Most people leave money on the table when it comes to taxes. Whether you’re self-employed, run a small business, or work a traditional job, there are concrete tax reduction strategies you’re probably not using.

At Clear View Business Solutions, we’ve helped countless clients cut their tax bills by thousands of dollars simply by being intentional about their approach. This guide walks you through the specific moves that work.

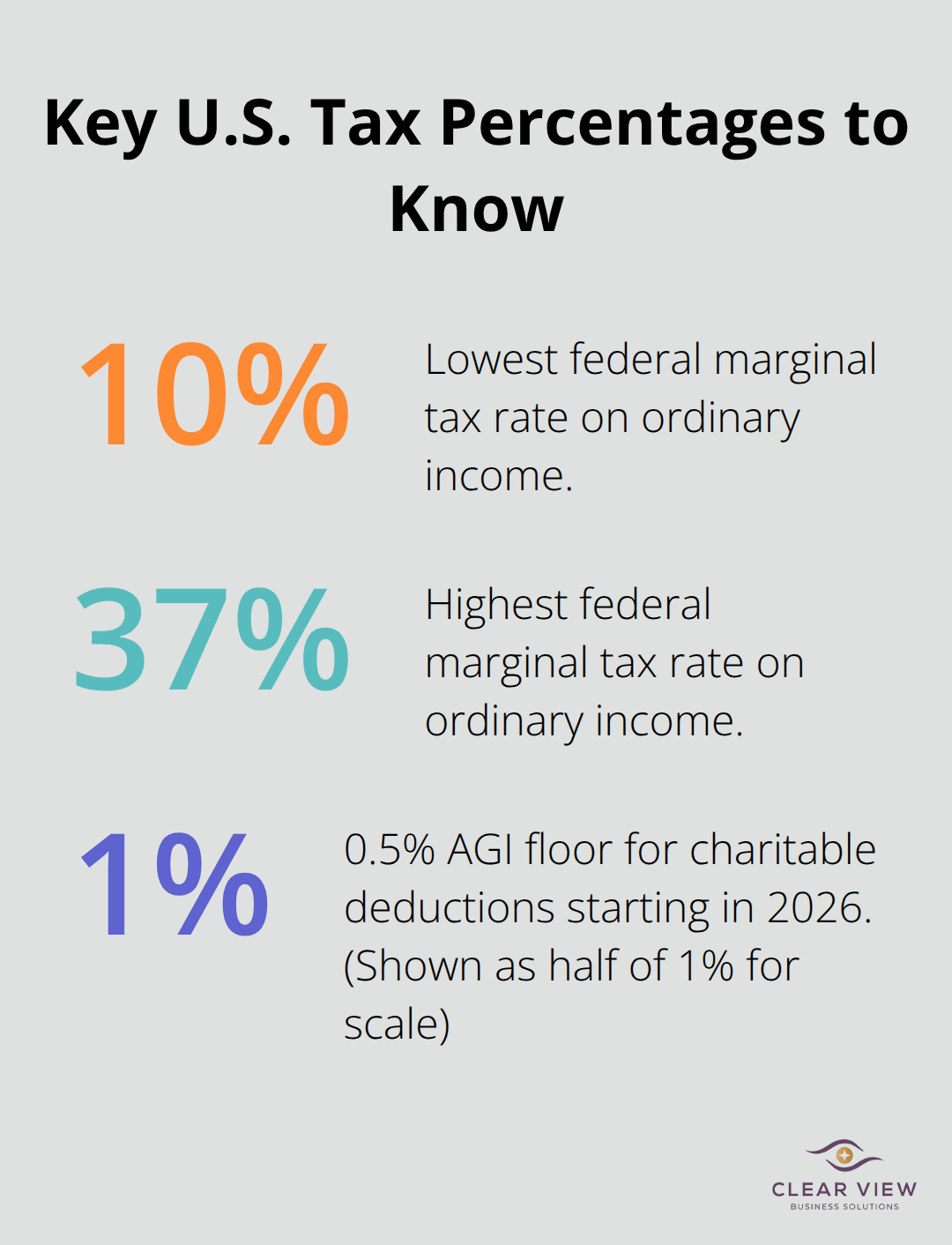

Your tax bracket determines how much of every additional dollar you earn goes to the IRS, yet most people guess at this number rather than calculate it precisely. The standard deduction sits at $16,100 for single filers and $32,200 for married couples filing jointly, meaning any income below these thresholds faces zero federal tax. Income above the standard deduction gets taxed at your marginal rate, which ranges from 10% at the lowest end to 37% at the highest.

