A Roth conversion can save you thousands in taxes, but only if you time it right. The wrong move in the wrong year can trigger unexpected tax bills and penalties.

We at Clear View Business Solutions help clients navigate Roth conversion strategies to maximize their tax savings. This guide walks you through when to convert, how the process works, and real examples showing exactly what you’ll owe.

A Roth conversion moves money from a traditional IRA or 401(k) into a Roth account, and the IRS treats that moved amount as taxable income in the year you convert. If you convert $50,000, you owe taxes on $50,000 of ordinary income that year, which could push you into a higher tax bracket. The conversion amount adds to your other income-wages, Social Security, investment gains-to determine your total tax liability. This is why timing matters so much. Converting in a year when you take a sabbatical, experience a business loss, or retire before Social Security kicks in can lower your tax bill significantly compared to converting in a high-income year. The tax you owe is based on the fair market value of the assets on the day the conversion processes, not what you paid for them originally. If your IRA holds stocks worth $100,000 on conversion day, you owe taxes on $100,000, even if you bought them for $40,000 years ago.

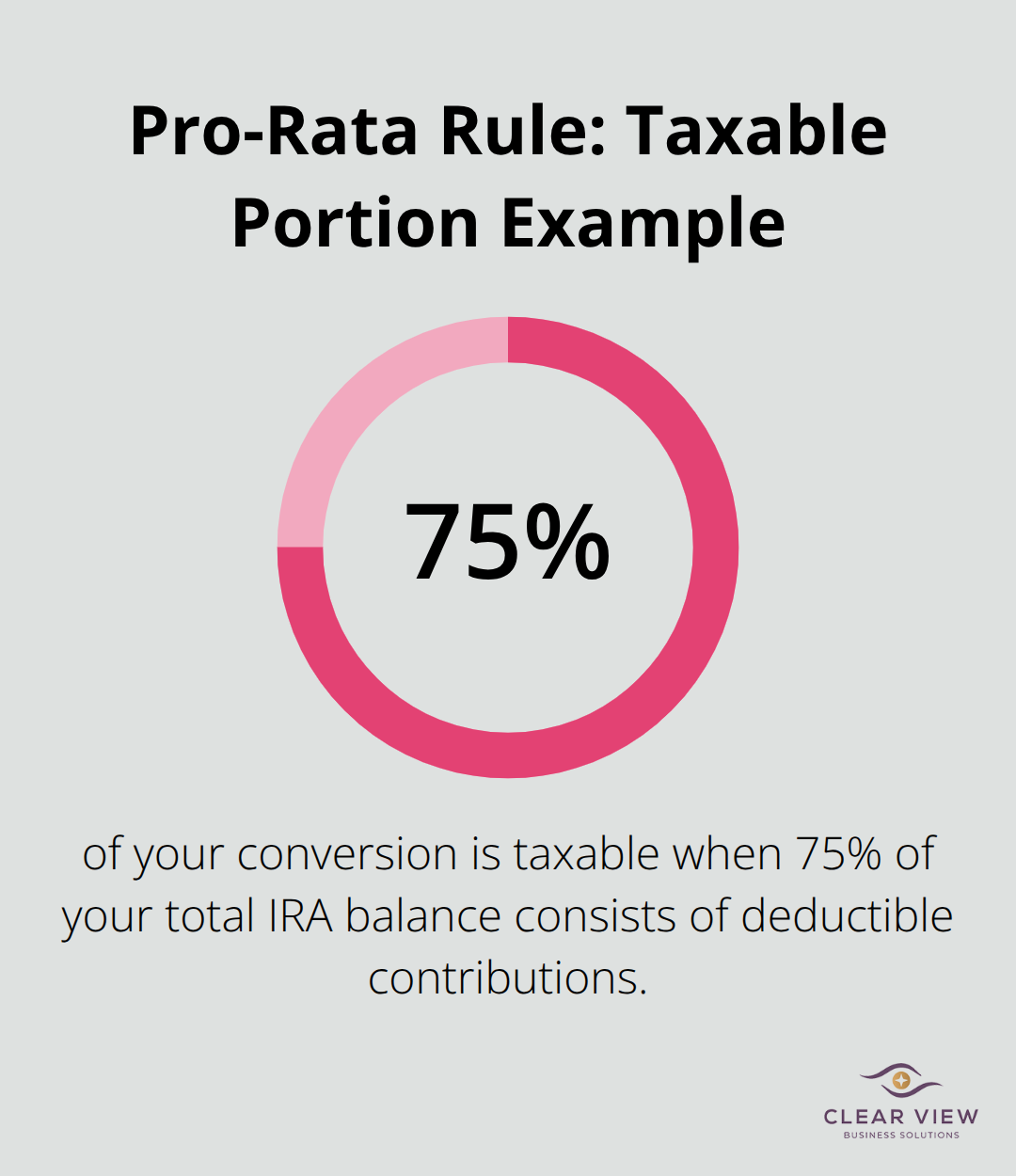

The IRS applies the pro-rata rule to conversions, which treats all your traditional IRAs, SEP IRAs, and SIMPLE IRAs as a single pool for tax purposes. If you have $200,000 in traditional IRAs with $50,000 of nondeductible contributions and $150,000 of deductible contributions, converting $50,000 does not mean you convert the nondeductible portion tax-free. Instead, 75 percent of your conversion becomes taxable because 75 percent of your total IRA balance consists of deductible contributions. This rule applies across every traditional IRA you own, not just the one you convert from.

High earners often try backdoor Roth strategies (nondeductible contributions followed by immediate conversions), but the pro-rata rule can derail this approach if you already hold other traditional IRAs with deductible funds. Many people discover this rule too late and face unexpected tax bills.

Converted funds must sit untouched for five years before you withdraw earnings penalty-free, with the clock starting January 1 of the conversion year. Each conversion has its own separate five-year rule. Withdraw too early and you face a 10 percent penalty on earnings, though the contribution portion can always come out tax-free. Understanding this timing requirement helps you plan when to access your converted funds without triggering penalties.

Now that you understand how taxes work during conversion and what rules apply to your accounts, the next step involves identifying the right year to convert and calculating your actual tax bill.

