Small business owners often leave thousands of dollars on the table each year simply because they don’t have a structured approach to managing their taxes. The difference between a business that pays more tax than necessary and one that doesn’t comes down to one thing: intentional planning.

At Clear View Business Solutions, we’ve seen firsthand how tax planning strategies for small businesses can transform a company’s financial health. When you take control of your tax situation now, you protect your profits and build a stronger foundation for growth.

Most small business owners think about taxes once a year, usually in March or April when the deadline looms. This reactive approach costs them significantly. Businesses with structured tax planning strategies can reduce their effective tax rate compared to those without planning. That’s not a minor adjustment-for a business generating $300,000 in profit, this difference means keeping additional capital annually. The math is straightforward: intentional tax planning isn’t optional if you want to maximize what stays in your business.

Cash flow determines whether your business survives or thrives. When you pay taxes without planning, you often overpay throughout the year, which means less money available for payroll, inventory, equipment, or emergencies. Section 179 expensing allows you to deduct qualifying asset purchases placed in service by year-end. This isn’t theoretical-if you purchase equipment or machinery strategically before year-end, you can eliminate taxable income entirely and preserve cash that would otherwise go to the IRS. Many small business owners miss this opportunity because they don’t plan ahead.

Quarterly estimated tax payments, when calculated correctly, prevent the shock of a massive tax bill in April. The safe harbor rules require you to pay 90 percent of your current-year tax or 100 percent of your prior-year tax, whichever is smaller. Missing these payments triggers penalties and interest that compound your problem.

The number 100% seems to be not appropriate for this chart. Please use a different chart type.

Competitors who plan taxes strategically have more capital for growth, better cash flow for unexpected challenges, and the ability to reinvest profits faster. If your competitor uses bonus depreciation at 100 percent for assets placed in service after January 19, 2025, they expense equipment immediately while you depreciate it over years. They also capture the Work Opportunity Tax Credit more often, which provides up to $9,600 per qualified employee hired, directly reducing their tax liability.

Retirement plan contributions offer another competitive lever. A Solo 401(k) allows contributions up to $76,500 in 2025 with catch-up provisions, meaning you reduce taxable income substantially while building retirement security. Businesses without this structure pay taxes on every dollar of profit. The difference compounds year after year, giving tax-planning businesses financial flexibility that others simply don’t have.

The businesses that win financially don’t leave tax decisions to chance. They coordinate with professionals who understand their industry, structure their entity correctly, and time major purchases and income strategically. This approach transforms tax planning from a compliance burden into a profit-protection tool. The next section outlines the specific strategies that produce these results.

The IRS allows you to deduct virtually every legitimate business expense, from office supplies to professional fees to advertising costs. Home office deductions work if you use part of your home exclusively for business-you can deduct a portion of mortgage interest, property taxes, utilities, and maintenance. Documentation matters here. The IRS scrutinizes these claims, so keep receipts, invoices, and records for everything.

Section 179 expensing lets you deduct the cost of certain property as an expense when the property is first placed in service, with a $3,130,000 phase-out threshold. If you purchase equipment or machinery before year-end, you eliminate taxable income dollar-for-dollar rather than spreading the deduction over years. Bonus depreciation at 100 percent for assets placed in service after January 19, 2025, means equipment expenses become immediate write-offs.

Employee-related costs also count: salaries, benefits, payroll taxes, training, and professional development all reduce taxable payroll. The Work Opportunity Tax Credit provides up to $9,600 per qualified employee you hire, directly cutting your tax liability without requiring additional deductions.

Your business structure determines whether you pay taxes once or twice and affects how much you ultimately owe. An S-Corporation becomes advantageous around $60,000 in profit because it allows you to split income between reasonable salary and distributions, with only the salary portion subject to self-employment taxes. A C-Corporation makes sense if you plan reinvestment exceeding $500,000 annually, since the 21 percent federal corporate rate often beats individual rates when profits stay in the business.

