Retirement tax planning isn’t optional-it’s the difference between keeping more of your money and handing it to the IRS. Most retirees leave thousands on the table each year by missing straightforward tax strategies.

We at Clear View Business Solutions have seen firsthand how the right approach transforms retirement finances. This guide walks you through the tactics that actually work.

Your retirement income doesn’t arrive from a single source, and how you manage each stream determines whether the IRS takes 20% or 40% of your money. Social Security, pensions, investment withdrawals, and annuities stack together in ways that trigger taxes you might not expect. The worst part: most retirees discover this stacking problem too late, after they’ve already locked in a higher tax bracket for the year.

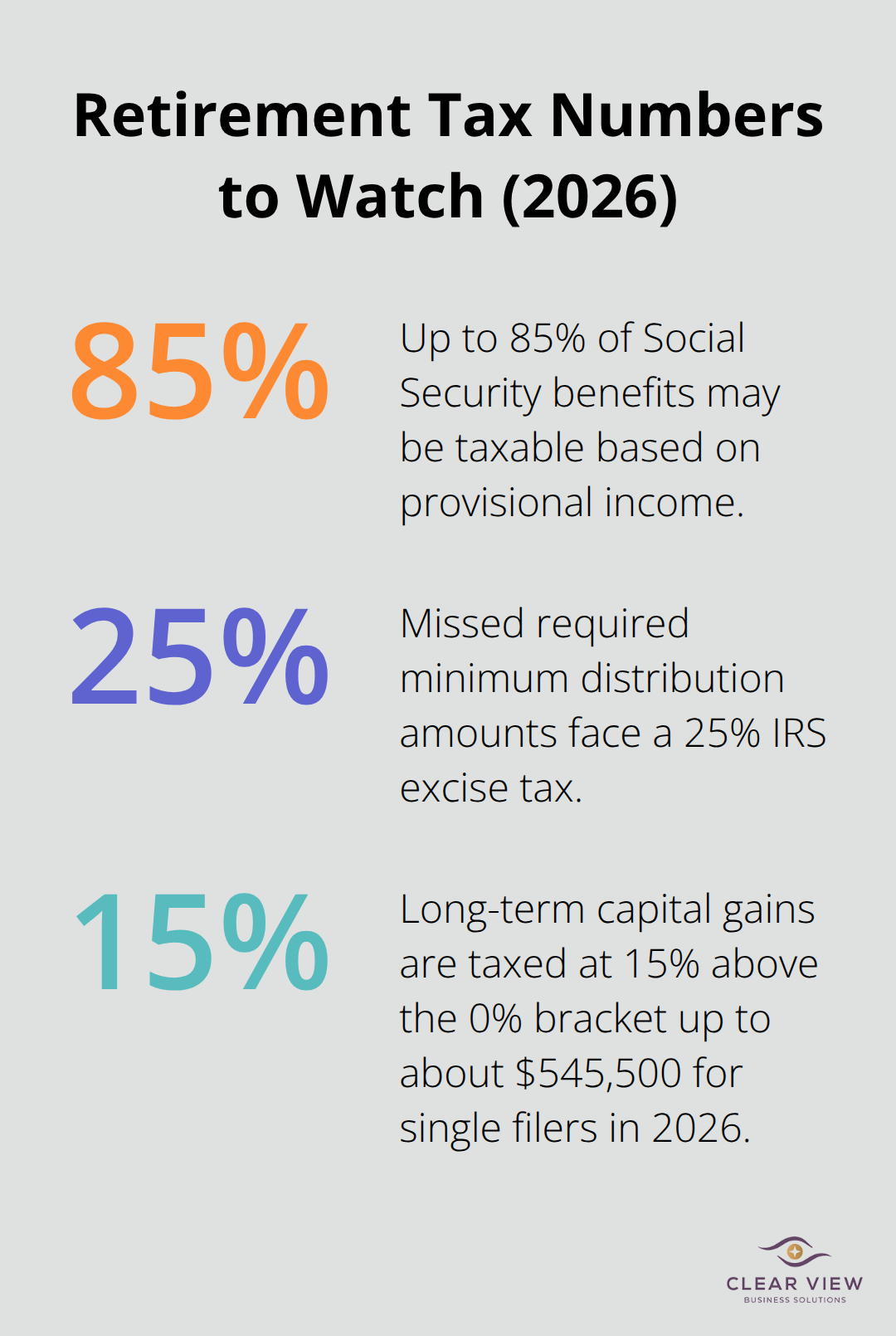

Social Security becomes taxable once your provisional income exceeds $25,000 for single filers or $32,000 for joint filers, and up to 85% of your benefits can be subject to federal income tax depending on how high that number climbs. A $30,000 pension combined with $20,000 in IRA withdrawals and $15,000 in Social Security can push you into a situation where more than half your Social Security gets taxed as ordinary income. The IRS doesn’t care that you earned that Social Security decades ago-it cares about your total income sources right now.

