Most business owners leave thousands of dollars on the table each year simply because they don’t know which deductions apply to them. Tax minimization isn’t about being aggressive with the IRS-it’s about understanding the legitimate strategies available to you.

At Clear View Business Solutions, we’ve helped countless entrepreneurs reduce their tax burden by implementing straightforward techniques that actually work. This guide walks you through the deductions you’re missing, the timing strategies that matter, and the business structure decisions that impact your bottom line.

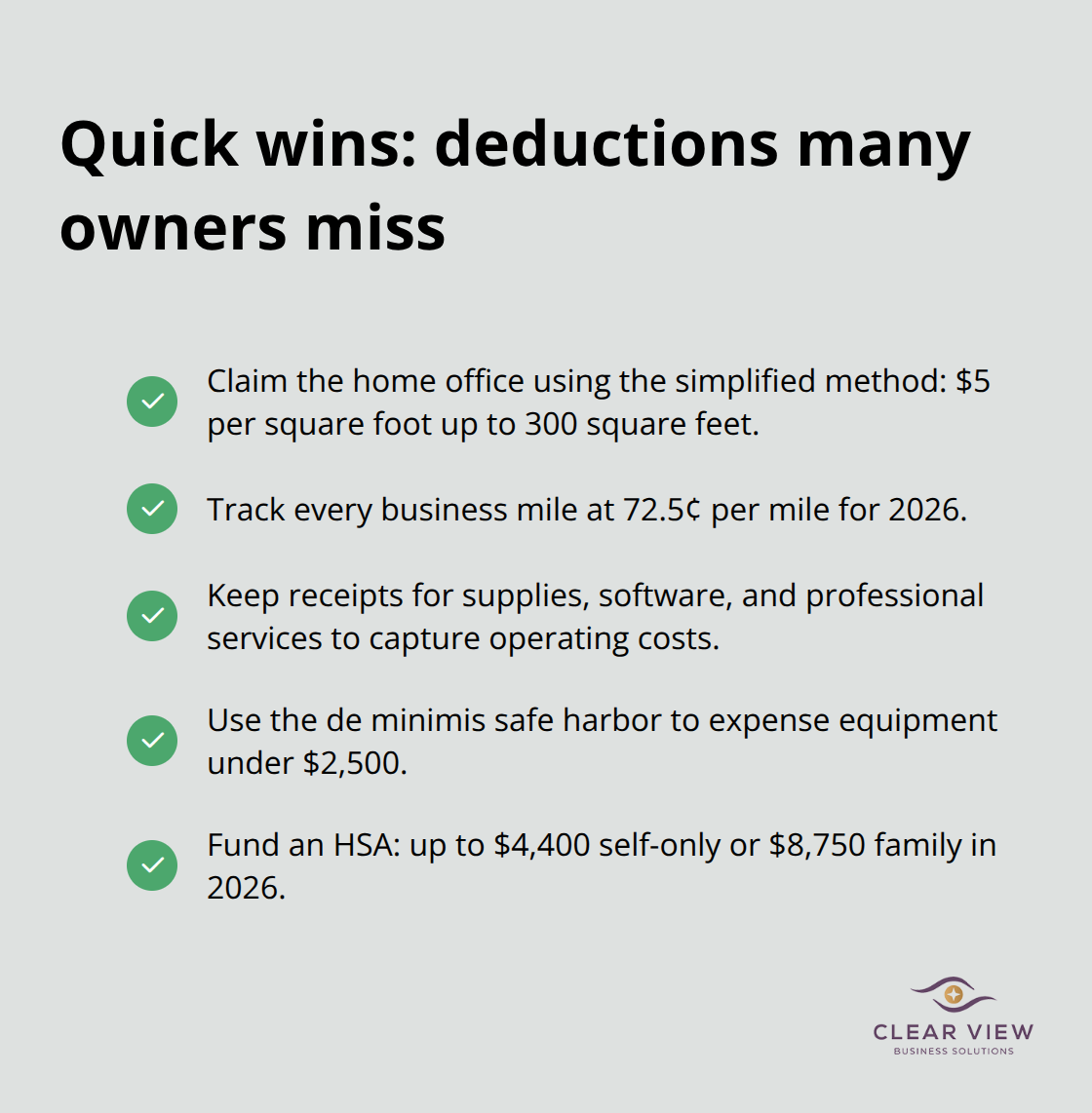

The home office deduction remains one of the most underutilized tax breaks available to self-employed workers. According to IRS guidelines, you can deduct a portion of your home expenses if you use a specific space regularly and exclusively for business. The IRS offers a simplified option with a standard deduction of $5 per square foot of home used for business, with a maximum of 300 square feet. Many owners skip this because they assume the deduction is too small to matter, but a modest home office generates meaningful annual tax savings.

Once you establish your home office, you can deduct business-related vehicle expenses. The standard mileage rate for 2026 is 72.5 cents per mile, which applies to trips between your home office and client meetings, supply runs, or other business destinations. Tracking mileage requires minimal effort-use a simple spreadsheet or a mileage app-yet most sole proprietors abandon this deduction entirely. If you drive 100 miles per week for business, that’s roughly 5,200 miles annually, translating to nearly $3,800 in deductions before considering actual vehicle costs like maintenance and insurance.

Business expenses form the foundation of tax minimization, yet many owners fail to categorize and document them properly. Office supplies, software subscriptions, professional services, equipment under $2,500, and client entertainment all qualify as deductible operating costs. The key is maintaining organized records and matching expenses to the correct tax year.

Medical and charitable contributions offer different leverage depending on your situation. If you’re self-employed and have high-deductible health insurance, a Health Savings Account allows you to contribute up to $4,400 for self-only coverage or $8,750 for family coverage in 2026, with every dollar reducing your taxable income while remaining available for medical expenses tax-free. Charitable contributions work best when you donate appreciated assets held longer than one year rather than cash. Donating appreciated stock or property lets you claim a deduction equal to the fair market value, subject to a 30 percent of AGI limit with five-year carryover, while completely avoiding capital gains tax on the appreciation. If you bought stock for $5,000 that’s now worth $15,000, donating it generates a $15,000 deduction and zero tax on the $10,000 gain. This strategy compounds when combined with donor-advised funds, which let you front-load multiple years of charitable giving into a single year for an immediate deduction, then distribute the funds to charities over time.

These deductions address immediate tax relief, but your real savings multiply when you coordinate them with strategic timing decisions throughout the year.

