Retirement brings a shift in how you manage money. The decisions you make about withdrawals, investments, and estate planning directly impact how much you keep.

We at Clear View Business Solutions have seen firsthand how tax planning strategies for retirees can add thousands of dollars back to your pocket each year. This guide walks you through the specific moves that work.

Required minimum distributions start at age 73, and the IRS enforces this strictly. Miss a withdrawal and you face a 50% penalty on the amount you should have taken. At age 74 and beyond, the deadline for taking your RMD each year is December 31. If you delay that first withdrawal to April 1, you’ll owe two RMDs in the same year, which pushes your income higher and can bump you into a higher tax bracket. That’s a mistake we see repeatedly. The smarter move takes your first RMD by December 31 of the year you turn 73 to spread the tax impact across two years.

If you have multiple traditional IRAs, the IRS lets you aggregate them for RMD purposes, meaning you can take the total from one account instead of calculating RMDs separately. This flexibility matters because you can draw from whichever account has underperformed, leaving your best-performing investments untouched. The strategy protects your growth while satisfying IRS requirements.

Withdrawal sequencing determines how much you actually keep. Ordinary income from traditional IRAs and 401(k)s gets taxed at your full marginal rate, while long-term capital gains and qualified dividends get favorable rates of 0%, 15%, or 20% depending on your income level. If you’re in the 24% bracket, that difference cuts your tax bill significantly.

The number 0% seems to be not appropriate for this chart. Please use a different chart type. The IRS data from the 2024 filing season showed average refunds around $3,453, but that money was yours in the first place. Proper sequencing prevents overpaying.

Tap taxable brokerage accounts first since you’ve already paid taxes on the contributions. Next, draw from tax-deferred accounts to satisfy RMDs. Save Roth withdrawals for last since they’re tax-free and grow without requiring distributions.

Social Security taxation compounds this challenge. If your combined income hits $25,000 as a single filer or $32,000 for joint filers, up to 50% of benefits become taxable. If you’re filing single with more than $34,000 income, up to 85% of benefits may be taxable. Combined income includes adjusted gross income, nontaxable interest, plus half your Social Security benefits. Taking $10,000 from a traditional IRA could trigger taxation on $8,500 of your Social Security benefits. Taking $10,000 from a Roth doesn’t count toward this calculation at all.

The math is clear: structure your withdrawals to keep combined income below these thresholds when possible. This coordination between account types and Social Security creates the foundation for your overall withdrawal strategy, which then connects directly to how you position your investments across different account types for maximum tax efficiency.

