Most startups fail because of cash flow problems, not bad products. Poor startup bookkeeping is often the culprit-founders get so focused on growth that financial records fall apart.

We at Clear View Business Solutions have seen this pattern repeatedly. The good news is that organized finances don’t require an accounting degree. This checklist walks you through the essential tasks that keep your money visible and your business on solid ground.

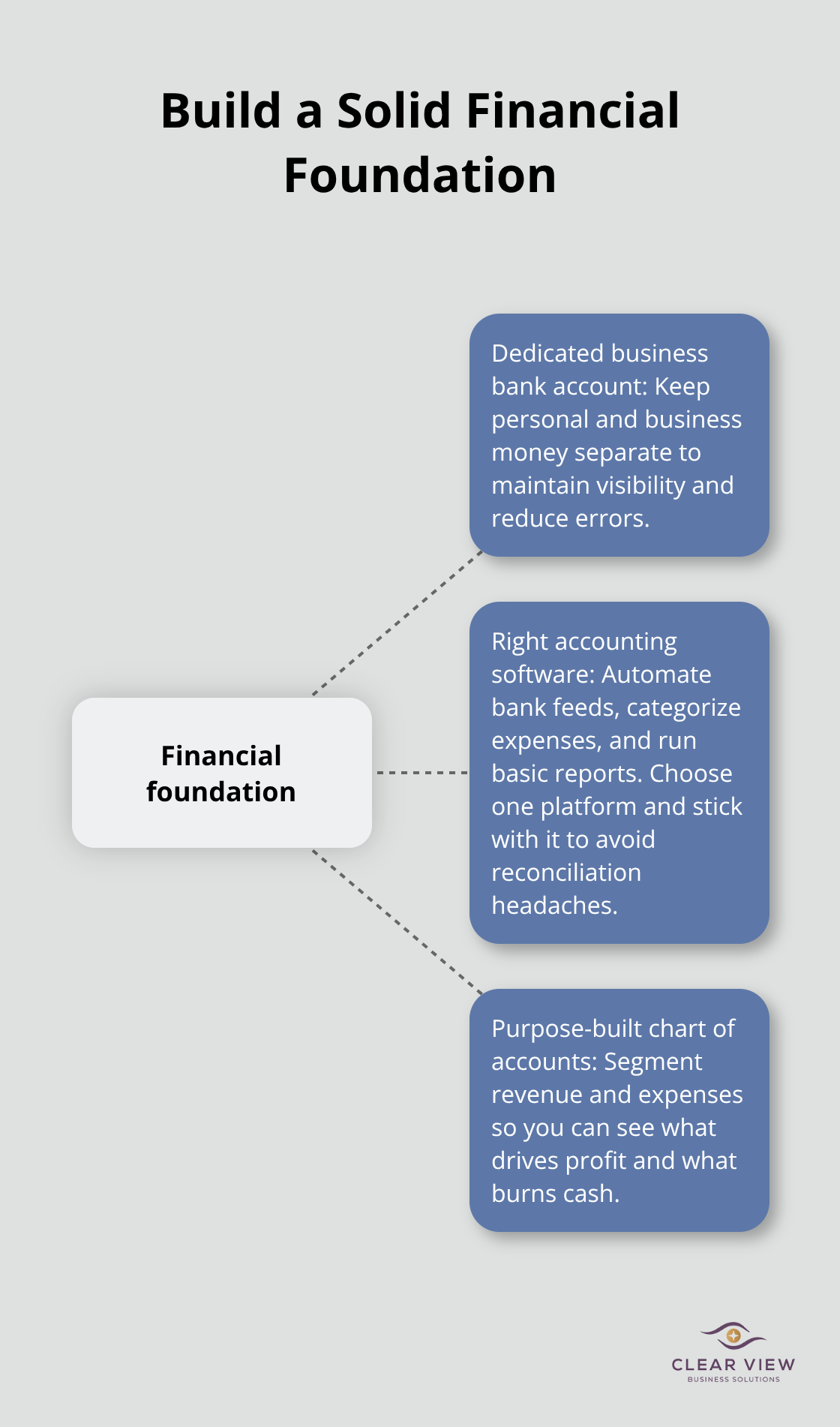

A separate business bank account isn’t optional-it’s the foundation that makes everything else possible. When personal and business money mix, you lose visibility into what your startup actually spends and earns. Open a business checking account within the first two weeks of operation. Most banks offer free or low-cost options for startups, and the setup takes less than an hour online. Link this account to your accounting software immediately so transactions import automatically. This single step eliminates manual data entry and catches errors faster than any other practice.

Accounting software matters far more than most founders realize. QuickBooks Online dominates for startups because it handles bank feeds, expense categorization, and basic reporting without overwhelming complexity. Xero works well if you operate internationally or manage multiple currencies. Wave is free but lacks depth for payroll and multi-user access. Pick one and stick with it for at least two years-switching costs time and introduces reconciliation headaches. Spend your first week learning the software’s core features: how to record income, categorize expenses, and run a profit-and-loss statement. You don’t need to master everything, but understanding these three functions prevents costly mistakes later.

Your chart of accounts is the organizational system for every dollar that flows through your business. Most startups inherit a generic template and never customize it, which creates bloated reports that hide important patterns. Instead, build your chart to match how you actually run the business. If you sell both services and products, create separate revenue accounts for each.

If you’re bootstrapped and watching cash obsessively, add a detailed expense breakdown that separates fixed costs from variable costs. This structure lets you spot which channels burn money and which generate profit. When you review monthly reports, a well-structured chart tells a clear story instead of overwhelming you with line items that don’t matter to your decisions.

With your foundation in place-a dedicated account, software that fits your needs, and a chart that reflects your business-you’re ready to establish the monthly and quarterly routines that keep finances visible and compliant.

