Capital gains tax hits your wallet when you sell investments or property for a profit. Most people overpay because they don’t know the rules or timing strategies that could save them thousands.

At Clear View Business Solutions, we’ve helped clients reduce their tax burden by understanding when to sell, what to hold, and how to structure their portfolios smartly. This guide walks you through proven tactics you can use today and planning moves for tomorrow.

The IRS treats investment profits differently depending on how long you hold an asset before selling. Assets you own for one year or less generate short-term capital gains, taxed at your ordinary income rate, which can reach 37% federally according to IRS Topic No. 409. That means a $10,000 short-term gain costs you up to $3,700 in federal taxes alone.

The number 0% seems to be not appropriate for this chart. Please use a different chart type. Long-term capital gains, earned on assets held longer than one year, receive preferential treatment at 0%, 15%, or 20% depending on your income level. For married couples filing jointly in 2025, the 0% rate applies to gains up to $96,700 of taxable income, the 15% rate extends to $600,050, and gains above that face the 20% top rate. This distinction matters enormously. A $50,000 long-term gain taxed at 15% costs $7,500, while the same gain taxed as short-term ordinary income at 37% would cost $18,500-more than double. The federal government also imposes a 3.8% Net Investment Income Tax on certain investment income for high earners above $200,000 of modified adjusted gross income for single filers and $250,000 for married couples filing jointly, further increasing your effective tax rate if you cross those thresholds.

The date you sell determines your tax bill far more than the profit itself. If you sell an investment that has appreciated significantly, waiting just a few weeks or months to cross the one-year holding threshold can drop your tax rate from 37% down to 15% or even 0%. For real estate, the rules shift further in your favor. If you sell your primary residence and meet the ownership and use tests-living in the home for at least two of the past five years-you can exclude up to $500,000 of capital gains if married filing jointly, or $250,000 if single. That means a couple selling a home with a $400,000 profit pays zero federal capital gains tax.

The bracket you fall into when you realize gains is not fixed; it shifts based on other income you report that year. This creates a powerful planning opportunity. If you have a year with lower ordinary income, realizing capital gains in that year may keep you in the 0% or 15% bracket rather than pushing you into the 20% tier. Conversely, if you anticipate a high-income year from a bonus or business sale, deferring capital gains to a lower-income year can save substantially. The math is concrete: staying in the 15% bracket instead of moving to 20% on a $100,000 long-term gain saves $5,000.

Some asset classes break the standard rate structure. Collectibles and unrecaptured Section 1250 real estate gains face a flat 28% rate regardless of your income level, and qualified small business stock can also carry higher rates in certain circumstances. Understanding whether your specific assets qualify for preferential rates or face these higher thresholds requires knowing exactly what you own. The complexity here is why many investors miss significant tax savings-they treat all gains the same when the IRS does not. Your next move should focus on identifying which of your holdings qualify for long-term treatment and which strategies can shift your gains into lower brackets.

