If you own a pass-through entity like an S-corp, partnership, or LLC, you’re sitting on a significant tax advantage. The pass-through deduction can reduce your taxable income by up to 20%, but only if you structure it correctly.

At Clear View Business Solutions, we’ve seen business owners leave thousands of dollars on the table by missing eligibility requirements or making calculation errors. This guide walks you through exactly how to claim this deduction and avoid the most common pitfalls.

The pass-through deduction applies to owners of S-corporations, partnerships, sole proprietorships, and certain LLCs that elect to be taxed as partnerships or S-corporations. If you operate your business through one of these structures, you can claim up to a 20% deduction on your qualified business income. C-corporations do not qualify for this deduction, which is a critical distinction that affects how you should structure your business. The IRS allows this deduction regardless of whether you take the standard deduction or itemize, making it available to virtually every pass-through owner who meets the income and business-type requirements.

Your taxable income determines whether you receive the full 20% deduction or face limitations. For 2024, if you’re single and earn less than $191,950 in taxable income, or married filing jointly with less than $383,900, you qualify for the full deduction without restrictions on W-2 wages or property values. Once you cross into the $191,950 to $241,950 range for singles (or $383,900 to $483,900 for married filers), the deduction begins phasing out and becomes subject to wage and property limitations. Above $241,950 for singles or $483,900 for married filers, the deduction disappears completely unless you meet specific wage or property requirements. These thresholds matter enormously because they determine your calculation method and potential deduction amount. A partnership owner earning $192,000 faces completely different rules than one earning $191,000, so you must know exactly where your income falls.

Certain professions face stricter rules that can eliminate the deduction entirely above the income thresholds. If you work in health, law, accounting, financial services, performing arts, or consulting, the IRS classifies your business as a Specified Service Trade or Business (SSTB). Below the threshold, these restrictions don’t apply, but once you exceed the income limits, the deduction disappears completely for SSTB owners unless they meet narrow wage and property requirements. This means a consulting firm with $250,000 in revenue could lose the entire 20% deduction, while a manufacturing business at the same income level might preserve most of it through qualified property. The catch-all definition for SSTBs includes any business where the principal asset is the reputation or skill of employees, which creates gray areas that require careful analysis. If you’re uncertain whether your business qualifies as an SSTB, you should make this determination before year-end so you can adjust your strategy accordingly.

The entity type you choose directly impacts how much deduction you ultimately claim. An S-corporation owner who pays reasonable compensation creates W-2 wages that feed into the wage limitation calculation, potentially unlocking additional deduction room. A sole proprietor with the same income faces different wage calculations because they don’t issue W-2s to themselves. Partnerships allocate QBI and W-2 wages to partners based on their ownership percentages, which means each partner’s deduction varies individually. LLCs that elect to be taxed as S-corporations or partnerships follow the rules of their elected entity type. These structural differences mean two business owners with identical income and business types can claim vastly different deductions based on how they’ve organized their entities.

Understanding your entity structure and income position sets the foundation for calculating your actual deduction amount.