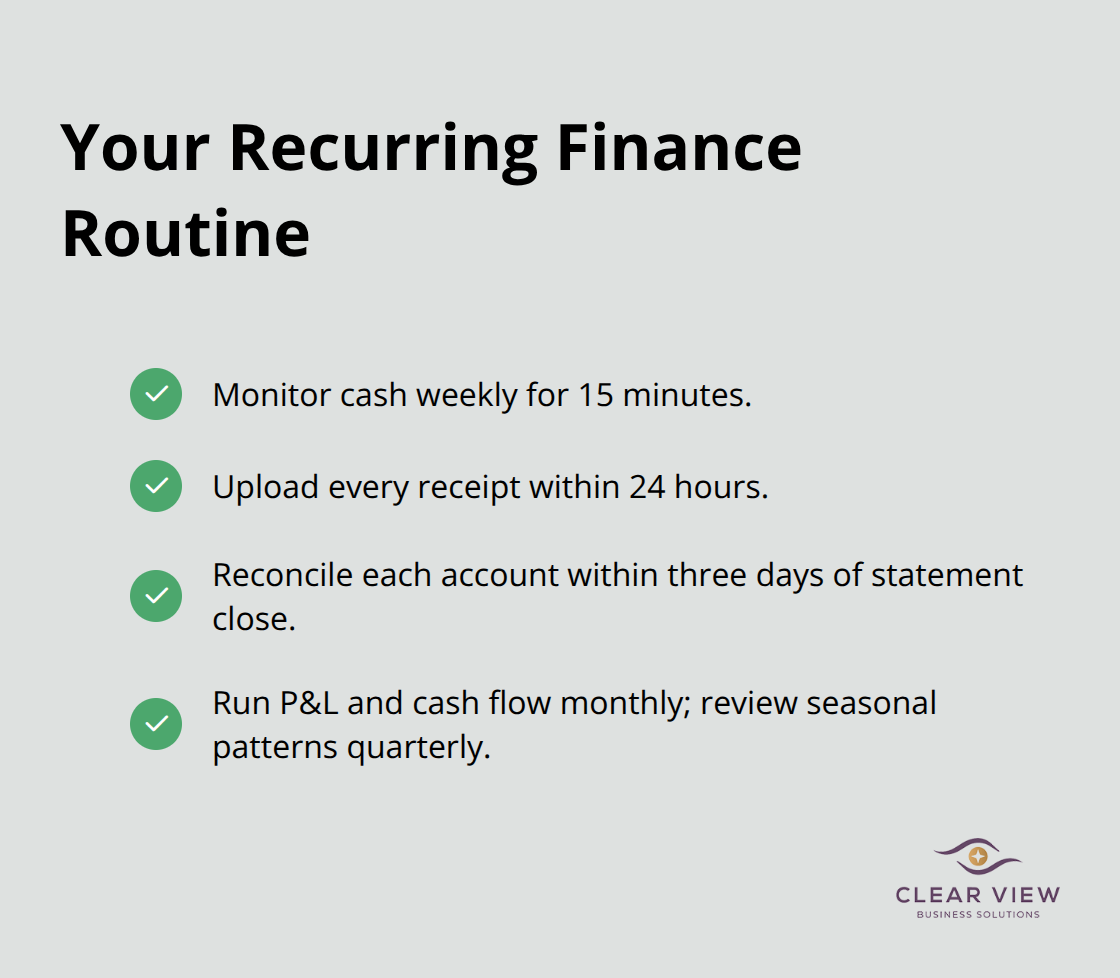

The difference between startups that survive and those that run out of cash comes down to one habit: weekly cash monitoring habits. Most founders wait until month-end to look at their finances, which means problems compound for 30 days before anyone notices. Instead, log into your accounting software every Friday and spend 15 minutes reviewing two numbers-your bank balance and your burn rate. Your burn rate is how much cash you spend each week divided by your revenue that week. If you spend $5,000 weekly and earn $2,000, your burn rate is $3,000 per week. Track this number obsessively in your first year. When you spot a week where burn accelerates or revenue dips unexpectedly, you have time to adjust before it becomes a cash crisis.

Income and expenses should be recorded as transactions happen, not batched at month-end. If you wait to log expense receipts, they pile up, categorization becomes guesswork, and reconciliation turns into a nightmare. Create a simple rule: photograph every receipt and upload it to your accounting software within 24 hours. Daily transaction recording takes two minutes per transaction but saves hours during reconciliation. Most founders skip this step thinking they’ll catch up later, and later never comes.

Bank reconciliation means comparing what your software shows against your actual bank statement. Most startups skip this until tax time, which is exactly when you discover a $3,000 duplicate charge from six months ago that’s now impossible to dispute. Reconcile every account-checking, savings, credit cards-within three days of the statement closing. This isn’t busywork; it’s your early warning system. A missing deposit might signal a customer who promised payment but never delivered. A duplicate charge catches billing errors before they become bigger problems. Unreconciled accounts also create false financial reports, which means you make decisions based on fiction. If your software shows $15,000 in the bank but reconciliation reveals only $12,000, those decisions are wrong. Set a calendar reminder for the same date each month and treat reconciliation like payroll-non-negotiable. Most accounting software flags discrepancies automatically, which makes the process faster than manual checking.

Monthly profit-and-loss statements and cash flow reports matter, but only if you know what to look for. Your P&L shows whether you’re profitable; your cash flow report shows whether you’ll run out of money. These are different things. A startup can be profitable on paper but cash-negative because customers haven’t paid invoices yet or you’ve invested in inventory. Generate both reports on the first business day of each month and compare this month to last month and to the same month last year. Look for line items that jumped unexpectedly. If payroll spiked 40% month-over-month, understand why before next month’s payroll hits. If customer acquisition cost rose, trace it to a specific marketing channel so you can decide whether to double down or cut it off.

