Most startups fail because of poor financial management, not bad ideas. Getting your startup accounting right from the start prevents costly mistakes and keeps you compliant with tax laws.

At Clear View Business Solutions, we’ve seen firsthand how solid accounting practices separate thriving businesses from those that struggle. This guide walks you through the systems, tax strategies, and financial habits that actually work.

Your first move is separating personal and business finances completely. Open a dedicated business bank account before you do anything else-this single step eliminates the messiest accounting problem we see with early-stage founders. When personal and business transactions mix, you lose the audit trail that investors and lenders demand, and you waste hours reconciling accounts that should take minutes. The IRS also views commingled accounts as a red flag during audits. Most banks offer free or low-cost business checking for startups, so cost isn’t the barrier. What matters is opening the account in your business name, not your personal name, and committing to run every transaction through it from day one.

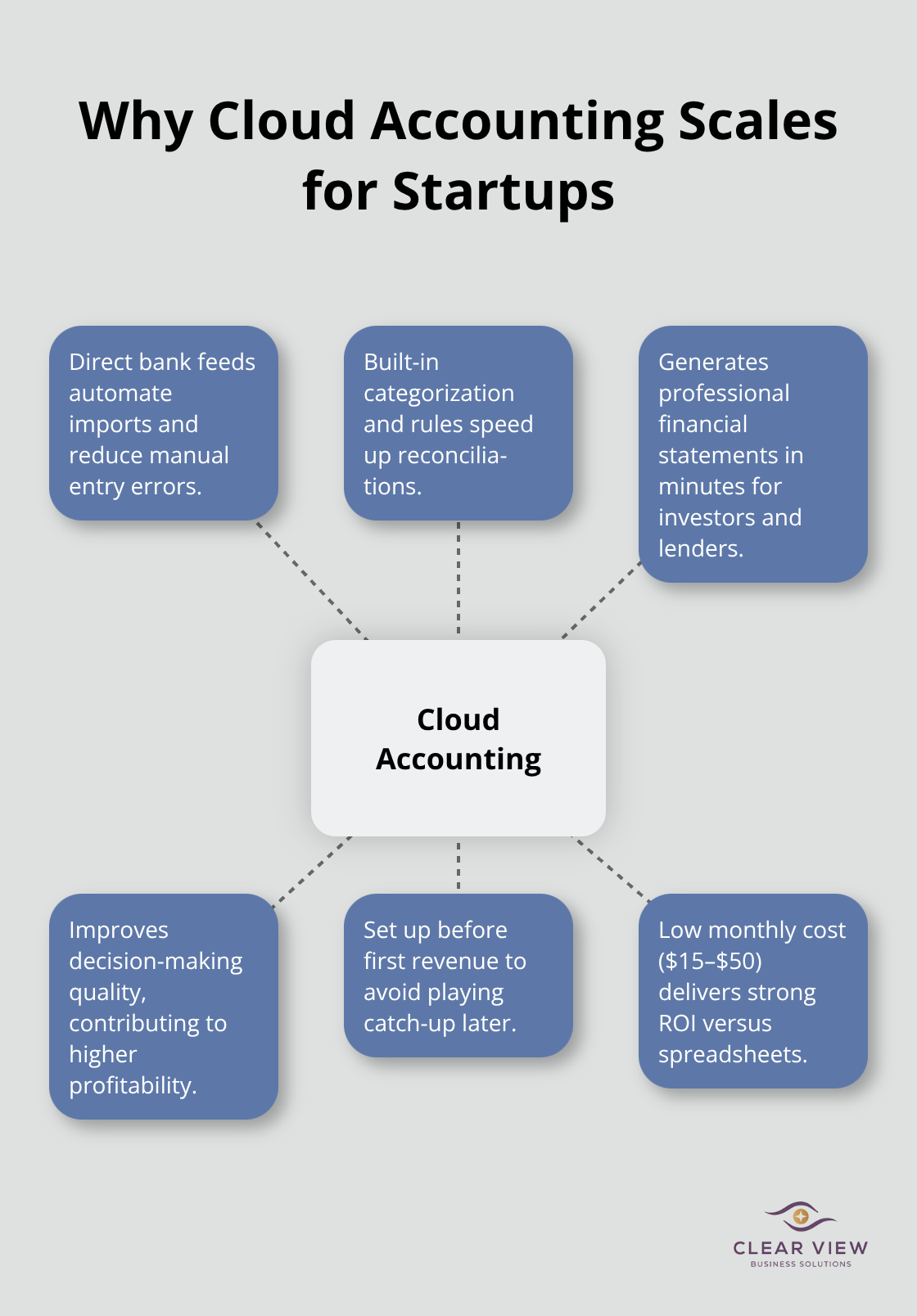

Next, implement accounting software immediately. This isn’t optional. Manual spreadsheets fail within months because they lack automation, create reconciliation nightmares, and won’t generate the financial statements investors expect. QuickBooks Online and Xero dominate the startup space for good reason-they integrate directly with your bank, automate transaction categorization, and produce professional reports in minutes. Cloud accounting users saw profit increases, which tells you the software itself drives better financial decisions.

Set up your account before your first revenue arrives so you’re never playing catch-up. The software costs $15 to $50 monthly, which is trivial compared to the time and accuracy gains.

