Retirement tax planning is a critical aspect of financial preparation that many overlook. At Clear View Business Solutions, we’ve seen how proper tax strategies can significantly impact retirees’ financial well-being.

Effective planning can help you keep more of your hard-earned money and avoid unexpected tax burdens during your golden years. This guide will explore key strategies to optimize your retirement tax planning, ensuring you’re well-prepared for a financially secure future.

Retirement brings a shift in your income sources and tax situation. At Clear View Business Solutions, we observe how proper tax strategies impact retirees’ financial health. Social Security benefits might be taxable depending on your total income, including tax-exempt interest. This underscores the importance of understanding how each income source affects your tax bill.

Retirement income sources come with varying tax consequences. Traditional IRA and 401(k) withdrawals typically incur taxes as ordinary income. Roth IRA distributions, however, are generally tax-free if you meet certain conditions. Pension payments usually face full taxation. Understanding these differences allows you to plan your withdrawals strategically and minimize your tax burden.

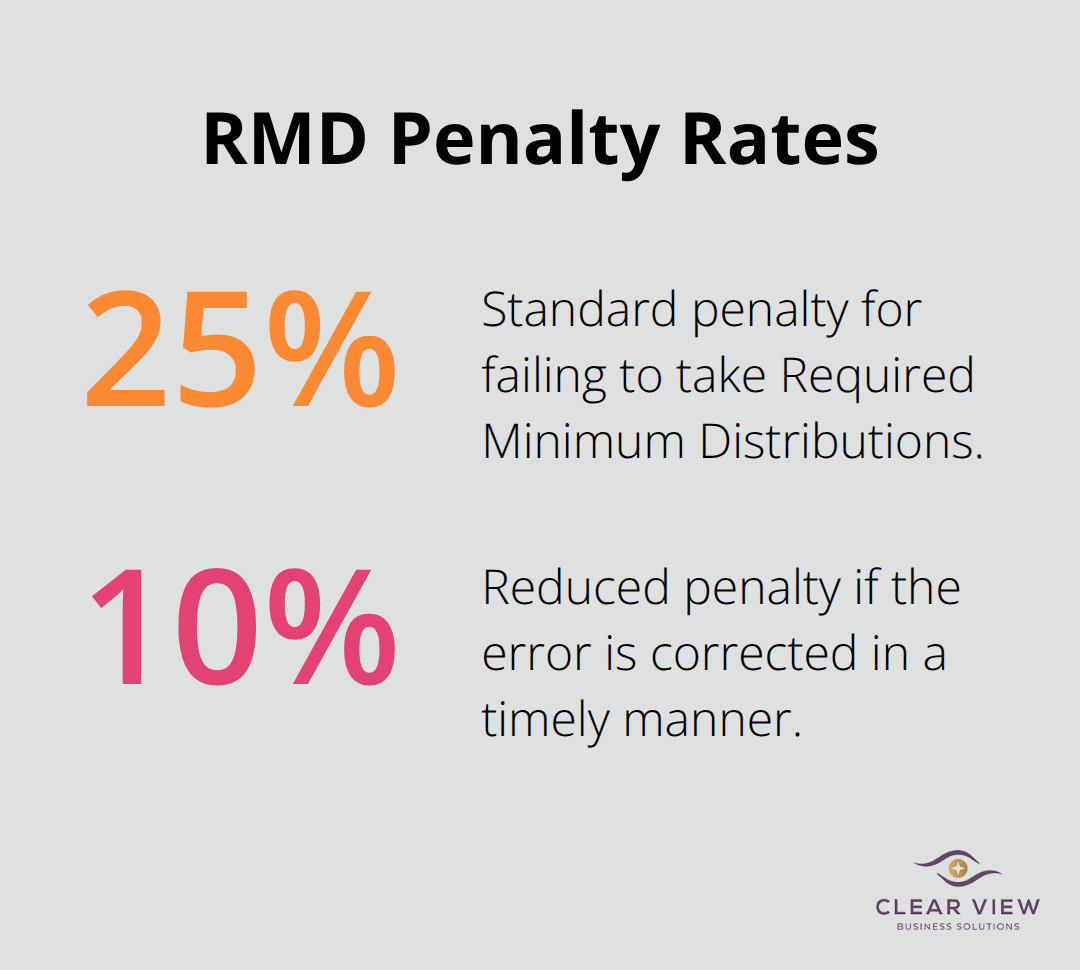

At age 73, you must start taking RMDs from most retirement accounts. These mandatory withdrawals can significantly impact your tax situation. Failing to take RMDs could trigger a 25% (or 10% if corrected in a timely manner) excess accumulation penalty from the IRS on the amount not withdrawn. Planning for RMDs helps you avoid unnecessary taxes and penalties.

