Most people pay more taxes than they need to because they never take time to plan. At Clear View Business Solutions, we’ve seen how individual tax planning strategies can save thousands of dollars when done right.

The difference between a random approach and a deliberate one is significant. This guide walks you through building a tax plan that actually fits your life.

Start by gathering every source of income you receive throughout the year. Most people focus only on their W-2 wages and miss significant tax-planning opportunities. If you have investment income, side business revenue, rental property earnings, or freelance work, each one affects your tax bracket differently. Pull together your pay stubs, 1099 forms for any contract work, brokerage statements showing dividends and capital gains, and records of rental income.

For 2025 taxes, you need to know your exact total income to determine which deductions and credits actually benefit you. Dividends and capital gains are taxable in the year they were paid, even if you automatically reinvested them. Short-term gains hit much harder than long-term gains, which receive preferential rates of 0%, 15%, or 20% depending on your bracket. This income calculation directly determines whether you should itemize deductions or take the standard deduction, which for 2025 is $15,750 for single filers, $31,500 for married filing jointly, and $23,625 for head of household.

The number 0% seems to be not appropriate for this chart. Please use a different chart type.

Deductions reduce your taxable income, so knowing which ones you qualify for saves real money. Many people leave thousands on the table by taking the standard deduction when itemizing would have saved more. Mortgage interest, property taxes, charitable contributions, and medical expenses exceeding 7.5% of your adjusted gross income all qualify as itemized deductions. If you own a home, mortgage interest alone often makes itemizing worthwhile.

For self-employed individuals and small business owners, business expenses directly reduce your taxable income dollar-for-dollar. Home office deductions, vehicle expenses, supplies, and professional fees all qualify. Keep detailed records of these expenses because the IRS expects documentation. Credits differ from deductions in a critical way: a $10,000 credit saves far more than a $10,000 deduction because credits reduce your actual tax owed while deductions only reduce your taxable income. The child tax credit provides a dollar-for-dollar reduction in your tax bill-$2,000 per child under 17. Earned income credits can result in refunds even if you owe no tax, so review whether your income falls below the eligibility thresholds.

Your filing status determines your tax brackets, standard deduction amount, and eligibility for certain credits. This choice matters enormously. Married filing jointly typically produces the lowest tax liability for married couples, but married filing separately sometimes works better if one spouse has significant losses or deductions. Head of household status applies if you’re unmarried and pay more than half the household expenses for yourself and a qualifying dependent. The difference between single and head of household can mean hundreds or thousands in annual tax savings.

If your marital status changed during 2025, the status on December 31st determines your filing status for the entire year. Dependents also affect your calculation significantly. Each dependent reduces your taxable income through the standard deduction and may qualify for the child tax credit. Verify that Social Security numbers are correct for all dependents because errors trigger IRS notices. If you support a parent, adult child, or other relative, they may qualify as dependents if they meet income and residency tests. These details create cascading effects throughout your return and determine your true tax obligation-which is why the next step involves building a strategy that leverages what you’ve just discovered.