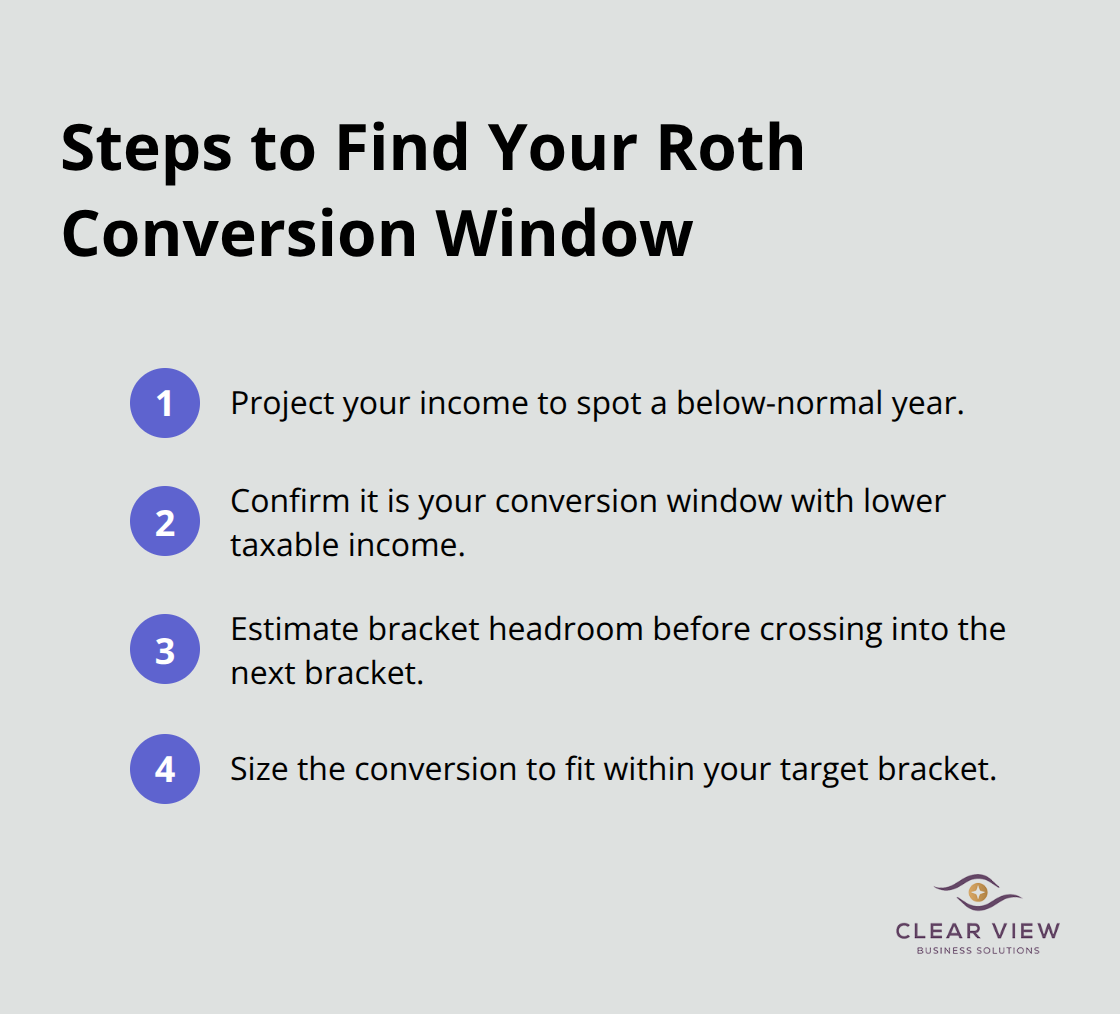

The math behind a successful Roth conversion starts with identifying a year when your income dips below your normal level. This is your conversion window. If you retire at 55 before claiming Social Security, take a sabbatical, experience a business loss, or transition between jobs, your taxable income that year could be 30 to 40 percent lower than a typical year.

Roth conversions during low-income years save substantial federal taxes; converting $50,000 during a low-income year might push you into the 12 percent federal tax bracket instead of the 22 percent bracket you normally occupy, saving you $5,000 in federal taxes alone.

The key is calculating your exact tax bracket for that year and determining how much you can convert before crossing into the next bracket. If you normally earn $120,000 annually and file single, your 2026 standard deduction is $15,000, leaving $105,000 of taxable income. For single filers in 2024, the 12 percent bracket runs from $11,601 to $47,150 of taxable income, so converting more than roughly $11,600 in that low year would push excess amounts into the 22 percent bracket.

Research by McQuarrie and DiLellio in the Journal of Financial Planning shows that converting earlier in your life produces substantially larger after-tax wealth than converting later. Their analysis found that converting at age 60 versus age 72 yields approximately 12 additional years of compounding, a significant advantage that compounds annually. The breakeven point between paying conversion taxes from outside funds versus inside your IRA depends heavily on your time horizon and expected investment returns. With an after-tax return around 8.5 percent, the breakeven occurs at roughly 12 years; with 9.7 percent returns, breakeven stretches to 60 years. This means if you have 15 or more years until retirement, paying the conversion tax from external cash reserves almost always outperforms paying it from within the IRA itself.

The mechanics of staying within your tax bracket require precision. Add your W-2 income, interest, dividends, capital gains, and the conversion amount to find your total taxable income for the year. State taxes compound the decision: residents of states like Florida, Texas, or Washington pay no state income tax on conversions, making those states particularly attractive for conversions. Conversely, if you live in California, New York, or New Jersey, state taxes can add 5 to 13 percent to your federal bill, dramatically raising the total cost.