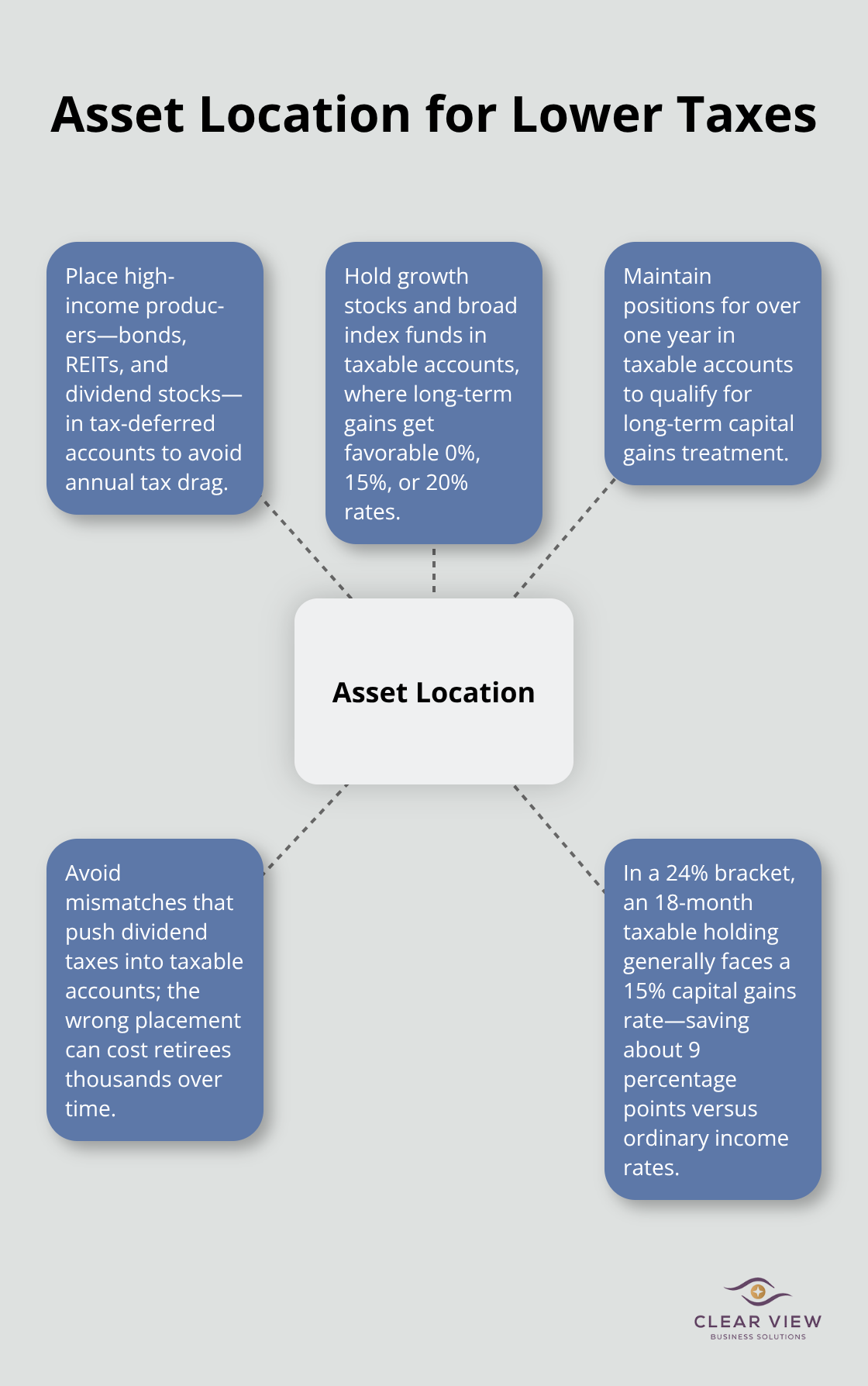

Your investment location matters as much as what you invest in. Holding dividend-paying stocks in a traditional IRA generates no immediate tax impact because the account is tax-deferred, but holding those same stocks in a taxable brokerage account triggers annual dividend taxes. This mismatch costs retirees thousands. Strategic asset location across account types helps lower your overall tax bill. Place high-income-producing investments like bonds, real estate investment trusts, and dividend stocks in tax-deferred accounts where they grow without annual tax drag. Meanwhile, growth stocks and index funds belong in taxable accounts because long-term capital gains receive favorable treatment at 0%, 15%, or 20% rates depending on your income level. When you hold an investment for more than one year before selling, the IRS taxes gains at these lower rates instead of ordinary income rates. A stock purchased in your taxable account and held for 18 months generates a 15% tax on gains if you’re in a 24% bracket, saving you 9 percentage points on every dollar of profit.

That difference compounds significantly over a retirement that spans decades.

Tax-loss harvesting transforms losses into tax advantages. Sell underperforming investments to realize losses that offset gains elsewhere or reduce ordinary income by up to $3,000 annually. If you sold a stock position with a $5,000 gain in your taxable brokerage account and another position shows a $3,000 loss, selling the loser wipes out the entire gain, saving roughly $450 in federal taxes at a 15% rate. Excess losses carry forward to future years indefinitely, creating a permanent tax benefit. The IRS requires a 30-day wash-sale period, meaning you cannot repurchase the same or substantially identical security within that window, but you can buy a similar investment immediately to maintain your desired allocation.

Holding investments for longer periods reduces tax drag from frequent trading, which academic research estimates costs investors roughly 1 to 3 percent annually in taxes. Tax-efficient ETF investments naturally minimize this drag because they trade infrequently and pass fewer taxable gains to shareholders compared to actively managed funds. Municipal bonds deserve a spot in taxable accounts too because their interest is exempt from federal income tax, making them particularly valuable when you’re in higher brackets.

