Retirement withdrawals are one of the biggest tax decisions you’ll make, yet most people approach them without a plan. The difference between a thoughtful strategy and random withdrawals can cost you thousands of dollars in unnecessary taxes.

At Clear View Business Solutions, we’ve seen firsthand how tax-efficient retirement withdrawal strategies transform retirement outcomes. This guide walks you through proven methods to keep more of your money where it belongs-in your pocket.

Traditional and Roth IRAs are taxed in opposite ways, and this fundamental difference shapes your entire withdrawal strategy. With a traditional IRA, you get a tax deduction when you contribute, but every dollar you withdraw in retirement counts as ordinary income at your current tax rate. A Roth IRA works differently: you contribute after-tax dollars with no deduction, but qualified withdrawals remain completely tax-free. This means your withdrawal order isn’t just about which account you tap first-it’s about controlling your taxable income in each year.

If you withdraw $50,000 from a traditional IRA, that entire amount counts toward your taxable income, potentially pushing you into a higher tax bracket and triggering taxes on your Social Security benefits. The same $50,000 from a Roth doesn’t count as income at all. According to IRS Publication 590-B, this distinction matters enormously when you manage required minimum distributions starting at age 73. RMDs force you to withdraw a calculated percentage from traditional accounts whether you need the money or not. Miss an RMD and you face a 50% penalty on the amount you should have withdrawn. Most retirees stumble here: they don’t plan ahead, and suddenly they face large withdrawals that spike their income and create unexpected tax bills.

