Most Americans overpay their taxes by $1,040 annually according to the National Association of Tax Professionals. Strategic tax planning throughout the year can dramatically reduce your tax burden.

We at Clear View Business Solutions see businesses and individuals miss thousands in potential savings by waiting until tax season. The right approach involves year-round strategies that maximize deductions and optimize your financial position.

Tax preparation happens once a year when you file your return, but tax planning operates continuously throughout the year to minimize your tax burden. The IRS reports that taxpayers who engage in year-round tax planning save an average of $2,847 annually compared to those who only focus on tax preparation.

Tax preparation is reactive – you work with what already happened. Tax planning is proactive – you make strategic decisions before they impact your taxes. This fundamental difference separates successful tax strategies from missed opportunities.

High earners in the 32% and 37% tax brackets benefit most from maxed-out 401k contributions, with contribution limits reaching $76,500 for 2024 when including catch-up contributions. These taxpayers should focus on income deferral strategies and maximize pre-tax retirement accounts.

Middle-income earners in the 22% bracket should prioritize Roth IRA conversions during lower-income years and strategic timing of capital gains. The sweet spot allows for tax diversification without pushing them into higher brackets.

Lower-income taxpayers focus on maximizing the Earned Income Tax Credit, which provides up to $632 for taxpayers with no qualifying children. The key difference lies in timing – high earners defer income while lower earners often accelerate it.