Your dividend income strategy should distinguish between qualified and non-qualified dividends. Qualified dividends from U.S. corporations receive the favorable capital gains rates, while interest from bonds and non-qualified dividends face ordinary income tax rates. Timing dividend reinvestment and managing the size of positions in dividend-paying stocks helps control your taxable income in any given year, especially when you’re close to Social Security taxation thresholds or Medicare premium brackets (where even small income changes trigger higher costs). These positioning decisions set the stage for how you’ll coordinate your overall withdrawal strategy with your investment mix, which directly influences your ability to manage Social Security taxation and stay within favorable tax brackets throughout retirement.

Your estate planning decisions determine whether your heirs inherit wealth or inherit taxes. The federal estate tax exemption sits at $13.61 million for 2024, but this exemption drops to approximately $7 million in 2026 when provisions of the Tax Cuts and Jobs Act expire. If your estate approaches this threshold, the difference between proper planning and no planning is roughly 40% of your assets. This shift makes action urgent for anyone with substantial wealth.

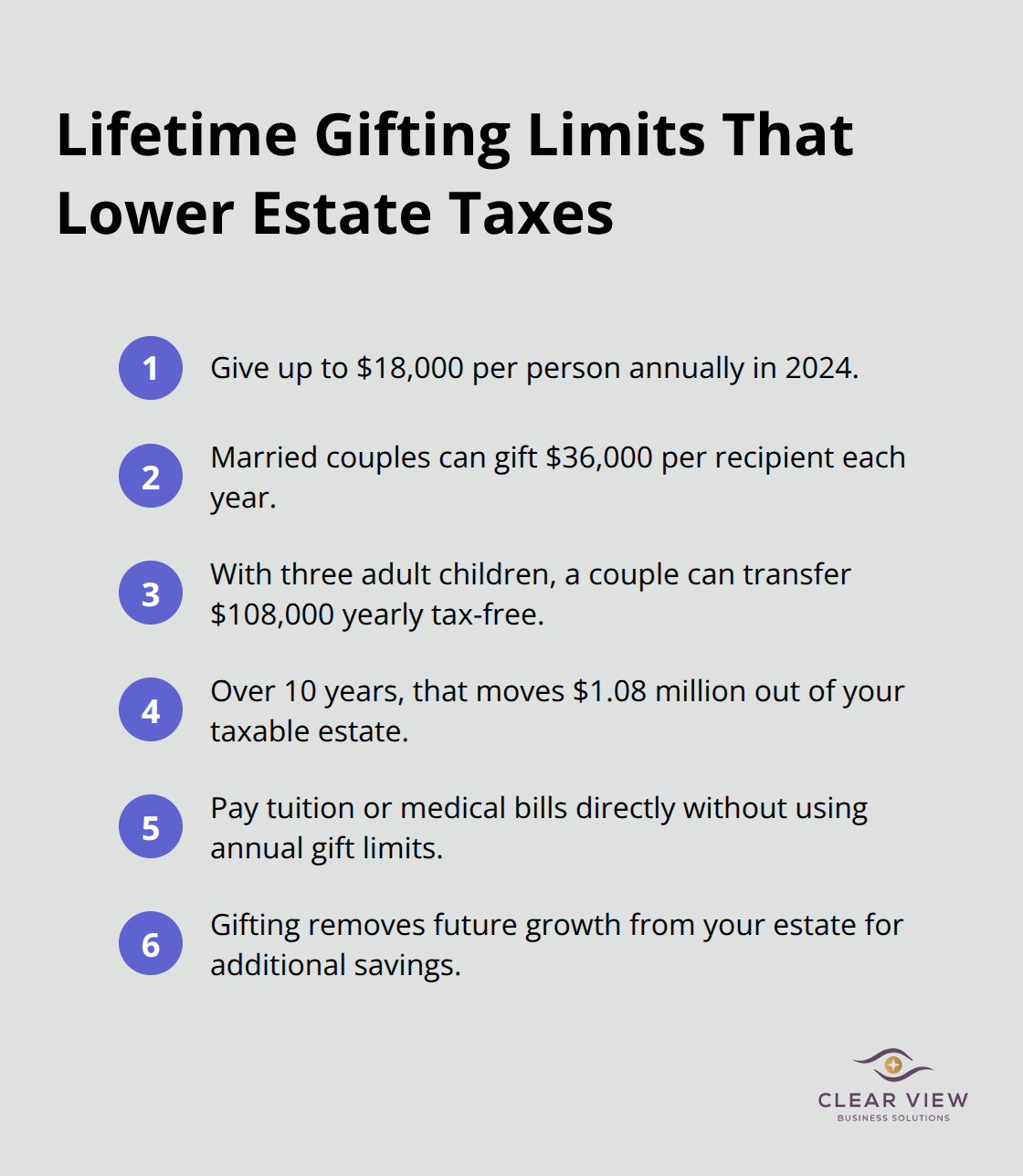

Gifting during your lifetime ranks among the most underused tax tools available. You can give up to $18,000 annually per person in 2024 without triggering gift tax or reducing your lifetime exemption, and married couples can double this to $36,000 per recipient. If you have three adult children, you and your spouse can transfer $108,000 yearly tax-free. Over ten years, that amounts to $1.08 million moved out of your taxable estate while you’re alive to see it benefit your family.

The IRS allows direct payment of medical bills and tuition for others without counting against gift limits, making this strategy particularly powerful for families with significant healthcare or education expenses. Strategic gifting also removes future growth from your estate-if you gift $36,000 that grows to $60,000 over a decade, your heirs keep all $24,000 of growth tax-free.

Beneficiary designations override your will entirely, making them critical to review after major life changes like marriage, divorce, or the birth of grandchildren. Many retirees carry outdated designations listing ex-spouses or deceased beneficiaries, which forces assets through probate and creates unnecessary delays and costs. Roth IRAs and Roth 401(k)s offer exceptional estate planning advantages because withdrawals by heirs are tax-free if the five-year rule is satisfied, whereas traditional IRA beneficiaries face immediate income tax on distributions. This distinction alone can save your heirs tens of thousands in taxes.

