Most small business owners focus on sales and growth, but weak accounting practices quietly drain profits and create legal headaches. At Clear View Business Solutions, we’ve seen firsthand how poor record-keeping leads to missed deductions, cash flow problems, and costly mistakes during tax season.

The good news: solid small business accounting doesn’t require an accounting degree. You just need the right systems, consistent habits, and knowledge of what actually matters.

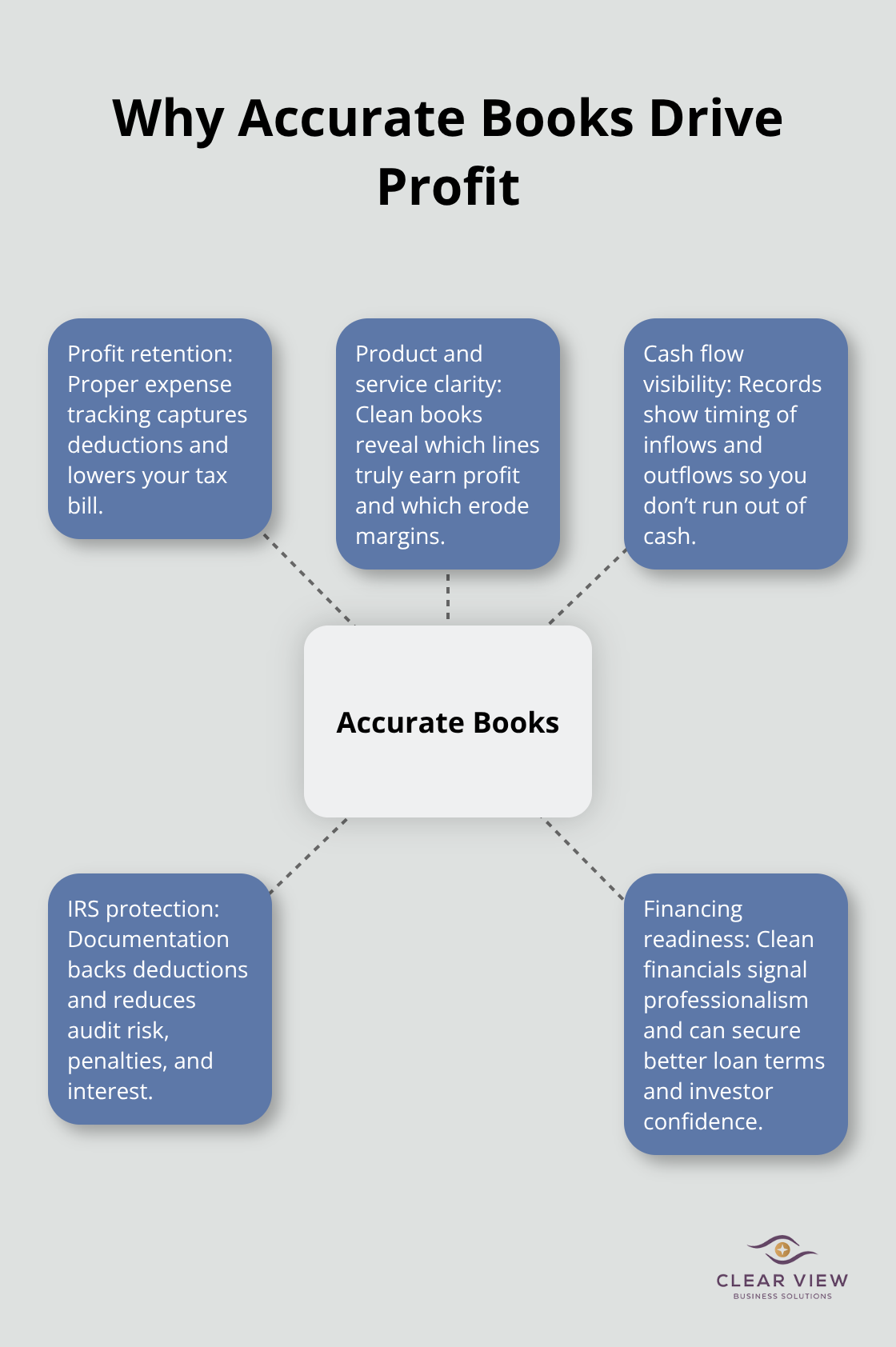

Accurate accounting directly determines how much profit you actually keep. When you fail to track expenses properly, you miss deductions that could reduce your tax bill by thousands. A business owner we know spent $8,000 on equipment but failed to document it, losing the depreciation benefit worth roughly $1,600 over five years. Without clean books, you cannot tell which products or services are actually profitable. You might think a product line is thriving when it actually drags down your margins.