An LLC offers flexibility-you choose whether to be taxed as a pass-through entity or corporation. The right structure depends on your profit level, growth plans, and reinvestment strategy. Getting this decision wrong costs thousands annually, so coordinate with a tax professional before establishing your entity.

Retirement plans represent the fastest way to reduce taxable income while securing your future. A Solo 401(k) allows total contributions to a participant’s account up to $69,000, not counting catch-up contributions for those age 50 and over. A SEP-IRA lets you contribute up to 25 percent of compensation or $69,000, whichever is lower. For businesses with employees, a SIMPLE IRA costs less to administer. Defined benefit and cash balance plans can exceed $300,000 in annual contributions for higher-income business owners.

Contributions must be made by your tax-return due date, including extensions. Establish the plan before year-end to claim the deduction, and coordinate contributions with your accountant to avoid missing deadlines or contribution limits that shrink your tax savings. The timing of these decisions determines whether you capture the full benefit or lose thousands in potential deductions.

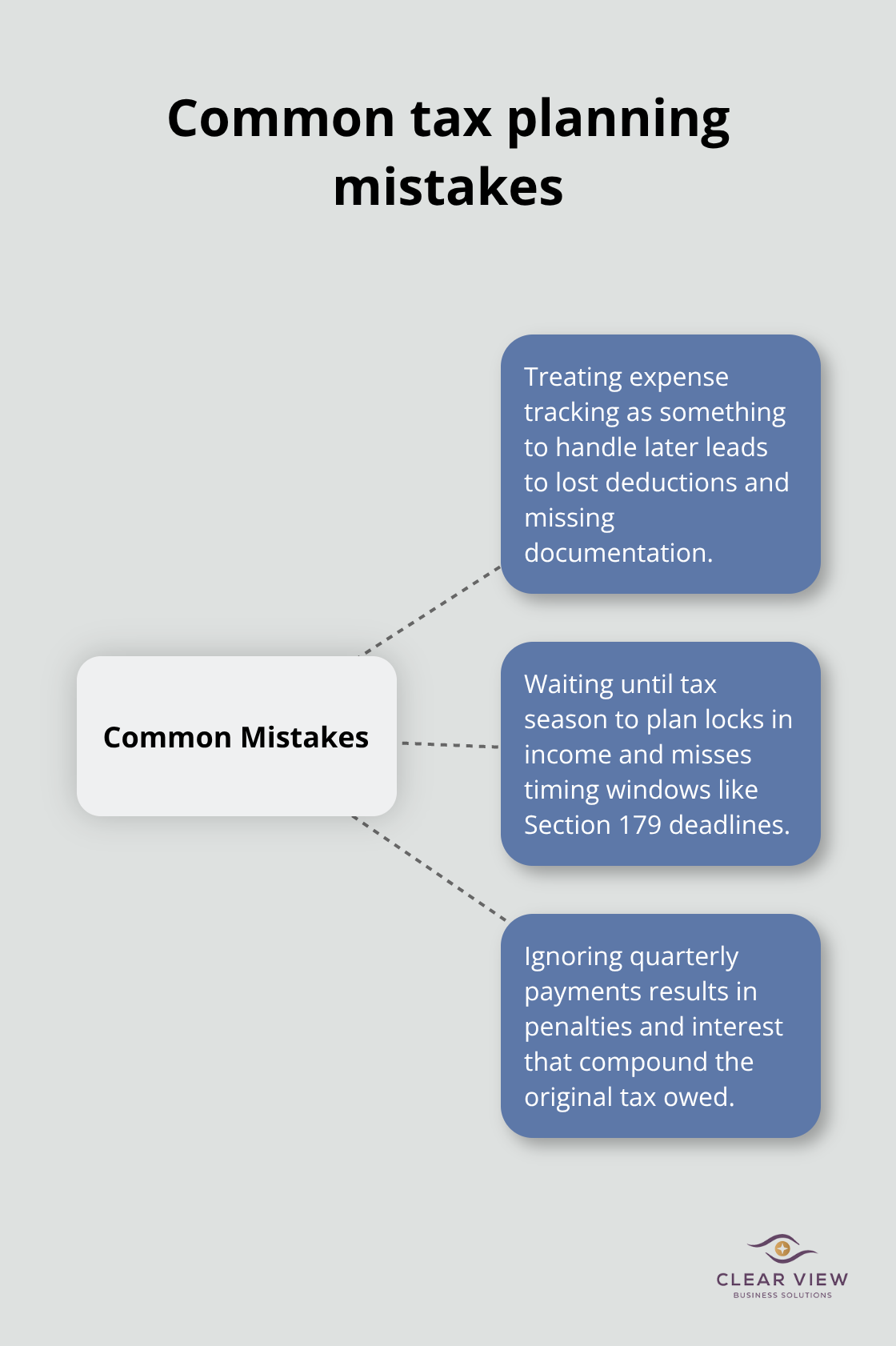

Most small business owners sabotage their own tax savings through preventable mistakes that compound year after year. The first mistake is treating expense tracking as something to handle later. When you wait until tax season to dig through bank statements and credit card receipts, you’ve already lost money. Expenses fade from memory, receipts disappear, and you miss deductions entirely because you cannot document them. The IRS requires meticulous records for every business expense-receipts, invoices, and documentation prove your claims hold up under scrutiny.

Real-world impact: businesses that track expenses throughout the year capture more deductions than those scrambling in April. If you generate $300,000 in annual revenue, poor tracking could cost you $5,000 to $10,000 in missed deductions. The solution requires discipline, not complexity. Use accounting software like QuickBooks to log expenses weekly, photograph receipts immediately, and categorize spending by type. Set a calendar reminder for the 15th of each month to review your records. This takes 30 minutes and prevents the chaos of year-end reconstruction.

The second critical mistake is waiting until tax season to plan. Tax planning in March or April is damage control, not strategy. Once tax season arrives, your income is locked in, asset purchases have passed, and retirement plan contribution windows have closed. The IRS established Section 179 expensing with a December 31 deadline specifically because timing matters-you must place assets in service before year-end to capture the deduction.