Your chart of accounts determines what financial insights you can extract later. Don’t copy a generic template. Instead, build one that reflects how your specific business operates. If you’re a SaaS startup, you need separate accounts for subscription revenue, one-time fees, and refunds. If you’re a service business, you need accounts that track revenue by service line and client segment. Keep it lean-too many accounts creates categorization confusion and bloated reports. Most startups need 50 to 100 accounts maximum. The time you invest structuring this correctly early saves you from expensive reclassification work later (when you’re preparing for funding rounds or tax filings).

With your bank account, software, and chart of accounts in place, you’re ready to tackle tax planning obligations. Most founders delay tax planning until the end of the year, which costs them thousands in missed deductions and unnecessary liability. The next section walks you through the tax strategies that protect your runway and keep you compliant from day one.

Your business structure determines everything about your tax liability. Most founders choose between an LLC, S corporation, or C corporation without understanding the actual tax consequences. An LLC taxed as a sole proprietor is simple but exposes you to self-employment taxes on all profits. An S corporation requires more paperwork but lets you split income between W-2 wages and distributions, potentially saving 15% on self-employment taxes once you hit around $60,000 in annual profit. A C corporation is rarely the right choice for early-stage startups because of double taxation. The structure you pick today affects your quarterly tax payments, your filing deadlines, and your ability to attract investors. If you’re uncertain, consult a CPA before filing your first business tax return, not after. The $300 to $500 investment in professional guidance prevents thousands in correctable errors that become expensive to fix retroactively.