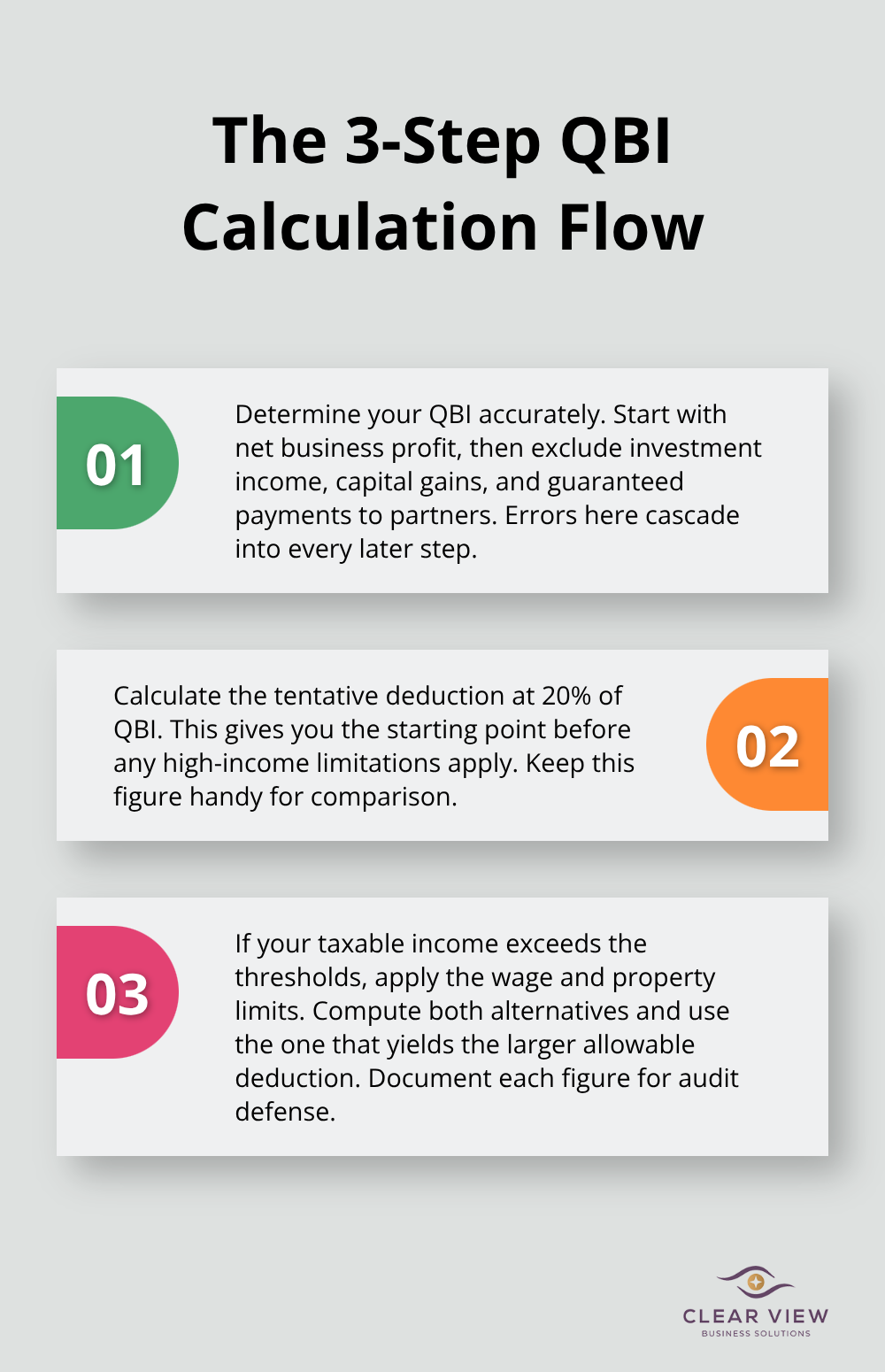

The calculation itself seems straightforward-take 20% of your qualified business income-but the IRS has layered in restrictions that change everything once your income exceeds certain thresholds. Your actual deduction depends on three separate calculations that you must run in sequence, and most business owners make errors in at least one of them. The first step is determining your qualified business income, which is your net business profit minus any W-2 wages you paid to employees and excluding investment income, capital gains, and guaranteed payments to partners.

