Most people have no idea what their net worth actually is. They don’t know how much they earn versus spend, and they certainly don’t have a plan for the future.

At Clear View Business Solutions, we’ve seen firsthand how financial planning transforms lives. The three core steps in this guide will help you take control of your money and build real wealth.

Most people never calculate their net worth, yet this single number reveals your true financial position. Your net worth equals total assets minus total liabilities-it’s your financial baseline. Gather bank statements, investment account statements, property valuations, and vehicle titles. Include savings accounts, retirement accounts, real estate equity, and personal items of significant value. The Federal Trade Commission recommends reviewing your credit report annually through your free credit report access to catch errors or hidden debts that might drag down your actual financial picture. Don’t be discouraged if liabilities exceed assets initially. Many people start with negative net worth and still build substantial wealth over time through consistent effort.

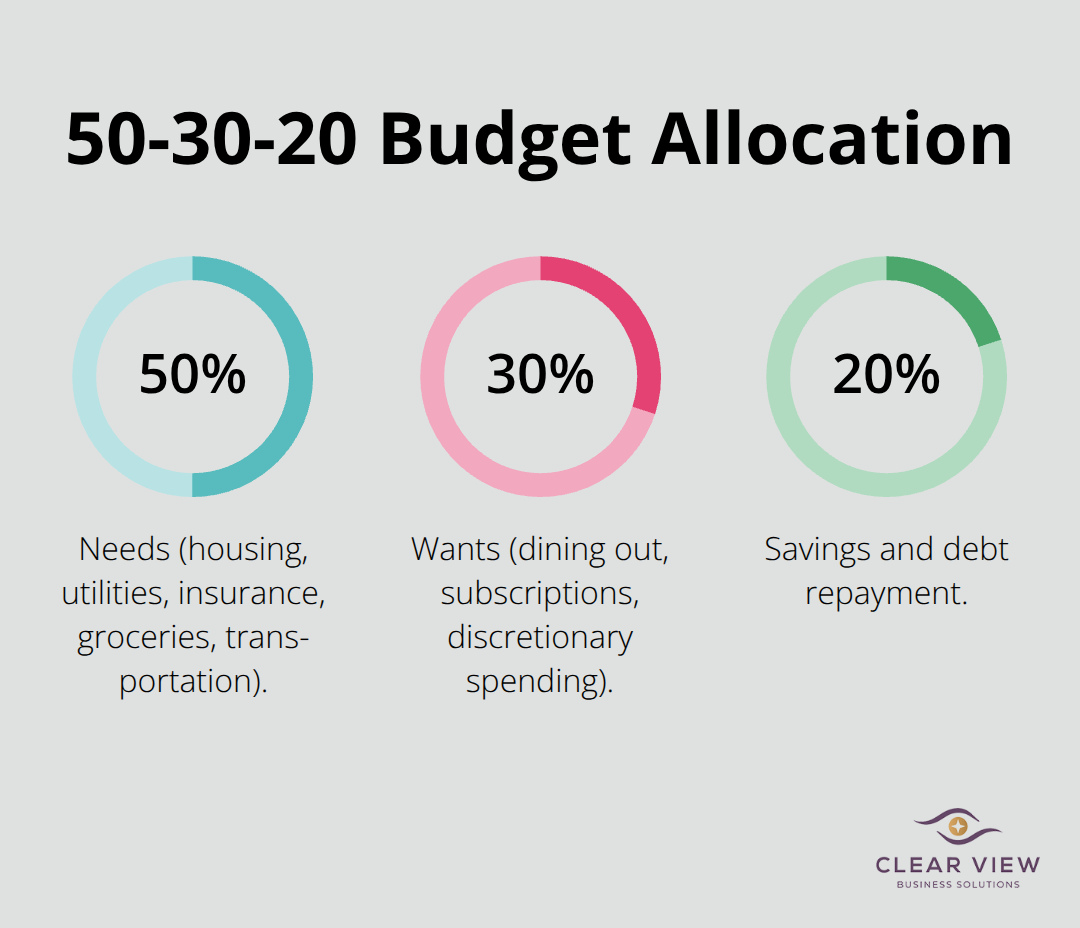

Income and expenses tell the real story of your financial health. Write down every source of income, including your salary, side work, rental income, or benefits. If you’re paid irregularly, take last year’s total income and divide by 12 to estimate monthly figures. Next, list all monthly expenses: housing, utilities, insurance, groceries, transportation, debt payments, and discretionary spending like dining out or subscriptions. The 50-30-20 rule recommends putting 50% of your money toward needs, 30% toward wants, and 20% toward savings and debt repayment. However, adjust these percentages based on your actual situation. Someone in a high cost-of-living area might need 60% for essentials, while someone debt-free might prioritize 25% savings.

Subtract total monthly expenses from income. If the result is negative, you’re spending more than you earn, and that’s your immediate priority to fix. Consider a bookkeeping file evaluation to gain clarity on your spending patterns and identify areas for improvement.