Tax planning creates a sustainable income stream throughout your retirement. It’s not a one-time event but an ongoing process. Understanding the tax implications of your retirement decisions enables you to make informed choices that benefit your long-term financial health.

As we move forward, we’ll explore specific strategies to minimize taxes in retirement, including diversifying retirement accounts and making strategic withdrawals. These tactics will help you keep more of your hard-earned money and avoid unexpected tax burdens during your golden years.

Don’t put all your eggs in one basket. Diversify your retirement savings across different account types. Traditional IRAs and 401(k)s offer tax-deferred growth, so you pay taxes only when you withdraw. Roth IRAs provide tax-free withdrawals in retirement. Maintain a mix to gain flexibility in managing your tax liability each year.

In a lower-income year, withdraw more from your traditional IRA. During higher-income years, tap into your Roth IRA for tax-free income. This strategy helps you stay in lower tax brackets and potentially reduces your overall tax bill.

Strategic withdrawals can significantly impact your tax situation. Start taking distributions from taxable accounts first, which allows tax-advantaged accounts to continue growing. This approach can help you delay Required Minimum Distributions (RMDs) and potentially reduce your lifetime tax burden.

If you’re in a lower tax bracket early in retirement, consider converting some traditional IRA funds to a Roth IRA. You’ll pay taxes on the conversion now, but future withdrawals will be tax-free. This can benefit you if you expect to be in a higher tax bracket later in retirement.

Where you hold your investments matters. Keep tax-inefficient investments (like bonds or REITs) in tax-advantaged accounts. Place more tax-efficient investments (such as index funds or long-term stocks) in taxable accounts.

Municipal bonds can excel in taxable accounts, as the interest is often exempt from federal taxes (and sometimes state taxes too). For instance, a high-yield savings account might offer a 3% return, but after taxes, you’re left with less. A municipal bond yielding 2.5% could actually provide a better after-tax return.

