Estimated taxes are payments you make directly to the IRS throughout the year, rather than waiting until tax season. If you’re self-employed, a freelancer, or earn income without withholding, you likely owe them.

Missing these payments can trigger penalties that add up quickly. We at Clear View Business Solutions help business owners understand their tax obligations and stay ahead of deadlines.

Estimated taxes exist because the U.S. tax system operates on a pay-as-you-go basis. The IRS expects you to pay taxes throughout the year, not in one lump sum when you file. If you have income without automatic withholding, you need estimated tax payments to avoid penalties. To figure your estimated tax, you must estimate your expected adjusted gross income, taxable income, taxes, deductions, and credits for the year.

Self-employed individuals, freelancers, gig workers, business owners, and anyone earning investment income like interest, dividends, capital gains, or rental income typically fall into this category. If you’re an S corporation shareholder or partner in a partnership, you may also owe estimated taxes on your share of business profits that pass through to your personal return.

Three specific conditions allow you to avoid estimated tax payments entirely. First, you had zero tax liability in the prior year. Second, you were a U.S. citizen or resident alien for the entire prior year. Third, your prior tax year covered a full 12 months. If all three conditions apply, you’re exempt from the estimated tax requirement.

Additionally, if you have enough tax withheld from wages, pensions, or government payments, you can avoid estimated taxes through withholding adjustments instead. The IRS Tax Withholding Estimator helps you determine if increasing withholding through Form W-4 is a better strategy than making quarterly payments. Many employees mistakenly assume they must pay estimated taxes when they could simply adjust their W-4 to cover additional income from side work or investments.

Form 1040-ES is the primary tool for calculating and paying estimated taxes. You can use the worksheet in Form 1040-ES to figure your estimated tax and estimate the amount of income you expect to earn for the year. You’ll use the worksheet to calculate your total expected tax, then divide it into four equal quarterly payments unless your income varies significantly.

If you’re a nonresident alien, you’ll use Form 1040-ES (NR) instead. When you file your annual return, you report all estimated tax payments on Form 1040, line 26. If your income fluctuates during the year, you can use Form 2210 with the Annualized Income Installment Method to calculate unequal quarterly payments, which can reduce or eliminate underpayment penalties.

Farmers and fishermen have access to Form 2210-F, which provides special rules allowing them to delay payments or file later than standard taxpayers. Understanding which form applies to your situation sets the foundation for accurate calculations and timely payments-the next section covers exactly how to calculate those amounts and when the IRS expects them.