Many people optimize for their current bracket without realizing where they’ll land after a bonus, side income, or investment gains push them into the next tier. Start by listing every income source: W-2 wages, self-employment income, rental income, investment dividends, and capital gains. Then calculate your total income and subtract the standard deduction to find your actual taxable income.

This single exercise reveals your marginal rate and shows exactly how much each additional dollar costs you in taxes. If you’re a single filer earning $70,000 in wages plus $15,000 from a side business, your total income is $85,000. Subtract $16,100 and you’re in the 22% bracket, meaning the last dollar you earn gets taxed at 22%. This matters because it changes how you should approach deductions and income timing.

Most people take the standard deduction and call it a day, but itemized deductions often deliver better results, especially if you own a home, donate to charity, or pay significant state and local taxes. The 2026 standard deduction increased, which sounds good until you realize that the SALT deduction cap of $40,000 now makes itemizing more attractive for higher earners.

If you donated $8,000 to charity last year and paid $12,000 in state income taxes, you’ve got $20,000 in itemized deductions already. Add mortgage interest and property taxes, and you could easily surpass $32,200. But starting in 2026, charitable deductions face a 0.5% AGI floor, meaning you only deduct the portion of donations exceeding 0.5% of your adjusted gross income.

This makes bunching donations into a single year far more effective than spreading them out. If you earn $100,000 and want to donate $5,000 annually, that’s $20,000 total across four years with most of it disallowed. Instead, donate $20,000 in one year and skip giving for three years, and you’ll actually capture the full deduction.

For business owners, the deductions are even more substantial. Home office space, vehicle mileage, office supplies, software subscriptions, professional development, and meals with clients all reduce taxable income if properly documented. The IRS allows a simplified home office deduction of $5 per square foot, up to 300 square feet, or you can deduct actual expenses.

Most owners leave thousands on the table by not tracking these business expenses systematically. The difference between haphazard record-keeping and organized documentation often amounts to thousands in lost deductions. Once you understand your tax bracket and identify what you can deduct, the next step involves taking action on strategies that actively reduce what you owe.

