Most individual investors leave money on the table by not using tax-loss harvesting to offset their gains. The strategy is straightforward, but the rules around it-especially wash-sale restrictions-trip up many people.

We at Clear View Business Solutions help investors implement these tactics correctly so they actually reduce their tax bills. This guide walks you through the mechanics, the pitfalls to avoid, and the practical steps to get it right.

Tax-loss harvesting involves selling investments that have declined in value to lock in losses, then using those losses to offset capital gains realized elsewhere in your portfolio. You sell a losing position, realize the loss on paper, and immediately reinvest the proceeds into a similar investment to stay in the market. This approach doesn’t abandon your investment strategy-it times your sales to capture tax benefits while maintaining your desired asset allocation.

The IRS allows you to offset unlimited capital gains with capital losses. If your losses exceed your gains, you can deduct up to $3,000 of ordinary income in a single year, with any remaining losses rolling forward indefinitely to future tax years. A high-income investor realizing $50,000 in capital gains can harvest $30,000 in losses, meaning only $20,000 of gains face taxation and potentially saving thousands in federal taxes depending on your bracket.

The real value emerges when you treat tax-loss harvesting as an ongoing process rather than a year-end scramble. JPMorgan Asset Management research shows that accounts receiving regular cash contributions can sustain roughly 1% annualized tax savings over a decade, with contributions of around 20% of account value annually maintaining near-linear growth in tax benefits. Volatile markets create more harvesting opportunities since asset values swing more dramatically, giving you more chances to identify losing positions.