Pension income and investment withdrawals don’t just add to your tax bill; they actively push more of your Social Security into taxable territory. A retiree with a $40,000 pension, $25,000 in 401(k) withdrawals, and $20,000 in Social Security might find that $17,000 of the Social Security becomes taxable, turning what feels like tax-free income into ordinary income.

The solution isn’t to avoid withdrawals-you need that money to live-but to coordinate the timing and sources. Roth IRA withdrawals don’t count toward provisional income, making them invisible to the Social Security tax calculation. If you have a Roth IRA available, pull from it strategically in high-income years to shield your Social Security from taxation. Traditional IRA and 401(k) withdrawals, by contrast, add directly to provisional income and accelerate the taxation of benefits. For married couples, delaying one spouse’s Social Security while the other takes benefits early sometimes reduces overall household taxation because you can control which years have large withdrawals.

Unlike retirement account withdrawals, pension and annuity payments arrive on a fixed schedule whether you need the money or not. This creates a permanent baseline income that compounds other tax problems. A $3,000 monthly pension means $36,000 hits your tax return every year, regardless of market performance or other income. If you also have required minimum distributions starting at age 73, you’re forced to take even more, potentially pushing yourself into the 22% or 24% federal bracket when you could have stayed in the 12% bracket with better planning.

If you have a choice about pension payout options before retirement, compare the lump sum versus monthly payments with a tax professional. A lump sum gives you control over withdrawal timing and can be rolled into an IRA, where you manage the tax impact year by year. Monthly pension payments lock you into a fixed income stream that will interact with Social Security and other withdrawals in ways you can’t adjust.

