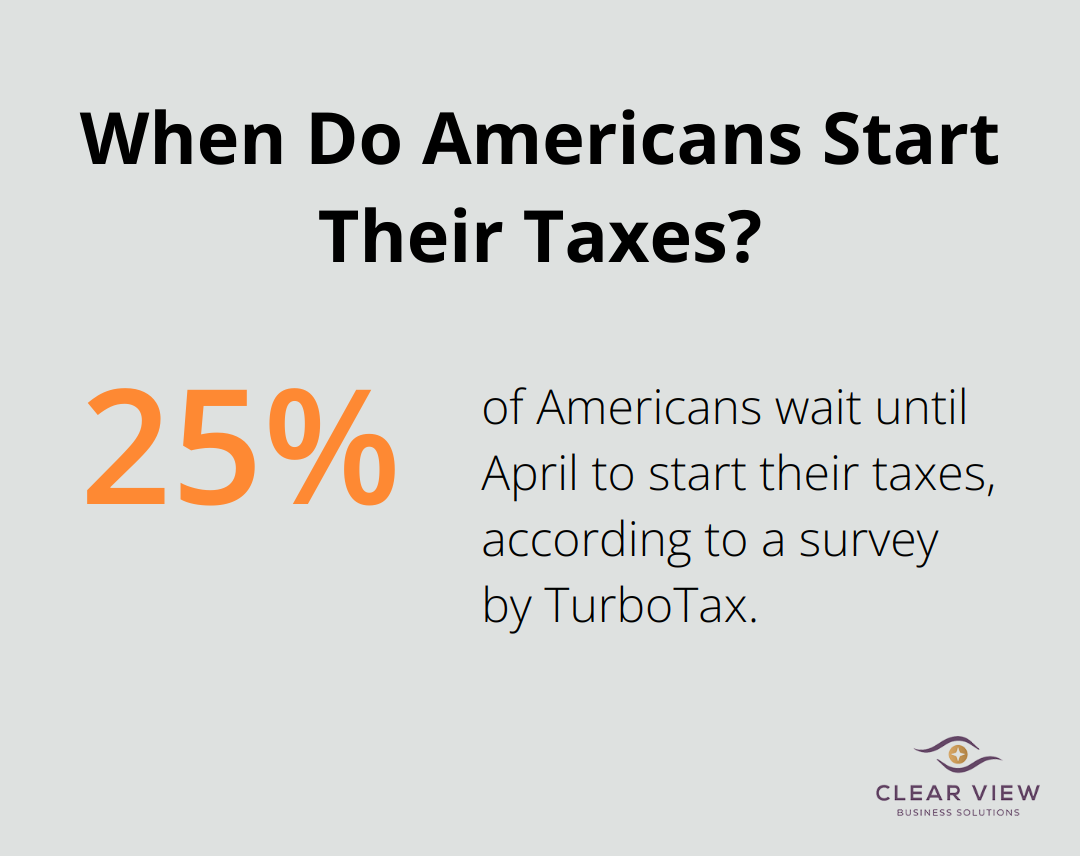

Last-minute tax planning often leads to rushed decisions and missed opportunities. A survey by TurboTax found that 25% of Americans wait until April to start their taxes. This procrastination can result in overlooked deductions, errors in filing, and missed deadlines for tax-saving strategies like retirement account contributions.

Implement a year-round tax planning approach. Set quarterly reminders to review your tax situation, adjust withholdings if necessary, and explore potential tax-saving investments or strategies. This proactive approach can lead to significant savings and reduce stress during tax season.

Many individuals and businesses attempt to navigate the complex world of taxes on their own, often to their detriment. Professional tax advisors (such as those at Clear View Business Solutions) can provide valuable insights, identify overlooked deductions, and ensure compliance with ever-changing tax laws.

Effective income tax planning tips can significantly impact your financial well-being. You can substantially reduce your tax liability through strategies like maximizing deductions, timing income and expenses wisely, and fully utilizing retirement accounts. Choosing the right business structure and staying informed about tax law changes will also optimize your tax situation.

The complex world of taxes requires ongoing attention, meticulous record-keeping, and a deep understanding of ever-changing laws. Professional guidance becomes invaluable in this context. At Clear View Business Solutions, we provide comprehensive tax services and personalized advice to individuals and small businesses in Tucson.

Our expertise in areas such as ITIN setup, tax planning, and IRS representation can help you avoid common pitfalls and maximize your tax benefits. A well-executed strategy contributes to financial stability, supports business growth, and helps you achieve your long-term financial goals. The most effective income tax planning approach is tailored to your unique situation.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2933 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.