Most startups fail because of cash flow problems, not bad ideas. Financial controls for startups aren’t boring compliance work-they’re the difference between a business that survives and one that collapses under its own disorganization.

At Clear View Business Solutions, we’ve seen firsthand how startups that implement basic financial controls early avoid costly mistakes and attract investors. This guide shows you exactly which systems to build from day one.

Fraud drains startup cash faster than any bad product ever could. The Association of Certified Fraud Examiners reports that U.S. companies lose an average of 9.8% of revenue to fraud, with median losses ranging from $120,000 for asset misappropriation to $766,000 for financial misstatement. For a startup burning through limited runway, losing nearly one dollar out of every ten to embezzlement or unauthorized spending is catastrophic. In early-stage companies, a single person often controls cash, approvals, and reconciliation simultaneously, creating the perfect conditions for theft or careless mistakes.

Segregation of duties splits responsibilities so no single person initiates, approves, records, and reconciles a transaction. Start with two people reviewing all cash disbursements from day one, even if that means the CEO approves everything initially. This simple control stops fraud before it starts and catches honest errors immediately. When you require dual authorization for disbursements over $1,000 and keep checkbooks physically locked with split duties, you eliminate the opportunity for one person to steal undetected.

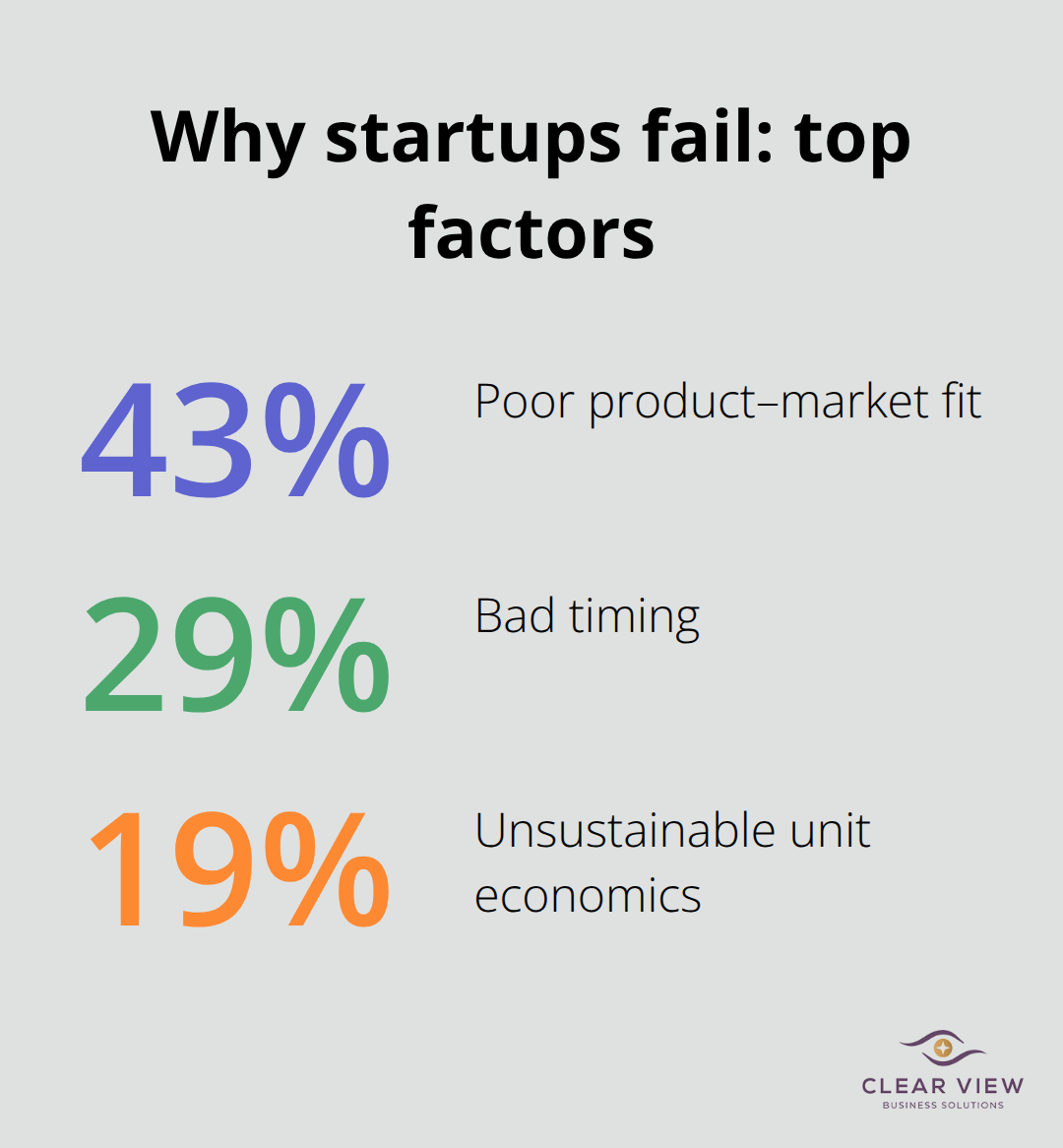

Lenders and investors scrutinize financial records during due diligence, and messy bookkeeping kills deals. Startups fail for many reasons, including poor product-market fit (43%), bad timing (29%), and unsustainable unit economics (19%), alongside capital constraints. Clean financials accelerate fundraising timelines and demonstrate that you understand your business.

When your bank reconciliation is current, expenses are documented with approvals recorded in your accounting system, and financial statements are prepared and reviewed by two people, investors see a founder who has their house in order.