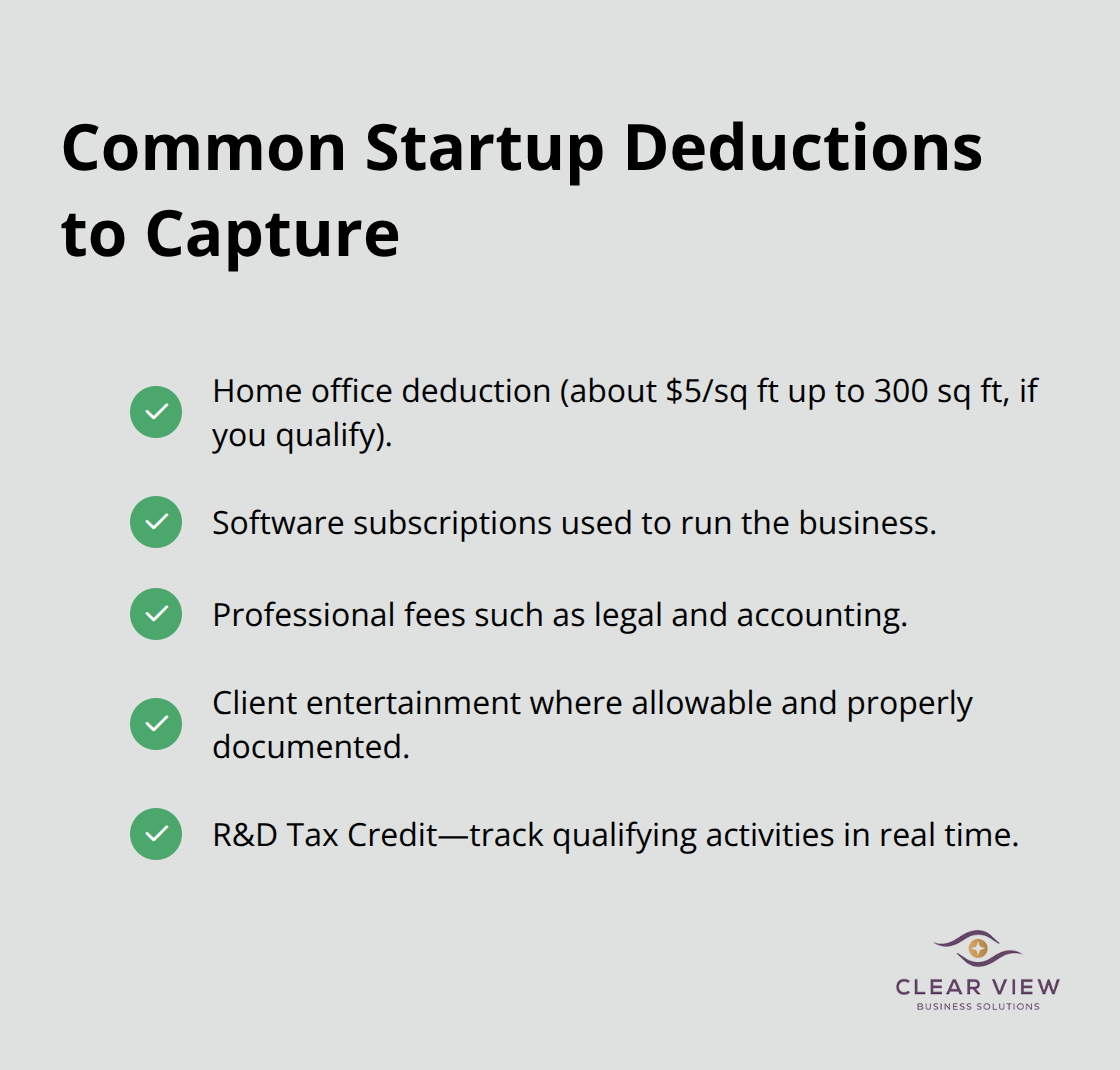

Most founders treat expense tracking as a year-end chore, but the IRS expects contemporaneous records. You must document every deductible expense the moment it occurs, not three months later when you’re scrambling before tax season. Capture receipts digitally using your accounting software’s mobile app, photograph credit card statements, and link everything to your chart of accounts. The most commonly missed deductions for startups include home office space (if you qualify, this runs roughly $5 per square foot annually up to 300 square feet), software subscriptions, professional fees, and client entertainment. The R&D Tax Credit represents another major opportunity that most early-stage founders ignore entirely. If your startup develops new processes, software, or products, you likely qualify for credits worth 10% to 15% of qualified R&D spending. The IRS allows you to carry credits back one year or forward 20 years, so even unprofitable startups can eventually claim them.

You should track your qualifying activities in real time rather than reconstruct them later.

Quarterly estimated tax payments become mandatory once your startup generates profit. Waiting until April to pay your annual tax bill triggers penalties and interest that compound quickly. The IRS sets deadlines on April 15, June 15, September 15, and January 15 for the following year. You calculate your expected annual profit, divide by four, and submit each quarter using IRS Form 1040-ES or your state’s equivalent. If you underpay by more than $1,000, penalties apply even if you have a refund coming at year-end. Many founders ignore this requirement thinking they’ll settle up annually, then face a surprise bill with penalties that eats into their runway. You should set calendar reminders for each deadline and treat these payments as non-negotiable business expenses.

With your business structure locked in, expenses tracked, and quarterly taxes scheduled, you now have the tax foundation that protects your business. The next section shows you how to build on this foundation by monitoring your actual financial performance through regular reporting and using that data to make smarter growth decisions.