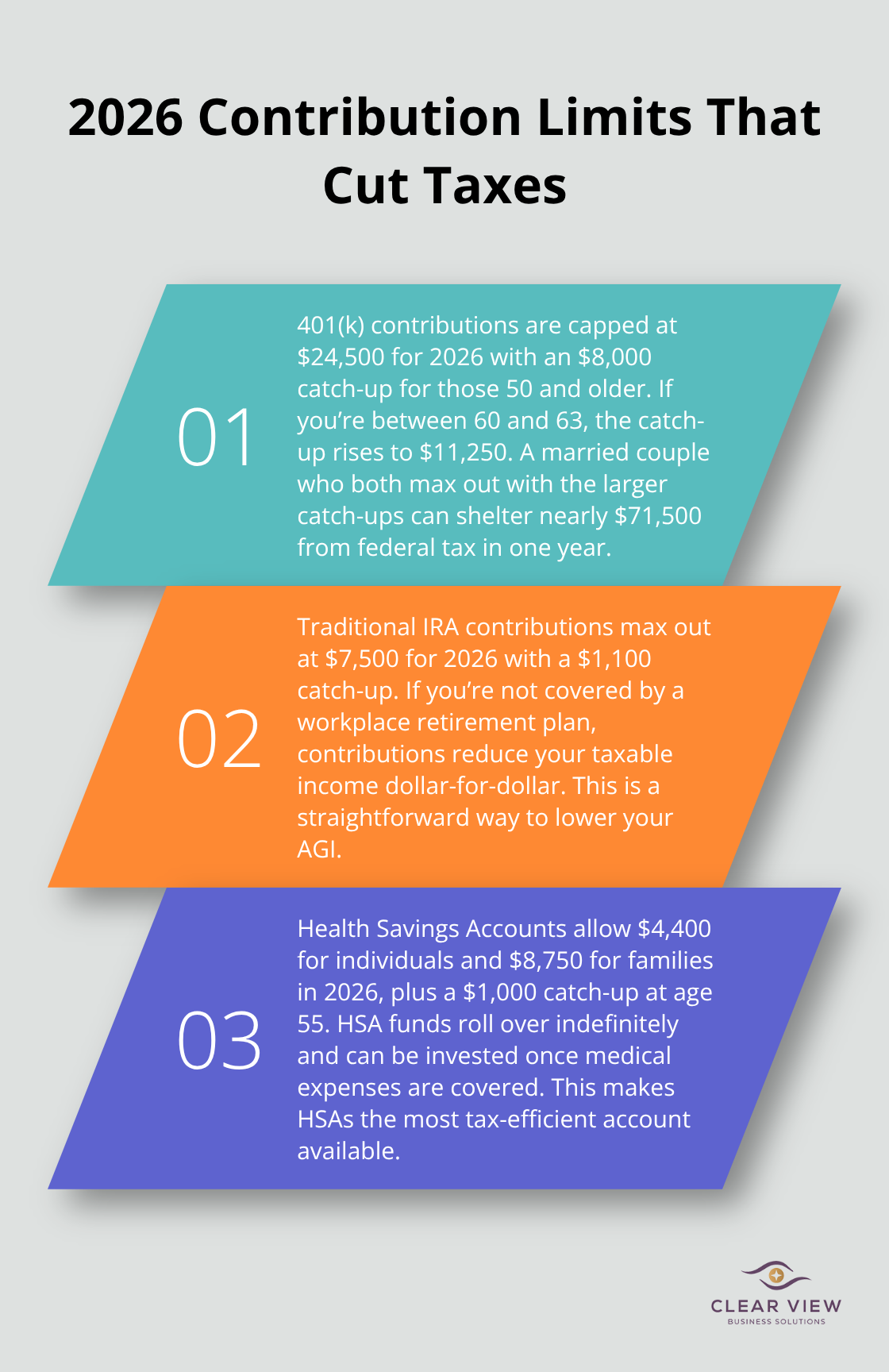

Retirement contributions and tax-advantaged accounts form the backbone of serious tax reduction, yet most people contribute far less than allowed. For 2026, the 401(k) contribution limit sits at $24,500, with an additional $8,000 catch-up contribution for those over 50. If you’re between 60 and 63, you get an even larger catch-up of $11,250 instead of the standard $8,000. A married couple where both earn enough to max out both 401(k)s and both qualify for the age 60-63 catch-up can shelter nearly $71,500 from federal taxation in a single year.

Traditional IRA contributions max out at $7,500 for 2026 with a $1,100 catch-up, and these reduce your taxable income dollar-for-dollar if you’re not covered by a workplace retirement plan. Health Savings Accounts offer $4,400 for individual coverage and $8,750 for family coverage in 2026, plus a $1,000 catch-up at age 55. The critical insight most people miss is that HSA funds roll over indefinitely and can be invested like a brokerage account once medical expenses are covered, making them the most tax-efficient account available.

For business owners specifically, a Solo 401(k) allows contributions up to $69,000 in 2026 when you account for both employee deferrals and employer contributions, dwarfing what W-2 employees can shelter.

Timing income and expenses matters far more than people realize, especially for self-employed individuals and business owners who control when invoices get paid and when expenses get incurred. If you’re on track to earn $95,000 this year and you know a $20,000 project will finish in December, consider deferring that invoice to January to spread income across two tax years and potentially stay in a lower bracket. Conversely, if you’re already solidly in the 24% bracket and a major expense is coming, accelerate it into the current year rather than paying it in January.