This credibility translates to faster funding decisions and better terms. Startups that postpone bookkeeping until fundraising begins face audit delays, restatements, and lost investor confidence. Cloud accounting software like QuickBooks Online or Xero automates reconciliation and creates an auditable digital trail that investors expect to see. Set up monthly close procedures now so that when you pitch, your financials tell a story of discipline, not damage control.

Financial controls don’t paralyze growth when you design them to evolve. Start lean with three non-negotiable foundations: separate personal and business finances with a dedicated business account and corporate card, implement monthly bank reconciliation (roughly two hours per month), and establish written approval thresholds starting at $500 with dual authorization above $1,000. As you hire, deepen these procedures by assigning specific roles and responsibilities.

Accounts payable controls require a matching purchase order before any invoice is paid, preventing unauthorized payments. Cash management controls include limiting access to bank accounts, requiring dual authorization for large disbursements, and keeping checkbooks physically locked with split duties. Financial reporting controls assign one person to prepare the monthly profit and loss statement and another to review it, catching errors and unusual spending patterns. This tiered approach means you’re not building enterprise-grade controls in month one, but you’re establishing the habits and mindset that make scaling safer.

When you hire your first accountant or bookkeeper, the foundation is already there, so they can focus on deeper analysis rather than reconstructing chaos. The next section covers the specific systems you need to implement right now to lock down your finances.

Open a dedicated business bank account and corporate credit card on day one. This single decision prevents commingling of funds, which destroys audit trails and creates tax nightmares. When personal and business expenses mix, the IRS scrutinizes your records more heavily, your accountant spends hours reconstructing transactions, and you lose the ability to track profitability accurately. A separate business account costs nothing at most banks and takes 30 minutes to set up. Use the business card exclusively for work expenses so your monthly statement becomes a built-in expense log. This separation is non-negotiable because it forms the foundation that makes every other control possible.