Charitable giving through qualified charitable distributions from your IRA after age 73 accomplishes multiple goals simultaneously. You can transfer up to $100,000 annually directly to charities, and this amount counts toward satisfying your required minimum distribution without increasing your taxable income. If you’re in the 24% bracket, a $50,000 qualified charitable distribution saves roughly $12,000 in federal taxes while supporting causes you care about. For non-itemizers in 2026, the new charitable deduction allows up to $1,000 for single filers and $2,000 for married couples filing jointly without itemizing, creating tax relief for those who give but don’t exceed standard deduction thresholds. Charitable remainder trusts offer another avenue for those with appreciated assets, allowing you to donate property while receiving income during your lifetime and leaving the remainder to charity, while also generating an immediate charitable deduction. These strategies work together to reduce estate taxes while ensuring your wealth flows to your intended recipients efficiently.

Tax planning strategies for retirees work because they address the specific income sources and account types you control. The moves outlined in this guide-managing required minimum distributions, sequencing withdrawals strategically, positioning investments for tax efficiency, and structuring your estate-all reduce what you owe while keeping more money in your pocket. A retiree in the 24% bracket who coordinates Social Security withdrawals with Roth distributions instead of traditional IRA withdrawals avoids taxation on thousands of dollars in benefits annually, while another who positions dividend stocks in tax-deferred accounts and growth stocks in taxable accounts saves roughly 1 to 3 percent annually in tax drag.

Your situation is unique because your income sources, account balances, family structure, and charitable goals differ from everyone else’s. The timing of Social Security, the size of your required minimum distributions, your state of residence, and your health care costs all influence which strategies deliver the biggest benefit for your specific circumstances. A tax strategy that works perfectly for one retiree may create problems for another, which is why personalized planning matters more than following generic advice.

We at Clear View Business Solutions help retirees navigate these decisions with comprehensive tax planning tailored to your situation. Our team handles the analysis, coordinates your withdrawal strategy, and identifies opportunities you might otherwise miss. Contact us today to discuss how tax planning can work for your retirement.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2025 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.