Quarterly, add your monthly reports together to spot seasonal patterns. A software-as-a-service startup might see revenue dip in August and spike in January. Knowing this pattern lets you plan cash reserves accordingly instead of panicking when August arrives. Quarterly earnings tracking also gives you time to adjust your budget against actual performance and recalibrate your forecast for the remaining months. This forward-looking approach prevents cash surprises and keeps your team aligned on financial reality.

With weekly cash monitoring, daily transaction uploads, monthly reconciliation, and quarterly pattern analysis in place, you’ve built a system that reveals problems before they spiral. The next step is understanding which mistakes derail most startups-and how to avoid them.

The moment you open a business bank account, the temptation to use it for everything starts immediately. You pay a personal expense from the business account, then move money back later. You buy office supplies with your personal card and plan to request reimbursement next month. Within three months, your bank statements become a tangled mess that no software can untangle. The IRS sees this mixing as a red flag during audits. More practically, you lose the ability to answer basic questions: How much did I actually spend on supplies last month? Did I overpay for inventory? Your financial reports become fiction because the underlying data is corrupted.

Separate accounts are non-negotiable, but separation only works if you enforce it religiously. If you slip and use the business account for personal expenses, reverse the transaction immediately and document why. If you use a personal card for business expenses, reimburse yourself within one week, not one month. The longer you wait, the harder reconciliation becomes and the more likely you’ll forget the original business purpose of the expense.

Most founders obsess over large purchases but ignore small ones. A $12 lunch, an $8 subscription renewal, a $45 software trial-these feel insignificant individually. The IRS allows deductions for ordinary business expenses, which includes meals during working hours, but only if you document them. Without receipts and dates, you can’t prove the expense was legitimate during an audit.

The real damage isn’t the missed deduction-it’s the false cash flow picture. If you don’t track small expenses, your P&L reports show higher profit than you actually have. You make hiring or spending decisions based on fake profitability. One founder discovered that when she started photographing every receipt and uploading them, her actual profit dropped from $8,000 to $4,200 monthly. The difference was untracked expenses under $50.

Set a hard rule: photograph and upload every receipt the same day, no minimum amount. QuickBooks and Xero both accept photo uploads directly from your phone, which takes 30 seconds per expense. Over a year, this discipline saves thousands in deductions and prevents cash surprises.

Record keeping delays are insidious because they don’t feel urgent until tax season arrives. You tell yourself you’ll catch up next week, then next month, then next quarter. A CPA will charge premium rates to sort through this chaos. Worse, you can’t generate accurate financial reports while reconciliation is pending, which means you’re flying blind on cash flow and profitability. The IRS expects organized records within four years, and disorganized records can trigger audit penalties.