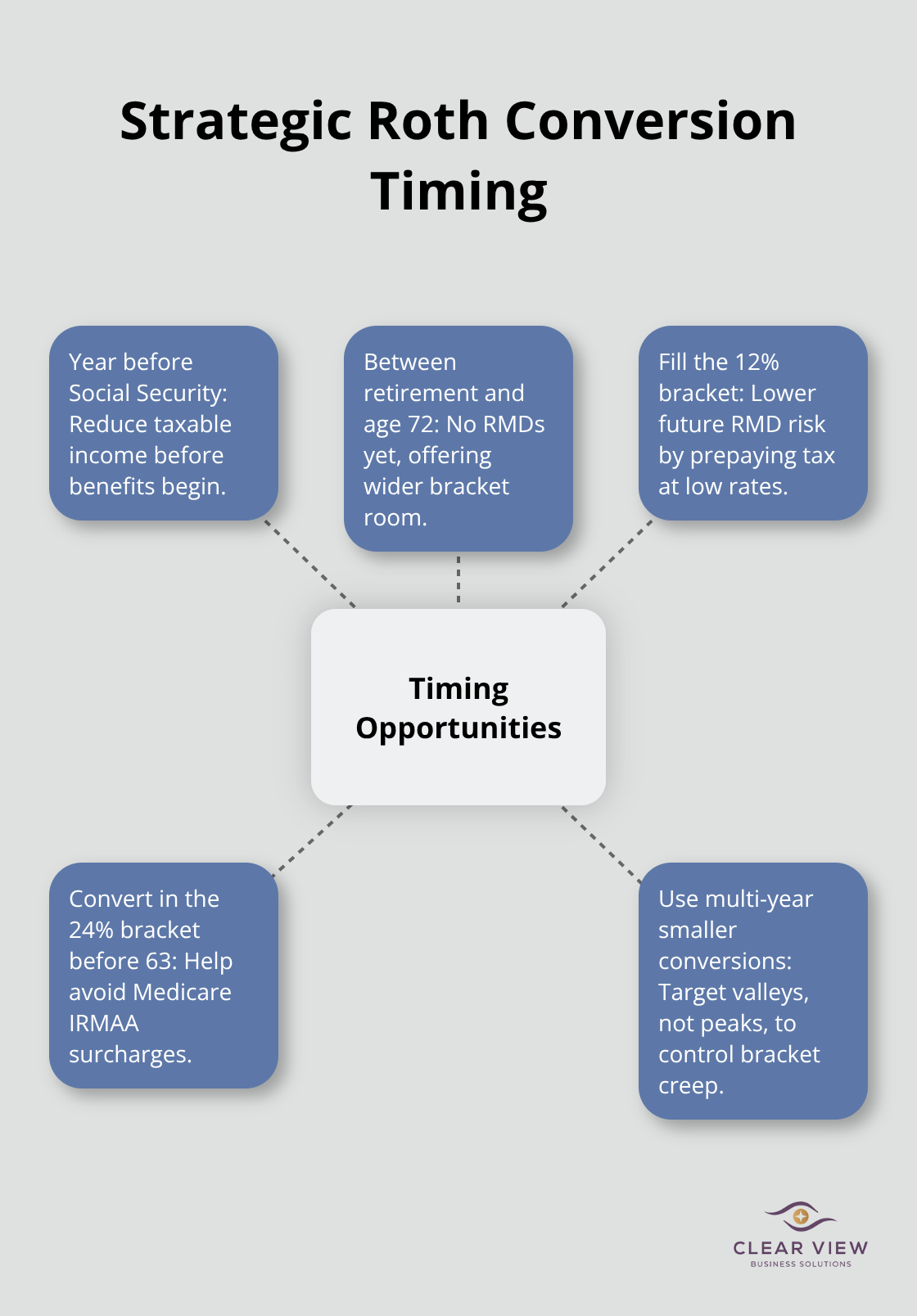

One tactical approach converts in the year before you claim Social Security, because Social Security has not yet entered your income calculation. Another strong opportunity exists between retirement and age 72, when you have no required minimum distributions forcing additional income into your calculation. The Journal of Financial Planning research identifies two sweet spots for robustness: converting high in the current 12 percent bracket (reducing risk that future RMDs push you into higher brackets) and converting in the 24 percent bracket before age 63 to avoid Medicare IRMAA surcharges.

If your income swings significantly year to year, plan conversions during the valleys, not the peaks. Many clients benefit from converting in multiple smaller amounts across several low-income years rather than one large conversion, spreading the tax impact and reducing the risk of bracket creep. This multi-year approach requires advance planning, but the payoff justifies the effort. Once you identify your conversion window and calculate the tax impact, the next step involves understanding exactly how to execute the conversion itself-whether you hold a traditional IRA, a 401(k), or both.