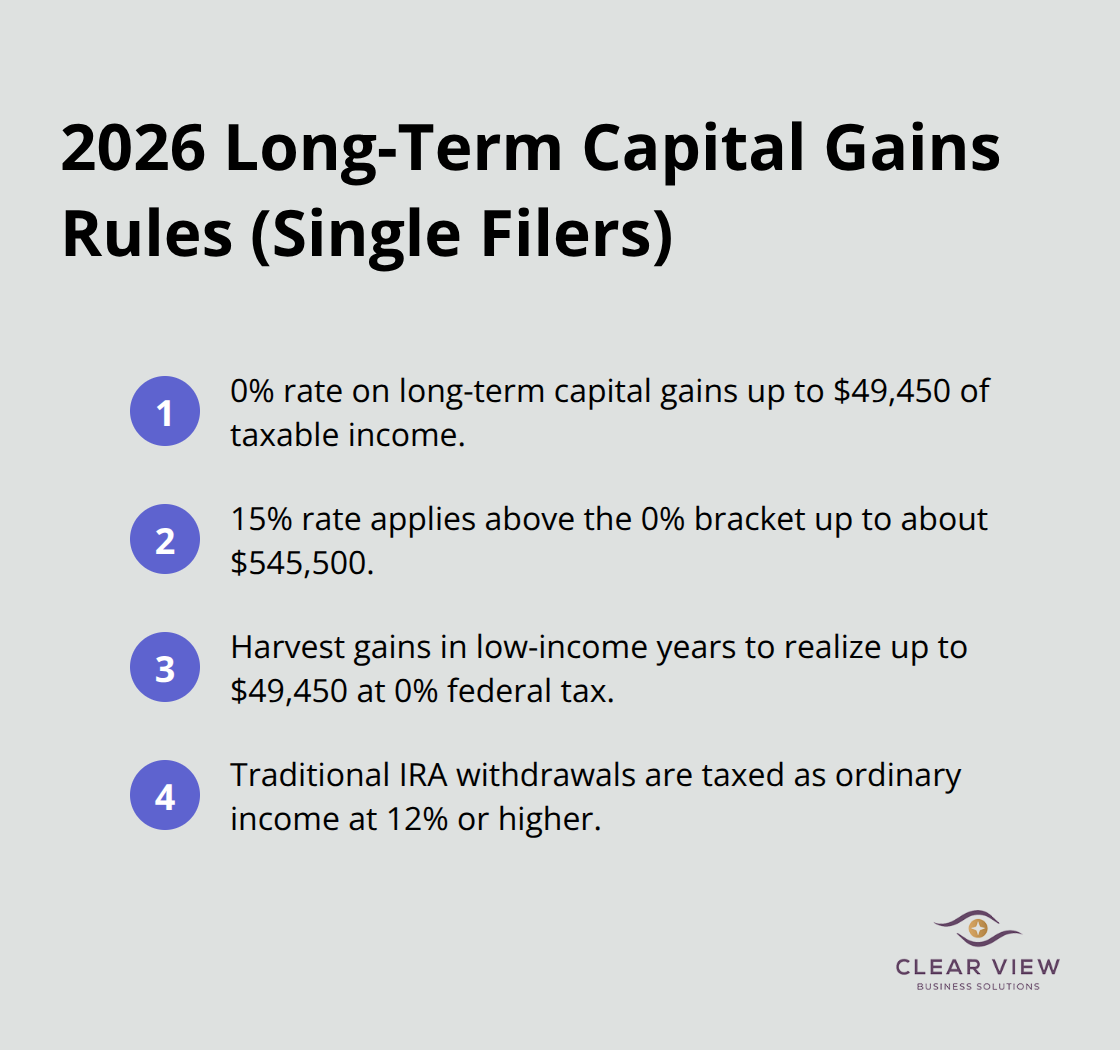

Taxable investment accounts, IRAs, and Roth accounts should never be withdrawn in the same order every year. Long-term capital gains in a taxable brokerage account are taxed at preferential rates-0% up to $49,450 of taxable income for single filers in 2026, then 15% up to about $545,500. This means you can harvest $49,450 of capital gains in a low-income year without owing federal tax, while withdrawing the same amount from a traditional IRA would be taxed as ordinary income at 12% or higher.

In years when your pension and Social Security total less than usual, or you’ve taken a smaller RMD, use that tax room to realize capital gains from your taxable account. In years when you’re forced to take large RMDs, pull from Roth accounts instead to keep your taxable income down. This sequencing strategy can reduce lifetime taxes by 45% compared to simply withdrawing from accounts in the order you opened them, according to Fidelity’s analysis of proportional withdrawal strategies. The right withdrawal order transforms how much money actually stays in your pocket-which makes the next step, understanding required minimum distributions, essential to your overall plan.