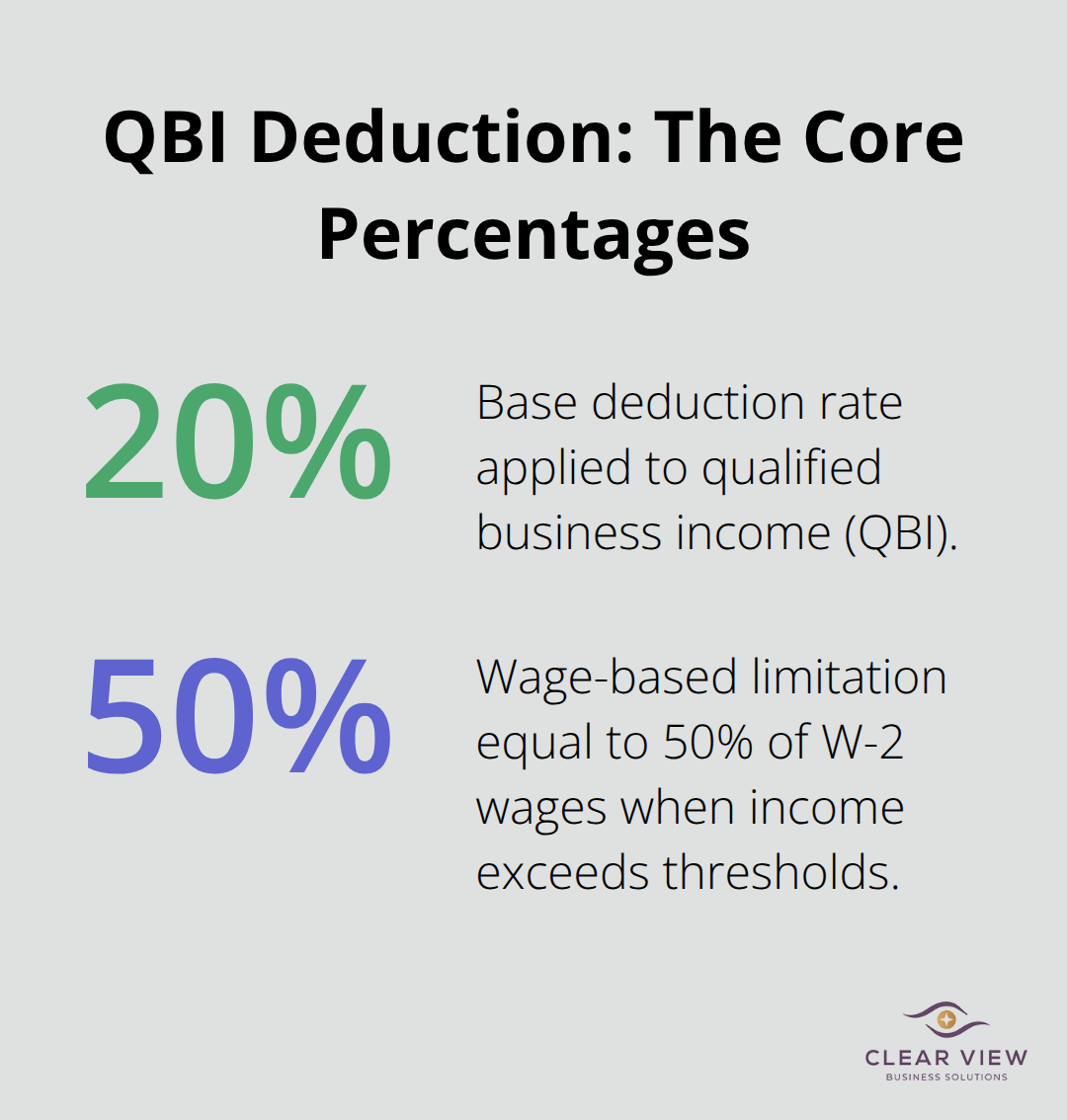

This number forms the foundation of your deduction, so if you miscalculate here, everything downstream falls apart. Once you have your QBI, you calculate a tentative deduction of 20% of that amount. Then you hit the wage and property limitations, which act as a ceiling on your deduction if your income exceeds the 2024 thresholds of $191,950 (single) or $383,900 (married filing jointly). These limitations exist to prevent high-income owners from claiming excessive deductions, and they’re where most owners either miss opportunities or make costly errors.

If your income falls below the threshold, you skip the wage and property calculation entirely and simply claim 20% of your QBI. Once you cross that line, you must calculate two alternative limits and use whichever produces the larger deduction. The first alternative is 50% of the W-2 wages you paid during the year to employees working in your business. If you paid $100,000 in W-2 wages, this limit allows you to deduct up to $50,000 worth of QBI at the 20% rate.

The second alternative is more complex: 25% of W-2 wages plus 2.5% of the unadjusted basis of qualified property you own. This second calculation helps capital-intensive businesses and real estate owners preserve larger deductions. A real estate partnership with $800,000 in QBI and $10 million in property basis can claim a deduction of $250,000 (25% of wages plus 2.5% of $10 million) even if it paid minimal W-2 wages. Your actual deduction cannot exceed the greater of these two calculations. Many owners focus only on wages and ignore the property basis component entirely, which costs them thousands in lost deductions. You must track depreciation schedules and basis calculations throughout the year to know your qualified property amount at tax time. If you own rental real estate, manufactured equipment, or other depreciable assets, pull those basis numbers now because they directly increase your deduction ceiling.

