Retirement should be a time of financial peace, not tax-induced stress. Yet, many retirees find themselves grappling with unexpected tax burdens that can significantly impact their nest egg.

At Clear View Business Solutions, we understand the importance of a solid retirement tax strategy. This blog post will guide you through practical ways to minimize your tax liability in retirement, helping you keep more of your hard-earned money.

Many retirees don’t expect Social Security benefits to be taxable. However, up to 85% of your benefits may face federal income tax, depending on your total income. For 2025, if your combined income (adjusted gross income + nontaxable interest + half of your Social Security benefits) exceeds $32,000 for married couples filing jointly, you may have to pay income tax on up to 50% of your benefits. If your combined income is more than $44,000, up to 85% of your benefits may be taxable.

Distributions from traditional IRAs and 401(k)s add to your taxable income for the year. Many people mistakenly believe these accounts are tax-free in retirement – they’re actually tax-deferred, which can result in significant tax bills if not managed properly.

Roth IRAs and Roth 401(k)s offer a tax-free option for your retirement savings. While contributions come from after-tax dollars, qualified withdrawals of contributions and earnings in retirement are not taxed.

Most pension payments are fully taxable. However, if you contributed after-tax dollars to your pension, a portion of your payments may be tax-free. Understanding the specifics of your pension plan is essential to avoid overpaying taxes. Splitting your 401(k), IRA or pension with an ex-spouse can have considerable tax implications, so it’s important to be aware of these potential effects.

Your investment portfolio’s income can significantly impact your tax situation. Long-term capital gains (from assets held more than a year) enjoy preferential tax rates – 0%, 15%, or 20%, depending on your income level.

Understanding these income sources and their tax implications forms the foundation of effective retirement tax planning. The next step involves implementing strategies to reduce your taxable income in retirement, which we’ll explore in the following section.

Minimizing taxes in retirement isn’t just about saving money-it’s about maximizing the value of your hard-earned savings. Strategic tax planning can significantly boost retirees’ financial well-being. Here are some powerful strategies to help you keep more of your money in your pocket.

When you claim Social Security can make a big difference in your tax bill. Delay benefits until age 70 to increase your monthly payments by a certain percentage for each month you delay starting your benefits beyond full retirement age. This strategy not only provides a larger income stream but can also help you manage your tax bracket more effectively in the long run.

