Most retirees leave thousands of dollars on the table each year through poor tax planning. The difference between a haphazard approach and a strategic one can mean tens of thousands of dollars over your retirement.

At Clear View Business Solutions, we’ve seen firsthand how creating tax-efficient retirement strategies transforms financial outcomes. This guide walks you through the specific accounts, withdrawal tactics, and positioning moves that actually reduce what you owe.

Traditional IRAs and 401(k)s remain the workhorses of tax-deferred retirement saving, but they come with a critical downside that most people overlook. Contributions reduce your taxable income today, which feels good on your current tax return, but every dollar you withdraw in retirement gets taxed as ordinary income. The IRS doesn’t care if you’re living on $40,000 or $140,000 annually-withdrawals from these accounts push you into higher tax brackets. At age 73, required minimum distributions force you to take money whether you need it or not, which can trigger unnecessary taxes on Social Security benefits and drive up Medicare premiums based on your modified adjusted gross income.

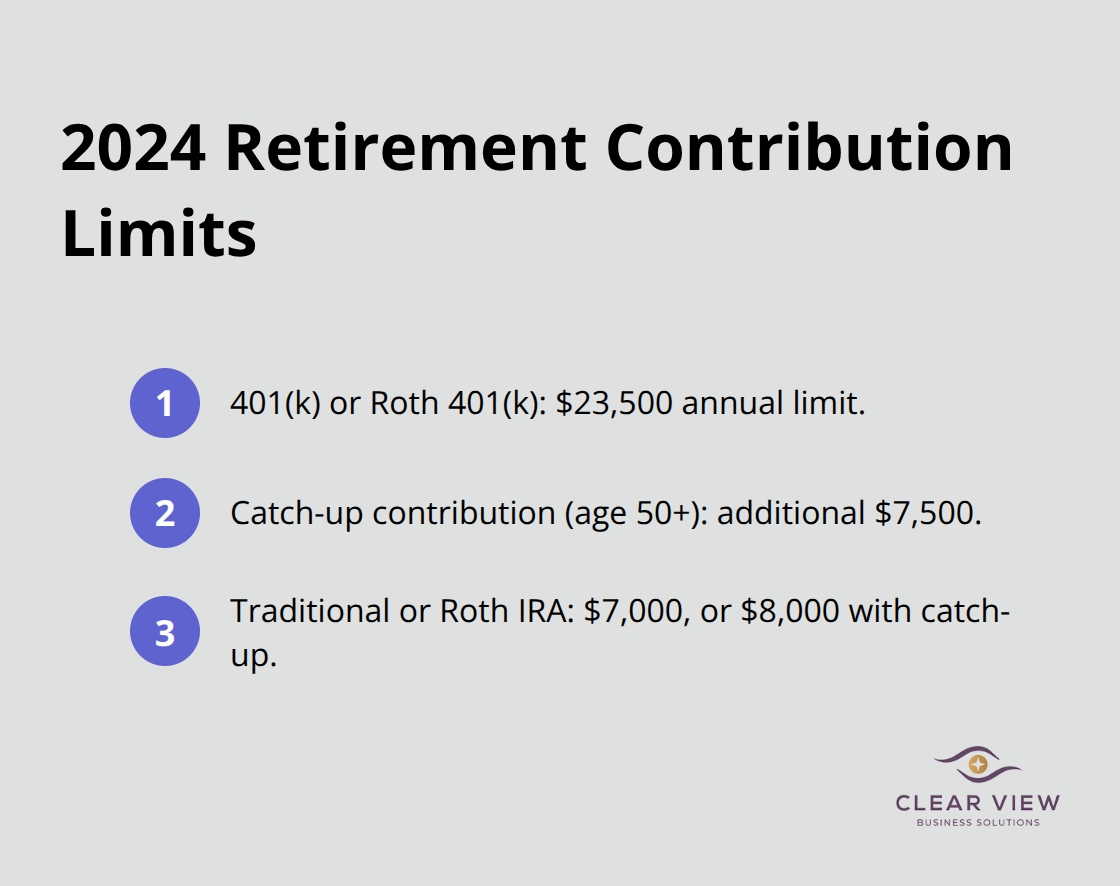

If you have a 401(k) through your employer, you’re limited to $23,500 in annual contributions for 2024, though catch-up contributions add another $7,500 if you’re 50 or older. Traditional IRAs cap out at $7,000 per year, or $8,000 with catch-up contributions. These accounts make sense when you’re in a high tax bracket now and expect to be in a lower one during retirement, but that scenario is increasingly rare.