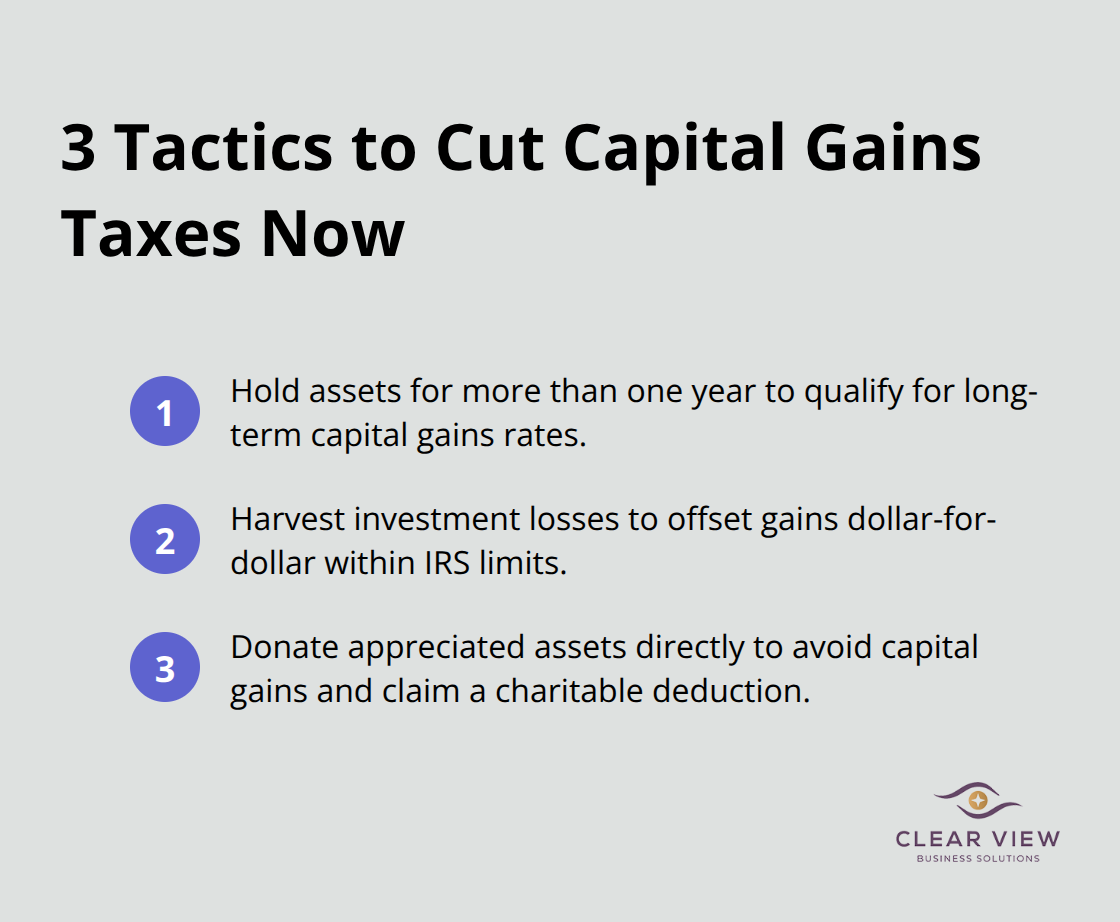

The gap between knowing about capital gains tax and actually reducing it comes down to execution. Clients leave thousands on the table each year by failing to act on straightforward moves available immediately. The first tactic is deceptively simple but requires discipline: hold investments past the one-year mark to shift your gains from the short-term rate down to long-term capital gains tax rates, depending on your income. That single decision on a $100,000 gain saves you between $22,000 and $37,000 in federal taxes. The math is so compelling that patience becomes a financial strategy.

If you own appreciated stock, real estate, or mutual funds currently below the one-year holding threshold, calculate exactly when you cross that line and mark the calendar. Many investors sell too early without realizing they are weeks away from a dramatic tax reduction. The holding period clock starts from the purchase date, not from when you decided to sell.

For those with concentrated positions in company stock or significant gains across a portfolio, even a 30-day delay can mean the difference between long-term and short-term treatment.

Tax-loss harvesting works by selling underperforming investments to generate losses that directly offset your capital gains. According to IRS guidance, you can deduct up to $3,000 of net losses against ordinary income each year, with unlimited losses carried forward to future years. This means if you have a $50,000 capital gain and a $50,000 loss available, you owe zero capital gains tax on that transaction.

The practical application matters: identify holdings in your portfolio that have declined in value, sell them to realize the loss, and use that loss to shelter gains from winners. One critical rule to watch is the tax-loss harvesting wash-sale rule 30 days IRS regulations. If you sell an investment at a loss, you cannot buy the same or substantially identical investment within 30 days before or after the sale, or the IRS will disallow your loss deduction.

The solution is straightforward: replace the sold position with a similar but not identical investment for at least 31 days, then swap back if desired. For example, if you sell a specific tech index fund at a loss, purchase a different tech fund for a month, then return to your original choice. This preserves the tax loss while maintaining your intended portfolio allocation.

The third tactic flips conventional thinking about charitable giving. Instead of selling an appreciated investment and donating the proceeds, donate the appreciated asset directly to a qualified charity. You receive a tax deduction equal to the full fair market value of the asset while avoiding the capital gains tax entirely. If you hold the asset for more than one year, the deduction is available without triggering any gain.

A concrete example illustrates the advantage: you own stock worth $50,000 with a $10,000 cost basis, meaning a $40,000 unrealized gain. Selling it first costs you $6,000 in capital gains tax at the 15% rate, leaving only $44,000 to donate. Donating the stock directly gives you a $50,000 charitable deduction while eliminating the $6,000 tax bill entirely.