Real estate owners and capital-intensive businesses often overlook the 2.5% property basis rule, which can produce larger deductions than the wage calculation alone. The unadjusted basis immediately after acquisition (UBIA) includes the original cost of depreciable property you use in your business, and the IRS allows you to count 2.5% of this total toward your deduction limit. A manufacturing business with $5 million in equipment basis can add $125,000 to its wage-based limit, which transforms the deduction calculation entirely. You must own the property at year-end for it to count, and inventory and land do not qualify. Track your depreciation schedules carefully because they show your basis in each asset. If you purchased equipment mid-year, only the portion you owned at December 31 counts toward your basis calculation. Many owners fail to coordinate their depreciation elections (Section 179 or bonus depreciation) with their QBI planning, which means they miss opportunities to time basis deductions strategically.

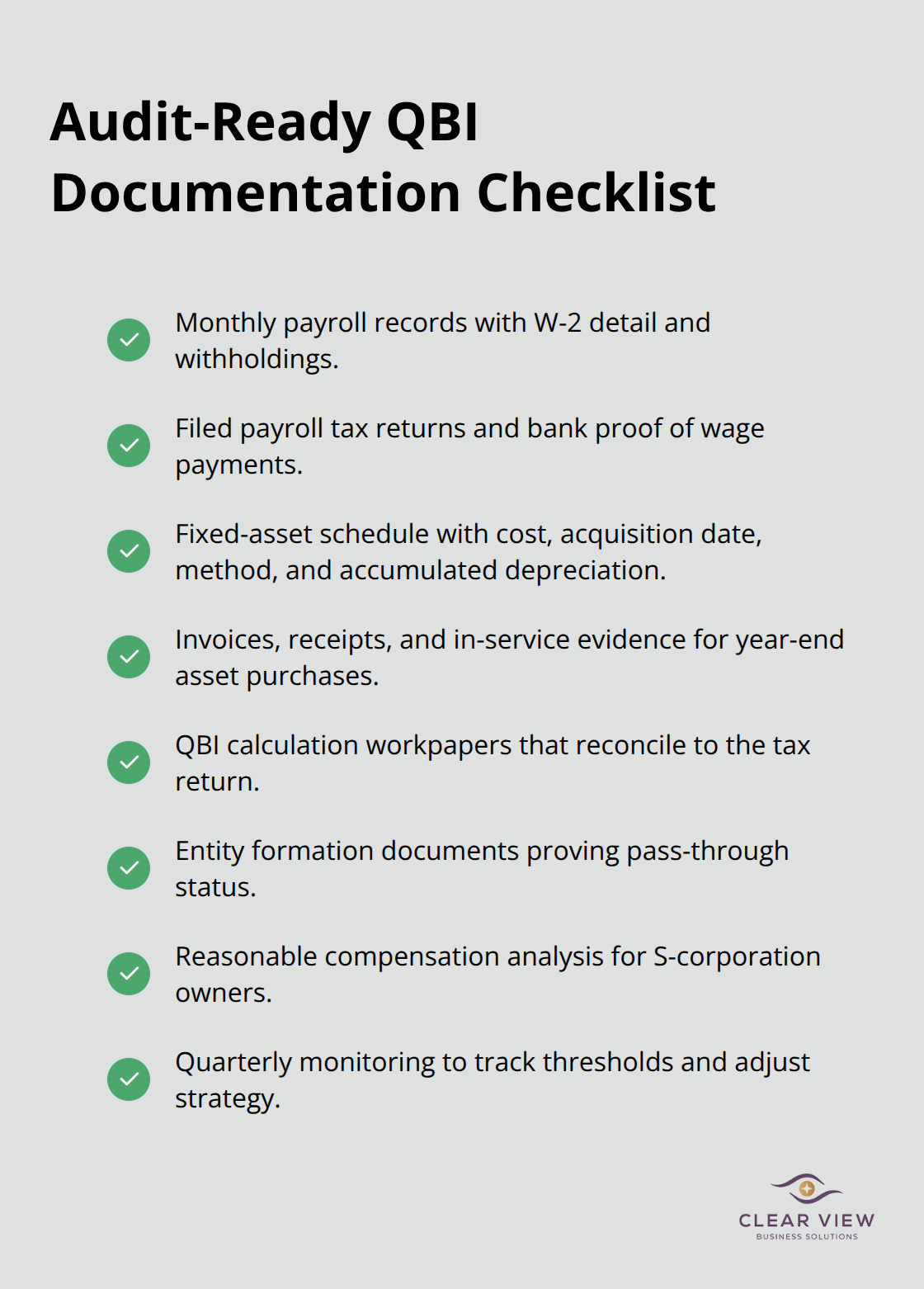

You need meticulous records showing your QBI calculation, W-2 wages paid by month, depreciation basis for all qualified property, and documentation proving your business qualifies as a pass-through entity. Many owners fail to maintain separate records for W-2 wages paid to themselves versus employees, which creates confusion during audit. S-corporation owners face particular risk because they must prove they paid reasonable compensation to themselves as W-2 wages. The IRS scrutinizes S-corps that show high QBI but minimal W-2 wages, and they will reclassify QBI as reasonable compensation if your wage structure looks unreasonable. A consulting S-corp generating $300,000 in net income that pays the owner $40,000 in W-2 wages will almost certainly face IRS challenges. Reasonable compensation means what you would pay a third party to do your job, so document your industry’s typical salary ranges and justify your specific wage choice. Keep your year-end depreciation schedule, monthly payroll records, and a calculation showing how you arrived at your QBI figure. Without this documentation, you cannot defend your deduction if audited, and the IRS will simply disallow it.

The way you structure your business directly impacts which wages count toward your deduction limit. An S-corporation owner who pays themselves reasonable W-2 compensation creates wages that feed into the limitation calculation, potentially unlocking additional deduction room. A sole proprietor with the same income cannot issue W-2s to themselves, which means they have zero wages to use in the calculation unless they employ other staff. Partnerships allocate W-2 wages to partners based on their ownership percentages, so each partner’s deduction varies individually. This structural difference means two business owners with identical income can claim vastly different deductions based on how they’ve organized their entities. If you operate as a sole proprietor with no employees, your wage-based limit is zero, which forces you to rely entirely on the property basis calculation. This is why some sole proprietors benefit from converting to S-corporation status-the W-2 wages they pay themselves create a higher deduction ceiling. The conversion decision requires careful analysis of payroll taxes and other factors, so consult a tax professional before making structural changes.

Your calculation method and documentation practices directly determine whether you claim the full deduction you’re entitled to or face audit risk and penalties. The next section covers specific strategies that allow you to maximize your deduction through timing decisions and business structure choices.