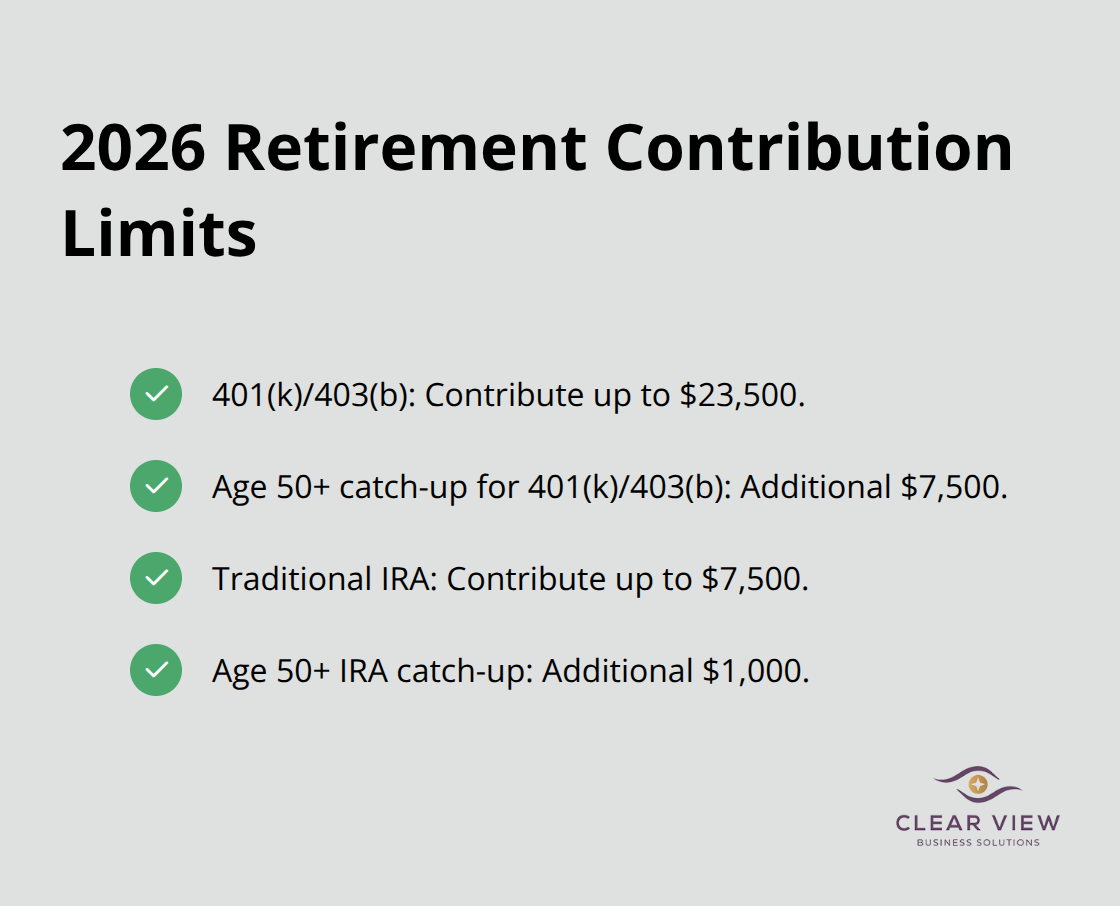

The most powerful tool available to you is maximizing retirement contributions because they shrink your taxable income directly. For 2026, you can contribute up to $23,500 to a 401(k) or 403(b), and if you’re 50 or older, you can add another $7,500 catch-up contribution. That’s real money off your tax bill. Traditional IRA contributions let you put away $7,500 annually, with an extra $1,000 if you’re 50 or older, and these contributions reduce your taxable income if you meet income requirements.

Many people stop at their employer match and miss thousands in tax savings because they don’t max out their own contributions. If your employer matches, that’s free money sitting on the table. Start by calculating exactly how much you can contribute before year-end and set up automatic transfers to hit that limit. The math is straightforward: a $10,000 additional 401(k) contribution in the 24% tax bracket saves you $2,400 in federal taxes alone. Don’t wait until December to scramble for contributions-automate them throughout the year so you actually follow through.

Tax-loss harvesting works by deliberately selling investments at a loss to offset gains elsewhere in your portfolio. If you realized $8,000 in capital gains this year, selling a stock position down $5,000 reduces your net gains to $3,000. The IRS allows you to deduct up to $3,000 of net losses against ordinary income each year, with excess losses carrying forward indefinitely.

The wash-sale rule presents the main constraint: you cannot buy a substantially identical security within 30 days before or after the sale, or the loss gets disallowed. This rule does not apply to cryptocurrency, which means you can sell virtual currency at a loss and immediately repurchase it to lock in the tax benefit while maintaining your position. Most people overlook this opportunity entirely because they assume they must hold positions or miss tax-loss harvesting windows.

The reality is that even in strong market years, individual stocks within the S&P 500 experience significant drawdowns. Work with your advisor to identify losing positions quarterly rather than waiting until December, when everyone scrambles and markets get crowded.

Marriage, divorce, buying a home, starting a business, and inheriting assets all trigger cascading tax changes that most people handle reactively instead of proactively. When you marry, filing jointly typically produces better results than filing separately, but run both scenarios if one spouse has significant losses or business deductions. If you buy a home, mortgage interest becomes deductible, which often tips you from the standard deduction to itemizing.