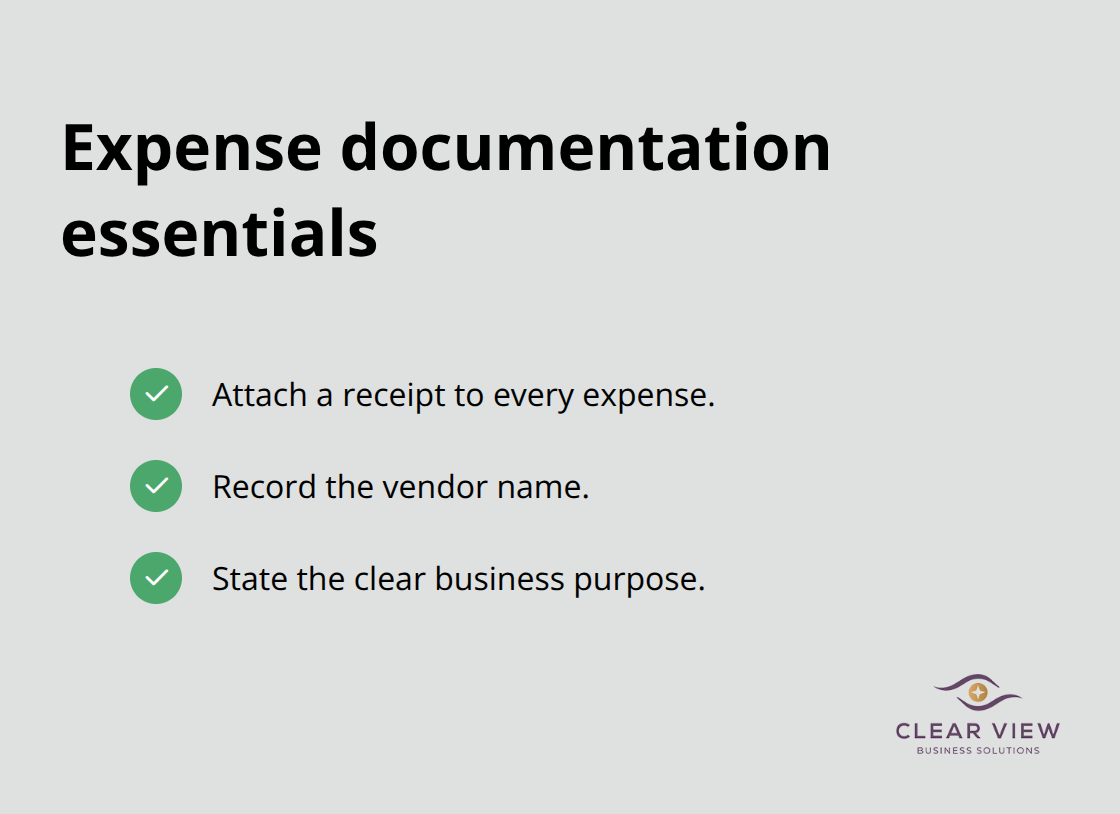

Most startups lose money not to fraud but to forgotten receipts and vague expense descriptions. Cloud accounting software like QuickBooks Online or Xero integrates directly with your bank account, automatically pulling transactions and categorizing them. This integration means you capture transactions in real time rather than manually entering data weeks later; the software does the heavy lifting, and you simply review and categorize each entry. Require every expense to include a receipt, vendor name, and business purpose. When someone submits a $200 expense marked only as “supplies,” you cannot verify it or defend it to auditors. A clear description like “office printer paper and ink cartridges from Staples” takes 10 seconds to write and saves hours later.

Start this habit now because the longer you wait, the harder it becomes to reconstruct what happened.

Monthly bank reconciliation matches your accounting records to your bank statement and catches errors, duplicate charges, and unauthorized transactions before they compound. Most startups skip this because it feels tedious, but the two hours per month you spend reconciling now prevents 20 hours of forensic accounting later. Open your bank statement the first Friday of every month, match each transaction to your accounting software, and investigate any gaps or mismatches immediately while the memory is fresh. If you find a duplicate charge from your cloud provider, you catch it in month one instead of month six when you have been overcharged five times. Unauthorized transactions stand out immediately when you review the statement yourself rather than assuming everything is correct. Require dual sign-off on the reconciliation so one person prepares it and another reviews it, catching mistakes before they embed themselves in your records.

Establish written approval procedures that scale with your company. Start by requiring written approval for any expense above $500 and dual authorization for anything above $1,000. This threshold balances operational speed with control-at $500, you catch meaningful spending without bogging down day-to-day operations, and at $1,000, you require two people to agree before large purchases leave your account. Document approvals directly in your accounting system so a permanent record links to each expense. Use approval workflow tools like Bill.com to automate this process and enforce the rules automatically. The software will not let an invoice over $1,000 be paid without a second approval, removing the possibility of someone forgetting the rule. As you grow and hire team members, expand these thresholds and assign specific approval authority to different roles, but the discipline remains the same from day one.

Limit who can access your bank accounts and corporate cards from the start. Initially, restrict corporate card access to the CEO and office manager; expand access only when proper controls are in place. Keep checkbooks physically locked and require split duties so one person cannot initiate, approve, and execute a payment alone. Require dual authorization for any disbursement over $1,000, and verify all requests to update vendor banking information directly with the vendor to avoid phishing scams. These safeguards sound paranoid until you hear about a startup that lost $50,000 to a fraudulent wire transfer because one person controlled both the bank account and vendor relationships. The cost of these controls is zero; the cost of not having them can be catastrophic.