Donor-advised funds simplify this strategy for ongoing giving. You contribute appreciated assets to a donor-advised fund, receive an immediate deduction for the full fair market value, and then distribute grants to charities over time. This vehicle works especially well if you want to bunch multiple years of charitable giving into a single year for tax purposes while spreading actual donations across several years. The IRS allows this flexibility, and it pairs perfectly with years when you have substantial capital gains to offset.

These three tactics work independently or together, but their effectiveness depends on your specific situation, income level, and investment timeline. The next section explores how to plan ahead strategically, timing your moves across multiple years to compound these benefits and position yourself for even greater tax savings.

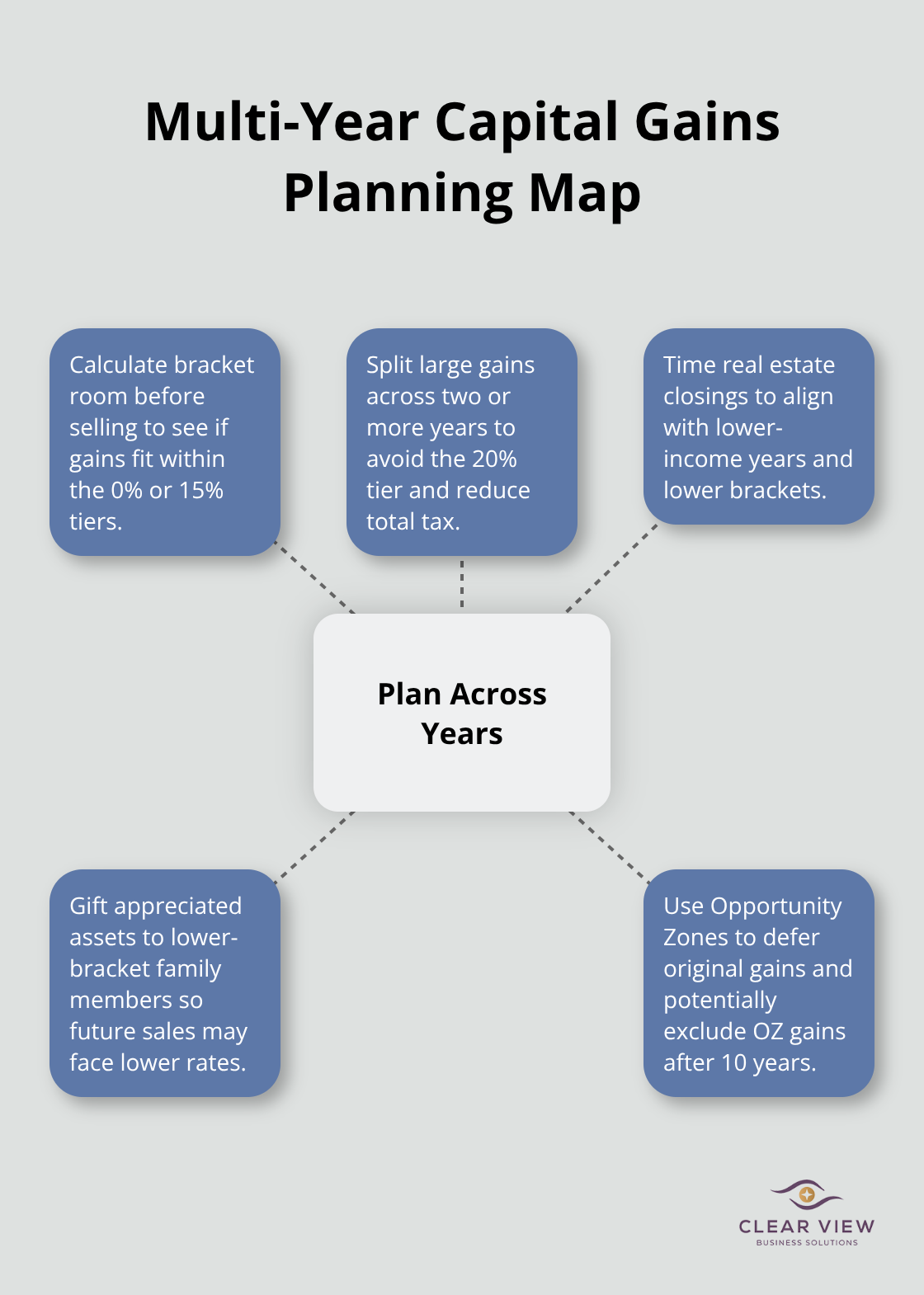

Strategic timing of capital gains realization across multiple tax years compounds the benefits of lower tax brackets far beyond what a single-year approach can achieve. Your annual income determines which capital gains tax bracket you occupy, and spreading gains across years with lower ordinary income keeps more of your profits in your pocket.