Not all debt is equal. A mortgage that builds home equity differs fundamentally from credit card debt charging 14–25% annual interest. Review each debt and note the interest rate. High-interest debt is your enemy because it compounds against you monthly. Paying down credit cards before investing typically makes financial sense since the guaranteed return from eliminating 20% interest exceeds most investment returns. However, debt under 6% interest might warrant different treatment. Calculate your total monthly debt payments and see how much of your cash flow goes toward obligations versus building wealth. This clarity reveals whether debt is manageable or consuming resources needed for an emergency fund and retirement savings. Once you understand your complete financial picture-assets, liabilities, income, and expenses-you can move forward with confidence to set meaningful goals that actually fit your situation.

Goals without specifics are just wishes. Instead of saying you want to save more, commit to concrete targets with dollar amounts and deadlines. Write down the exact dollar amount needed for each goal and the precise date you want to achieve it. For example, instead of saving for retirement, commit to accumulating $500,000 by age 65. This clarity forces you to calculate how much you need to save monthly and whether your current income supports that timeline.

Short-term goals typically span one to two years and include items like building an emergency fund of three to six months of living expenses, paying down high-interest credit card debt, or saving for a car. Medium-term goals cover three to ten years and might involve saving for a home down payment, funding education, or eliminating a mortgage faster. Long-term goals extend beyond ten years and usually center on retirement savings or wealth building. The key difference between people who achieve financial stability and those who don’t is specificity. Research shows that having a written plan with measurable targets increases the likelihood of reaching your goals substantially compared to vague intentions.