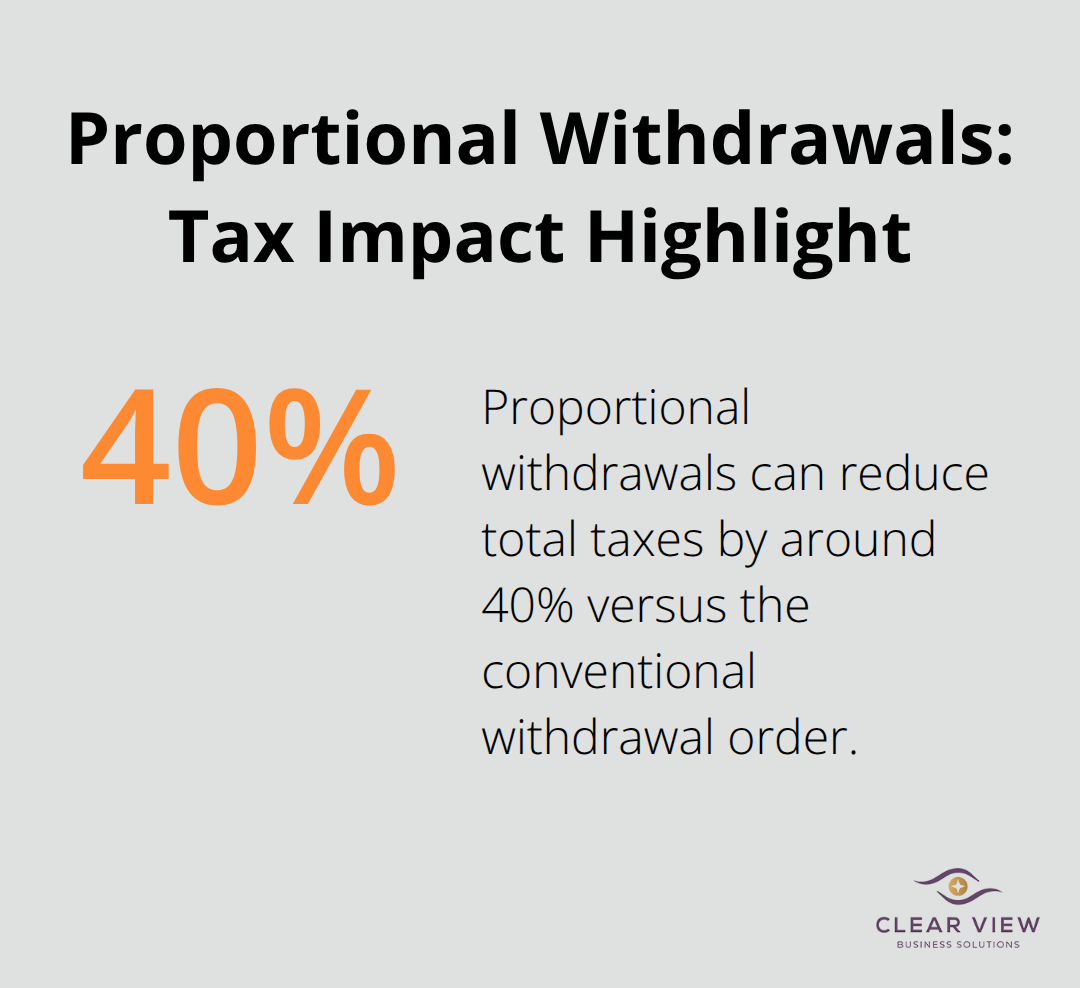

The conventional wisdom says withdraw from taxable accounts first, then traditional IRAs, then Roth accounts last. This approach fails for most people. Research from Fidelity shows that proportional withdrawals-taking from each account type in proportion to how much you have in each-extend your portfolio longevity from roughly 23 to 24 years and cut your total taxes by around 40%. A better strategy targets your tax brackets deliberately.