Calculate your expected taxable income for the current year and the next two years before you commit to a sale. For married couples filing jointly in 2025, the 0% long-term capital gains tax bracket applies only to gains up to $96,700 of taxable income. If your ordinary income already consumes $80,000 of that threshold, realizing a $50,000 gain this year means $30,000 faces the 15% rate instead of staying in the 0% bracket. Deferring that gain to a lower-income year keeps the entire $50,000 in the 0% zone, saving $7,500 in federal taxes.

The same logic applies to the boundary between 15% and 20% rates at $600,050 for married couples. A client with $580,000 in taxable income who realizes a $100,000 gain pays $20,000 at the top rate on the overage. Splitting that gain across two years, with $50,000 in each, keeps both portions in the 15% bracket, reducing the tax bill to $7,500 total. This two-year approach saves $12,500 on a single decision about timing.

Real estate sales offer the most obvious opportunity for this planning because you control when the closing occurs. If you own commercial property or investment real estate generating gains, coordinate the sale date with your income projections for that year. If you took a sabbatical, sold a business last year, or expect a major bonus this year, delay the real estate closing to a year with lower projected income. This simple shift in timing can move your entire transaction into a lower tax bracket.

Gifting appreciated assets to family members in lower tax brackets presents another dimension of multi-year tax planning, though the mechanics differ from what many assume. You cannot shift the capital gains tax burden to a recipient simply through a gift of appreciated stock or property. When the recipient sells, they owe tax based on their own cost basis, which remains your original purchase price. However, if you gift to a family member in a substantially lower tax bracket, they may face a lower tax rate on the gain when they eventually sell.

This works best with younger family members still building careers or retirees with minimal income. Gifting $100,000 of appreciated stock to an adult child with little income allows them to sell and realize the gain at the 0% long-term rate if their total taxable income stays below $96,700. The gift itself carries no income tax, and your child pays zero capital gains tax on the sale. This approach requires coordination with your tax professional to verify income levels and avoid unintended consequences, but it is a legitimate strategy for concentrated positions you want to diversify across family members anyway.

Opportunity Zones represent a specialized approach to capital gains deferral that applies if you have proceeds from a recent gain and want to invest in qualified economic development areas. Opportunity Zone investments allow you to defer capital gains by reinvesting the proceeds into qualified funds. If you hold the Opportunity Zone investment for at least ten years, the gain on that investment itself is excluded from taxation. This creates a powerful compounding effect: you defer the original gain while potentially eliminating all tax on the Opportunity Zone investment gains if held long enough.

In practice, Opportunity Zone strategies pair most effectively with real estate development in designated zones, which have expanded eligibility through 2027. Before pursuing this path, verify that the specific project and zone meet current IRS and Treasury criteria, as rules have shifted and will continue to change.

Capital gains tax reduction requires action, not just knowledge. The strategies outlined here work because they address the three levers you control: holding period, income timing, and asset placement. Short-term gains taxed at ordinary income rates destroy wealth unnecessarily when a few weeks of patience shifts your tax rate from 37% down to 15%, while tax-loss harvesting and charitable giving eliminate thousands in taxes through mechanics the IRS explicitly permits.

The gap between understanding these tactics and implementing them is where most people stumble. Tax law changes annually, your personal situation evolves, and the interaction between capital gains, ordinary income, and alternative minimum tax creates complexity that generic advice cannot address. A tax professional identifies opportunities specific to your holdings, income trajectory, and life circumstances that a general strategy misses entirely.

We at Clear View Business Solutions work with individuals and small business owners to build tax plans that reduce what you owe while keeping your portfolio aligned with your goals. Our team handles the mechanics of tax planning, from identifying which assets to sell first to structuring charitable giving vehicles that maximize deductions, and we represent you with the IRS when questions arise. Contact Clear View Business Solutions to discuss how these strategies apply to your specific situation and build a plan that works for your timeline and goals.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.