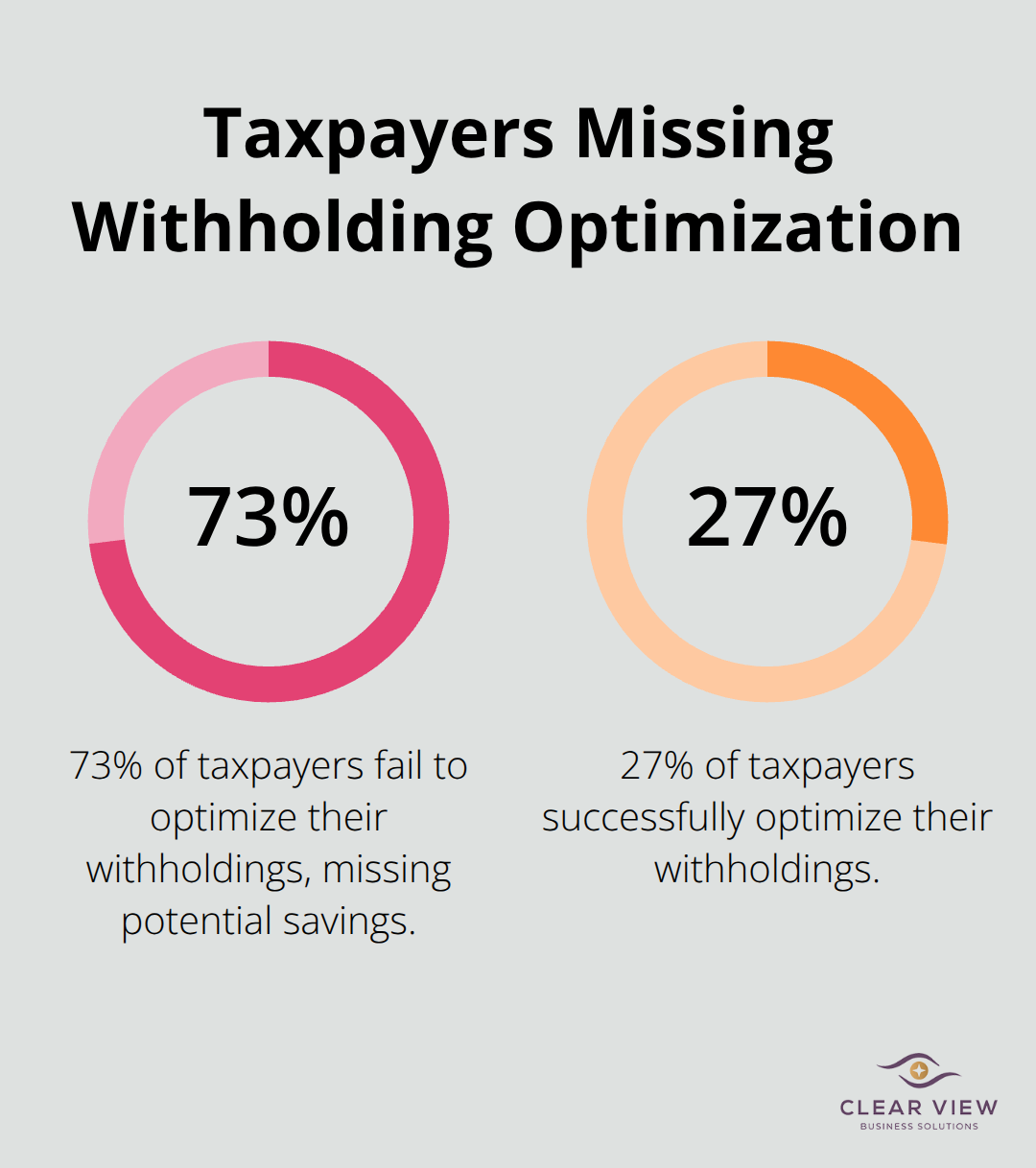

The most expensive mistake involves missing the December 31 deadline for retirement contributions and tax-loss harvesting. The IRS data shows 73% of taxpayers fail to optimize their withholdings, resulting in interest-free loans to the government through large refunds.

Another critical error involves neglected quarterly estimated payments, which triggers underpayment penalties at 8% interest rates. Small business owners frequently mix personal and business expenses, losing valuable deductions worth thousands annually.

These mistakes compound over time, costing the average taxpayer $15,000 over a decade (according to the Tax Foundation). The next step involves implementing specific strategies that maximize your savings potential throughout the year.

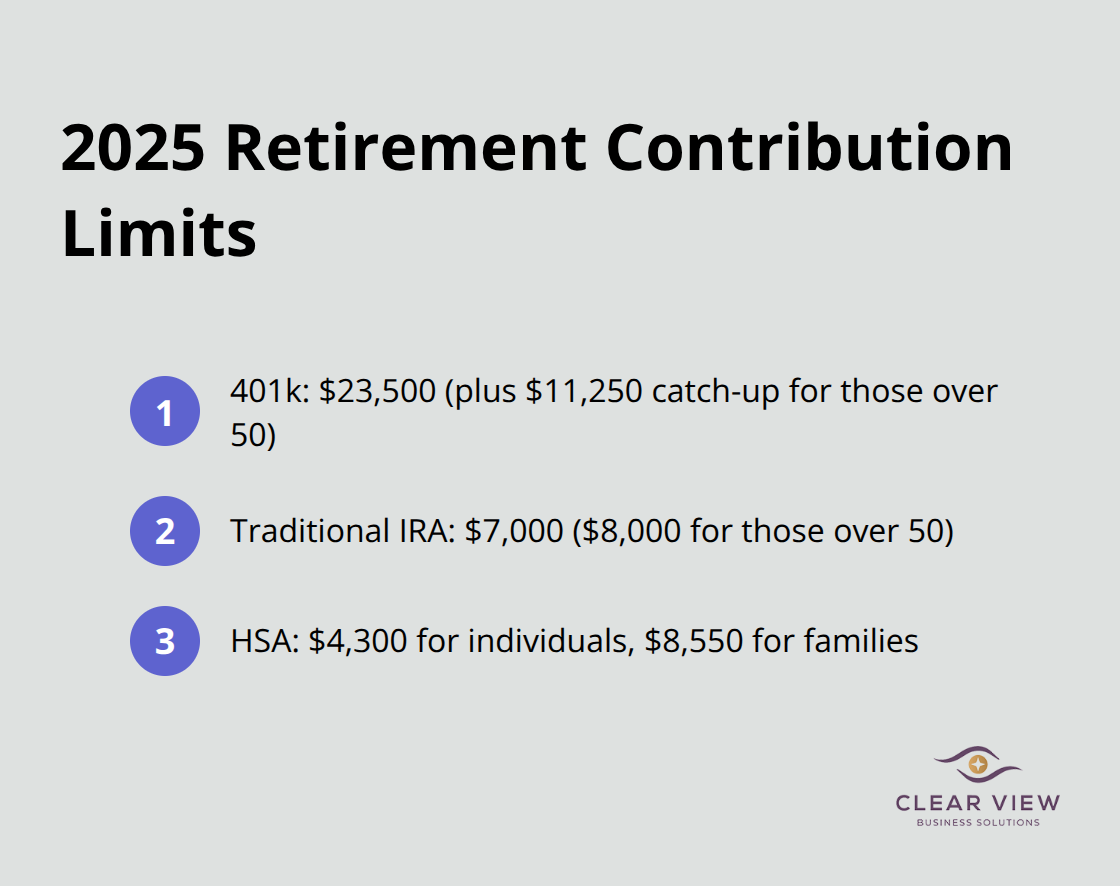

The 401k contribution limit for 2025 reaches $23,500, with an additional $11,250 catch-up contribution for those over 50, totaling $34,750 in tax-deferred savings. Workers in the 32% tax bracket save $9,920 annually through maximum contributions, according to Employee Benefit Research Institute data. Traditional IRA contributions add another $7,000 ($8,000 for those over 50) in tax deferrals, but phase out at $87,000 for single filers with employer plans.

