Most people avoid financial planning because they think it’s too complicated. The truth is that a comprehensive financial planning strategy doesn’t require a finance degree-it requires a clear process.

At Clear View Business Solutions, we’ve helped countless clients build plans that actually work. This guide walks you through each step, from understanding where you stand today to making decisions that align with your real life.

You cannot build a financial plan without knowing exactly where you stand. This means calculating your net worth, understanding your cash flow, and facing your debt situation head-on. Most people skip this step because it feels uncomfortable, especially if debt is high or savings are low. That’s a mistake. The uncomfortable truth is always better than the comfortable fiction, because only the truth lets you make real decisions.

Start by calculating your net worth. List everything you own: bank accounts, investment accounts, real estate value, vehicles, and any valuable personal property. Then subtract everything you owe: mortgage balance, car loans, credit card debt, student loans, and any other liabilities. Your personal number tells you whether you’re ahead or behind, and more importantly, it gives you a baseline to measure progress against.

Calculate this quarterly, not annually, because quarterly reviews force accountability and catch problems early.

Your income and expenses tell the real story of your financial health. Track your income and expenses for at least one month, but ideally three months to account for seasonal variations. Many people discover that discretionary spending like subscriptions, dining out, and impulse purchases adds up to a significant portion of their take-home pay.

The difference between your income and expenses is the money available for debt payoff, savings, and investments, and this number matters more than your total income. Separate your expenses into fixed costs like housing and insurance versus variable costs like groceries and entertainment. This distinction shows you where you have flexibility to cut back if needed.