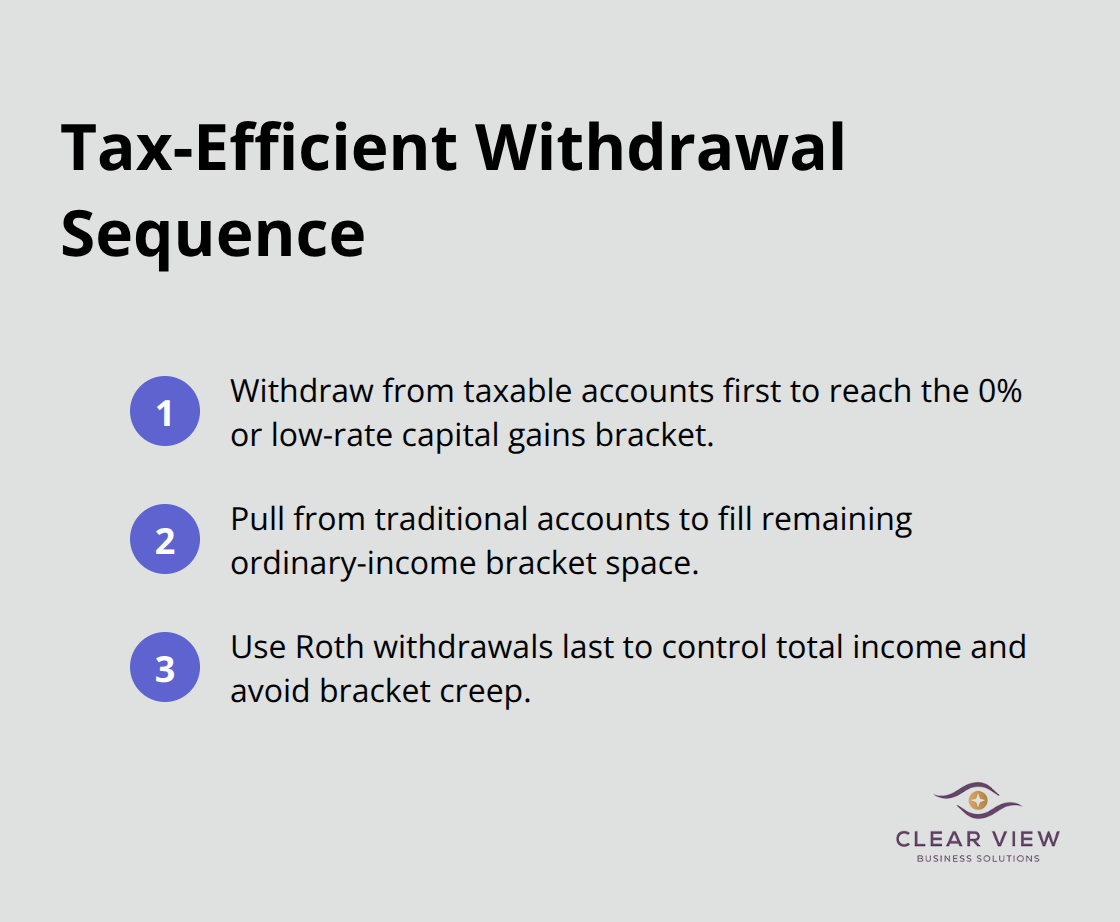

If you have $63,000 in ordinary income and $5,000 in long-term capital gains, that $5,000 gets taxed at 15% based on 2025 rates. But if you have $27,000 in ordinary income and the same $5,000 in gains, those gains get taxed at 0% because you haven’t filled your 0% capital gains bracket. This is why withdrawal sequencing matters so much. You should consider withdrawing from taxable accounts first to reach the 0% or low-rate capital gains bracket, then pulling from traditional accounts to fill remaining bracket space, and finally using Roth withdrawals to manage your overall income.

The order shifts based on your specific numbers, which is why working with a tax professional matters. RMDs add complexity because you must take them regardless of your strategy, so you need to plan withdrawals around these forced distributions to avoid overfilling your tax bracket in any single year. Your withdrawal strategy must account for these mandatory distributions from the start. Understanding how to sequence your withdrawals around RMDs sets the stage for exploring specific methods that professionals use to minimize taxes across your entire retirement.

Most retirees never move beyond the basic withdrawal order, which costs them significantly. The three approaches that actually work require deliberate action, but each addresses real gaps in standard retirement planning.

The bucket strategy organizes your accounts into time-based tiers so you know exactly which funds cover your immediate expenses, medium-term needs, and long-term growth. Your first bucket holds one to three years of living expenses in cash or bonds, your second bucket covers four to ten years in balanced investments, and your third bucket sits in growth-oriented assets for money you won’t touch for over a decade. This prevents panic selling during market downturns and forces you to think clearly about which account type you’re actually spending from each year.

When markets drop, you’re already pulling from your cash bucket, not liquidating stocks at losses. The real benefit emerges when you coordinate this with your tax brackets. If you’re in a low-income year, you can refill your cash bucket from a traditional IRA without triggering a tax spike because you’re using that year’s bracket capacity strategically.

Roth conversion ladders work differently but solve a specific problem: accessing Roth funds before age 59½ without penalties. You convert a portion of your traditional IRA to a Roth in year one, then wait five years before touching those converted funds, which you can withdraw penalty-free. Meanwhile, you repeat the process annually, creating a ladder of conversions that matures each year.

This matters because conversions done during low-income years cost less in taxes. If you retire at 62 but don’t plan to claim Social Security until 70, you have eight years of relatively low income to convert at favorable rates. Strategic conversions amplify this benefit further.

The third method focuses on sequencing taxable accounts strategically. Rather than depleting them first as convention suggests, use them when you’ve filled your 0% capital gains bracket with ordinary income. If you’re single with $48,350 in taxable income, you have room for long-term capital gains at 0% before hitting the 15% bracket. Withdrawing stock gains within that space means paying zero federal tax on those gains.

This requires tracking your ordinary income sources like Social Security and pension payments, then calculating remaining bracket space. A tax professional running scenarios through tools like Fidelity’s Retirement Strategies Tax Estimator shows you exactly how much to withdraw from each account type each year to minimize total taxes. The difference between guessing and calculating often exceeds $5,000 annually for retirees with moderate portfolios. These three methods work best when combined with careful attention to your specific tax situation, which is why the mistakes most retirees make often stem from overlooking how their withdrawal choices interact with Social Security taxation and state income taxes.