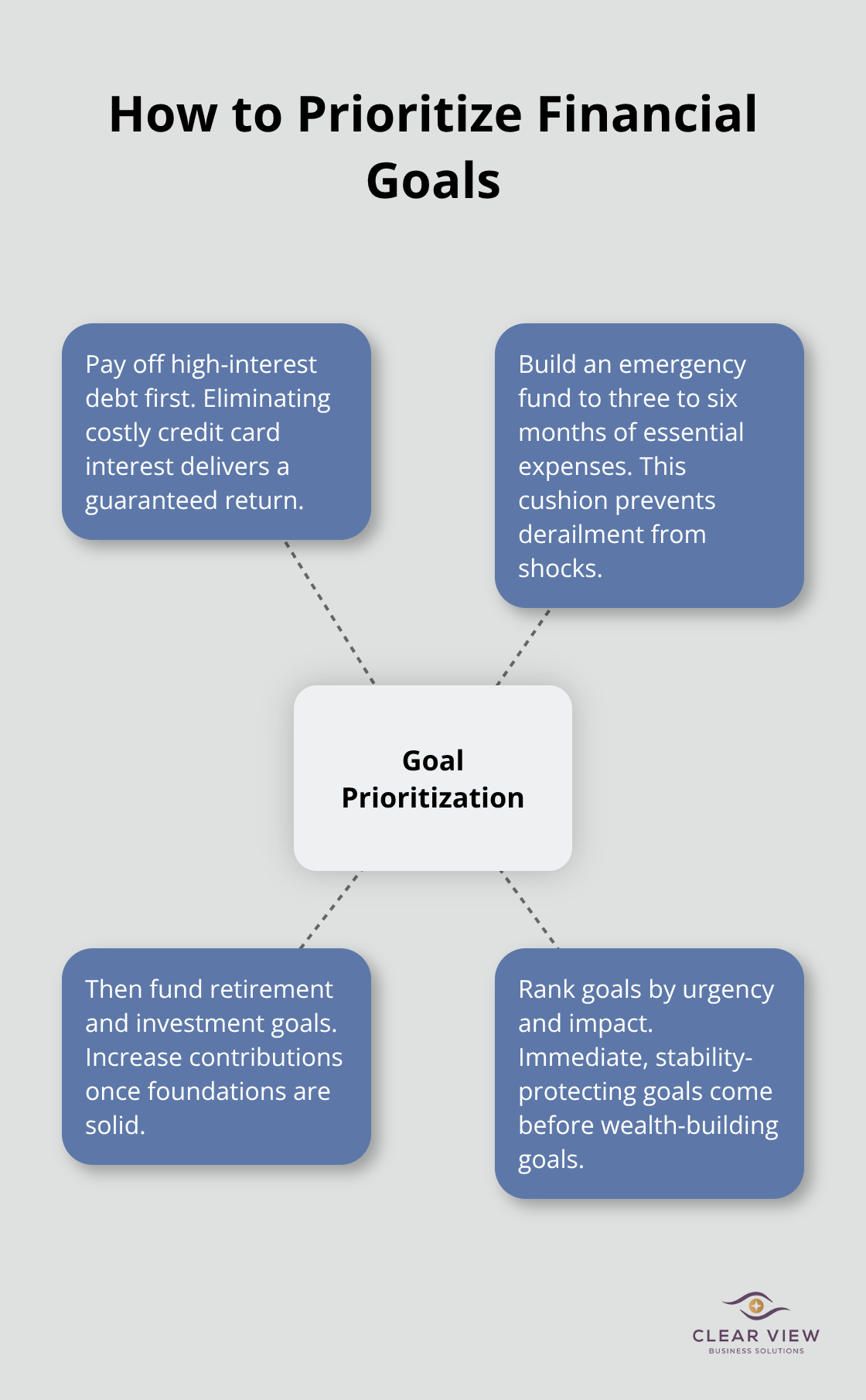

Prioritization separates realistic planning from fantasy. If you have five goals competing for limited cash flow, you’ll accomplish none of them. Start by addressing high-interest debt first because paying off 20% credit card interest delivers a guaranteed return that beats most investments. Once high-interest debt is controlled, build your emergency fund to three to six months of essential expenses. Only after these foundations are solid should you aggressively fund retirement accounts and investment goals.

This sequencing matters because an unexpected job loss or medical bill will derail everything if you lack an emergency cushion. Use a simple ranking system based on urgency and impact. Goals that protect your financial stability come before goals that build wealth. Goals with immediate deadlines take precedence over distant ones (for instance, paying off a car loan due next year ranks higher than saving for a vacation five years away).

If you’re unsure how to sequence competing priorities, a financial advisor can help you stress-test your plan against realistic scenarios like income loss or market downturns and recommend the most effective allocation of your available funds. This professional perspective prevents costly mistakes and accelerates your progress toward financial stability. With your goals clearly defined and prioritized, you’re ready to translate them into action through a realistic budget and investment strategy.

A budget without execution is just paperwork. Start by tracking every dollar you spend for one month without changing anything-this reveals your actual spending patterns, not what you think you spend. Most people discover they waste 10–15% of income on subscriptions, dining out, and impulse purchases they don’t remember making.

Once you see the real numbers, build your monthly budget by listing fixed expenses like rent or mortgage, utilities, and insurance, then add variable expenses like groceries and gas. The 50/30/20 rule is a simple way to plan your budget, but adjust it to your situation. If you earn $4,000 monthly and have $2,200 in housing costs, you’re already at 55% on essentials before food or transportation. Accept this reality and find cuts elsewhere rather than pretending you can live on 50%.

Set aside 20% of your income for savings and debt repayment first, before you spend on wants. This reversal-paying yourself first instead of saving leftovers-changes everything because you’ll actually build the cushion you need instead of discovering at month-end that nothing was left.

Your emergency fund is non-negotiable, and most people severely underestimate how much they need. Try for three to six months of essential living expenses in a high-yield savings account earning 4–5% annual interest. If your essential monthly expenses total $3,000, your target is $9,000 to $18,000. This sounds large, but a single job loss or major car repair without this buffer forces you into high-interest debt that undoes years of progress.

Start smaller if necessary-$1,000 or one month of expenses-then grow it monthly. Once your emergency fund reaches three months of expenses and high-interest debt is eliminated, redirect that same monthly amount toward investment accounts.

Open a 401(k) if your employer offers one and contribute enough to capture the full employer match-this is free money you’re leaving on the table otherwise. For 2026, the 401(k) contribution limit is $24,500 annually. If you’re self-employed or your employer lacks a plan, open a traditional or Roth IRA with a $7,500 annual limit for 2026.

Choose a Roth IRA if you expect higher tax rates in retirement; choose traditional if you want to reduce taxable income now. Invest these retirement funds in a diversified portfolio of low-cost index funds tracking the S&P 500 or total market rather than individual stocks or expensive actively managed funds. Index funds charge 0.03–0.20% in annual fees, while actively managed funds often charge 0.50–1.50% and rarely beat the market after fees. Over 30 years, this fee difference compounds into tens of thousands of dollars in your favor.

Align your investment risk level with your time horizon-aggressive stock-heavy portfolios for money you won’t touch for 20+ years, conservative bond-heavy allocations for money needed within 5 years. This approach protects you from forced selling during market downturns and maximizes growth when time works in your favor.

Financial planning adapts as your life changes, so you must review your progress quarterly and adjust your budget when spending patterns shift. Check your actual expenses against your plan each month, and recalculate your net worth annually to track whether you’re moving toward your goals. Life throws unexpected challenges-job changes, medical emergencies, market swings-and your plan must flex to handle them without falling apart.

Many people build a solid financial plan but fail to execute it because they lack clarity on their spending or miss opportunities to optimize their finances. At Clear View Business Solutions, we help individuals and small business owners simplify their finances through comprehensive accounting, bookkeeping, and tax planning services that reveal your true cash flow and tax situation. Visit Clear View Business Solutions to explore how we can support your financial stability and growth.

Start taking action today by calculating your net worth this week, opening a high-yield savings account for your emergency fund, or enrolling in your employer’s 401(k) to capture the full match. Small consistent actions compound into substantial wealth over time, and your financial future builds through disciplined execution of a realistic plan.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.