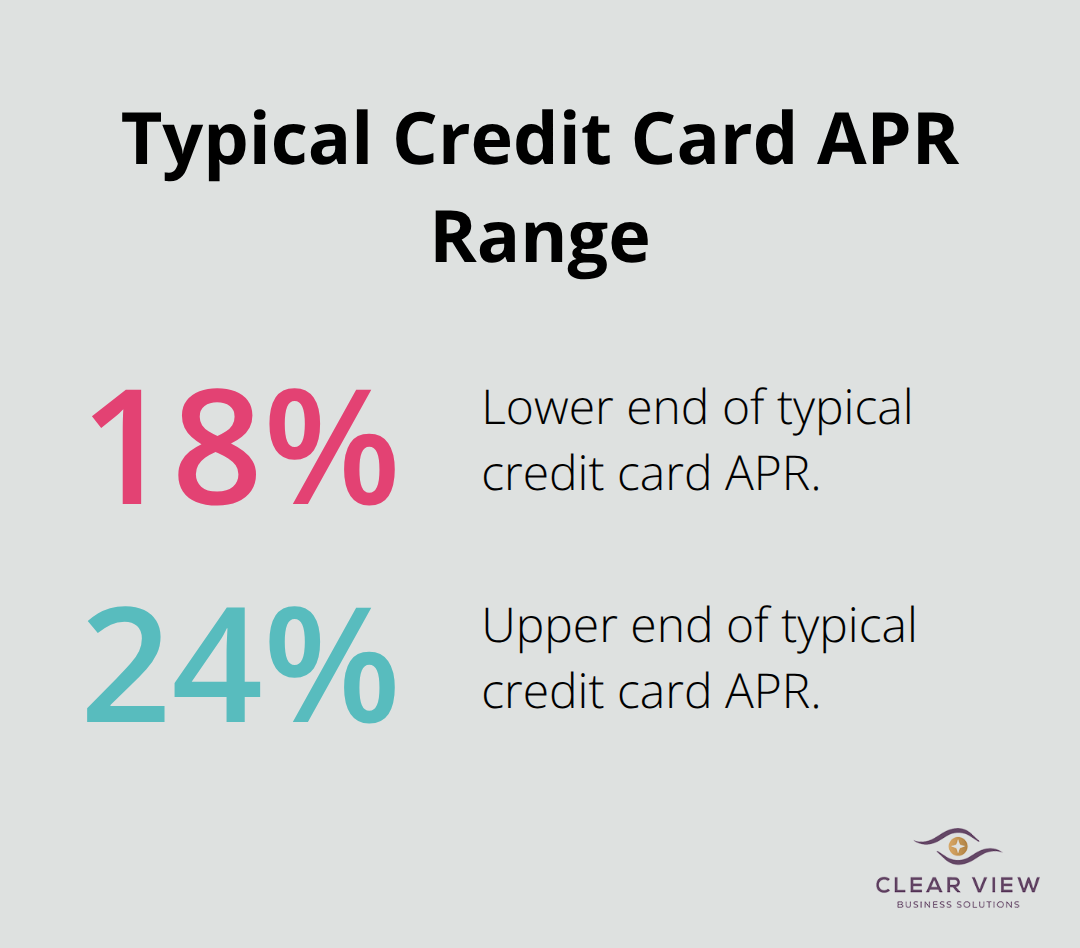

Your debt situation requires brutal honesty. List every debt with the balance, interest rate, and minimum payment. High-interest debt like credit cards typically charges 18-24% annually, which means a $5,000 balance costs you $900-$1,200 per year just in interest.

Mortgage debt is different because real estate typically appreciates, and mortgage rates are currently lower than historical averages. Prioritize paying down high-interest debt aggressively while maintaining minimum payments on lower-rate debt. This assessment takes a few hours but saves you from years of financial mistakes. Once you understand your complete financial picture, you’re ready to move forward with setting goals that actually reflect your situation.

Now that you understand your complete financial picture, you need to define what you’re actually working toward. Most people fail at financial planning because they set vague goals like “earn more money” or “save for retirement” without attaching specific dollar amounts and timelines. This vagueness kills momentum because you never know if you’re winning or losing. Instead, write down three to five concrete financial goals with exact numbers and dates. A real goal sounds like “pay off $15,000 in credit card debt within 18 months” or “accumulate $50,000 for a home down payment by 2028,” not just “pay off debt” or “save for a house.” Research from the Journal of Financial Planning shows that advisors who work with clients using this specificity method see significantly better plan adherence and client outcomes than those using general goal-setting approaches.

Your short-term goals typically span one to three years and address immediate financial pressure, like eliminating high-interest debt or building an emergency fund. Your long-term goals span five to ten years or beyond and include retirement savings, real estate investment, or education funding. The critical move is ranking these goals by priority because competing goals force trade-offs. If you want to pay down debt aggressively and invest for retirement simultaneously, you’re spreading resources thin and accomplishing neither quickly.