If you inherit an IRA after 2019, the 10-year rule applies, and you must empty the account by the end of year 10-but you have flexibility in how much you withdraw annually. Taking small distributions early and a large payout in year 10 keeps you in lower brackets longer than taking equal amounts each year. These timing decisions compound over the decade and can save tens of thousands in taxes. Treating tax planning as an ongoing process tied to your actual life changes rather than an annual April scramble positions you to capture these opportunities when they arise.

Most people treat tax planning as an April emergency rather than a year-round process, and this mistake costs them thousands. The IRS issued approximately 1 million math-error notices for the 2023 tax year, and many of those errors stem from rushed filing and incomplete planning. When you wait until tax season, you eliminate your ability to make strategic moves that actually reduce what you owe. Roth conversions, retirement contributions, charitable donations, and tax-loss harvesting all require decisions made before December 31st. If you realize in March that you could have harvested losses or maxed out retirement contributions, you have missed the entire year.

The window closes once the calendar flips to January. You cannot claim a $23,500 401(k) contribution for 2025 when you file in 2026 unless you file an amended return within specific timeframes, which creates additional complexity and paperwork. Smart planning means checking your tax situation quarterly, not annually. Pull a year-to-date income summary from your payroll system or brokerage in September and run preliminary calculations with your tax advisor. This gives you four months to adjust withholding, harvest losses, accelerate or defer income, and max out retirement accounts.

If your employer offers a 401(k), increasing contributions in October or November actually works because payroll can adjust immediately. Waiting until December means you scramble, miss contribution deadlines, and start 2026 in the same reactive position.

State and local tax obligations compound this problem because most people focus exclusively on federal taxes and ignore SALT planning entirely. For 2025, the SALT deduction cap remains at $10,000 regardless of your actual state and local taxes paid. If you live in a high-tax state like California or New York and pay $25,000 in combined state income tax and property taxes, you can only deduct $10,000. This cap has existed since the Tax Cuts and Jobs Act took effect, yet countless high-income earners still treat state taxes as an afterthought.

The strategy here involves timing income recognition and deductions across state lines if you have flexibility. If you are self-employed and moved states during 2025, your income allocation between states affects your total tax burden significantly. Some states tax you based on where you earned the income, while others tax based on where you lived when you earned it. If you worked remotely for a New York employer but lived in Texas for part of the year, both states may claim tax rights unless you document your residency carefully. Business owners with multiple locations face even steeper complexity. Proper state tax planning requires understanding your specific state’s rules before year-end, not discovering them when filing.

Business expenses and home office deductions represent the largest missed opportunity for self-employed individuals and small business owners. The IRS allows a simplified option of $5 per square foot up to 300 square feet, which yields a maximum $1,500 deduction, or you can use actual expenses and depreciate your home. Most people choose the simplified method because it avoids documentation requirements, but actual expenses often produce larger deductions. If your home office occupies 200 square feet and your total home is 2,000 square feet, your office represents 10 percent of your home. You can deduct 10 percent of mortgage interest, property taxes, utilities, insurance, repairs, and depreciation. For someone paying $12,000 annually in mortgage interest plus $4,000 in property taxes, 10 percent equals $1,600 in deductible expenses before utilities and other costs.

