As the year draws to a close, it’s time to focus on year-end tax planning tips that can significantly impact your financial health.

At Clear View Business Solutions, we understand the importance of optimizing your tax strategy to maximize savings and minimize liabilities.

This guide will walk you through key strategies to help you make the most of available deductions, time your income and expenses wisely, and leverage investment opportunities for a stronger financial future.

At Clear View Business Solutions, we know that maximizing tax deductions and credits is essential for optimizing your financial situation. Let’s explore some practical strategies to help you reduce your tax burden and keep more money in your pocket.

Many taxpayers miss out on valuable deductions simply because they’re unaware of them. If you’re self-employed, you can deduct a portion of your home office expenses, including utilities and insurance. The IRS allows a simplified method where you can deduct $5 per square foot of your home office (up to 300 square feet).

Another frequently overlooked deduction is for medical expenses. You can only deduct medical expenses that exceed 7.5% of your adjusted gross income, but this threshold is lower than many people realize. Keep track of all medical-related costs, including mileage for doctor visits and parking fees at medical facilities.

Different industries often have unique tax benefits. For example, if you work in construction, you might qualify for the Domestic Production Activities Deduction, which can reduce your taxable income by up to 9% of your qualified production activities income.

Teachers can deduct up to $300 for unreimbursed classroom expenses. This above-the-line deduction is available even if you don’t itemize.

Charitable giving not only helps worthy causes but can also significantly reduce your tax liability. Consider donating appreciated stocks instead of cash. You’ll avoid capital gains tax and can deduct the full fair market value of the stock if you’ve held it for more than a year.

For those over 70½, a Qualified Charitable Distribution (QCD) from your IRA can satisfy your Required Minimum Distribution (RMD) while excluding the amount from your taxable income. Each year, an IRA owner age 70½ or over when the distribution is made can exclude from gross income up to $100,000 of these QCDs. This strategy can be particularly beneficial if you don’t itemize deductions.

Tax credits are even more valuable than deductions because they directly reduce your tax bill dollar-for-dollar. The Inflation Reduction Act of 2022 introduced several new energy-related tax credits. For instance, you can receive up to $7,500 for purchasing a new electric vehicle or up to $4,000 for a used one (subject to income limits and other restrictions).

Homeowners can benefit from the Energy Efficient Home Improvement Credit, which offers a 30% tax credit (up to $1,200 annually) for energy-saving improvements like new windows, doors, or insulation.

Tax laws change frequently, and what worked last year might not be the best strategy this year. Our personalized approach means we can identify the most relevant deductions and credits for your unique situation, helping you navigate the complex world of taxes with confidence. Now, let’s move on to explore how strategic timing of income and expenses can further optimize your tax situation.

Timing your income and expenses strategically can significantly impact your tax liability. If you expect to be in a lower tax bracket next year, deferring income can be a smart move. For employees, this might mean delaying year-end bonuses until January. Self-employed individuals have more flexibility and can delay billing clients until late December, ensuring payment arrives in the new year.

Consider this example: If you’re a consultant expecting a $10,000 payment in December, pushing it to January could save you $2,200 in taxes if you drop from the 32% to 24% tax bracket. However, always consider your cash flow needs before deferring income.

Accelerating deductible expenses into the current year can lower your taxable income. This strategy is particularly effective if you anticipate being in a higher tax bracket this year compared to the next.

For instance, if you’re a small business owner, consider purchasing necessary equipment or supplies in December rather than January. In 2025, a Section 179 deduction may still be available to businesses that spend less than $4.38 million per year for equipment, potentially reducing your taxable income significantly.