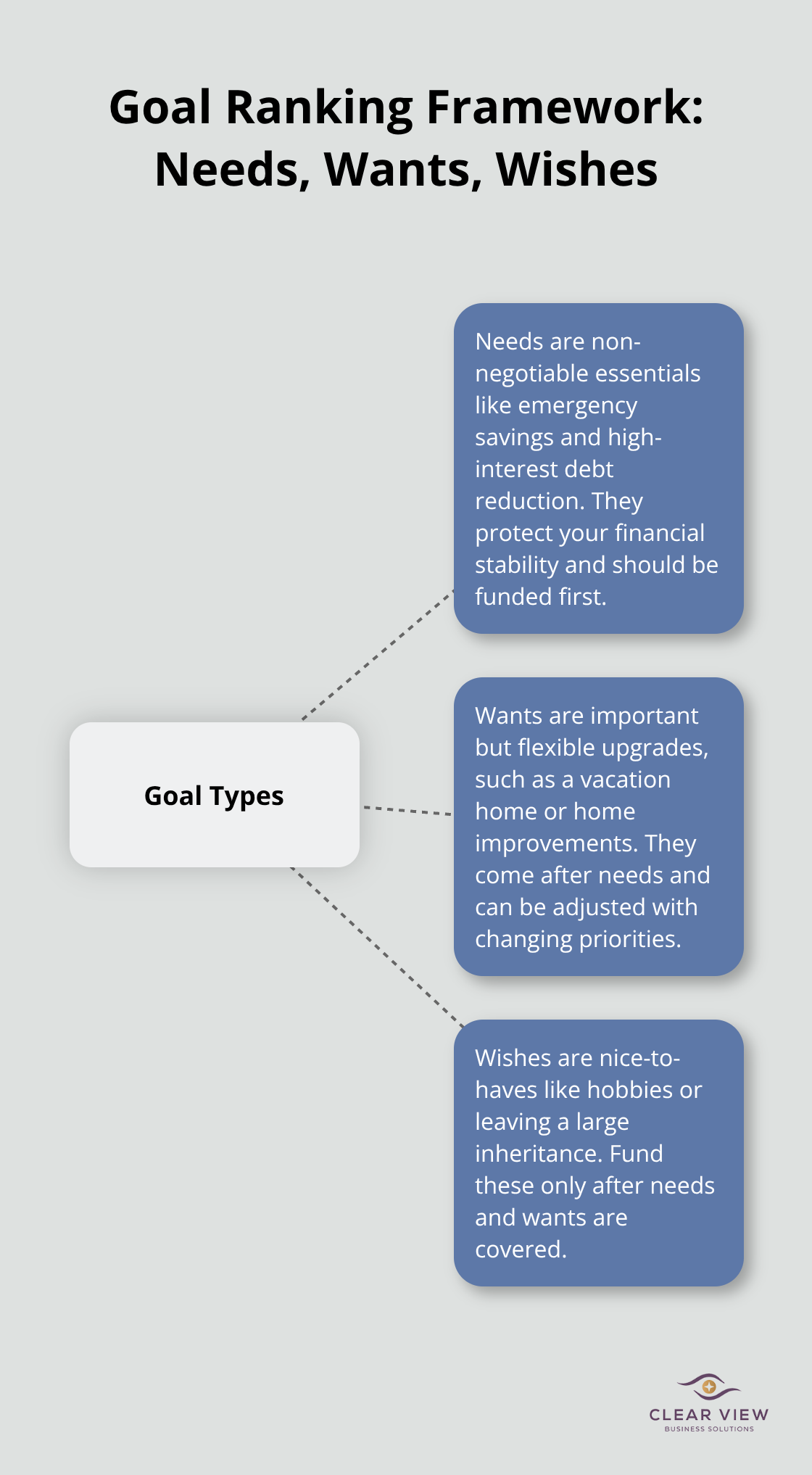

Rank goals as needs, wants, and wishes. Needs are non-negotiable (like building emergency savings or paying down credit card debt above 20% interest). Wants are important but flexible (like saving for a vacation home or upgrading your primary residence). Wishes are nice-to-haves like funding a hobby or leaving a large inheritance.

This framework prevents you from chasing every goal at once.

Your goals must also align with how you actually want to live, not how you think you should live. If you hate budgeting down to the penny, a rigid spending plan will fail no matter how logical it looks on paper. If you value experiences and travel, forcing yourself to save 40% of income for a house down payment will create resentment and trigger abandonment of the entire plan. Instead, build a financial strategy that accounts for your real priorities. If travel matters, budget for it explicitly rather than trying to eliminate it. If you prefer simple systems over complex optimization, choose straightforward investment options over tax-optimized but complicated strategies.

The difference between your income and your essential expenses is the discretionary capital available for debt payoff, savings, and investments. Allocate this capital across your ranked goals based on your values. Someone with young children might prioritize life insurance and education savings. Someone nearing retirement might prioritize debt elimination and healthcare cost planning. Someone starting a business might prioritize building operating capital and emergency reserves. None of these is wrong because financial planning is personal, not universal. Once your goals are specific, ranked, and aligned with your actual life, you’re ready to build concrete action steps that move you toward those goals systematically.