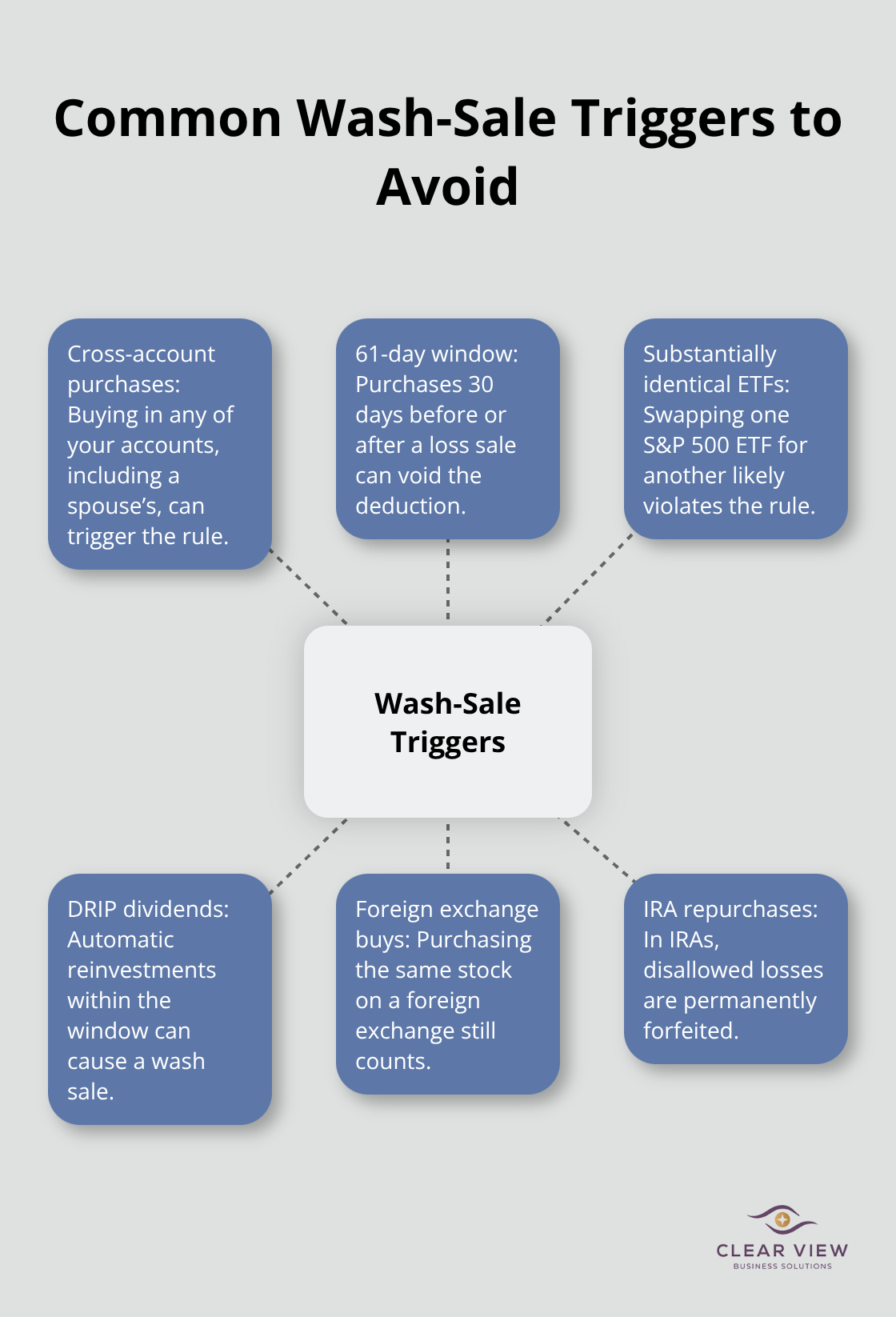

Tax-loss harvesting works best in taxable accounts-the strategy delivers zero benefit in IRAs, 401(k)s, or Roth IRAs because those accounts already shield gains from taxation. In Roth IRAs specifically, a particularly harsh penalty applies: if you sell a security at a loss in a taxable account and repurchase it in an IRA within the wash-sale window, the IRS disallows the loss entirely and you forfeit the deduction permanently. This cross-account rule catches many investors off guard, so you must track all your accounts together when implementing this strategy.

Understanding these mechanics sets the foundation, but the wash-sale rule represents the biggest obstacle most investors face when executing tax-loss harvesting correctly.

The wash-sale rule keeps investors from selling at a loss and buying the same or substantially identical security within a 61-day window. The rule applies across all your accounts simultaneously, including taxable accounts, IRAs, 401(k)s, and even your spouse’s accounts. This cross-account enforcement catches most investors off guard.

You can sell Apple stock at a $5,000 loss in your taxable brokerage account on December 20th, then accidentally trigger a wash sale on January 5th by purchasing Apple shares in your IRA. The IRS disallows the entire loss, and in an IRA specifically, you forfeit the deduction permanently-there’s no catch-up later.

The wash-sale window spans 61 days total: 30 days before the sale, the sale date itself, and 30 days after. If you sold a losing position on December 15th, you cannot repurchase the same or substantially identical investment until January 15th of the following year without triggering the rule.

The core problem lies in defining substantially identical investments. The IRS rule focuses on whether investments are substantially identical, not similar. Selling one S&P 500 ETF and buying a different S&P 500 ETF within the window likely violates the rule because both track the same index. However, selling an S&P 500 ETF and buying a Russell 1000 ETF creates meaningful separation-the Russell 1000 excludes smaller companies, so the holdings genuinely differ. Buying the same stock on a foreign exchange would also trigger the rule.

A practical substitution strategy works well: if you harvest a loss in a large-cap growth fund, replace it with a large-cap value fund tracking different companies. You maintain your growth exposure while avoiding wash-sale triggers. This approach preserves your asset allocation without sacrificing tax benefits.

Dividend reinvestments complicate matters further and trip up disciplined investors constantly. If you sold XYZ stock at a loss on November 15th and XYZ paid a dividend that automatically reinvested on December 10th through a DRIP program, you’ve repurchased XYZ within the window and triggered a wash sale-even though you didn’t actively buy anything.

When you harvest a loss, suspend automatic dividend reinvestment for 31 days minimum, or redirect dividends to cash. This simple step prevents accidental violations that would otherwise erase your tax benefit.

The disallowed loss doesn’t vanish entirely. It adds to the cost basis of your replacement security, deferring the tax benefit. If you sold 100 shares at a $2,000 loss and repurchased within 30 days, your new shares carry a higher cost basis by $2,000. This increases future taxes when you eventually sell those replacement shares, unless prices rise enough to create gains that absorb the higher basis.

Your holding period also transfers to the replacement security, which matters for long-term versus short-term capital gains treatment. This transfer can work in your favor if the original holding period qualifies for long-term rates.

Brokers track wash sales by CUSIP (Committee on Uniform Security Identification Procedures) within individual accounts, so your brokerage software should flag obvious violations. However, cross-account monitoring depends on you. If you hold accounts at multiple institutions, you must manually monitor the 30-day window across all of them. Spreadsheets work effectively-record the security sold, the sale date, the loss amount, and the 31-day reinvestment date. Set calendar reminders for each position.