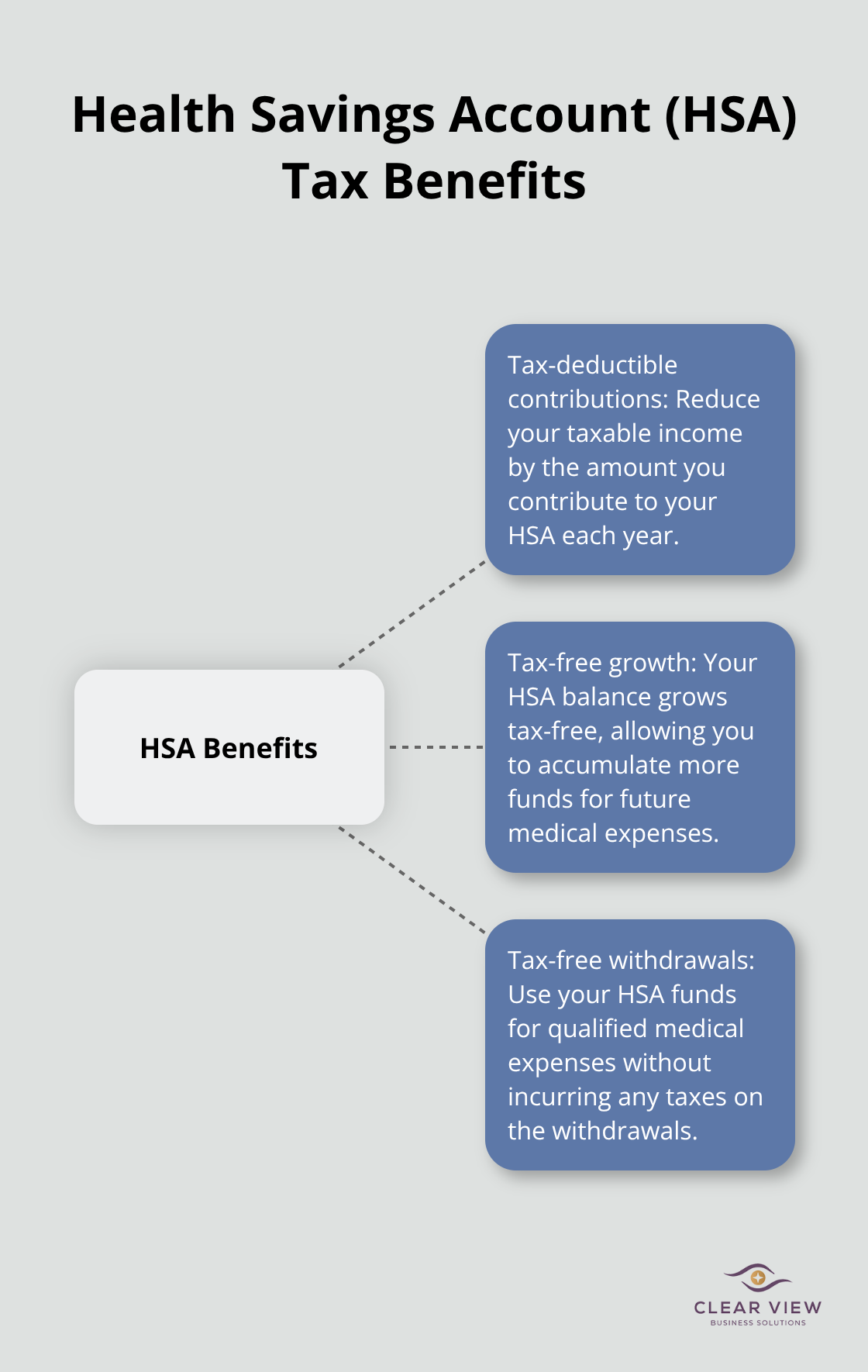

Health savings accounts (HSAs) are savings vehicles that offer tax benefits and can help you cover what may be your largest expense in retirement: health care. If you’re eligible, maximize your HSA contributions. You can even invest these funds for potential growth, creating a tax-free medical expense fund for retirement.

