W2 employees often believe they have limited options for reducing their tax burden. This misconception costs thousands of workers significant money each year.

We at Clear View Business Solutions have identified multiple tax saving strategies for W2 employees that can substantially lower your annual tax bill. The IRS provides numerous deductions and savings opportunities specifically designed for traditional employees.

The Tax Cuts and Jobs Act of 2017 eliminated most traditional W2 employee deductions, but three significant opportunities remain that can save you thousands annually. Most tax professionals overlook these strategies or explain them poorly, which leaves employees to miss substantial savings.

W2 employees cannot claim home office deductions under current tax law, despite widespread confusion about this rule. The IRS eliminated this deduction for traditional employees in 2018, even if you work remotely full-time or maintain a dedicated workspace.

Only self-employed individuals and business owners can claim home office expenses. Your employer can reimburse home office costs tax-free, so negotiate this benefit during salary discussions or performance reviews.

The American Opportunity Tax Credit provides up to $2,500 per student for qualified education expenses, with $1,000 refundable even if you owe no taxes. The Lifetime Learning Credit offers up to $2,000 for professional development courses, certifications, and continuing education.

Student loan interest deduction allows up to $2,500 annually for interest payments. Income limits apply at $85,000 for single filers and $175,000 for married couples who file jointly (according to IRS guidelines).

HSAs provide the strongest tax benefits available to W2 employees. Contributions reduce current taxable income, funds grow tax-free, and withdrawals for qualified medical expenses remain tax-free.

The 2024 contribution limits reach $4,150 for individual coverage and $8,300 for family coverage, with an additional $1,000 catch-up contribution for those 55 and older. Unlike FSAs, HSA funds roll over indefinitely and become a retirement account after age 65.

These deductions form just one part of your tax strategy. Retirement account optimization offers even greater potential for long-term tax savings.

The 2024 401k contribution limit of $23,000 represents the single most powerful tax reduction tool for W2 employees, potentially saving high earners over $8,000 annually in federal taxes alone. Workers who maximize their 401k contributions while capturing full employer matching essentially receive guaranteed returns of 50% to 100% on their initial investment through company match programs.

Traditional 401k contributions reduce your current taxable income dollar-for-dollar, which makes them superior to Roth options for workers in the 22% tax bracket or higher. A software engineer who earns $120,000 and contributes the maximum $23,000 to a traditional 401k drops their taxable income to $97,000, which saves approximately $5,060 in federal taxes.

The IRS data shows that 87% of high-income W2 employees benefit more from traditional contributions than Roth alternatives due to lower retirement tax rates. Most financial advisors recommend traditional 401k contributions for anyone who expects to retire in a lower tax bracket than their current rate.

Workers aged 50 and older can contribute an additional $7,500 annually to their 401k, which brings total contributions to $30,500 for 2024. This catch-up provision allows late-career employees to save an extra $1,650 to $2,775 in annual federal taxes (depending on their bracket).

The IRS permits catch-up contributions to IRAs as well, with an extra $1,000 allowed for those 50 and older. Income limits may restrict high earners from deducting traditional IRA contributions, but the backdoor Roth strategy provides an alternative path for retirement savings.

Traditional IRA deductions phase out completely for single filers who earn more than $87,000 and married couples who earn more than $143,000 when covered by workplace retirement plans. High earners lose this $7,000 annual deduction opportunity, which forces them to explore alternative tax strategies beyond basic retirement accounts.