The rule doesn’t pause for weekends or holidays; if the 30th day falls on a Saturday, your earliest repurchase date is Monday. December sales deserve special attention because the 30-day window extends into January, crossing tax years. A December 28th sale means you cannot repurchase until January 28th, making year-end tax planning urgent. Document your loss sales by mid-December to leave enough time for substitution purchases without rushing into a wash sale.

IRS Publication 550 covers wash-sale mechanics in detail, but the practical takeaway is this: harvest losses aggressively throughout the year, but treat the 61-day window as sacred. One mistake erases the tax benefit and complicates your cost basis for years. The complexity is why many investors benefit from professional guidance when managing multiple accounts or frequent trading. Once you master wash-sale avoidance, you can focus on the strategic side of tax-loss harvesting-identifying which positions to sell and when to maximize your after-tax returns.

Identifying which positions to sell requires a systematic approach, not gut feeling. Start with a comprehensive report of all holdings in your taxable accounts, sorted by unrealized gain or loss. Most brokerages provide this data directly in your portfolio dashboard. Focus on positions with losses exceeding $500, as smaller losses create administrative burden without meaningful tax savings. Calculate the tax value of each loss by multiplying the loss amount by your marginal federal tax rate. A $3,000 loss in the 24% bracket saves $720 in federal taxes, while the same loss in the 32% bracket saves $960. This calculation reveals which losses matter most.

Market volatility creates harvesting opportunities throughout the year. During market corrections, more positions slip underwater, giving you multiple candidates to choose from. JPMorgan Asset Management research found that accounts receiving regular cash contributions can generate roughly 1% annualized tax savings over a decade, but this requires harvesting losses consistently throughout the year rather than waiting for December. The worst time to harvest is during strong bull markets when few positions carry losses.

Implement harvesting as an ongoing discipline, checking your portfolio quarterly for new loss opportunities. When you identify a position to harvest, execute the sale immediately rather than hesitating, because losses can reverse quickly in volatile markets. Volatile markets reward speed-the longer you wait, the greater the chance that a losing position rebounds and eliminates your harvesting opportunity.

Reinvesting proceeds demands careful planning to avoid accidentally triggering a wash sale while staying invested. A wash sale occurs when you sell or trade securities at a loss and within 30 days before or after the sale you buy substantially identical securities. The moment you sell at a loss, simultaneously identify a replacement investment that tracks a different index or sector than the original position. If you sold a large-cap growth fund, replace it with a large-cap value fund or a total market fund with different holdings. If you sold a specific stock, consider an ETF tracking the same sector instead. Execute the replacement purchase on the same day as the loss sale to minimize tracking error and market-timing risk.

Create a spreadsheet documenting each harvested loss with five columns: security sold, sale date, loss amount, replacement security purchased, and the earliest date you can repurchase the original security without triggering a wash sale (31 days after the sale date). Set calendar alerts for that repurchase date so you can return to the original position if desired.

Never reinvest dividends from the original security during the 31-day window, and temporarily disable dividend reinvestment for replacement holdings purchased within 30 days of a loss sale.

Documentation becomes your shield against IRS scrutiny and internal confusion. Many investors maintain sloppy records, then cannot prove they avoided wash sales when audited. Maintain a master tax-loss harvesting log alongside your regular investment records, keeping detailed records of the sale and subsequent purchase, including the date, amount, and the specific ETFs involved. Your brokerage tracks wash sales by CUSIP within individual accounts, but cross-account wash sales depend entirely on your monitoring.

If you hold accounts at multiple institutions, manually track the 30-day window across all accounts because each broker only sees their own data. Print or screenshot your loss sales by mid-December and set specific reminders for January repurchase dates, because year-end timing creates the most complex wash-sale scenarios. This disciplined approach transforms tax-loss harvesting from a chaotic year-end scramble into a controlled, documented strategy that withstands scrutiny.

Tax-loss harvesting works only when you execute it correctly and maintain discipline across all your accounts. The mechanics are straightforward, but wash-sale violations and poor documentation destroy the tax benefits you worked to capture. Your success depends on three things: identifying losing positions systematically, reinvesting strategically to avoid wash sales, and tracking everything meticulously across multiple institutions.

Most individual investors benefit from professional guidance when implementing these strategies. Tax rules change, your personal situation evolves, and cross-account monitoring becomes complex as your portfolio grows. A tax professional reviews your specific circumstances, confirms you’re harvesting losses in the right accounts, and ensures your documentation withstands IRS scrutiny.

If you’re ready to stop leaving money on the table, contact us to discuss how tax-loss harvesting fits into your broader financial plan. We’ll review your current situation, identify specific opportunities, and build a strategy that works for your goals.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.