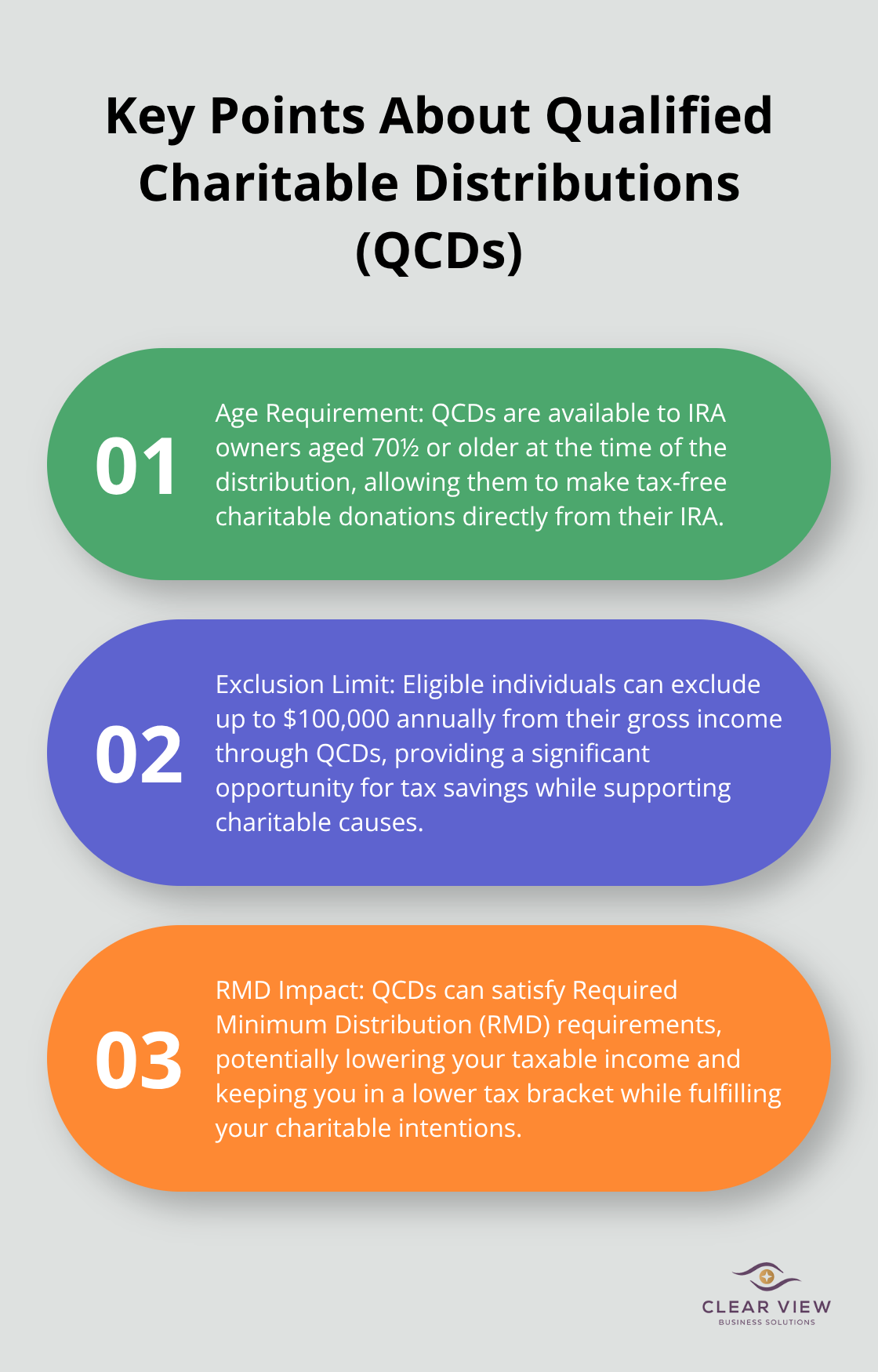

If you’re charitably inclined and over 70½, QCDs allow you to donate up to $100,000 annually directly from your IRA to eligible charitable organizations. These distributions become tax-free as long as they’re paid directly from the IRA to the charity. It’s a win-win: you support causes you care about while potentially lowering your tax bill.

These strategies can make a real difference in your retirement finances. Implement a mix of these approaches, tailored to your specific situation, and you might save thousands in taxes over your retirement years. Tax laws change frequently, so review and adjust your strategy regularly with a professional advisor. As we move forward, let’s explore some advanced tax-saving techniques that can further optimize your retirement tax planning.

Roth IRA conversions can transform your retirement tax strategy. This strategy might benefit those who anticipate being in a higher tax bracket in the future, as it allows you to pay taxes on the converted amount now, potentially saving on taxes in retirement.

Example: If you’re in a lower tax bracket now but anticipate a higher bracket in retirement, converting some funds to a Roth IRA could result in tax savings on those withdrawals. However, large conversions might push you into a higher tax bracket for the year.

The IRS allows you to spread conversions over several years, which helps manage the tax impact. Work with a tax professional to determine the optimal conversion amount and timing for your situation.

Qualified Charitable Distributions (QCDs) offer a win-win opportunity for philanthropically-minded retirees aged 70½ or older. Each year, an IRA owner age 70½ or over when the distribution is made can exclude from gross income up to $100,000 of these QCDs.

QCDs can satisfy your Required Minimum Distribution (RMD) while reducing your Adjusted Gross Income (AGI). A lower AGI can lead to reduced Medicare premiums and may keep you in a lower tax bracket. It’s a powerful way to support causes you care about while optimizing your tax situation.

Health Savings Accounts (HSAs) often go underutilized in retirement planning. If you’re eligible, maxing out your HSA contributions can provide triple tax benefits: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

In 2025, individuals can contribute up to $4,150, and families can contribute up to $8,300 to their HSAs. If you’re 55 or older, you can add an extra $1,000 as a catch-up contribution. Unlike Flexible Spending Accounts, HSA funds roll over year to year, allowing you to build a substantial tax-free medical expense fund for retirement.

Try to invest your HSA funds for long-term growth. Many HSA providers offer investment options similar to those in 401(k) plans. Treat your HSA as a long-term investment vehicle to potentially accumulate a significant tax-free nest egg for healthcare costs in retirement.

Tax-loss harvesting is a potent strategy for managing your tax liability in retirement. This involves selling investments that have declined in value to offset capital gains in your taxable accounts. The IRS allows you to deduct up to $3,000 in net capital losses against your ordinary income each year (with any excess carried forward to future years).

Example: If you have $10,000 in capital gains and harvest $13,000 in losses, you can offset your gains entirely and deduct an additional $3,000 against your ordinary income. The remaining $7,000 in losses can be carried forward to future tax years.

The wash-sale rule prohibits claiming a loss on a security if you buy the same or a substantially identical security within 30 days before or after the sale. To maintain your investment strategy while harvesting losses, replace the sold security with a similar but not identical investment.

These advanced strategies can significantly enhance your retirement tax planning. They require careful consideration and often benefit from professional guidance.

Retirement tax planning requires a personalized approach tailored to your unique financial situation and goals. You can reduce your tax burden through strategies like diversifying retirement accounts, timing withdrawals, and using tax-efficient investments. Advanced techniques such as Roth IRA conversions and Qualified Charitable Distributions offer additional opportunities to optimize your tax situation.

Professional guidance proves invaluable in navigating the complexities of retirement tax planning. We at Clear View Business Solutions offer comprehensive financial advisory and tax services customized to individual needs. Our expertise in tax planning (for both individuals and entities) can help you make informed decisions and maximize your tax benefits in retirement.

Tax laws change frequently, so you must stay informed and regularly review your retirement tax strategy. A proactive approach to retirement tax planning will help you work towards a more financially secure and enjoyable retirement. Our team stands ready to assist you in creating and implementing an effective tax strategy for your golden years.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.