The most overlooked strategy for maximizing your pass-through deduction involves deliberate timing of income and expenses within your control. Most business owners treat their year-end tax situation as fixed, but you have far more flexibility than you think if you plan strategically throughout the year. Your deduction calculation depends on your taxable income and QBI amount, both of which respond to timing choices you make before December 31. If you approach a threshold where wage or property limitations will activate, accelerating deductible expenses into the current year can keep your income below that threshold and preserve the full 20% deduction without restrictions. A consulting partnership generating $195,000 in projected income faces the phase-out zone starting at $191,950 for single owners, so investing $5,000 in equipment, software licenses, or professional development before year-end drops income below the threshold and eliminates the wage limitation entirely. This single decision preserves thousands in deduction value. Conversely, if you sit well above the threshold and already face wage limitations, deferring income to the next year while accelerating deductible expenses into the current year can improve your overall tax position across both years. A real estate partnership with $500,000 in QBI and $50,000 in W-2 wages faces a wage-based deduction limit of $25,000 (50% of wages), but if partners defer $100,000 in rental income to January, they reduce current-year QBI to $400,000 and potentially drop below the threshold entirely if other factors align. The tax planning strategies you implement require advance planning, not year-end scrambling, so you need visibility into your income trajectory by September at the latest.

Real estate owners and capital-intensive businesses unlock additional deduction room through deliberate depreciation timing. The property basis rule means your deduction ceiling increases with unadjusted basis you own at year-end, so purchasing depreciable assets before December 31 directly increases your deduction limit. A manufacturing business with $2 million in current equipment basis can add significant value to its wage-based deduction ceiling, but if that business delays a $500,000 equipment purchase to January, it loses potential deduction value immediately. Equipment purchases must be in service by year-end to count, so buying equipment in December only works if you actually place it in service and document that placement before the calendar flips. Section 179 expensing and bonus depreciation elections determine whether you deduct the full cost immediately or spread it across multiple years, and this choice affects your QBI differently depending on your income level. If you sit below the threshold, claiming bonus depreciation immediately reduces your current-year income and QBI, potentially keeping you below the phase-out zone. If you already sit above the threshold and face wage limitations, you might benefit from spreading depreciation across years to manage your QBI in a way that maximizes deductions over time. This strategy requires detailed coordination with your tax advisor because the math changes based on your specific situation, but the potential value is substantial. A real estate partnership that times equipment purchases and depreciation elections strategically can increase its deduction compared to a business that makes these decisions haphazardly.