The moment you have real numbers, you can make decisions based on facts instead of guesses.

Accurate records reveal cash flow problems before they become emergencies. If you do not track when money comes in versus when it goes out, you could have profitable sales on paper but run out of cash to pay suppliers. This kills businesses faster than anything else. Many owners focus on revenue and ignore the timing of payments, which creates a false sense of security. You need visibility into both your profitability and your liquidity to survive.

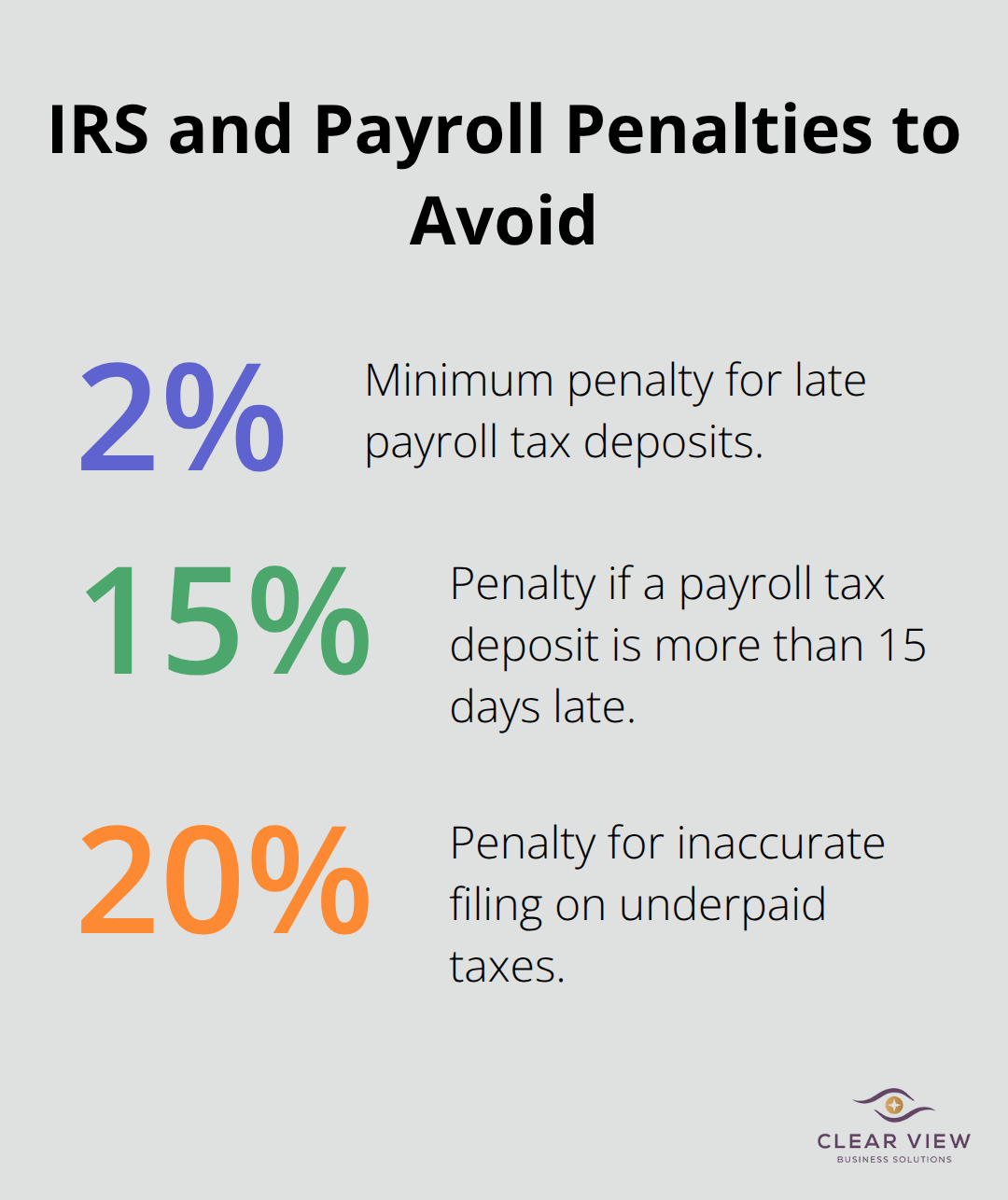

The IRS does not care about your intentions-it cares about your records. If you face an audit and cannot back up your deductions with receipts and documentation, you lose them. The average small business audit costs $3,000 to $5,000 in professional fees alone, not counting penalties and interest on unpaid taxes. Penalties for inaccurate filing can reach 20% of underpaid taxes, and if the IRS suspects fraud, criminal prosecution becomes possible. Maintaining organized records takes a few hours per month but saves you from catastrophic consequences.

Banks and investors want to see clean books before they lend you money or invest in your business. A lender reviewing your financials will immediately spot sloppy accounting and either deny your application or charge higher interest rates. If your books are tight, you get better terms. Sloppy records signal poor management to anyone evaluating your creditworthiness or investment potential. Clean accounting demonstrates that you run a professional operation.

With the right systems in place, you can produce accurate financial statements that support both compliance and growth. The next step is choosing the tools and structures that make this possible without consuming your entire week.