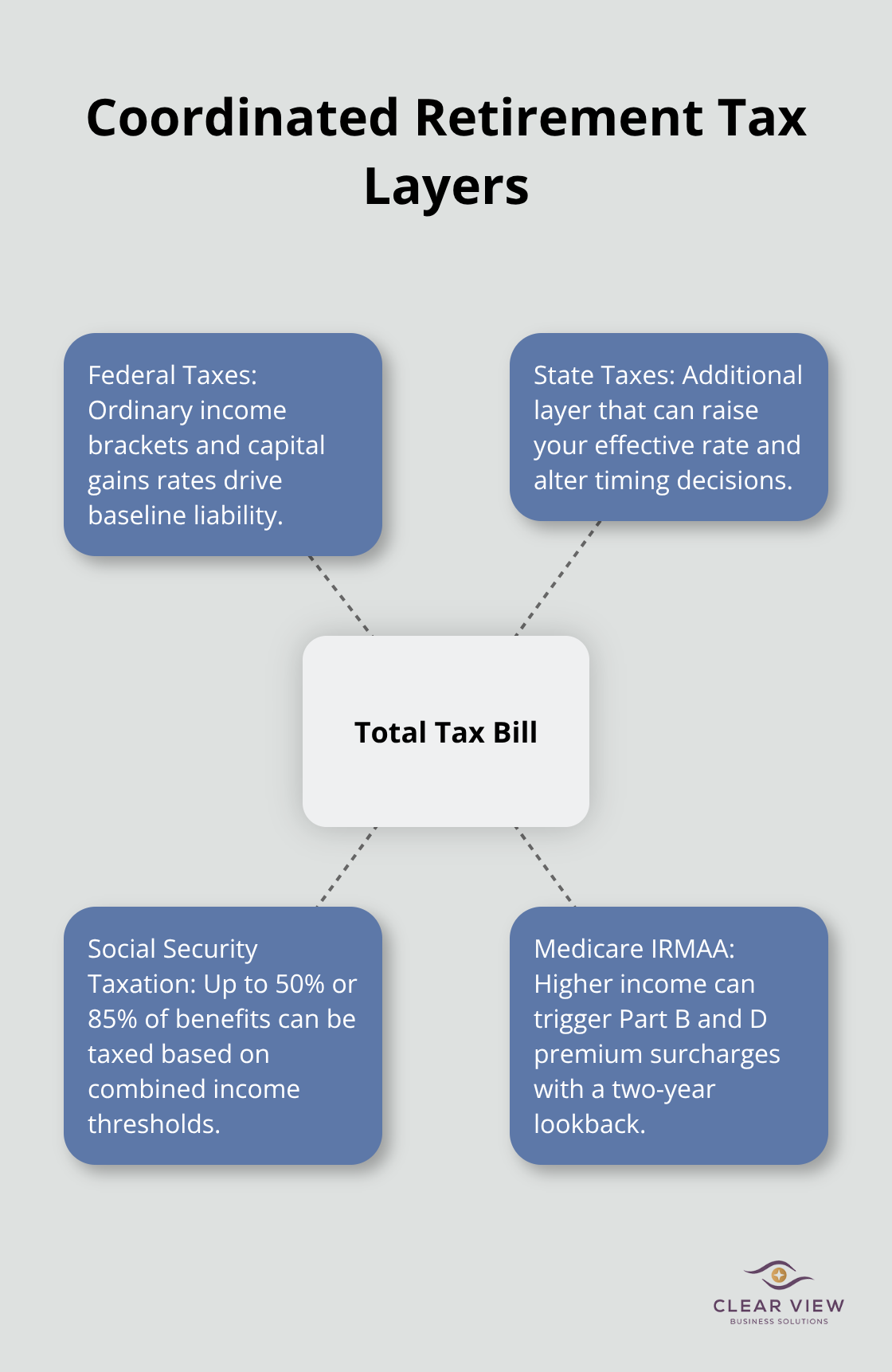

Most retirees make the same critical error: they withdraw money without calculating how those withdrawals affect their total tax burden. A $20,000 withdrawal from a traditional IRA doesn’t cost the same in taxes for everyone because the real damage happens when that withdrawal pushes you into a higher tax bracket or triggers taxes on Social Security benefits you thought were protected. The IRS doesn’t tax these income sources in isolation. Your ordinary income from retirement accounts combines with Social Security benefits, pension payments, and investment gains to determine your overall tax bill. If you withdraw $40,000 from a traditional IRA and receive $25,000 in Social Security, the IRS treats your combined income as $65,000 for tax purposes, even though you might think of these as separate income streams. This combined income number determines whether you pay taxes on 50% or 85% of your Social Security benefits according to IRS rules. A single filer with combined income between $25,000 and $34,000 faces taxes on up to 50% of Social Security benefits. Cross $34,000 and the taxable portion jumps to 85%, according to IRS Publication 915. That threshold matters enormously because pushing $5,000 over the limit can unexpectedly tax an additional $4,250 of your Social Security benefits. Many retirees discover this mistake only after filing their tax return, which means they’ve already made the withdrawal and cannot undo the damage.

Tax brackets create invisible cliffs that catch unprepared retirees. For 2025, a single filer in the 22% federal tax bracket pays more in taxes on a withdrawal than someone in the 12% bracket pays on the same withdrawal. The difference isn’t just the bracket percentage either. Pushing into a higher bracket can trigger the Medicare Income-Related Monthly Adjustment Amounts, which means your Medicare Part B and Part D premiums jump significantly starting the following year. A married couple filing jointly who cross $236,000 in modified adjusted gross income faces higher Medicare premiums for both spouses. This cost persists for multiple years because Medicare uses income from two years prior to set premiums. A large withdrawal in one year affects your Medicare costs for the next two years, creating a ripple effect most people never anticipate.

State income taxes compound this problem further. If you live in a state with income tax, every dollar of ordinary income gets taxed twice: once federally and once at the state level. A $50,000 withdrawal from a traditional IRA costs you federal tax plus your state’s income tax rate. Someone in a high-tax state faces significant combined federal and state taxes on that same withdrawal. That’s a substantial effective tax rate on your withdrawal before you even account for Social Security taxation or Medicare premium adjustments. Coordinating withdrawals with your state’s tax situation requires knowing exactly when you cross into higher brackets and whether your state offers any tax breaks for retirees or specific income sources.