Roth accounts flip the equation entirely, and they’re the superior choice for most people building wealth today. You pay taxes on contributions upfront, but qualified withdrawals in retirement are completely tax-free, and there’s no requirement to take money out at any age. The IRS doesn’t force distributions, so your money keeps compounding without triggering taxable events. Roth 401(k)s allow you to contribute the same $23,500 limit as traditional 401(k)s, while Roth IRAs cap at $7,000 annually but with income restrictions if your modified adjusted gross income exceeds $161,000 for single filers or $240,000 for married couples filing jointly in 2024.

For self-employed individuals, SEP-IRAs and solo 401(k)s offer dramatically higher contribution limits. You can set aside up to 25 percent of your net self-employment income in a SEP-IRA, or up to $69,000 in a solo 401(k) for 2024. The solo 401(k) option is particularly powerful because it allows both employee and employer contributions, and you can even make backdoor Roth conversions if your income exceeds Roth eligibility limits.

The real strategy isn’t choosing one account type-it’s building across all three buckets: taxable, tax-deferred, and tax-free. This diversification lets you manage your tax bracket in any given year and gives you flexibility that pure traditional or pure Roth approaches can never achieve. Once you understand which accounts work best for your situation, the next critical move is timing your withdrawals strategically to minimize what you owe the IRS.

Required minimum distributions force the issue at age 73, and ignoring them costs a penalty. The IRS calculates your RMD by dividing your prior year account balance by a life expectancy factor published in IRS tables, meaning the amount grows each year as you age. If you have multiple traditional IRAs, you can aggregate them for RMD calculation purposes and withdraw from whichever account makes the most sense, though 401(k) RMDs must be calculated separately for each plan.