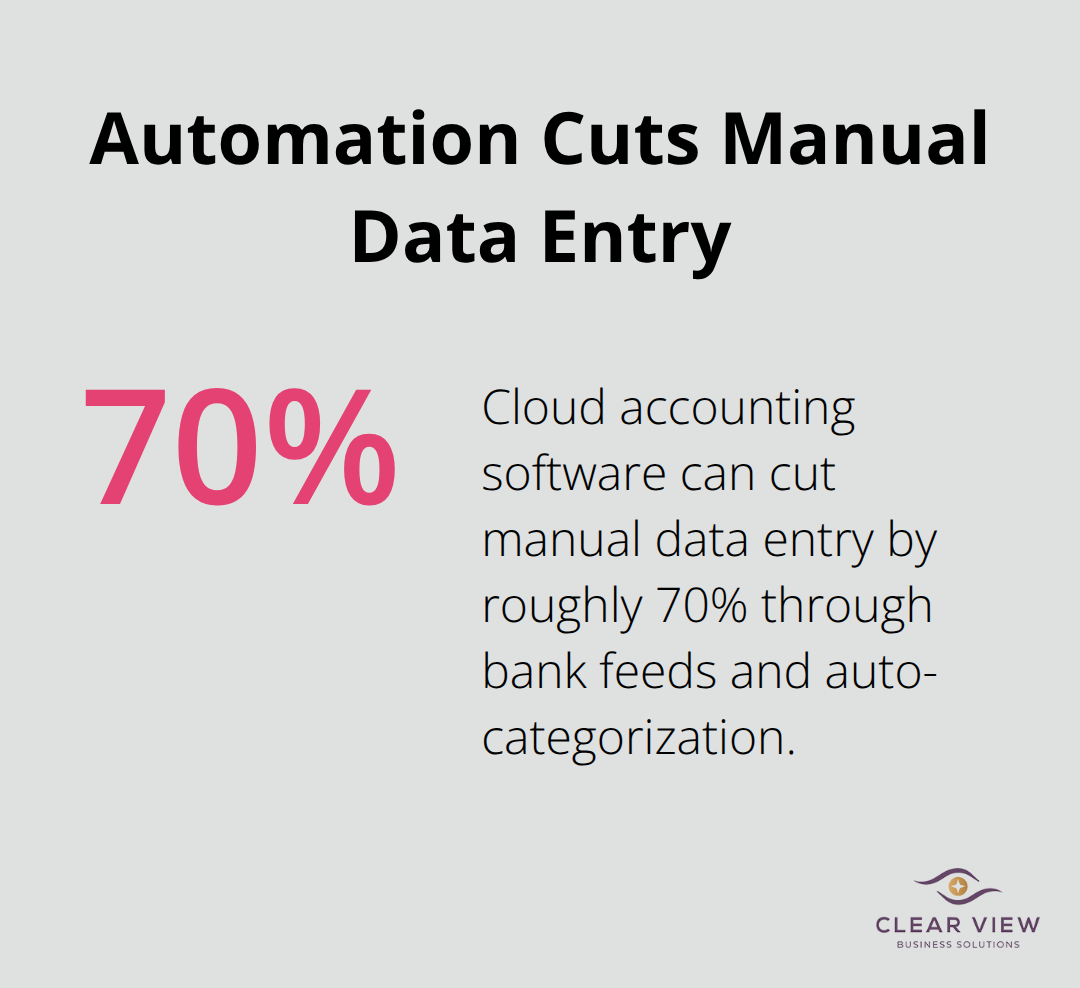

The tools you select determine whether accounting feels like a burden or a natural part of running your business. Cloud-based accounting software outperforms spreadsheets and outdated desktop programs for most small businesses. QuickBooks Online, Xero, and FreshBooks integrate with your bank accounts, automatically categorizing transactions and cutting manual data entry by roughly 70%. This matters because less time spent on data entry means more time analyzing what the numbers actually mean. When selecting software, prioritize one that connects directly to your business bank account and offers mobile access so you can log expenses on the spot.

Most small business owners choose based on price alone, but a $30 per month tool that saves you five hours weekly beats a $10 tool that requires manual uploads. Start with the software’s free trial and test it with your actual transactions before committing.

Your chart of accounts forms the skeleton of everything that follows. Rather than using the software’s default chart, customize it to match how you actually run your business. If you sell both products and services, separate those revenue streams so you can see which generates more profit. If you have multiple locations or sales channels, create accounts for each one. A restaurant owner kept all expenses in one account and had no idea whether their lunch service or dinner service was more profitable. Once they split expenses by service period, they discovered lunch was barely breaking even and adjusted pricing accordingly. The chart of accounts should contain roughly 30 to 50 accounts for a typical small business, organized into five categories: assets, liabilities, equity, revenue, and expenses. Too few accounts and you lose visibility; too many and you waste time categorizing transactions.

Paper receipts and digital chaos destroy accounting accuracy faster than any software limitation. Implement a system immediately, whether that means a filing cabinet with labeled folders or a receipt scanning app like Expensify or Receipt Bank. The key is capturing documentation the day the transaction happens, not three months