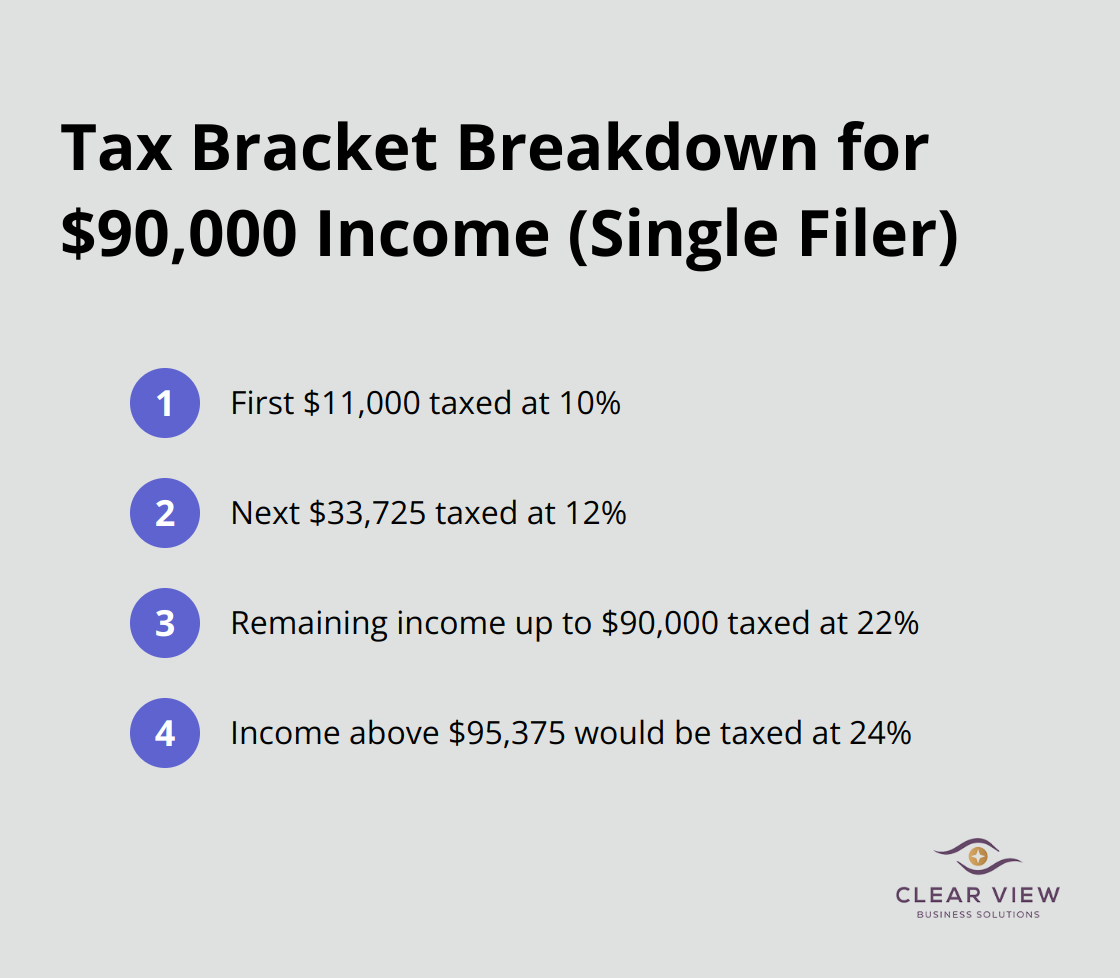

Understanding your current and projected tax brackets is essential for effective timing strategies. You pay tax as a percentage of your income in layers called tax brackets. As your income goes up, the tax rate on the next layer of income is higher.

For example, if you’re single and your taxable income is $90,000, you’re in the 24% bracket. But you’re not paying 24% on all $90,000. The first $11,000 is taxed at 10%, the next $33,725 at 12%, and so on. Only the income above $95,375 would be taxed at 24%.

While these strategies can be powerful, you must implement them correctly and in compliance with IRS regulations. The key is to plan ahead and seek professional guidance to ensure you’re making the most of these opportunities without running afoul of tax laws.

Professional tax advisors (like those at Clear View Business Solutions) use sophisticated tax planning software to model different scenarios and identify the most tax-efficient timing strategies for their clients. Their goal is to help you keep more of your hard-earned money while staying fully compliant with tax laws.

Now that we’ve explored the importance of timing in tax planning, let’s turn our attention to retirement and investment considerations that can further optimize your tax situation.

One of the most effective ways to reduce your current tax burden while securing your financial future is to maximize contributions to your retirement accounts. In 2025, you can contribute up to $23,500 to your 401(k) plan. If you’re 50 or older, you can make an additional catch-up contribution of $7,500, bringing your total to $31,000. These contributions are made with pre-tax dollars, which effectively lowers your taxable income for the year.

For Individual Retirement Accounts (IRAs), the contribution limit for 2025 is $6,500, with an additional $1,000 catch-up contribution for those 50 and older. If you haven’t maxed out your contributions for the year, consider doing so before December 31st to take advantage of the tax benefits.

A Roth IRA conversion can be a powerful tax planning tool, especially if you expect to be in a higher tax bracket in retirement. You will owe taxes on the money you convert, but you’ll be able to take tax-free withdrawals from the Roth IRA in the future.

This strategy can benefit you if your income is lower this year or if you have a year with significant deductions that can offset the tax impact of the conversion. For example, if you’re between jobs or have experienced a temporary dip in income, a Roth conversion could allow you to pay taxes at a lower rate than you might face in the future.

Tax-loss harvesting is when you sell investments at a loss and use those losses to offset gains in other investments. This strategy can help you reduce your tax liability.

For instance, if you have $10,000 in capital gains this year and sell underperforming stocks at a $7,000 loss, you can reduce your taxable gains to $3,000. Moreover, if your capital losses exceed your capital gains, you can use up to $3,000 of excess loss to offset ordinary income.

However, be cautious of the wash-sale rule. The IRS prohibits claiming a loss on a security if you buy the same (or a substantially identical) security within 30 days before or after the sale.

Charitable giving can allow you to support causes you care about while potentially reducing your tax burden. If you’re over 70½, consider making Qualified Charitable Distributions (QCDs) directly from your IRA to eligible charities. These distributions can satisfy your Required Minimum Distribution (RMD) without increasing your taxable income.

Another strategy is to bunch your charitable contributions. If your itemized deductions are close to the standard deduction threshold, try making two years’ worth of charitable contributions in a single year. This can push you over the threshold, allowing you to itemize and potentially reduce your tax liability more than if you had spread the donations over two years.

These strategies can significantly enhance your retirement savings, optimize your investment portfolio, and potentially reduce your tax burden. However, these decisions can be complex and should be tailored to your specific financial situation. A professional tax advisor can help you navigate these choices and create a personalized plan that aligns with your financial goals and tax situation.

Year-end tax planning tips can significantly reduce your tax burden and improve your financial health. A proactive approach to finances yields substantial benefits through maximizing deductions, strategic timing, and optimized retirement strategies. Your unique financial situation should guide your strategy, as what works for one person may not be the best option for another.

Clear View Business Solutions specializes in personalized tax planning for individuals and small businesses in Tucson. We offer services from ITIN setup and tax planning to full-cycle bookkeeping and IRS representation (our goal is to simplify your finances). Our team can help you navigate complex tax laws, ensure compliance, and maximize your tax benefits.

Don’t wait until the last minute to start your year-end tax planning. Taking action early allows more time to implement strategies effectively and can lead to better outcomes. Contact us today to review your financial situation and put these year-end tax planning tips into action.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2933 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.