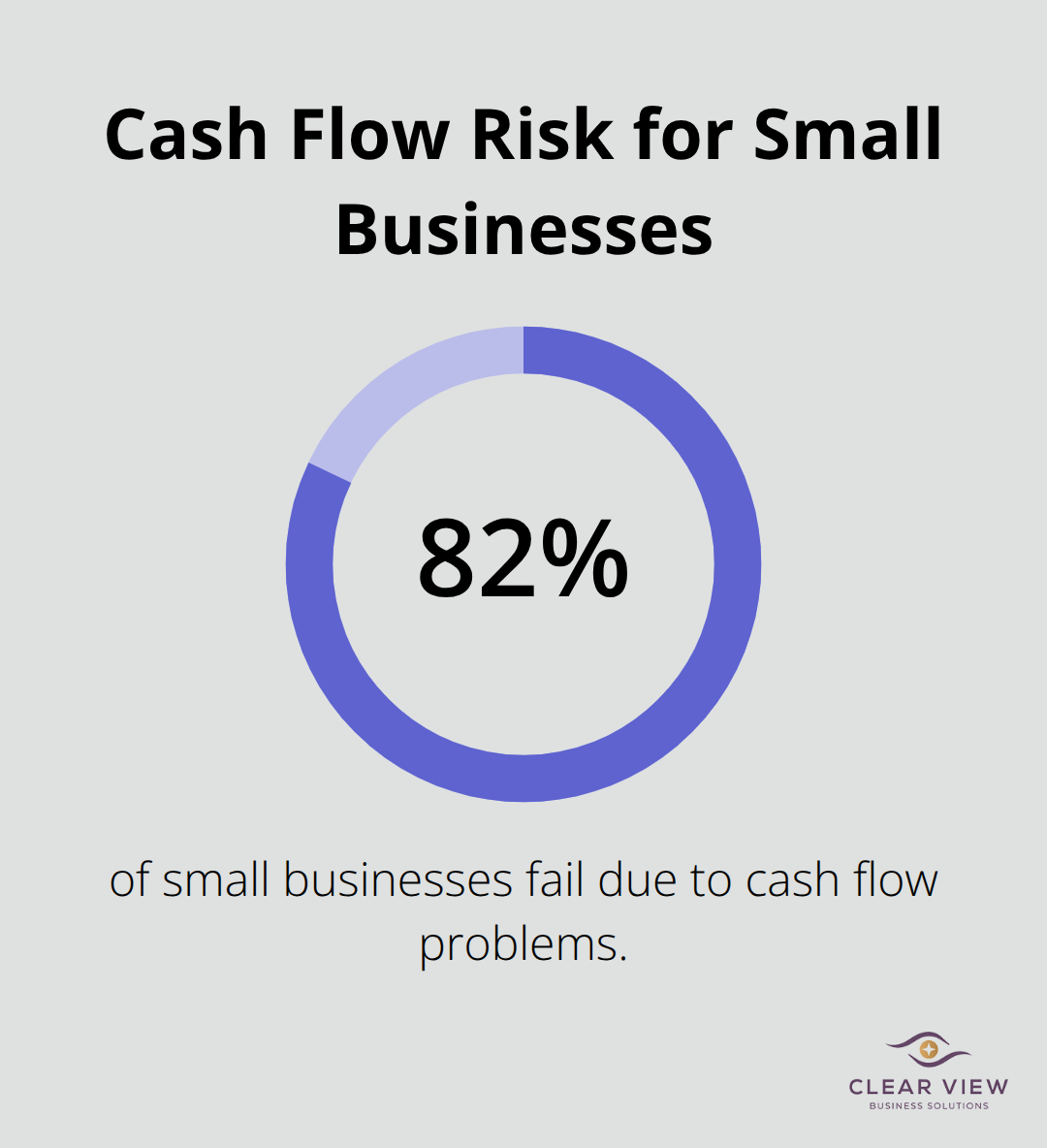

Cash flow is the single metric that determines whether your startup survives the next six months. A profitable business on paper can run out of money and fail if you neglect cash flow management. You need to know your cash position every week, not monthly. This means tracking when money actually enters and leaves your bank account, separate from when you recognize revenue or expenses on your profit and loss statement. 82% of small businesses fail due to cash flow problems, which underscores why this matters more than profit margins or growth rates.