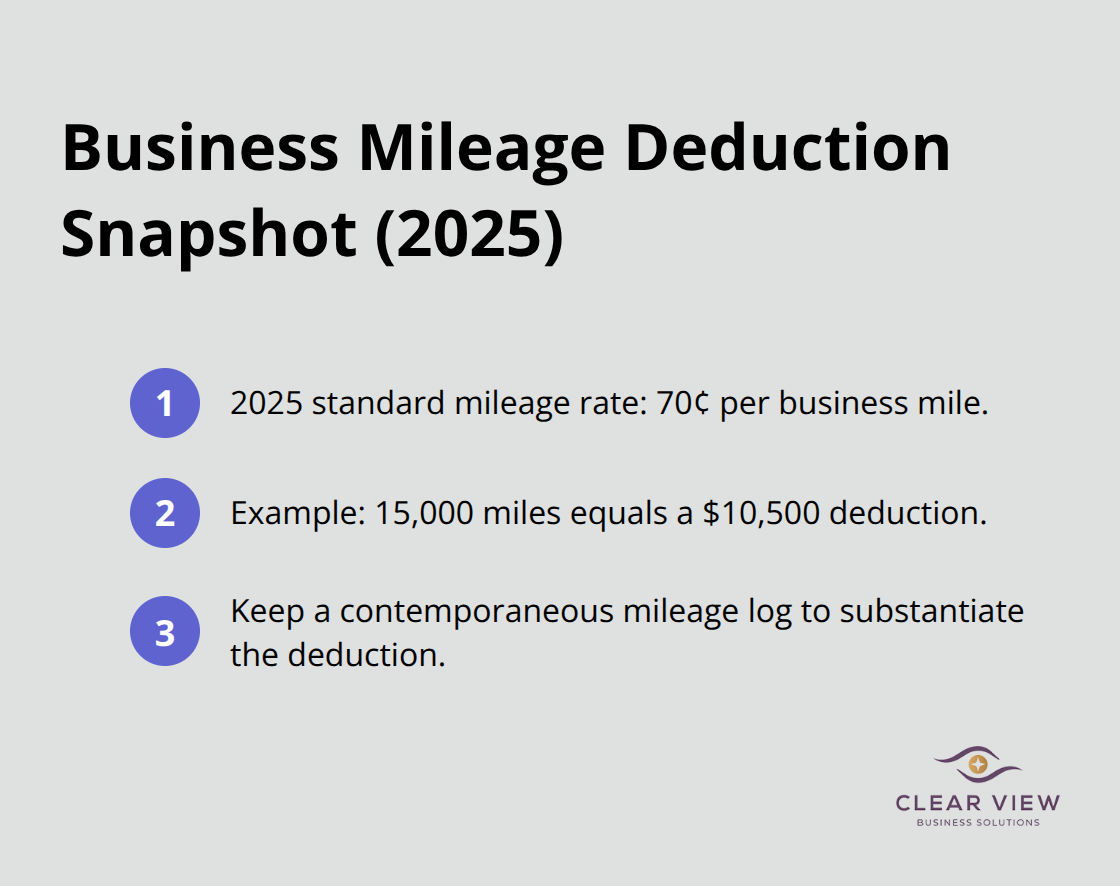

Vehicle expenses follow the same pattern. The IRS standard mileage rate for 2025 is 70 cents per mile for business driving. If you drive 15,000 business miles annually, that generates a $10,500 deduction. Most self-employed people either do not track mileage at all or severely underestimate actual business miles. Start a mileage log immediately and maintain it throughout the year because the IRS expects contemporaneous documentation.

Supplies, software subscriptions, professional development, and equipment purchases all qualify as deductible business expenses. Many owners expense items they should capitalize and depreciate, or capitalize items they should expense, both of which create unnecessary complexity. The key distinction involves useful life: items lasting more than one year typically require depreciation, while supplies and services consumed within the year are immediate deductions.

Staying organized means maintaining a separate business bank account and credit card, which creates an automatic audit trail. If business and personal expenses mix in a single account, the IRS assumes you are hiding something, and the burden falls on you to prove otherwise. Strategic tax planning shows up most clearly in business deductions because they directly reduce your self-employment tax and income tax simultaneously.

Effective tax planning requires you to treat your taxes as a year-round priority rather than an April scramble. The individual tax planning strategies outlined in this guide work because they address your actual financial situation, not generic advice that applies to everyone. Start now by pulling together your income documents and running a preliminary tax calculation in September, then adjust your W-4 if needed, max out retirement contributions before December 31st, and identify tax-loss harvesting opportunities in your portfolio.

If you own a business or work from home, organize your expenses now so deductions are documented and defensible. These actions compound over time and create thousands in cumulative tax savings. Working with a tax professional transforms planning from overwhelming to manageable, and Clear View Business Solutions helps individuals and small business owners build personalized tax strategies that actually work.

Contact Clear View Business Solutions to create a personalized tax plan tailored to your specific situation. The difference between reactive and proactive planning shows up directly in your bank account.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2025 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.