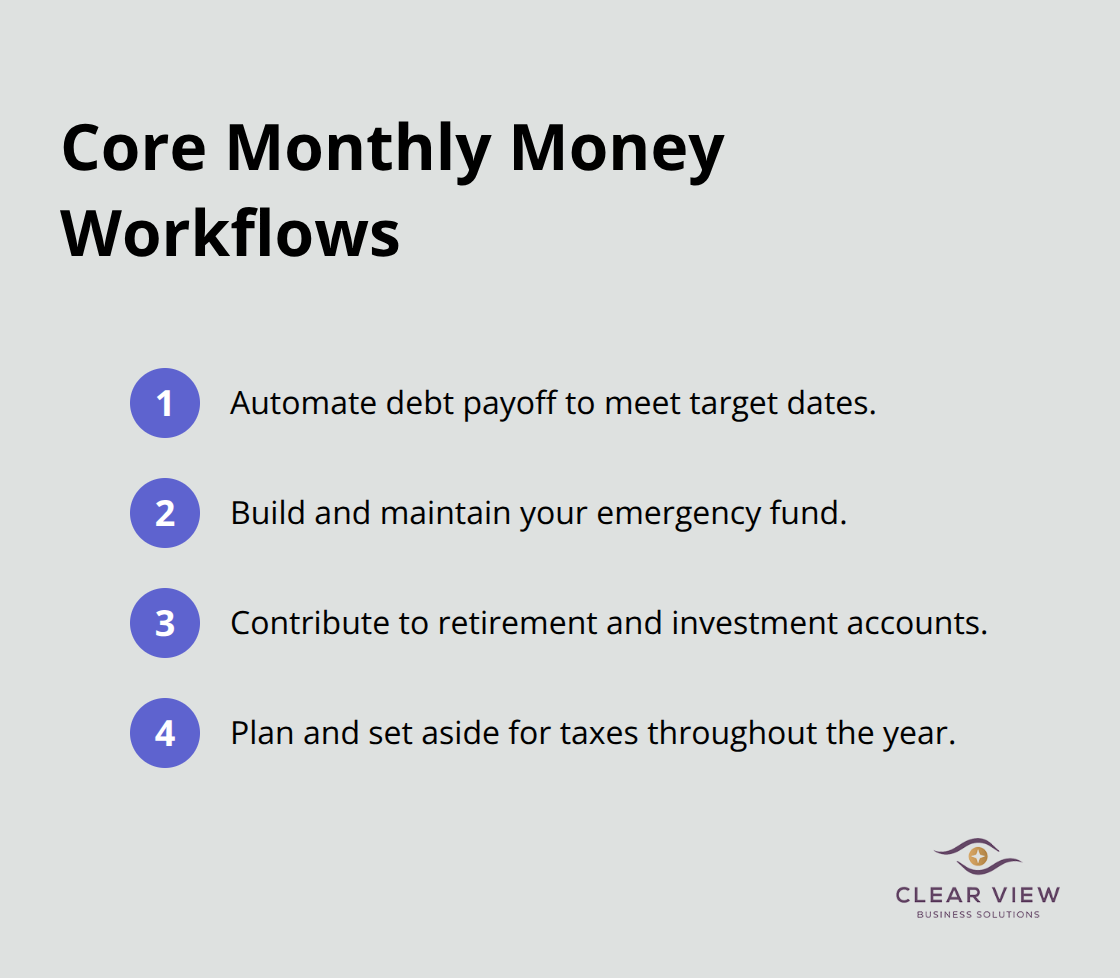

Your financial goals mean nothing without concrete actions that move you toward them each month. The difference between people who build wealth and those who remain stuck is not intelligence or income-it’s a disciplined system for translating goals into weekly and monthly habits. Start by separating your financial plan into distinct workflows: debt payoff, emergency fund building, investment contributions, and tax planning. Assign a specific dollar amount and timeline to each workflow based on your ranked goals and available discretionary capital. If you ranked paying off $15,000 in credit card debt as your top priority, calculate exactly how much you need to allocate monthly to hit that 18-month target, then automate that payment.

If retirement savings ranks second, determine your contribution to employer-sponsored plans or IRAs based on remaining discretionary capital. Advisors who implement a workflow-based approach see higher plan adherence than those using generic budgeting templates. Set up automatic transfers on the same day your paycheck arrives so money flows to each goal before you see it in your checking account. This removes willpower from the equation and treats your financial goals with the same priority as your mortgage payment.