Open your accounting software each Monday morning and review your bank balance against your projections. If actual cash trails projections by more than 10%, you need to act immediately-accelerate customer collections, negotiate extended payment terms with vendors, or reduce discretionary spending. Most founders treat cash flow as something to monitor quarterly alongside tax filings. That approach guarantees you’ll miss the warning signs until it’s too late.

The income statement shows you whether you’re profitable, but the cash flow statement shows you whether you’ll survive. These are completely different things. A startup can be profitable and insolvent simultaneously if customers pay you 60 days after invoicing while you pay suppliers in 30 days. Your accounting software should generate a cash flow forecast automatically, projecting inflows and outflows for the next 13 weeks. Review this forecast weekly and update it with actual results. If your forecast shows cash running below $30,000 in any month, start raising capital or cutting expenses now, not when the crisis hits.

Your profit and loss statement reveals which parts of your business actually generate money and which parts drain it. Pull this report on the same day each month and spend 30 minutes analyzing what changed from the prior month. Look at your gross margin first-for SaaS startups, this should be between 70% and 90% according to industry benchmarks. If your gross margin drops, you’re either paying too much to deliver your product or your pricing is too low. Neither situation fixes itself.

Compare your operating expenses to revenue and calculate your burn rate, which is your monthly cash outflow. If you burn $50,000 monthly and have $200,000 in the bank, your runway is four months. This calculation is non-negotiable for any founder seeking investment. Track your customer acquisition cost by dividing total sales and marketing spend by the number of new customers acquired that month. If your CAC is $500 and your average customer lifetime value is $400, you’re losing money on every customer you acquire. This is a business model problem, not a marketing problem, and it needs fixing before you scale.

Most founders ignore the P&L until tax season, treating it as a compliance document rather than a decision-making tool. Daily transaction recording, monthly bank reconciliation, and regular financial report generation are essential tasks for maintaining organized finances. Set a calendar reminder for the 5th of each month and review it immediately.

Financial metrics should drive every major decision you make about hiring, pricing, and expansion. If you’re considering hiring a new salesperson at $80,000 annually, your financial statements should tell you whether you can afford it. Calculate how many additional customers that salesperson needs to acquire to cover their salary and benefits. If your CAC is $500 and average customer value is $3,000, that salesperson needs to acquire 32 new customers annually just to break even on their cost. If your sales team currently closes 20 customers per year, hiring a second salesperson should increase your total to 40, creating a net gain of 8 customers. That’s not enough margin for comfort. You need the new hire to generate at least 40 additional customers to justify the expense.

This is where scenario planning becomes essential. Your accounting software should let you build multiple financial models showing what happens if you hire that salesperson versus if you invest the same $80,000 in paid advertising instead. Model these scenarios quarterly and compare actual results to your projections. When reality diverges from your model, investigate why. Did customer acquisition cost spike? Did churn accelerate? Did pricing resistance emerge? These deviations are information.

Most founders make hiring and spending decisions based on intuition or competitive pressure rather than their actual financial capacity. Integrating tax considerations into your business planning can lead to better decision-making and improved financial outcomes. If a marketing channel generates customers at $300 CAC but another channel costs $800 CAC, you should shift spending toward the cheaper channel immediately. Financial data removes emotion from these decisions and keeps you focused on what’s working.

Startup accounting isn’t a task you complete once annually-it’s the operating system that keeps your business running. The practices we’ve covered form the backbone of every successful startup we work with at Clear View Business Solutions. Separating finances, selecting the right software, tracking expenses in real time, and monitoring cash flow weekly aren’t optional tasks. They’re the difference between founders who know exactly where their business stands and those who discover problems too late to fix them.

The financial data you collect today becomes the foundation for every decision you make tomorrow. When you decide whether to hire, expand into a new market, or adjust pricing, your accounting records provide the evidence you need. Without clean, accurate data, you’re guessing-with it, you’re strategizing. Many founders try to handle startup accounting alone in the early stages, but this approach breaks down quickly as complexity increases (payroll taxes, sales tax nexus requirements, and investor-ready financial statements all demand expertise most founders lack).

A qualified accounting partner catches mistakes before they become expensive problems and identifies tax deductions you’d miss. We at Clear View Business Solutions specialize in helping startups build financial foundations that support growth. Visit Clear View Business Solutions to learn how we can strengthen your financial foundation and help you make informed financial decisions.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2933 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.