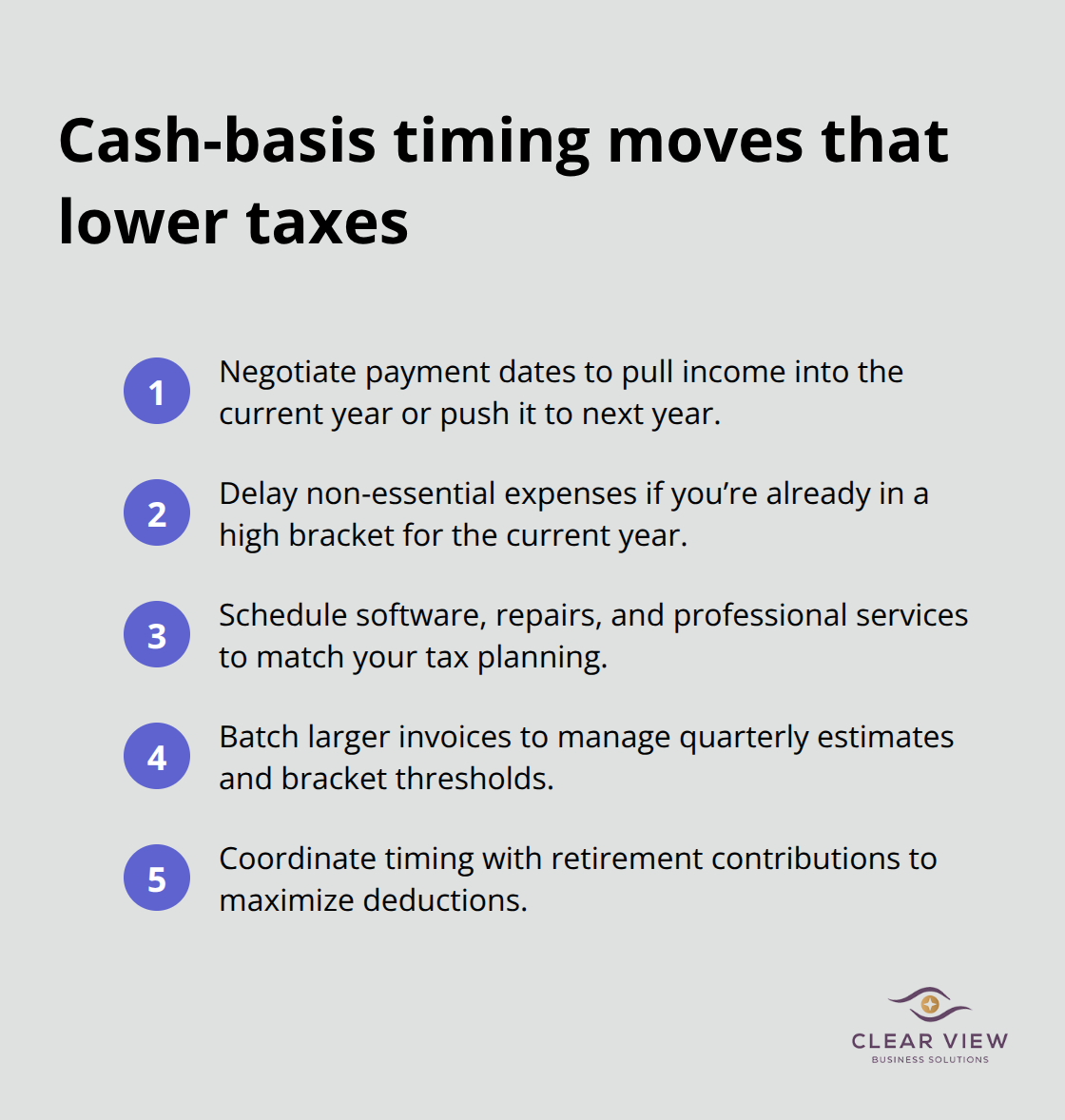

The strategic timing of income and expenses represents one of the most direct levers available to reduce your tax bill, yet most business owners treat it as an afterthought. When your business operates on a cash basis-meaning you report income when you receive payment and expenses when you pay them-you control the timing of both. A straightforward example: if you expect a $20,000 contract payment in early January, negotiate to receive it before year-end instead. That single shift moves $20,000 into the current tax year, potentially pushing you into a lower bracket or allowing you to absorb other deductions. Conversely, delay non-essential expenses into January if you’re already in a high bracket for the current year. Software licenses, equipment repairs, and professional services can often be scheduled strategically without affecting operations.

The IRS allows you to prepay certain expenses in advance, so paying your January insurance premium in December is legitimate tax planning. Beyond individual transactions, consider your overall income trajectory. If you anticipate lower income next year due to a planned sabbatical or market slowdown, accelerate income recognition this year and defer expenses when possible. The opposite strategy applies if you expect significantly higher income ahead-hold income in the current year and push expenses forward to offset gains in the higher-income year.

Retirement contributions deliver powerful results when properly sequenced. The 2026 contribution limits are straightforward: 401(k) contributions cap at $24,500 for those under 50 and $32,500 with catch-up contributions for those 50 and older, while traditional IRA contributions max at $6,500 ($7,500 if you’re age 50 or older). These contributions reduce your taxable income dollar-for-dollar, so maxing them out should be non-negotiable if you have the cash flow. The critical timing mistake is waiting until April 15 to fund your IRA for the prior year-you lose eleven months of tax-deferred growth. Fund retirement accounts throughout the year, especially if you’re self-employed and can adjust quarterly estimated tax payments downward once you’ve made contributions.