The solution requires calculating your total tax bill across all layers simultaneously rather than thinking about federal taxes in isolation. A tax professional can show you exactly how a $20,000 withdrawal affects your federal taxes, state taxes, Social Security taxation, and Medicare premiums all in one calculation. This comprehensive view prevents the costly mistakes that happen when you optimize for one variable while ignoring others. If you’re in a year with lower ordinary income from other sources, that year represents an opportunity to make a large traditional IRA withdrawal at a lower combined tax rate.

Conversely, if you’re claiming Social Security and receiving a pension payment, your combined income might already be high enough that any additional withdrawal pushes you into the 85% Social Security taxation zone. The decision to withdraw $30,000 versus $25,000 might cost you extra in taxes when you factor in all three layers. Testing different withdrawal amounts before actually withdrawing prevents these expensive surprises. This is why working with a tax professional who understands how your specific situation interacts with federal brackets, state taxes, and Social Security rules matters so much more than following generic withdrawal guidelines.

Tax-efficient retirement withdrawal strategies require you to view withdrawals as part of a coordinated system rather than isolated transactions. Your withdrawal strategy must reflect your specific numbers: your ordinary income sources, your capital gains, your state of residence, and your timeline. A $30,000 withdrawal costs different amounts in taxes depending on whether you’re in year one or year ten of retirement, whether you’ve claimed Social Security yet, and whether you live in a state with income tax.

Tools like Fidelity’s Retirement Strategies Tax Estimator let you compare withdrawal strategies side by side and see the actual tax impact of your choices before you execute them. Testing different withdrawal amounts prevents expensive mistakes that you cannot undo once the money leaves your account. Professional guidance transforms retirement from a guessing game into a deliberate strategy tailored to your complete financial picture.

Start by gathering your account statements and income projections for the next three years, then calculate your combined income from all sources to identify which tax brackets you’ll occupy. Clear View Business Solutions can model your withdrawal options and identify opportunities to reduce your lifetime tax burden through comprehensive tax planning and advisory services. The cost of professional guidance typically pays for itself many times over through taxes saved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.