Quarterly estimated tax payments follow the same principle. To figure your estimated tax, you must calculate your expected adjusted gross income, taxable income, taxes, deductions, and credits for the year. Early planning prevents penalties and interest that multiply your tax burden.

The third mistake flows directly from the second: small business owners ignore quarterly payments entirely. Many assume they will handle taxes when they file, then discover they owe penalties on top of the tax bill itself. These penalties compound because they apply to both the unpaid tax and any interest accrued.

The solution is straightforward-coordinate with a tax professional in January to establish your quarterly payment schedule based on projected income. Then automate those payments through your bank. You avoid penalties, maintain cash flow predictability, and prevent April surprises. Businesses that implement quarterly planning consistently report better cash management and lower overall tax liability because they control timing rather than react to it.

Tax planning strategies for small businesses work because they shift you from reactive to intentional. You’ve seen throughout this article how the difference between paying more tax than necessary and keeping more profit comes down to structured decisions made throughout the year, not scrambling in April. Deductions eliminate taxable income, the right business structure cuts your overall tax burden, and retirement plans reduce what you owe while securing your future.

The businesses that win financially protect their bottom line through professional guidance. When you coordinate with someone who understands your industry and your goals, tax planning transforms from a compliance headache into a profit-protection strategy. You capture deductions you would otherwise miss, time major purchases strategically, and avoid penalties that compound your problems (the cost of professional guidance pays for itself many times over through deductions and credits you wouldn’t find alone).

Start tracking expenses this week using accounting software, establish your quarterly payment schedule in January, and coordinate with a tax professional before year-end to identify opportunities specific to your business. We at Clear View Business Solutions help small business owners in Tucson implement tax planning that actually works. Contact Clear View Business Solutions to discuss how we can help you keep more of what you earn and build financial stability for growth.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2025 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.