Tax credits work differently than deductions because they reduce your actual tax owed rather than your taxable income. The Earned Income Tax Credit, Child Tax Credit, and education-related credits are powerful, but many business owners miss them entirely because they focus only on deductions. Run the numbers in September, not April, to identify which credits apply to your situation. If you’re eligible for the Saver’s Credit-a refundable credit rewarding low- to moderate-income savers-contributing to a retirement account generates tax savings twice: once through the deduction and again through the credit itself. This compounding effect is why year-round planning beats last-minute scrambling, and it sets the stage for the structural decisions that can amplify your tax efficiency even further.

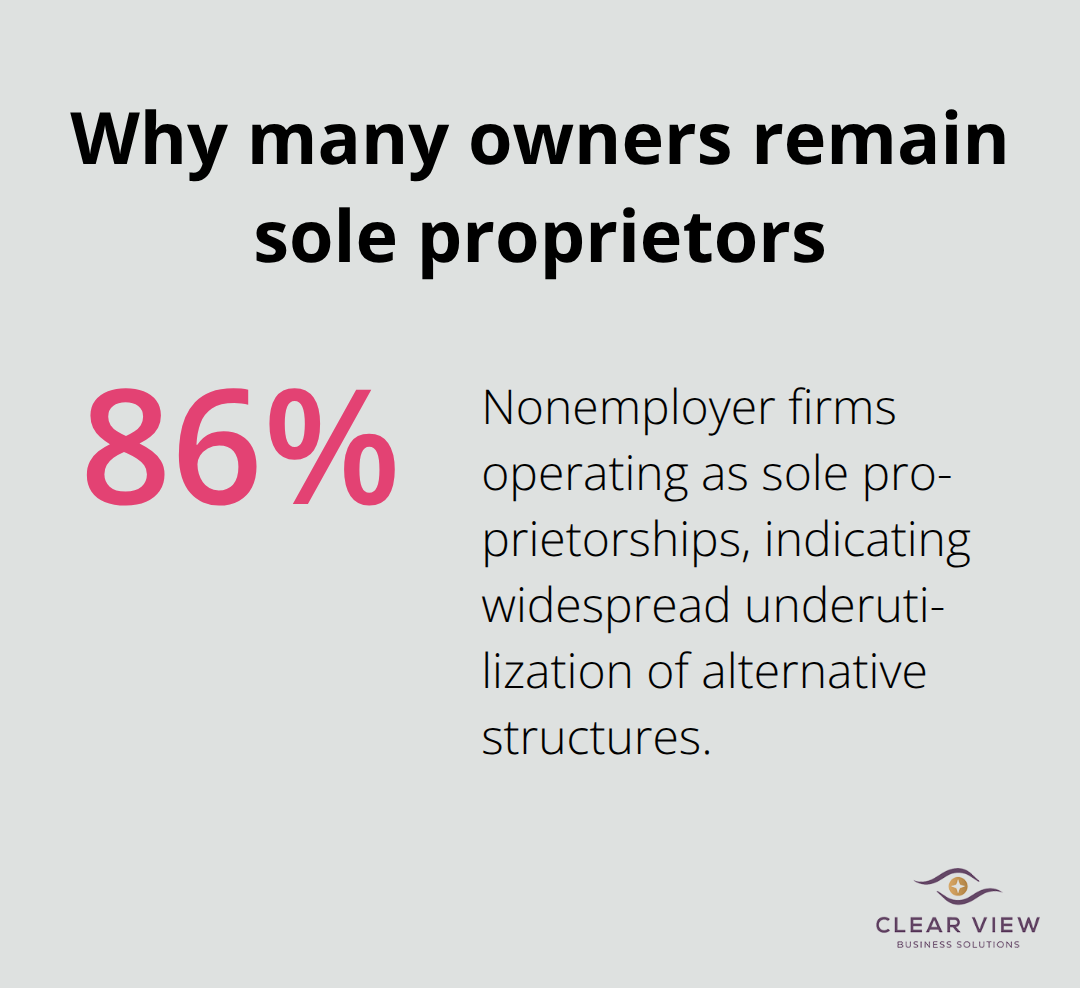

The entity structure you choose isn’t a legal formality-it’s one of the highest-leverage tax decisions you’ll make. Most sole proprietors pay self-employment tax on net profit, a burden that shrinks dramatically under different structures. An S corporation lets you split income into a reasonable salary subject to payroll taxes and a distribution that avoids self-employment tax entirely. If your business generates $100,000 in profit, you might pay yourself a $60,000 salary and take a $40,000 distribution. The salary triggers payroll taxes on the full amount, but the distribution avoids the self-employment tax hit, saving roughly $6,120 in self-employment tax annually. That’s real money that compounds year after year.

SBA data shows 86 percent of nonemployer firms operate as sole proprietorships, meaning the vast majority of business owners leave thousands on the table simply because they haven’t restructured. If your net profit exceeds roughly $75,000, switching to an S corporation almost always makes financial sense.

The administrative costs-filing fees, payroll processing, additional tax returns-typically run $1,500 to $3,000 annually, but the self-employment tax savings dwarf that expense for any business with meaningful profit. An LLC taxed as an S corporation gives you liability protection and the tax advantages of an S corp without the restrictions that traditional S corporations impose on ownership.

Many states allow pass-through entity elections, which convert SALT deductions into an entity-level tax that’s fully deductible under the new $40,000 SALT cap introduced by the One Big Beautiful Bill Act. This strategy requires careful modeling because the interaction between state elections, federal deductions, and your overall tax situation varies significantly based on income level and state residency. The timing of restructuring matters as much as the decision itself. If you’re mid-year and already approaching $75,000 in profit, waiting until January to switch to an S corp costs you an entire year of tax savings. Conversely, restructuring in December when you’re uncertain about next year’s income creates unnecessary complexity. The sweet spot is September or October when you have visibility into year-end profit and can make an informed decision with time to implement it before the calendar flips.