Health Savings Accounts provide triple tax advantages with 2025 limits at $4,300 for individuals and $8,550 for families. HSA funds roll over indefinitely and become retirement accounts after age 65, which makes them superior to traditional retirement accounts for long-term planning.

Small business owners lose $4,200 annually in unclaimed deductions according to the National Federation of Independent Business. The home office deduction allows $5 per square foot up to 300 square feet, which provides $1,500 in automatic deductions without receipts. Vehicle expenses offer two options: standard mileage at $0.67 per mile for 2025 or actual expenses that include depreciation, insurance, and maintenance.

Business meals remain 100% deductible through 2025, while entertainment expenses stay non-deductible. Professional development, software subscriptions, and equipment purchases under $2,500 qualify for immediate expense rather than depreciation schedules. Digital receipt apps like Expensify or Receipt Bank eliminate the 90% documentation failure rate the IRS reports among audited businesses.

Tax-loss harvest reduces capital gains taxes when you sell investments at a loss to offset winners. The wash sale rule prohibits repurchase of identical securities within 30 days, but similar investments in different asset classes remain permissible. Morningstar research shows systematic loss harvest adds 0.77% annually to after-tax returns over 20-year periods.

Capital losses offset ordinary income up to $3,000 annually, with unlimited carryforward for future years. Short-term losses first offset short-term gains (taxed at ordinary rates up to 37%), then long-term gains taxed at preferential rates up to 20%. December tax-loss harvest requires execution before market close on the last trade day to count for the current tax year.

These strategies work best when you implement them consistently throughout the year rather than scramble at year-end.