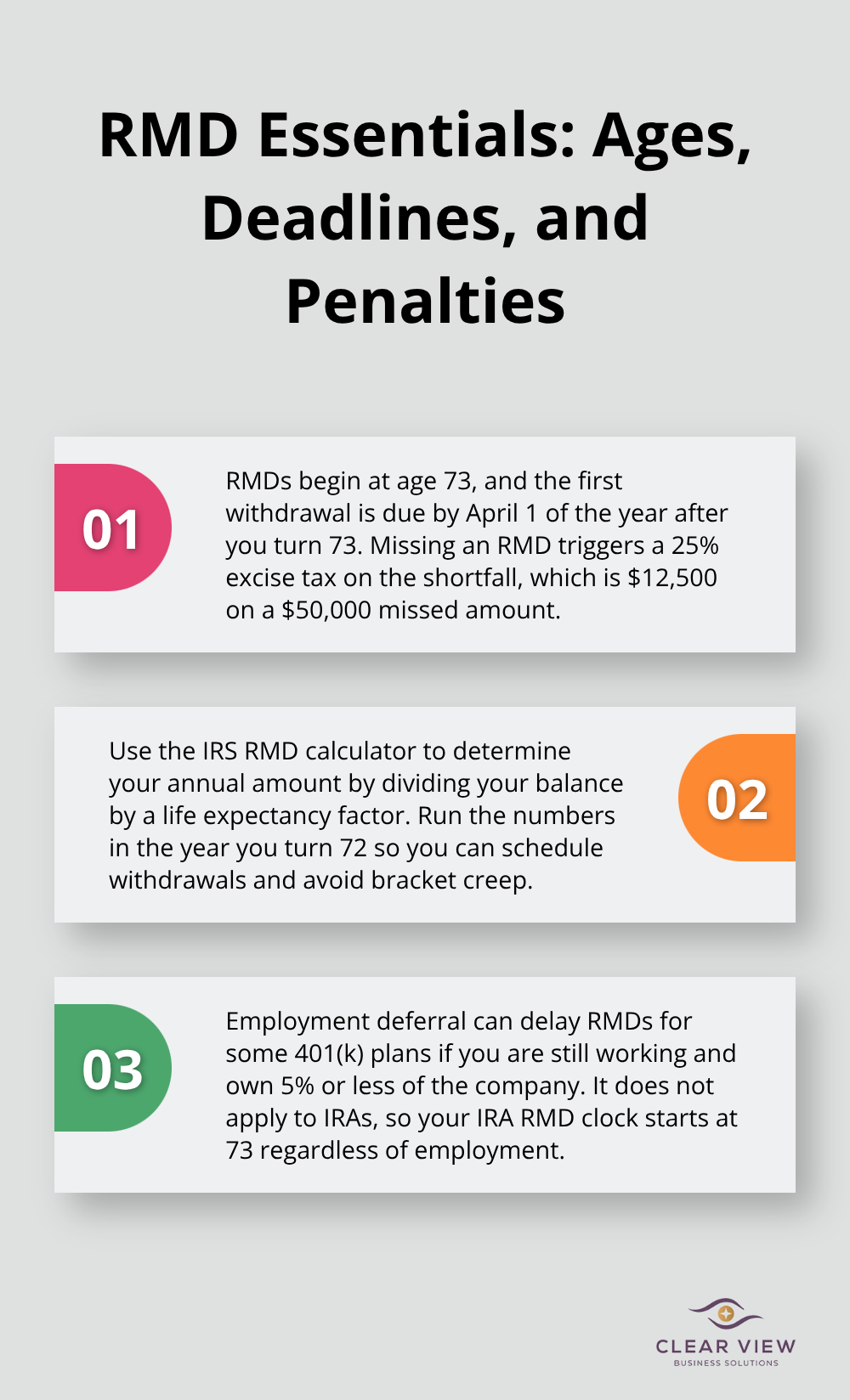

Required minimum distributions start at age 73, and the IRS imposes a severe penalty for missing one: a 25% excise tax on the amount not distributed. A missed $50,000 RMD costs you $12,500 in penalties before you even owe income tax on the money. The IRS RMD calculator determines your exact withdrawal amount by dividing your account balance by a life expectancy factor. You must take the first RMD by April 1 of the year after you turn 73.

Most retirees who miss RMDs do so because they didn’t realize the deadline applied to them or thought they could delay by staying employed.

Employment deferral works for 401(k) plans if you still work and don’t own more than 5% of the company, but it does not work for IRAs. The moment you turn 73, your IRA RMD clock starts ticking regardless of your employment status. Plan ahead using the IRS calculator in the year you turn 72 so you know exactly what you owe and can structure your withdrawals to minimize tax bracket creep.

The years between retirement and age 73 represent your last chance to move money from traditional accounts to Roth accounts at rates you control. Once RMDs begin, you face forced taxable withdrawals whether you need the money or not, which limits your ability to convert at lower tax rates. A 65-year-old in the 12% tax bracket can convert $50,000 per year for eight years, moving roughly $400,000 to tax-free status before RMDs arrive. After age 73, that same conversion would push taxable income higher and trigger larger RMDs in future years, making the tax cost much steeper.

The math works best in years when your income naturally dips, such as the first year of retirement before pension payments start or after a market downturn reduces investment income. Roth conversions are not mandatory, but the window to execute them cheaply closes the moment RMDs begin. If you have both traditional and Roth accounts, converting portions of the traditional balance now locks in lower tax rates on future growth and reduces the RMD burden that will compound later.

If you’re age 70½ or older and charitably inclined, qualified charitable distributions allow you to transfer up to $111,000 directly from your IRA to a qualified charity in 2026. This distribution counts toward your RMD requirement but does not increase your taxable income, which means it avoids triggering higher Medicare premiums, higher Social Security taxation, or higher capital gains rates. A retiree who needs to take a $50,000 RMD can direct that money straight to their favorite charity, satisfy the RMD requirement, and keep taxable income $50,000 lower than if they took the distribution to their bank account.