The wrong structure also creates unnecessary friction with retirement contributions and qualified business income deductions. Sole proprietors and partners can deduct contributions to SEP IRAs up to 25 percent of net profit, but S corporation owners face different rules that often result in lower contribution limits. The qualified business income deduction under Section 199A allows pass-through entities to deduct up to 20 percent of qualified business income, but the benefit phases out for high earners and carries complexity around W-2 wages and asset basis that S corporations must track meticulously.

If you’re already working with a CPA, discuss your structure annually, not just when you file taxes. Most business owners set their structure once and never revisit it, even though changes in income, state residence, or tax law can make restructuring beneficial. The cost of switching structures is minimal compared to the multi-year tax savings, but the decision requires professional guidance because it touches payroll, accounting, and state filings simultaneously. We help clients evaluate these decisions with concrete numbers, not theoretical concepts. We model the actual tax impact of each business structure for your specific situation, account for state-level implications, and time the transition to maximize first-year savings. The goal isn’t complexity-it’s identifying the structure that keeps the most of your income in your pocket.

Tax minimization works best when you treat it as a year-round discipline rather than a once-a-year scramble. The three pillars covered in this guide-capturing overlooked deductions, timing income and expenses strategically, and selecting the right business structure-compound when you coordinate them simultaneously. Most business owners implement one tactic sporadically, then wonder why their tax bill stays painful. The owners who see real results execute all three in concert.

Start with the easiest wins: claim your home office deduction, track business mileage, and audit your structure. If you operate as a sole proprietor with profit above $75,000, switching to an S corporation or LLC taxed as an S corporation typically saves thousands annually in self-employment tax. Mark September on your calendar to review year-end projections, identify applicable tax credits, and plan retirement contributions for the remainder of the year. The complexity increases when you layer in state-level SALT strategies, charitable giving coordination, and multi-year income forecasting-this is where professional guidance becomes essential.

We at Clear View Business Solutions help business owners implement these strategies with concrete numbers specific to your situation. Schedule a consultation to review your current tax situation and identify which strategies apply to you. Your tax bill for next year doesn’t have to match this year’s-but only if you plan for it now.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2025 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.