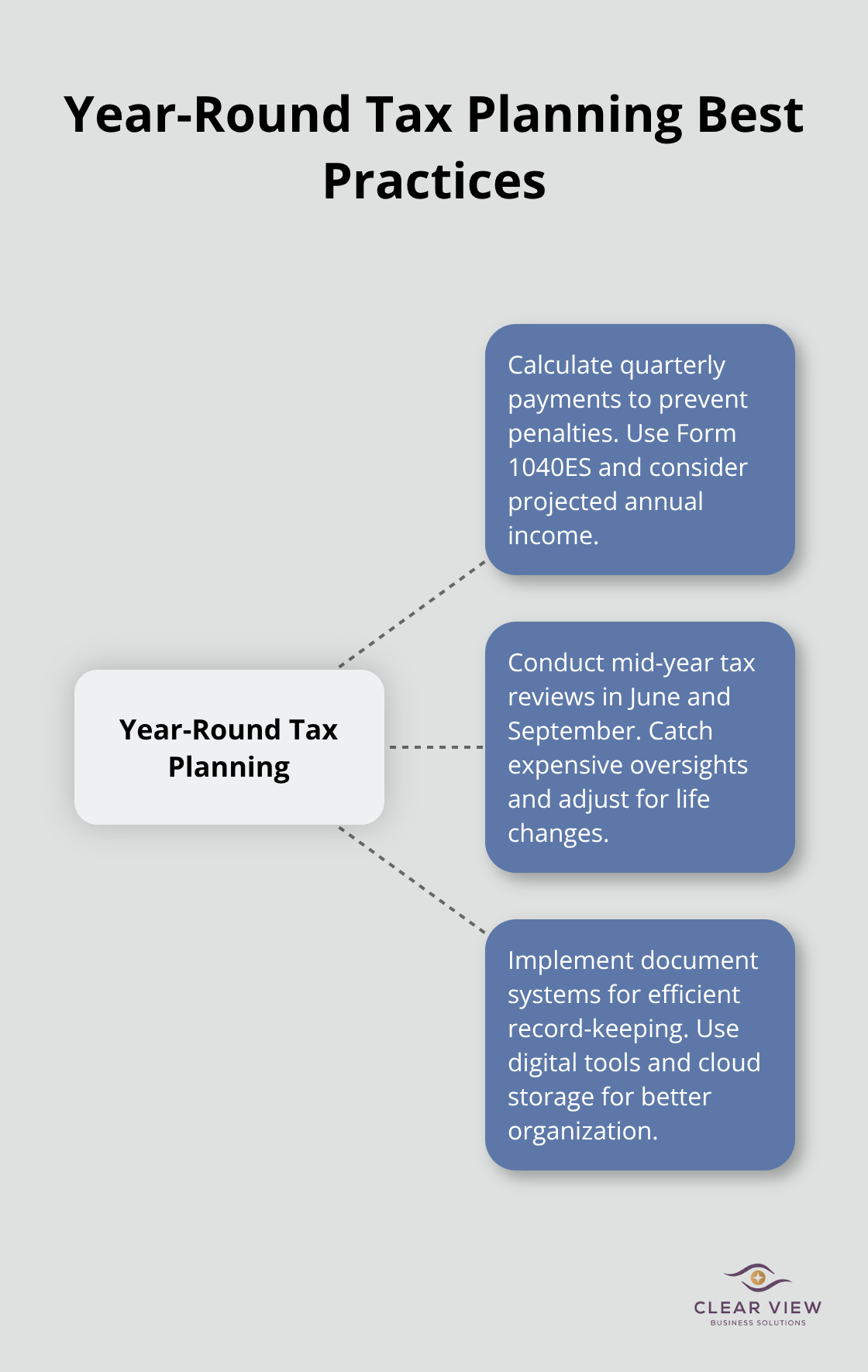

The IRS underpayment penalty hits at 8% annually when you owe more than $1,000 at tax time. Self-employed individuals and investors with irregular income face the highest risk. The safe harbor rule requires you to pay 100% of last year’s tax liability (110% if your prior year adjusted gross income exceeded $150,000) to avoid penalties regardless of current year income fluctuations. Form 1040ES provides worksheets for quarterly calculations, but many taxpayers underestimate their liability when they ignore capital gains, side income, or reduced withholdings from job changes.

We recommend you calculate payments based on projected annual income rather than prior year amounts when income increases significantly. This approach prevents large April surprises and optimizes cash flow management. Third-quarter payments due September 15 often catch taxpayers off guard after summer capital gains realizations or business income spikes.

Tax situations change dramatically between January and December due to job changes, marriage, divorce, home purchases, or business developments. Many taxpayers experience significant life changes that affect their tax liability within any given year. June and September represent optimal review periods – June catches first-half developments while September allows final quarter adjustments before year-end deadlines.

Mid-year reviews focus on withholding adequacy, retirement contribution opportunities, and estimated payment adjustments. Newly married couples often discover their combined income pushes them into higher brackets, which requires immediate withholding increases. Job changes frequently reset 401k contribution tracking and cause missed opportunities to maximize annual limits. Real estate transactions trigger depreciation recapture or capital gains that demand immediate attention from professional tax advisors.

Paper receipts fade within 18 months according to thermal printing studies, which makes digital systems mandatory for audit protection. The IRS accepts digital records for all documentation requirements, but demands consistent organization and backup systems. Receipt scanning apps like Shoeboxed or CamScanner integrate with accounting software to categorize expenses automatically and reduce manual data entry significantly.

Monthly bank statement reviews catch missed deductions before year-end deadlines. Business owners should separate personal and business accounts completely – mixed accounts trigger audit red flags and complicate deduction substantiation. Proper bookkeeping systems organized by year and category (medical, charitable, business, investment) eliminate last-minute scrambles. Cloud storage with automatic backup prevents document loss that costs taxpayers thousands in missed deductions and audit defense fees.

Effective tax planning demands year-round attention rather than last-minute scrambles. The strategies we outlined can save the average taxpayer $2,847 annually when you implement them consistently throughout the year. You must start now with retirement contributions, quarterly payments, and digital expense documentation to avoid costly penalties and missed opportunities.

Professional tax advisory becomes necessary when your situation involves multiple income sources, business ownership, or significant life changes. Complex scenarios require expertise that goes beyond basic tax software capabilities (especially for real estate transactions or entity structures). Mid-year reviews in June and September catch expensive oversights that cost thousands in missed deductions.

We at Clear View Business Solutions help clients maximize tax benefits while maintaining full compliance through personalized tax planning services. Our team works with individuals and small businesses to implement these strategies effectively throughout the year. Start these tax planning strategies immediately rather than wait for next season – the sooner you begin, the more you save.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.