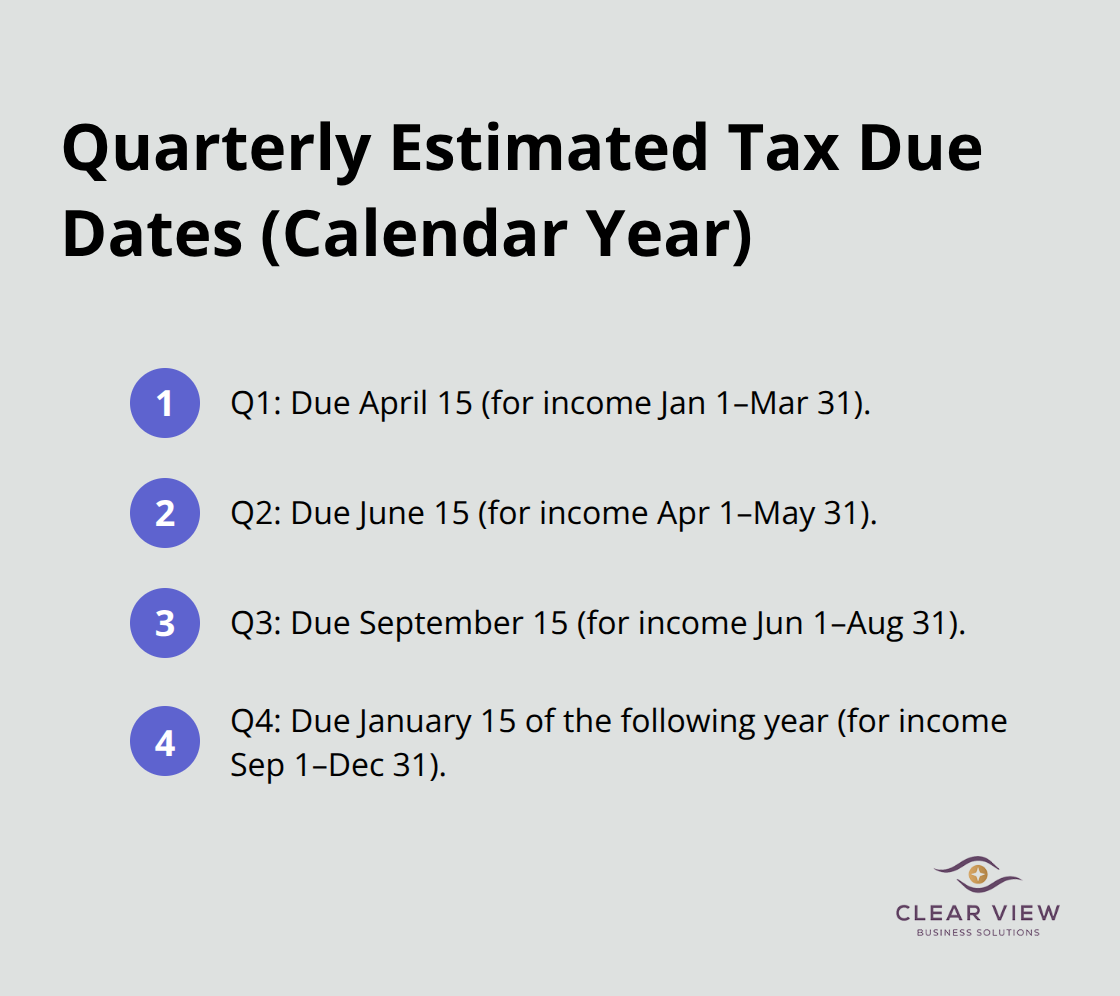

The IRS divides the tax year into four quarterly periods, each with a specific due date. For calendar-year taxpayers, Q1 runs January 1 through March 31 with a payment due April 15. Q2 covers April 1 through May 31, due June 15. Q3 spans June 1 through August 31, due September 15. Q4 runs September 1 through December 31, with payment due January 15 of the following year. If a due date falls on a weekend or holiday, you can pay on the next business day. The postmark date counts as your payment date if you mail a check with Form 1040-ES.

Many taxpayers treat these deadlines as flexible or assume they can catch up later. The IRS charges an underpayment penalty starting immediately after each missed deadline, even if you expect a refund when you file your annual return.

Start with Form 1040-ES to estimate your adjusted gross income, taxable income, and total tax for the year. Use your prior-year tax return as a starting point, then adjust for income changes and new tax laws. The form includes a worksheet where you calculate expected tax, then divide by four for equal quarterly payments.

Equal payments don’t always work, however. If your income is uneven (say you earn most revenue in Q4 or you received a large capital gain in one quarter), you can file Form 2210 with the Annualized Income Installment Method to calculate unequal quarterly payments. This approach can significantly reduce or eliminate underpayment penalties because the IRS penalizes only the amount underpaid during each specific quarter, not your total annual shortfall.

You can adjust your estimated tax payments after each quarter if your income projections change. If you overestimated, simply refigure your remaining quarterly payments and pay less. If you underestimated, increase the next quarter’s payment to catch up. This flexibility matters most for self-employed individuals and business owners whose income fluctuates.

You can pay estimated taxes online through Direct Pay on the IRS website, via the IRS2Go mobile app, or through EFTPS. You can schedule payments up to 365 days in advance at any interval that works for you, as long as you’ve paid enough by the end of each quarter. Scheduling automatic payments on or before each due date eliminates the stress of remembering deadlines and reduces the risk of penalties.