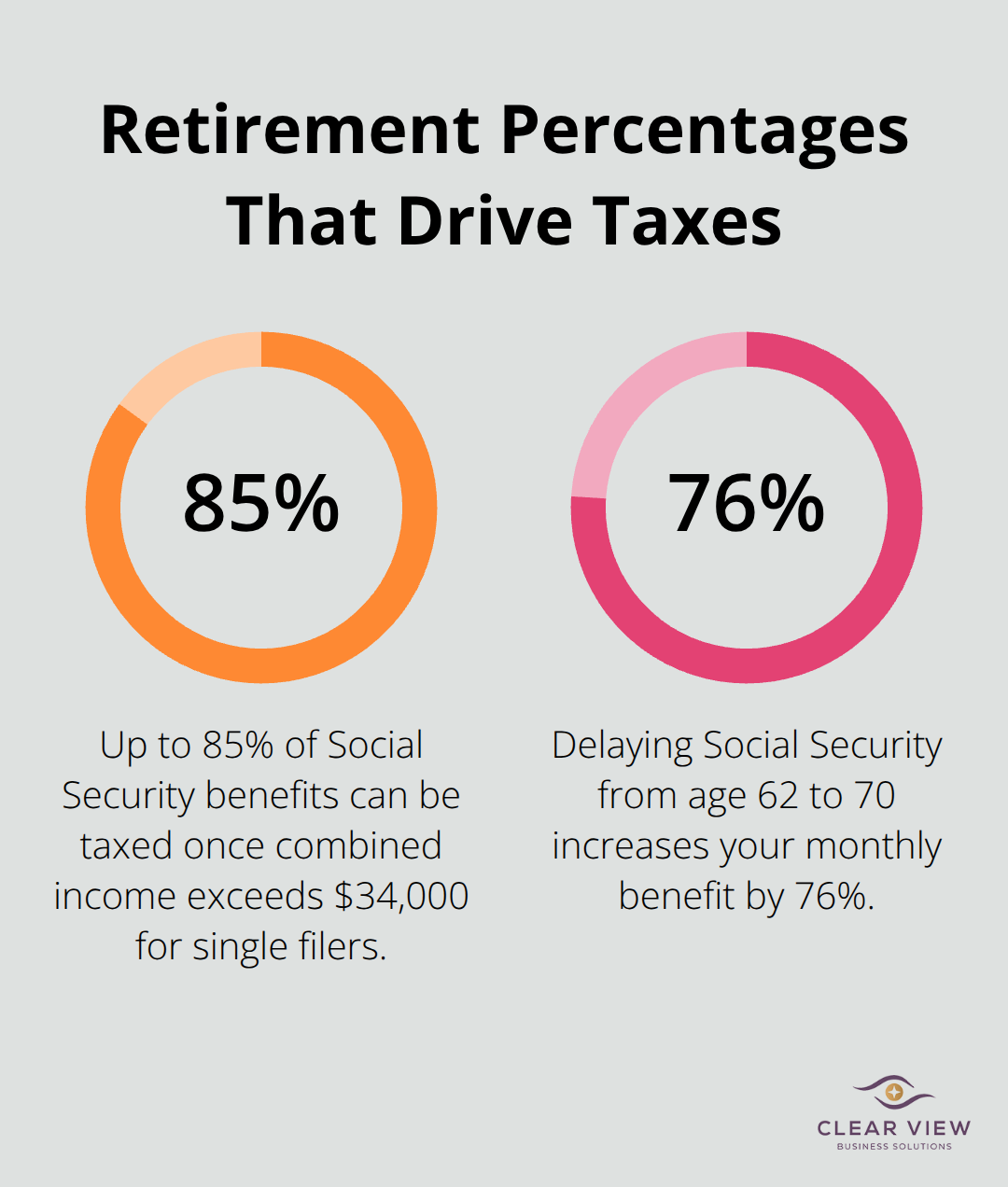

The real problem with RMDs isn’t the withdrawal itself but the timing. Forced withdrawals push income into higher brackets and trigger taxation of Social Security benefits under IRS rules that tax up to 85 percent of benefits once combined income exceeds $34,000 for single filers. These withdrawals also activate Medicare premium surcharges based on modified adjusted gross income with a two-year lookback period.

Taking a single large withdrawal in December creates tax damage that reverberates into the next two years through Medicare calculations.

The practical solution is proportional withdrawal sequencing across your three account buckets. Instead of draining taxable accounts first and forcing RMDs later, withdraw roughly the same percentage from each account type annually to smooth your tax bill and keep your modified adjusted gross income predictable. If you hold 40 percent of assets in taxable accounts, 35 percent in traditional retirement accounts, and 25 percent in Roth accounts, withdraw those same percentages each year rather than liquidating one bucket completely.

This approach reduces lifetime taxes compared to sequential withdrawal strategies because it prevents the mid-retirement tax bump when RMDs eventually force large traditional account withdrawals. You avoid the scenario where early years feel manageable, then suddenly at 73 you’re forced to take distributions that push you into a much higher bracket.

Social Security timing amplifies this benefit. Delaying benefits from age 62 to age 70 increases your monthly payment by 76 percent according to the Social Security Administration, and spreading those higher payments across a diversified withdrawal strategy means you’re less likely to push into the 85 percent taxation zone for benefits. Coordinate your withdrawal plan around when you claim Social Security rather than treating it as separate from your account strategy.

If you claim at 62 and immediately start large RMD withdrawals, you’ve locked in maximum taxation on benefits for two decades. Waiting until 70 to claim while executing proportional withdrawals from age 66 to 69 gives you control over your income level during the critical years before RMDs begin. This coordination between withdrawal sequencing and Social Security timing is where most retirees miss significant tax savings-and where the next layer of strategy comes into play.