The choice between operating as a sole proprietorship, partnership, S-corporation, or LLC fundamentally affects your wage-based deduction ceiling. A sole proprietor with $300,000 in net income and no employees has zero W-2 wages to use in the limitation calculation, which means they cannot exceed the 50% wage threshold and must rely entirely on property basis. Converting that same business to S-corporation status allows the owner to pay themselves reasonable W-2 compensation, which creates wages that feed the deduction calculation. If that owner pays themselves $150,000 in W-2 wages, the wage-based limit becomes $75,000, which dramatically increases the deduction room available. The conversion decision requires careful analysis because S-corporation taxation involves self-employment tax savings but also payroll processing costs and complexity, and the net benefit depends on your specific income level and business structure. For a consulting business generating $300,000 in net income, converting to S-corporation status typically saves $15,000 to $20,000 annually in self-employment taxes, which often exceeds the cost of payroll processing and compliance. However, you must pay reasonable W-2 compensation to yourself, which the IRS defines as what you would pay a third party to perform your role. The IRS scrutinizes S-corporations that show high income with minimal W-2 wages, so this strategy only works if your wage structure can withstand audit scrutiny. A consulting S-corp that generates $300,000 in net income but pays the owner $40,000 in wages will face IRS challenges, but one that pays $120,000 to $150,000 in wages creates legitimate deduction room that survives examination. Partnership owners face different considerations because they allocate QBI and wages individually, meaning each partner’s deduction varies based on their ownership percentage. A two-person partnership where one partner is an SSTB professional and the other owns non-SSTB rental property might benefit from restructuring to isolate those activities into separate entities, allowing the non-SSTB partner to claim the full deduction while the SSTB partner faces restrictions only on their allocated share.

The IRS has increased scrutiny of pass-through deduction claims, with accuracy-related penalties triggered at low thresholds. This means your documentation system must be bulletproof because the cost of an audit far exceeds the effort of maintaining proper records. You need monthly payroll records showing gross wages, payroll taxes, and W-2 withholdings broken down by employee and by month, because the IRS will examine whether your W-2 wages are reasonable and properly documented. A spreadsheet tracking QBI by month is insufficient; you need actual payroll tax returns, W-2 forms, and bank statements showing wage payments. For depreciation basis, maintain a detailed fixed-asset schedule showing the original cost, acquisition date, depreciation method, and accumulated depreciation for every asset you claim. This schedule must tie directly to your tax return, and you need supporting documentation like purchase invoices and receipts. If you claim a $500,000 equipment purchase in December, you need the invoice, proof of payment, and evidence that the equipment was placed in service before year-end. Many business owners maintain disorganized records and reconstruct their numbers at tax time, which immediately signals audit risk to the IRS. A real estate partnership that maintains monthly records showing rental income, repairs, depreciation, and W-2 wages can defend its deduction during examination, but one that provides a rough estimate and scattered documentation will face denial or reclassification. Your documentation system should tie directly to your accounting software, whether that’s QuickBooks or another platform, and you should run your deduction calculation quarterly to verify you remain on track. This discipline prevents year-end surprises and gives you time to adjust your strategy if you approach a threshold or face wage limitations. The investment in proper documentation and quarterly planning costs a few hundred dollars but saves thousands in potential audit exposure and missed deduction opportunities.

The pass-through deduction represents one of the most valuable tax benefits available to business owners, yet most fail to claim the full amount they’re entitled to. Your deduction depends on three critical factors: your income level, your business structure, and your documentation practices. Missing any one of these creates unnecessary tax liability that could have been avoided with proper planning.

A sole proprietor earning $191,000 operates under completely different rules than one earning $192,000, which is why you must know your exact income position by mid-year. If you operate as an SSTB professional, the restrictions tighten considerably, and your deduction disappears entirely above the threshold unless you meet specific wage or property requirements. Your business structure directly impacts your wage calculation, meaning two owners with identical income can claim vastly different deductions based on whether they operate as sole proprietors, S-corporations, or partnerships.

The strategies that actually move the needle involve timing decisions you make before December 31, not scrambling at tax time. Accelerating equipment purchases, deferring income, and adjusting your entity structure require advance planning and professional guidance. We at Clear View Business Solutions offer comprehensive tax planning and accounting services specifically designed for small business owners who want to maximize their pass-through deduction while staying audit-ready-contact us to discuss how we can help you claim the full deduction you’re entitled to.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2025 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.