later. Banks and the IRS require you to keep records for at least three years, and if you face an audit, missing receipts mean lost deductions. Store digital copies in cloud storage with a backup so a computer crash does not wipe out your records. The IRS does not accept memory as proof-a receipt showing the vendor, date, and amount is non-negotiable. Set a weekly routine, even if it takes just 30 minutes, to upload receipts and reconcile your accounts. This prevents the nightmare of discovering three months of unreconciled transactions right before tax season.

Monthly bank reconciliation catches errors before they compound and protects you from fraud. Your bank statement should match your accounting software exactly. If it does not, investigate the discrepancy immediately rather than assuming the software is correct. This step takes an hour or two each month but reveals problems that compound into serious issues. Once your foundation is solid, the next step involves mastering the specific accounting tasks that keep your business running smoothly.

Monthly bank reconciliation is not optional, and treating it as a tedious chore costs you money. Most small business owners reconcile their accounts quarterly or only when something feels wrong, which means errors compound for months before discovery. Your accounting software records what you think happened, but your bank statement shows what actually happened. These two must match exactly every single month.

Start by downloading your bank statement and comparing each transaction to your software. Look for timing differences first-payments you recorded in January might not clear the bank until February, which is normal. Flag anything else immediately. A business owner discovered their bookkeeper had been recording personal withdrawals as business expenses, stealing roughly $2,000 per month. Without monthly reconciliation, this continued for eight months.

Set aside one hour on the same day each month, usually the first business day after your bank closes the previous month. If reconciliation takes longer than an hour, your chart of accounts needs simplification or your transaction volume requires professional help.