Property improvements, vehicle purchases, and professional development can all be timed strategically. One specific tactic that works well: if you’re self-employed and expecting a strong year, make estimated quarterly tax payments that are slightly higher than required, then adjust your final payment downward when you file. This prevents a massive tax bill in April and avoids underpayment penalties while keeping more cash in your business longer.

For those with investment portfolios, tax-loss harvesting offsets capital gains directly and up to $3,000 of ordinary income annually, with unlimited carryforward of excess losses. The wash-sale rule blocks you from repurchasing substantially identical securities within 30 days, so harvest losses in December and wait until January to rebuild positions, or sell a losing fund and immediately buy a similar but different fund in the same category.

This isn’t theoretical-executing one well-timed harvest can save $600 to $1,200 in taxes depending on your bracket, and the losses persist for years if unused. The strategy works because you capture the tax benefit while maintaining your desired asset allocation through alternative investments. These moves reduce what you owe today, but advanced planning strategies address the bigger picture of your overall financial structure and long-term tax exposure.

Tax-loss harvesting delivers real money back, but most investors abandon the strategy too early or execute it incorrectly. The wash-sale rule blocks repurchasing substantially identical securities within 30 days, yet this constraint creates opportunity rather than limitation. Sell a losing position in early December, wait until January 2nd to rebuild with a similar but different fund in the same asset class, and you lock in the loss while maintaining your portfolio allocation. A $50,000 position that dropped to $45,000 generates a $5,000 loss that offsets $5,000 in capital gains or reduces ordinary income by up to $3,000 in the current year, with the remaining $2,000 carrying forward indefinitely. If you’re in the 24% federal bracket, that $3,000 ordinary income deduction saves $720 immediately. The IRS allows unlimited carryforward of unused losses, meaning a harsh market year can shield you from taxes for years afterward. What matters most is documenting the harvest carefully and avoiding the wash-sale trap, which disallows the deduction if you repurchase the same security too soon. Many investors fail to execute this because they fear being out of the market, but the 30-day window is short enough that missing a few percentage points matters far less than the tax savings.

Your business structure determines whether you pay taxes once or twice, whether you can deduct losses, and how much self-employment tax you owe. As a sole proprietor, you pay 15.3% self-employment tax on most of your net business income, while an S-corporation election lets you split income into W-2 wages and distributions, paying self-employment tax only on the W-2 portion. For someone earning $100,000 net profit, an S-corp election can save $2,000 to $4,000 annually depending on how you allocate income. The tradeoff involves additional accounting and payroll processing, which typically costs $1,500 to $2,500 annually, so the strategy makes sense only if your net self-employment income exceeds $60,000. Most business owners should work with a tax professional to model whether S-corp status makes financial sense in their specific situation, since the calculation depends on your income level, state taxes, and business structure.