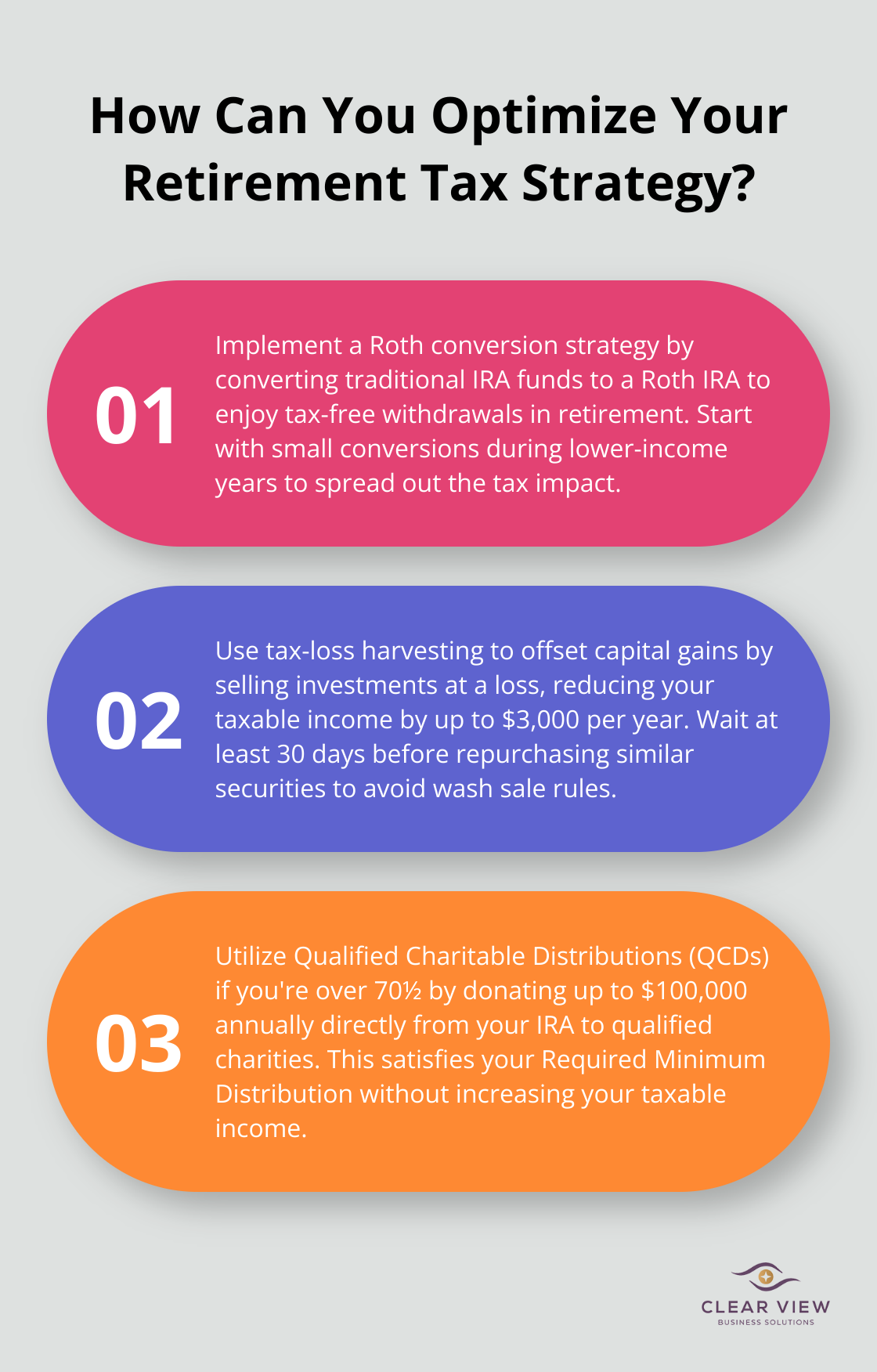

Convert traditional IRA funds to a Roth IRA to change your retirement tax strategy. You’ll pay taxes on the converted amount now, but future withdrawals will be tax-free. This can potentially allow you to better manage your tax brackets and enable more flexibility in retirement.

RMDs can push you into a higher tax bracket if not managed properly. Take distributions before you’re required to, spreading out the tax impact over more years. For those who don’t need the income, donate your RMD directly to charity through a Qualified Charitable Distribution (QCD), which can satisfy your RMD without increasing your taxable income.

Charitable giving isn’t just good for the soul-it’s good for your tax bill too. Bunch donations in a single year to exceed the standard deduction and itemize, potentially lowering your overall tax liability. Use a donor-advised fund to maintain consistent giving while maximizing tax benefits.

Don’t let market downturns go to waste. Sell investments at a loss to offset capital gains (tax-loss harvesting). This strategy can reduce your taxable income by up to $3,000 per year, with additional losses carried forward to future years. Just avoid wash sale rules by waiting at least 30 days before repurchasing similar securities.

Implementing these strategies requires careful planning and consideration of your unique financial situation. The potential tax savings are significant, but it’s important to approach retirement tax planning holistically. Clear View Business Solutions specializes in creating personalized tax strategies that align with your overall financial goals. Our expertise in navigating complex tax laws can help ensure you’re not leaving money on the table when it comes to your retirement savings.

The tax landscape is always changing. What works today might not be the best strategy tomorrow. That’s why it’s essential to work with professionals who stay up-to-date on the latest tax laws and can adjust your plan accordingly. With the right approach, you can significantly reduce your tax burden and enjoy a more financially secure retirement.

Now that we’ve explored strategies to reduce your taxable income in retirement, let’s examine how to withdraw your funds in the most tax-efficient manner possible.

Divide your retirement assets into three buckets: short-term (cash and cash equivalents), medium-term (fixed income), and long-term (stocks). This approach allows you to withdraw from the short-term bucket for immediate needs while the long-term bucket grows. You can potentially lower your overall tax liability by controlling when and how much you withdraw from taxable accounts.

Start withdrawals from taxable accounts first, then tax-deferred accounts, and finally tax-free accounts like Roth IRAs. This sequence can help you maintain a lower tax bracket for longer. For example, if you’re in the 22% tax bracket, you might consider withdrawing just enough from your traditional IRA to “fill up” that bracket before tapping into your Roth IRA.

Municipal bonds can provide an excellent source of tax-free income in retirement. The interest from these bonds is typically exempt from federal taxes (and sometimes state and local taxes as well). While the yields might be lower than corporate bonds, the tax benefits often make them more attractive for retirees in higher tax brackets.

If you’re charitably inclined and over 70½, QCDs allow you to donate up to $100,000 annually directly from your IRA to qualified charities. These distributions count towards your Required Minimum Distributions (RMDs) but aren’t included in your taxable income. This strategy can benefit you particularly if you don’t itemize deductions.

HSAs offer tax-free withdrawals for qualified medical expenses. If you’re eligible, maximize your HSA contributions before retirement. In retirement, you can use these funds tax-free for medical expenses, effectively reducing your taxable withdrawals from other retirement accounts.

Implementing these strategies requires careful planning and consideration of your unique financial situation. While these approaches can serve as powerful tools for tax efficiency, it’s important to consult with a qualified tax professional. Clear View Business Solutions specializes in creating personalized retirement withdrawal strategies that align with your overall financial goals and minimize your tax burden.

A well-planned retirement tax strategy can significantly reduce your tax burden and maximize your financial freedom. We explored various approaches to minimize taxes, from optimizing Social Security claims to leveraging Roth conversions and managing required minimum distributions. The bucket strategy, balanced withdrawals, and use of tax-efficient vehicles can further enhance your retirement tax plan.

Your unique financial situation, goals, and lifestyle choices all play a role in determining the most effective approach for you. What works for one retiree might not be the best option for another. Personalized tax planning helps you make the most of your retirement savings, ensuring you don’t pay more in taxes than necessary.

The intricacies of tax law and the changing financial landscape make professional guidance invaluable. At Clear View Business Solutions, we create personalized retirement tax strategies that align with your overall financial goals. Our team can help you navigate complex tax laws, maximize your savings, and enjoy a more financially secure retirement.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.