If you can’t pay the full amount by the due date, apply for a payment plan immediately. The IRS will still assess a penalty on the unpaid balance, but a formal payment plan shows good faith and can help reduce future penalties. Tracking your withholdings and estimated payments throughout the year proves essential. If you had taxes withheld from wages, pension income, or government payments, those credits count toward your estimated tax obligations and reduce the amount you need to pay quarterly. Understanding how these pieces fit together sets you up to recognize when you’ve underpaid and what penalties the IRS will assess-the next section explains exactly how the agency calculates those penalties and what safe harbor rules can protect you.

The IRS calculates underpayment penalties using three specific factors: the amount you underpaid, how long that underpayment lasted, and the agency’s published quarterly interest rate for underpayments. The penalty compounds quarterly, meaning the longer money remains unpaid, the more you owe. A taxpayer who underpaid by $2,000 for all four quarters faces a much larger penalty than someone who underpaid by $500 in just one quarter. The IRS will send you a notice if you owe the penalty, and interest accrues on top of it until you pay the balance in full.

The critical insight here is that the penalty applies even if you expect a refund when you file your annual return. Many business owners mistakenly believe they can underpay quarters one through three and make everything up with a massive Q4 payment. That strategy backfires because the IRS charges the penalty on each quarter’s shortfall independently, not on your overall annual tax liability.

You can avoid this penalty entirely by meeting one of two safe harbor tests. First, your withholding and estimated payments combined must equal at least 90 percent of your current-year tax. Second, you can pay 100 percent of your prior-year tax liability instead, or 110 percent if your adjusted gross income exceeded $150,000 in the prior year.

The number 100% seems to be not appropriate for this chart. Please use a different chart type. These thresholds provide a clear target for your quarterly payments and eliminate the penalty risk once you hit them.

Self-employed individuals with uneven income should use the Annualized Income Installment Method on Form 2210, which allows you to calculate smaller payments in low-income quarters and larger payments in high-income quarters. This approach directly addresses how the penalty works by ensuring you don’t underpay during any single quarter.

Farmers and fishermen operate under different rules entirely. If two-thirds of your gross income comes from farming or fishing, you can delay all estimated tax payments until January 15 of the following year or file your return by March 1 and pay the full amount then. These extended deadlines recognize the seasonal nature of agricultural income and provide meaningful flexibility that other taxpayers don’t receive.

Track your income and withholdings monthly, not quarterly, because this habit reveals underpayment trends before the quarterly deadline arrives. When circumstances beyond your control cause underpayment (such as casualty, disaster, or disability after age 62), the IRS may waive the penalty if you demonstrate reasonable cause and submit a signed explanation under penalty of perjury. If you relied on written IRS advice that turned out to be incorrect, you can also dispute the penalty with proper documentation.

Estimated taxes form the backbone of the U.S. pay-as-you-go tax system, and understanding them protects your business from costly penalties. The key takeaway is straightforward: calculate your expected annual tax using Form 1040-ES, divide it into four quarterly payments, and submit them by April 15, June 15, September 15, and January 15. Meeting the 90 percent safe harbor test on your current-year tax or 100 percent of your prior-year tax eliminates penalty risk entirely.

If your income fluctuates, use Form 2210 with the Annualized Income Installment Method to avoid overpaying in slow quarters and underpaying in strong ones. The IRS charges underpayment penalties based on how much you owe and how long it remains unpaid, with interest accruing quarterly. Adjusting your payments after each quarter gives you control-if income drops, reduce the next payment; if it surges, increase it.

We at Clear View Business Solutions help Tucson business owners and individuals navigate estimated taxes through comprehensive tax planning and accounting services. Our team handles the calculations, tracks your quarterly obligations, and keeps you compliant year-round. Visit Clear View Business Solutions to discuss your estimated tax strategy and discover how personalized tax planning maximizes your deductions while keeping penalties off the table.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2025 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.