QCDs cannot be claimed as itemized deductions, so they work best for retirees who take the standard deduction anyway. If you’re charitably generous, QCDs transform your RMDs from a tax problem into a tax solution that aligns your required withdrawals with your values. The IRS limits QCDs to $111,000 per person per year, and the money must transfer directly from the IRA custodian to the charity. Coordinate with your IRA provider early to ensure the transaction processes before your RMD deadline, and you’ll move into the next critical phase of retirement tax planning: managing the interaction between your withdrawals and Social Security taxation.

Medicare premiums rise automatically when your income climbs, and most retirees fail to realize how a single withdrawal decision triggers thousands in additional charges. The IRS uses Modified Adjusted Gross Income Medicare surcharges to calculate Medicare Part B and Part D surcharges, and even $1 of excess income can push you into a higher premium bracket. A 65-year-old retiree in 2026 pays the standard Part B premium of $202.90 per month, but if MAGI exceeds $97,000, that same premium jumps to $245.90. At $194,000 of MAGI, the premium reaches $385.80 monthly-more than double the base rate.

These surcharges persist for two years after the income spike occurs, so a large withdrawal in year one continues draining your bank account in year two. The solution is straightforward: structure withdrawals to keep MAGI below critical thresholds. If you approach $97,000 in MAGI, stop taking IRA distributions and pull from a Roth account instead, which does not count toward MAGI. If you near $194,000, the tax savings from staying below that threshold often exceed the benefit of taking a larger withdrawal.

State income tax compounds the Medicare problem because nine states charge no income tax whatsoever, while others tax retirement income heavily. Moving from California to Nevada eliminates the 9.3% state income tax on IRA and pension withdrawals permanently, saving a retiree with $60,000 in annual withdrawals roughly $5,580 per year. If you fall within five years of retirement, consult with a tax professional about whether relocation makes financial sense before you lock yourself into a permanent tax residency. The decision to relocate affects not just current taxes but also your long-term Medicare costs and Social Security taxation.

Charitable giving offers a tax strategy that most retirees ignore until they retire and the opportunity has passed. Donor-advised funds let you bunch deductions into one year, claim a large tax deduction immediately, and then distribute the money to charities over several years. A retiree who donates $25,000 to a donor-advised fund in a high-income year captures a $25,000 deduction that might save $6,000 in federal taxes at the 24% bracket, even though the actual charity distributions happen later when income is lower. This strategy works because the deduction occurs in the year you fund the account, not when the charity receives the money.

If you hold appreciated securities in a taxable brokerage account, donate those directly to charity instead of selling them and donating the cash. You avoid capital gains tax on the appreciation, receive a full fair-market-value deduction, and the charity receives the full value without paying taxes. A retiree with $30,000 in unrealized gains on company stock can donate the shares, claim a $30,000 deduction worth roughly $7,200 in tax savings at the 24% bracket, and avoid the $4,500 capital gains tax that would have hit if they sold first.

The combination of qualified charitable distributions RMD from IRAs at age 70½ and strategic giving through donor-advised funds transforms charitable intent from an afterthought into a centerpiece of your tax plan. A retiree who needs to take a required minimum distribution can direct that money straight to their favorite charity, satisfy the RMD requirement, and keep taxable income lower than if they took the distribution to their bank account. This approach works best for retirees who take the standard deduction anyway, since QCDs cannot be claimed as itemized deductions. The IRS limits QCDs to $100,000 per person per year, and the money must transfer directly from the IRA custodian to the charity.

Retirement tax planning transforms what feels like a fixed tax bill into a series of decisions you control. The strategies in this guide-coordinating Social Security with withdrawals, timing Roth conversions before RMDs arrive, directing charitable gifts through QCDs, and managing state tax exposure-reduce what retirees actually owe by thousands of dollars annually. Your retirement income sources interact in ways the IRS rewards you for managing well and punishes you for ignoring.

A $50,000 withdrawal looks identical on paper, but its tax impact swings wildly depending on whether it comes from a Roth account, a taxable brokerage account, or a traditional IRA. The difference between a smart withdrawal sequence and a careless one compounds over decades, potentially adding or subtracting hundreds of thousands from your lifetime after-tax income. Personalized tax planning matters because your situation is unique-your pension amount, Social Security claiming age, account balances, state of residence, and charitable goals create a specific tax picture that generic advice cannot address.

We at Clear View Business Solutions help individuals navigate these decisions with tax planning that accounts for your complete financial picture. Contact Clear View Business Solutions to build a retirement tax plan tailored to your circumstances and ensure you keep more of what you’ve earned.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2933 N Campbell Avenue, Tucson, AZ 85719

© 2026 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.