With your financial foundation locked in place, you now need to establish the approval workflows and documentation practices that prevent unauthorized spending and create an audit trail. The next chapter covers the specific approval processes and documentation standards that protect your cash as your team grows.

Startups that commingle personal and business expenses destroy audit trails within months. The IRS scrutinizes mixed accounts heavily, your accountant spends double the hours reconstructing transactions, and you lose the ability to calculate actual profitability. A founder who runs personal groceries through the business account cannot later claim they do not know whether the company is profitable. When you apply for a business loan or pitch investors, lenders pull your bank statements and see personal expenses mixed with business spending, which signals either incompetence or dishonesty. Neither impression secures funding. The fix is brutal in its simplicity: open a business account on day one and use it exclusively for business. Do not make exceptions. Do not tell yourself you will separate finances later. Later never comes, and by then you have six months of tangled transactions that cost thousands in accounting fees to untangle.

Bank reconciliation is the second control startups abandon, and it is the worst decision they make. Founders skip monthly reconciliation because it feels tedious, but this creates a blind spot where errors, duplicate charges, and unauthorized transactions hide for months. A startup that does not reconcile discovers in month six that the cloud provider has been charging them twice since month one, costing $4,000 in overcharges that are now harder to recover. Unauthorized transactions sit undetected until the damage spreads. One employee with access to the corporate card makes fraudulent purchases, and without monthly reconciliation, the startup does not catch it until the credit card company flags the pattern. Monthly reconciliation ensures your records are accurate, helps detect fraud, and simplifies cash flow management.

Expenses without receipts, vendor names, or business purposes cannot be defended during an audit or to investors. When a founder cannot explain why $500 left the account, auditors flag it as a control weakness, and investors worry about what else is hidden. A $500 unexplained expense seems minor until you have fifty of them and investors question whether the founder is tracking cash at all. Each transaction needs a clear description-not “supplies,” but “office printer paper and ink cartridges from Staples.” This habit takes seconds to establish and hours to reconstruct later. Require every expense to include a receipt, vendor name, and business purpose from your first transaction forward.

Startups that postpone bookkeeping for six months face a reconstruction nightmare. Your accountant must hunt through bank statements, credit card statements, and scattered receipts to rebuild records that should have been clean from the start. This reconstruction costs three to five times what bookkeeping would have cost. The startup misses tax planning opportunities because records are incomplete. When the pitch meeting arrives, financials are stale or unreliable, and investors demand a restatement before committing capital. Cloud accounting software like QuickBooks Online or Xero automates much of this work and creates an auditable trail from day one. Starting bookkeeping immediately means your records stay current, your accountant focuses on analysis rather than reconstruction, and your financials tell a story of discipline when investors ask to see them.

None of these mistakes are unavoidable. Each one is solved by spending a few hours per month on basics from day one: separate accounts, monthly reconciliation, documented expenses, and timely bookkeeping. Startups that build these habits early move faster, raise capital on better terms, and maintain defensible financial records throughout their growth.

Financial controls for startups are not optional extras that you implement once you have money to spare. They form the operational backbone that keeps your business solvent, your records defensible, and your growth trajectory intact. The systems you build in month one determine whether you spend your energy scaling or firefighting financial chaos six months later.

The three foundations we covered-separate accounts, monthly reconciliation, and documented approvals-cost almost nothing to implement but prevent thousands in losses, audit delays, and investor skepticism. A startup that reconciles monthly catches fraud in week one instead of month six. A founder who documents expenses with clear descriptions avoids the nightmare of reconstructing six months of tangled transactions. A team that enforces approval thresholds prevents unauthorized spending and builds the discipline that investors expect to see.

Start today with these actions: open a business account if you have not already, set up cloud accounting software and reconcile your first month this week, and write down your approval thresholds to share with anyone who touches company cash. We at Clear View Business Solutions work with startups every day to build financial systems that protect cash and accelerate growth, handling bookkeeping, tax planning, and financial advisory specifically designed for early-stage companies that need clean records without the overhead of a full finance department. Visit our website to learn how we help startups establish the financial foundation that supports fundraising, compliance, and sustainable growth.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2933 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.