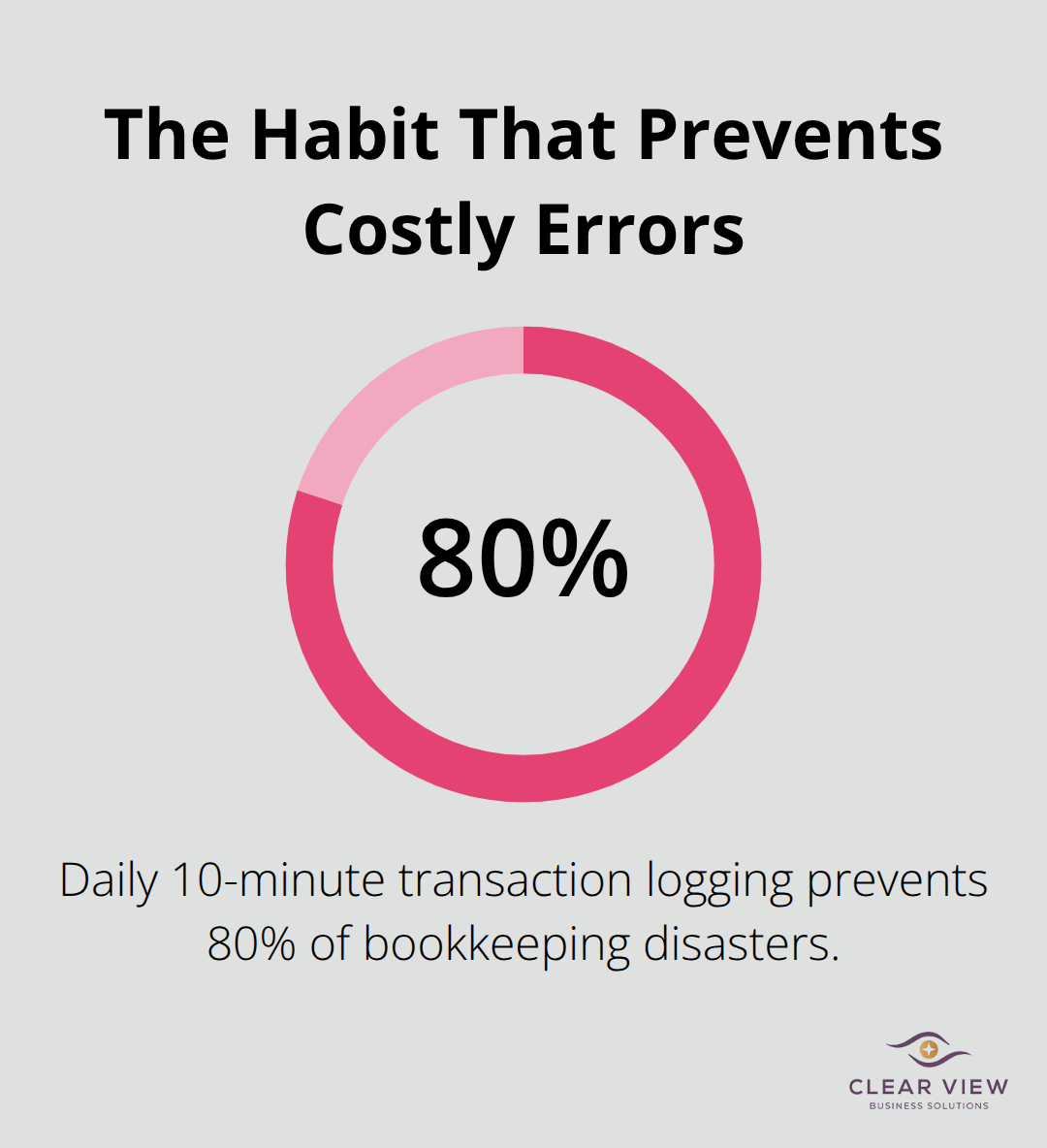

The solution is brutal simplicity: record transactions when they happen, not later. If you receive an invoice from a vendor, enter it into your accounting software within 24 hours. If a customer pays you, log the deposit the same day. Daily recording takes 5–10 minutes per day, not 10 hours once monthly. Most founders resist this discipline because it feels tedious, but tedious daily work beats frantic month-end scrambling. Set a calendar reminder for 4 PM each business day and spend those 10 minutes clearing your transaction backlog. This single habit prevents 80% of bookkeeping disasters that plague startups.

Organized startup bookkeeping prevents the cash flow crises that kill most new businesses. The practices in this checklist-separating accounts, recording transactions daily, reconciling monthly, and reviewing reports quarterly-aren’t optional extras. They’re the difference between founders who understand their financial reality and those who discover problems too late to fix them.

Many founders reach a point where startup bookkeeping demands more time than they can afford to spend. If you’re hiring employees, managing multiple revenue streams, or preparing for fundraising, that point arrives faster than you expect. Professional bookkeeping support isn’t a luxury at that stage-it’s a practical decision that frees you to focus on growth while someone else handles compliance and accuracy. We at Clear View Business Solutions work with startups to handle full-cycle bookkeeping, tax planning, and QuickBooks training so you maintain control without drowning in spreadsheets.

Start today with one habit: photograph and upload your first receipt. Visit Clear View Business Solutions to explore how we can support your financial foundation and build the systems that let your startup thrive.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.