Most budgets fail because they’re built on theoretical spending patterns rather than your actual behavior. We recommend tracking your real spending for three months, then building your budget backward from that data. If you consistently spend $400 monthly on dining out despite planning for $150, your budget is lying to you. Instead, acknowledge the $400 reality and decide whether to accept it, actively reduce it, or adjust other categories to compensate. Separate fixed costs like insurance and housing payments from variable costs like groceries and entertainment. Fixed costs typically account for 50-60% of take-home income for most households, which means your flexibility exists almost entirely in variable spending. Create specific spending caps for variable categories and track them weekly, not monthly, because weekly accountability catches overspending before it becomes a $1,000 problem. Use a simple spreadsheet or app like YNAB or EveryDollar to record spending as it happens rather than reconciling at month-end when the damage is done. The key insight is that budgeting works only when it accounts for your actual preferences and behavior, not some idealized version of yourself.

Once you’ve allocated funds to debt payoff and emergency savings, the remaining surplus must flow into investments aligned with your timeline and risk tolerance. If you’re saving for retirement more than ten years away, stock-based investments historically return 10% annually versus 4-5% for bonds, according to historical market analysis. If you’re saving for a goal within five years, bonds and money market funds protect your capital from market volatility even if returns are lower. The critical mistake most people make is investing without understanding their actual risk tolerance, then panicking and selling during market downturns. Instead, take 20 minutes to complete a risk tolerance questionnaire before investing anything. Determine your asset allocation based on that assessment and your timeline, then automate monthly contributions to maintain discipline. If your employer offers matching contributions to a 401(k), contribute enough to capture the full match-that’s an immediate 50-100% return on your money. Max out tax-advantaged accounts like IRAs and 401(k)s before investing in taxable accounts because the tax savings compound significantly over decades. The average household that maximizes employer 401(k) matching and contributes the annual IRA limit accumulates roughly 40% more retirement wealth than households that don’t, based on decades of retirement savings data.

Tax planning cannot wait until April when you’re filing returns-it must happen continuously throughout the year. If you’re self-employed or have significant investment income, make quarterly estimated tax payments to avoid penalties and interest charges. Review your W-4 withholding annually because underwithholding creates a surprise tax bill while overwithholding is an interest-free loan to the government. Consider tax-loss harvesting in taxable investment accounts, which means selling losing positions to offset capital gains and reduce taxable income. Maximize contributions to tax-deferred accounts like traditional IRAs and 401(k)s before year-end because these contributions reduce your taxable income dollar-for-dollar. For retirement planning specifically, stop relying on the outdated 80% income replacement rule and instead plan to cover 100% of your pre-retirement income minus what you’ll no longer spend, such as work-related expenses and retirement savings contributions. If you earn $100,000 and spend $80,000 after accounting for taxes and savings, you need to replace $80,000 in retirement, not $80,000 of gross income. Healthcare costs in retirement typically run 15-20% higher than pre-retirement years according to Fidelity research, so explicitly budget for increased medical expenses. Calculate your projected Social Security benefits at ssa.gov and assume you’ll receive them at age 70 rather than earlier, which maximizes your monthly payment. The combination of maximized Social Security, tax-efficient withdrawals from retirement accounts, and a disciplined spending plan creates retirement income that actually sustains your lifestyle rather than forcing cutbacks.

Your comprehensive financial planning strategy requires quarterly reviews to compare actual spending against your budget, track progress toward goals, and identify where you’re winning or falling behind. Major life events like marriage, children, job changes, or inheritance shift your priorities and available resources, so your plan must adapt immediately when these situations occur. A plan built for a single person without dependents looks completely different from a plan for a family with young children, and a strategy that made sense at age 35 needs significant adjustments by age 55 when retirement moves from distant future to near reality.

Most people cannot build and maintain a comprehensive financial planning strategy alone because your situation is unique, your goals are personal, and the tax implications of your decisions matter more than you probably realize. The complexity of coordinating debt payoff, retirement savings, tax optimization, and insurance protection creates blind spots that cost thousands of dollars over time. We at Clear View Business Solutions work with individuals and small business owners to build financial strategies that actually work in the real world, whether you need help with tax planning, retirement strategy, or understanding how your business finances connect to your personal wealth.

Your financial plan is the roadmap to the life you actually want to live, so treat it seriously and adjust it as your circumstances change. That discipline compounds into real wealth over time, and professional guidance prevents costly mistakes that derail your progress. Start your comprehensive financial planning journey today and take control of your financial future.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.