A traditional IRA conversion to a Roth IRA requires opening a Roth IRA if you lack one, then initiating the conversion through your brokerage. Most traditional IRA investments transfer directly to your Roth without forced liquidation, so you can convert individual stocks or mutual funds intact and preserve your holdings. The conversion value calculates using the closing market price on the processing day, not the price when you initiated the request. This timing distinction matters significantly in volatile markets. If your IRA holds $100,000 in securities on Monday but drops to $92,000 by Wednesday when the conversion processes, you owe taxes only on $92,000. Conversely, if markets rally, your tax bill rises with them.

Processing typically completes within three to five business days after submission, so monitor market conditions if you convert in a volatile period. The deadline for completing a Roth conversion to count toward a given tax year is December 31, and once processed, conversions cannot be reversed. This finality demands careful calculation beforehand. Many clients work backward from their target tax bracket: if you want to stay in the 24 percent bracket and your current taxable income sits at $160,000, converting roughly $28,000 stays near the bracket ceiling for single filers in 2026, avoiding unnecessary bracket creep.

A 401(k) conversion follows different mechanics than an IRA conversion. Some employer plans offer in-plan Roth conversions, allowing you to convert directly from your 401(k) to a Roth 401(k) without leaving the plan. Others require you to roll the 401(k) balance to a traditional IRA first, then convert that IRA to a Roth. The two-step approach adds complexity but may be necessary depending on your plan’s rules. Contact your plan administrator directly to confirm which option applies, because the path you choose affects both taxes and fees. In-plan conversions typically process faster and keep funds within employer plan protections, while rollover conversions offer more flexibility on investment choices.

The pro-rata rule applies to 401(k) conversions identically to IRA conversions, meaning if you hold other traditional IRAs, the taxable portion of your 401(k) conversion depends on your combined traditional IRA balances across all accounts. This is where many high earners stumble: they attempt a backdoor Roth strategy without realizing existing traditional IRA balances will trigger substantial taxes on the conversion. Calculate your total traditional IRA basis before initiating any 401(k) conversion.

Real numbers clarify the stakes. Suppose you earn $180,000 annually, retire early at 55, and take no other income that year. Your 2026 standard deduction is $15,000, leaving $165,000 of taxable income. The 24 percent federal bracket for single filers extends to $191,950, so you could convert up to roughly $26,950 staying within that bracket. Converting $30,000 would push $4,050 into the 32 percent bracket, costing an extra $162 in federal taxes plus applicable state taxes. In a state like California, that $4,050 faces an additional 9.3 percent tax, adding $377 more. These incremental costs compound across multiple conversions, making precision essential.

Another scenario illustrates the pro-rata rule’s impact. You own $300,000 in a traditional IRA with $60,000 of nondeductible contributions and $240,000 deductible. Converting $100,000 triggers the pro-rata rule: 80 percent of your IRA balance is deductible, so $80,000 of the conversion becomes taxable while only $20,000 remains tax-free. At a 24 percent federal rate, you owe $19,200 on that conversion. Paying that tax from external funds positions your Roth for maximum growth, and with 15 years until age 70, the tax advantage over paying the tax internally reaches approximately $5,000 to $8,000 depending on market returns.

A successful Roth conversion strategy hinges on identifying your lowest-income year, calculating the exact tax impact, and executing the conversion before December 31. Converting during a sabbatical, early retirement, or business loss year saves thousands in federal and state taxes compared to converting in a high-income year, and the pro-rata rule demands that you account for all traditional IRAs when calculating your tax bill. Time horizon matters enormously-converting at 60 instead of 72 generates roughly 12 additional years of compounding, a substantial advantage that justifies paying conversion taxes from external cash reserves in most scenarios.

The mechanics are straightforward once you understand the rules. Traditional IRA conversions transfer holdings directly without forced liquidation, while 401(k) conversions may require a rollover step depending on your plan, and processing takes three to five business days with the conversion value locking in at the closing market price on the processing day. State taxes compound your federal bill, making conversions particularly attractive in no-income-tax states like Florida, Texas, or Washington.

Your next step involves scheduling a consultation to review your current IRA and 401(k) balances, estimate your tax brackets for the next five years, and model Roth conversion strategies specific to your situation. Contact Clear View Business Solutions to start planning your conversion strategy today.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.