Accurate income and expense tracking requires you to record every dollar the moment it enters or leaves your business, not wait until you have time to organize receipts. Many owners use multiple payment methods-personal credit cards, business accounts, cash, digital wallets-which creates chaos during tax season. The solution is harsh but necessary: use one business bank account and one business credit card exclusively for business transactions. Stop mixing personal and business money.

When you separate accounts completely, your accounting software can automatically import transactions from your bank, eliminating manual data entry and the errors that follow. Categorize expenses the same way every single time. If you purchase office supplies on Monday and categorize it as Office Supplies, do not categorize the same purchase as Equipment on Thursday. Inconsistent categorization destroys your ability to see spending patterns and identify where your money actually goes.

Track expenses by category weekly rather than monthly, which prevents the backlog that causes mistakes. This habit takes 20 minutes per week and saves hours of confusion later.

Payroll demands even more attention because mistakes trigger IRS penalties and employee frustration. Calculate gross pay, deduct federal and state income taxes, Social Security, Medicare, and any voluntary deductions like health insurance or retirement contributions. Federal payroll taxes must be deposited on specific schedules-either semi-weekly or monthly depending on your total tax liability.

Missing a payroll tax deposit results in penalties starting at 2% and climbing to 15% if the deposit is more than 15 days late. Use payroll software rather than calculate manually, which eliminates math errors and automatically handles tax deposits and filings. If you have employees in multiple states, state payroll taxes vary significantly, making software essential.

Keep detailed payroll records for at least three years, including timesheets, tax withholdings, and deposit confirmations. The IRS audits payroll records more frequently than other areas because penalties generate substantial revenue for the government.

Solid small business accounting rests on three fundamentals: using the right software, maintaining consistent records, and reconciling your accounts monthly. These practices eliminate guesswork, protect you during audits, and give you the financial clarity needed to make smart decisions. When you track income and expenses accurately, manage payroll correctly, and keep documentation organized, your books become a reliable source of truth instead of a source of stress.

The benefits compound over time. Clean books mean lower tax bills through proper deductions, faster loan approvals with better terms, and the confidence that comes from knowing your actual profitability. You avoid costly mistakes, catch fraud early, and demonstrate professionalism to anyone evaluating your business. Most importantly, accurate accounting frees you to focus on growth instead of scrambling to find receipts or reconcile mysterious discrepancies.

Many small business owners reach a point where managing accounting alone becomes impractical. If you find yourself overwhelmed, spending hours on bookkeeping instead of building your business, or uncertain whether your records are audit-ready, Clear View Business Solutions provides full-cycle bookkeeping, QuickBooks training, tax planning, and IRS representation specifically designed for small businesses and startups in Tucson. The right accounting partner removes the burden and ensures compliance while maximizing your tax benefits.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there.

Northwest Location:

7530 N. La Cholla Blvd., Tucson, AZ 85741

Central Location:

2929 N Campbell Avenue, Tucson, AZ 85719

© 2025 Clear View Business Solutions. All Rights Reserved.

At Clear View Business Solutions, we know you want your business to prosper without having to worry about whether you are paying more in taxes than you should or whether your business is set up correctly. The problem is it's hard to find a trusted advisor who can translate financial jargon to layman's terms and who can actually help you plan for better results.

We believe it doesn't have to be this way! No business owner should settle for working with a CPA firm that falls short of understanding what you want to achieve and how to help you get there. With over 20 years of experience serving hundreds of business owners like you, our team of experts combines financial expertise and proactive communication with our drive to help each client achieve results and have fun along the way.

Here's how we do it:

Discover: We start with a consultation to understand your specific goals, what's holding you back, and what success looks like for you.

Strategize & Optimize: Together, we design a customized strategy that empowers you to progress toward your goals, and we optimize our communication as partners.

Thrive: You enjoy a clear view of your business and your financial prosperity.

Schedule a consultation today, and take the first step toward being able to focus on your core business again without wondering if your numbers are right- or what they mean to your business.

In the meantime, download, "The Business Owner's Essential Guide to Tax Deductions" and make sure you aren't leaving money on the table.