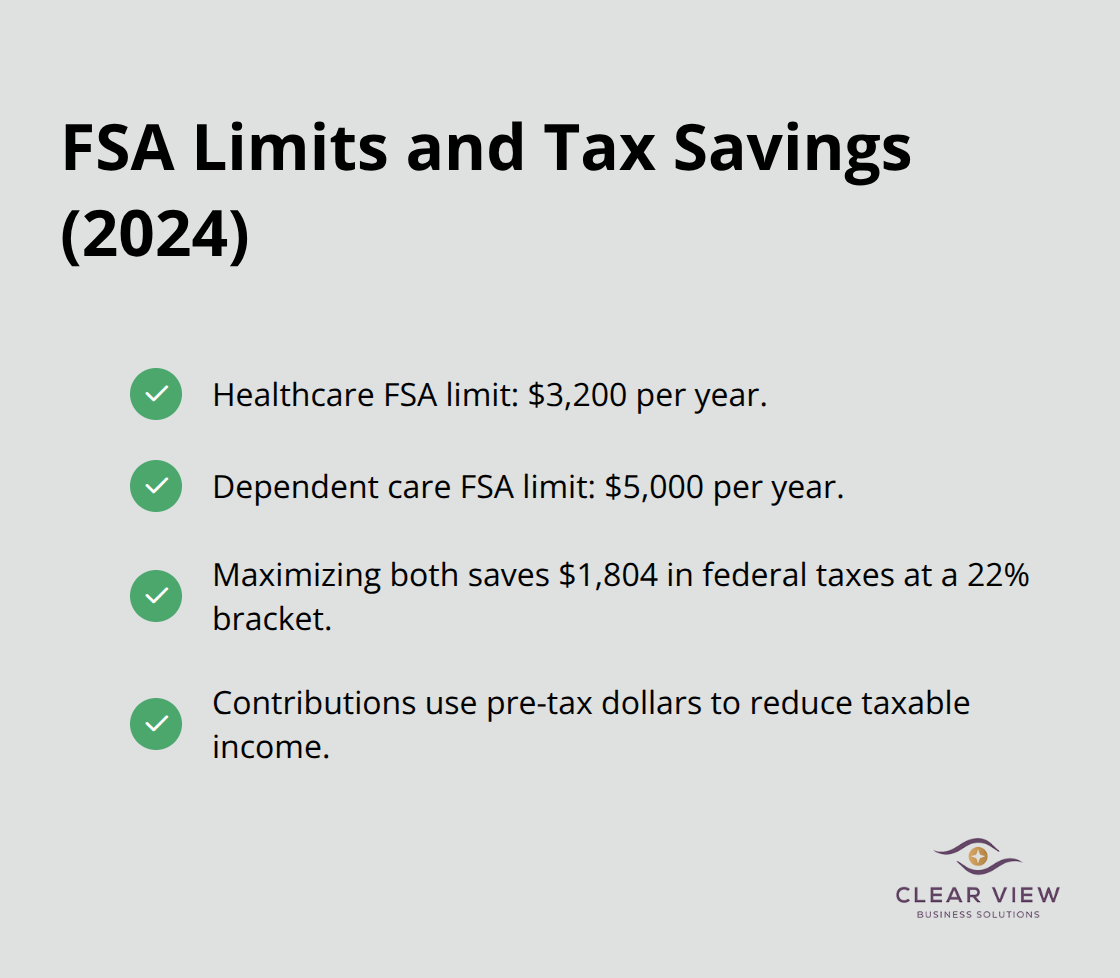

Flexible Spending Accounts deliver immediate tax savings that most W2 employees ignore completely. The IRS allows up to $3,200 annually for healthcare FSAs and $5,000 for dependent care FSAs. Both accounts use pre-tax dollars that reduce your taxable income directly. A worker in the 22% tax bracket who maximizes both FSAs saves $1,804 in federal taxes plus additional state tax savings.

Healthcare FSAs cover prescription drugs, dental work, vision care, and over-the-counter medications with proper documentation. Dependent care FSAs pay for daycare, summer camps, and after-school programs for children under 13. This makes them particularly valuable for parents who face high childcare costs.

Tax-loss harvesting allows investors to offset capital gains with investment losses. This strategy reduces taxable income by up to $3,000 annually beyond gains offset. The IRS wash-sale rule prohibits repurchasing identical securities within 30 days, but investors can buy similar assets to maintain market exposure while they claim the loss.

Robo-advisors like Betterment and Wealthfront automate this process. These platforms typically generate 0.77% additional annual returns through systematic tax-loss harvesting (according to their published data). High earners benefit most from this strategy since they face higher capital gains rates and can offset ordinary income up to the annual limit.

Charitable contributions require itemized deductions to provide tax benefits. This limits their value for taxpayers who claim the standard deduction of $14,600 for singles or $29,200 for married couples in 2024. Bunching charitable donations into alternating years maximizes tax benefits. This approach pushes total itemized deductions above standard deduction thresholds.

Donors who give appreciated securities directly to charities avoid capital gains taxes while they receive full fair market value deductions. This strategy works particularly well for long-term investors with substantial gains. The IRS requires written acknowledgment for donations over $250 and detailed records for all charitable deductions to withstand potential audits.

The most effective tax saving strategies for W2 employees focus on retirement contributions and pre-tax benefits. You can save $8,000 to $12,000 annually in federal taxes when you contribute the full $23,000 to your 401k and capture employer matches. HSAs provide triple tax advantages that beat other savings vehicles, while FSAs reduce taxable income through healthcare and dependent care expenses.

Tax-loss harvesting creates additional savings for investors, and strategic charitable donations benefit those who itemize deductions. Professional tax planning becomes essential as your income grows and situations become more complex (especially for high earners who face unique challenges). Experienced advisors help identify opportunities you might miss and prevent costly mistakes.

Start with a review of your current 401k contributions and employer benefits. Calculate potential HSA savings if you have a high-deductible health plan. We at Clear View Business Solutions help clients optimize their tax positions through comprehensive financial advisory services.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2933 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.