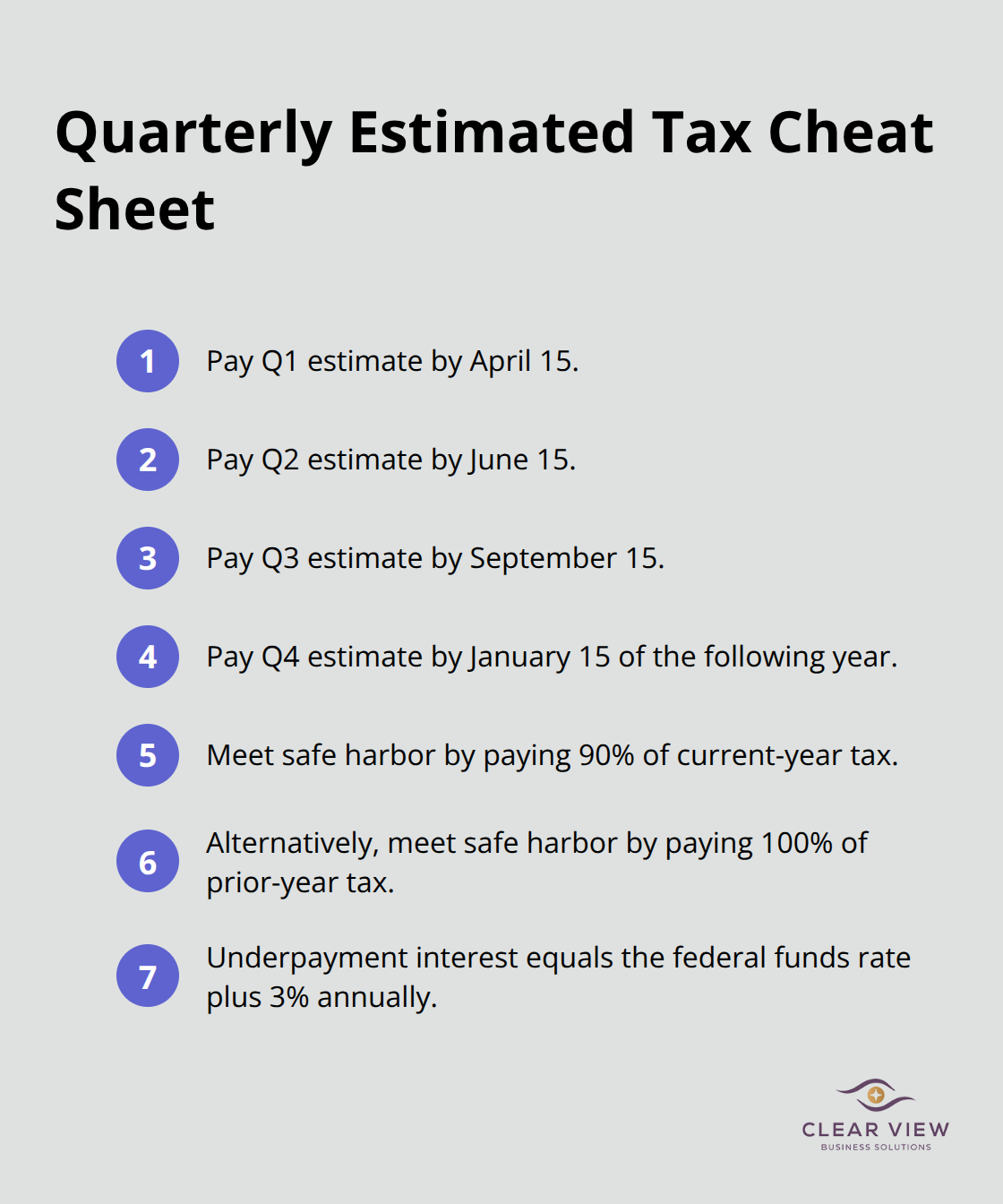

Quarterly estimated tax payments prevent penalties and underpayment interest, which the IRS charges at the federal funds rate plus 3% annually. If you owe $10,000 in taxes and pay nothing until April, you’ll owe roughly $300 in penalty and interest on top of the tax itself. The safer approach divides your expected annual tax liability by four and pays that amount on April 15th, June 15th, September 15th, and January 15th of the following year. Underestimating is acceptable if your payment reaches 90% of current-year tax or 100% of prior-year tax, whichever is smaller.

The tax reduction strategies outlined in this guide work because they align with how the tax code actually functions, not against it. Proactive tax planning compounds over time-a business owner who saves $3,000 annually through strategic S-corp structuring and consistent expense tracking accumulates $30,000 in savings over a decade, while an investor who harvests losses systematically shields themselves from taxes during strong market years. Every dollar you overpay in taxes is a dollar that could have stayed in your business, funded your retirement, or strengthened your financial position.

Start by calculating your precise tax bracket and listing every deduction you might be missing. Then prioritize the moves that deliver the biggest impact for your situation-most people see immediate results from maximizing retirement contributions and controlling income timing, while business owners should evaluate S-corp status and ensure systematic expense tracking. Investors should implement tax-loss harvesting before year-end to capture available losses.

We at Clear View Business Solutions help individuals and small business owners implement these tax reduction strategies with personalized tax planning and accounting services. Contact Clear View Business Solutions to discuss your specific situation and build a tax plan that actually works.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2025 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.