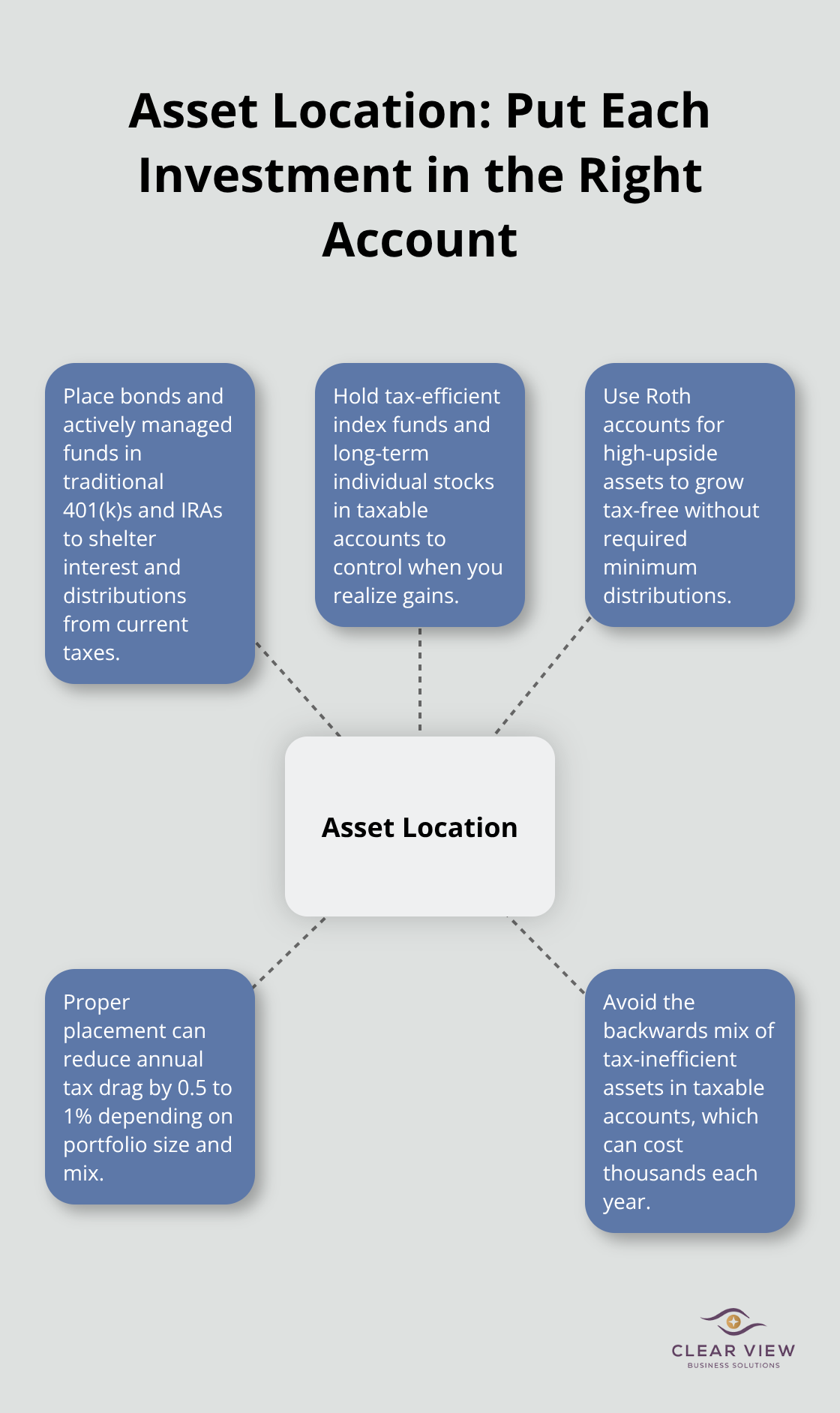

The account you choose matters far less than where you hold specific investments within your account structure. Tax-inefficient investments like actively managed mutual funds, REITs, and bonds produce constant taxable income through dividends, interest, or frequent capital gains distributions that you cannot avoid in a taxable account. Conversely, tax-efficient index funds and individual stocks held long-term create minimal taxable events and work better in taxable accounts where you control when to realize gains. The practical move is straightforward: place your bond holdings and actively managed funds inside traditional 401(k)s and IRAs where distributions never trigger current taxes, then hold index funds and growth stocks in your taxable accounts where you benefit from long-term capital gains rates for high earners according to IRS rules.

This asset location strategy alone can reduce your annual tax drag by 0.5 to 1 percent depending on your portfolio size and asset mix. A retiree with $500,000 split across accounts and holding bonds in taxable accounts instead of retirement accounts might unnecessarily pay $2,500 to $5,000 annually in avoidable taxes. Most people sabotage their tax efficiency by holding tax-inefficient investments in taxable accounts while keeping tax-efficient ones locked inside retirement accounts-a backwards approach that costs thousands in unnecessary taxes.

Rebalancing your portfolio creates a second tax trap that most people ignore until it’s too late. When your stock allocation drifts from 60 percent to 70 percent and you sell appreciated stocks to rebalance, you trigger long-term capital gains taxes that reduce the amount you reinvest. The solution is to rebalance inside retirement accounts where sales create no tax consequences, then rebalance your taxable accounts through new contributions rather than sales whenever possible.

If you must sell in taxable accounts, use tax-loss harvesting to offset gains. Sell losing positions and immediately purchase a similar but not substantially identical investment to maintain your allocation. The wash-sale rule prevents you from selling a security at a loss and repurchasing it within 30 days, but you can sell a total stock market index fund at a loss and immediately purchase a similar large-cap index fund to capture the loss without changing your exposure. This approach converts market downturns into tax deductions that offset capital gains from winners elsewhere in your portfolio or reduce ordinary income by up to $3,000 annually according to IRS limits, with unused losses carrying forward indefinitely.

The three decisions you make about accounts, withdrawal timing, and investment positioning determine whether you keep thousands of dollars or hand them to the IRS. Proportional withdrawal sequencing across taxable, tax-deferred, and tax-free buckets prevents the mid-retirement tax spike that forces unnecessary taxation on Social Security benefits and Medicare surcharges, while asset location reduces your annual tax drag by thousands without changing your overall portfolio. Tax-loss harvesting in down years converts market losses into deductions that offset gains elsewhere, and Social Security timing amplifies these benefits when you coordinate it with your withdrawal plan rather than treat it separately.

Most retirees struggle with creating tax efficient retirement strategies because coordinating RMD timing, Roth conversions, withdrawal sequencing, and Social Security claiming across multiple account types requires expertise in both mechanics and tax consequences. The complexity compounds when you factor in state taxes, health insurance costs, and legacy goals into your overall plan. We at Clear View Business Solutions help individuals and small business owners navigate this complexity through comprehensive tax planning and financial advisory services.

Your current account structure likely contains inefficiencies that cost you money every year. Schedule a consultation with us to review where you’re paying unnecessary taxes and build a personalized strategy that accounts for your specific situation, income sources, and retirement goals.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.